Optical Fiber Fusion Splicer Market

Optical Fiber Fusion Splicer Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707740 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

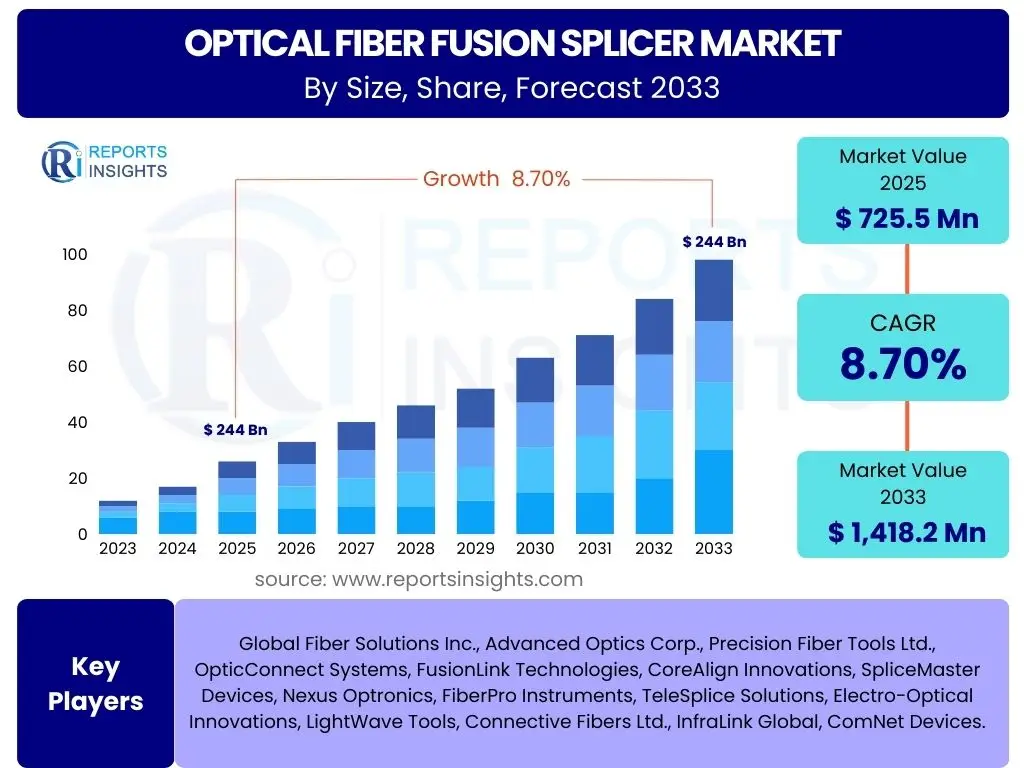

Optical Fiber Fusion Splicer Market Size

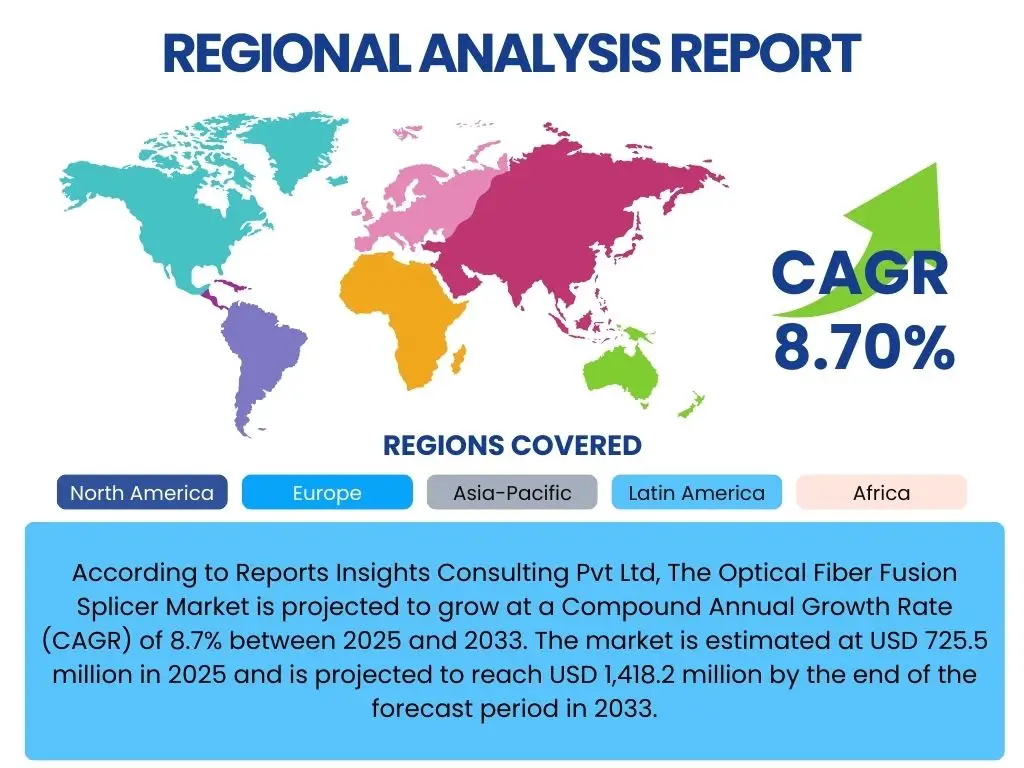

According to Reports Insights Consulting Pvt Ltd, The Optical Fiber Fusion Splicer Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033. The market is estimated at USD 725.5 million in 2025 and is projected to reach USD 1,418.2 million by the end of the forecast period in 2033.

The consistent growth trajectory of the optical fiber fusion splicer market is primarily attributed to the global surge in demand for high-speed data connectivity. The expansive rollout of 5G networks, coupled with the ongoing deployment of Fiber-to-the-Home (FTTH), Fiber-to-the-Curb (FTTC), and Fiber-to-the-Building (FTTB) infrastructure, necessitates extensive optical fiber installation and maintenance. These developments are critical in both urban and increasingly, rural areas, where digital inclusion initiatives are gaining momentum.

Furthermore, the proliferation of cloud computing, big data analytics, and the Internet of Things (IoT) demands robust and reliable network backbones, driving the need for precision fiber optic connectivity. Fusion splicers are indispensable tools for achieving low-loss, high-strength splices, which are crucial for maintaining signal integrity over long distances and across complex network architectures. This technological reliance ensures a stable and growing demand for these sophisticated devices throughout the forecast period.

Key Optical Fiber Fusion Splicer Market Trends & Insights

Users frequently inquire about the evolving landscape of optical fiber fusion splicing technology, focusing on how advancements are shaping market dynamics, improving efficiency, and addressing emerging network demands. Common themes include the impact of 5G and FTTx deployments, the increasing need for automation, portability, and user-friendliness in splicing equipment, and the integration of smart features for enhanced performance and diagnostics. There is also significant interest in solutions that reduce operational costs and accelerate deployment times, reflecting a market moving towards more efficient and resilient fiber optic infrastructure.

- Increased demand for ruggedized and portable splicers suitable for field deployment in diverse environments, driven by widespread FTTH and 5G rollouts.

- Growing adoption of automation and artificial intelligence (AI) features in splicers for improved accuracy, reduced splicing time, and automated fault detection.

- Emphasis on enhanced battery life and faster splicing cycles to boost operational efficiency and productivity for technicians.

- Integration of cloud connectivity and IoT capabilities for remote monitoring, data logging, and predictive maintenance of splicing equipment.

- Development of specialized splicers for various fiber types, including bend-insensitive fibers and specialty fibers used in industrial and medical applications.

- Rising focus on training and certification programs to address the skilled labor shortage in optical fiber installation and maintenance.

AI Impact Analysis on Optical Fiber Fusion Splicer

Common user questions regarding AI's impact on optical fiber fusion splicers often revolve around how artificial intelligence can enhance the precision, speed, and reliability of splicing operations, as well as its potential for predictive maintenance and remote diagnostics. Users are keen to understand if AI can automate complex decision-making during the splicing process, reduce human error, and provide real-time feedback on splice quality. There is also interest in AI's role in optimizing network performance through intelligent data analysis derived from splicing operations and equipment usage patterns, ultimately leading to more robust and efficient fiber optic deployments.

- AI-powered image recognition for precise fiber core alignment, minimizing splice loss and enhancing splice quality by intelligently identifying fiber types and potential defects.

- Predictive maintenance algorithms for fusion splicers, using AI to analyze usage patterns and operational data to forecast equipment failures, schedule maintenance, and reduce downtime.

- Automated optimization of splicing parameters based on environmental conditions and fiber characteristics, allowing the splicer to adapt autonomously for optimal performance.

- Real-time splice quality analysis and feedback systems, leveraging AI to immediately detect imperfections and guide technicians for corrective actions, thereby reducing reworks.

- Integration of AI with cloud platforms for comprehensive data analytics on splicing operations, enabling insights into project progress, technician performance, and network health.

Key Takeaways Optical Fiber Fusion Splicer Market Size & Forecast

The primary insights from the optical fiber fusion splicer market size and forecast indicate a robust and sustained growth trajectory, largely propelled by fundamental shifts in global digital infrastructure. Stakeholders consistently seek clarity on the driving forces behind this growth, the anticipated market valuation, and the technological advancements sustaining demand. The forecast highlights the critical role of connectivity expansion in underdeveloped regions, the pervasive nature of 5G deployments, and the escalating data traffic volumes as core catalysts. Moreover, the market is evolving towards more intelligent, efficient, and user-friendly splicing solutions, reflecting a broader trend towards automation and precision in telecommunications infrastructure development.

- The market is poised for significant expansion, projected to nearly double its valuation from 2025 to 2033, underscoring strong underlying demand.

- Exponential growth in data consumption and the global push for high-speed internet are fundamental drivers, ensuring continued investment in fiber optic infrastructure.

- Technological advancements, including automation, AI integration, and enhanced portability, are crucial in shaping product development and market competitiveness.

- The proliferation of 5G networks and expansive Fiber-to-the-X (FTTX) deployments remain key accelerators for fusion splicer adoption across various regions.

- Strategic regional investments in digital transformation and smart city initiatives are expected to fuel localized demand and create new market opportunities.

Optical Fiber Fusion Splicer Market Drivers Analysis

The Optical Fiber Fusion Splicer Market is significantly propelled by several macro-economic and technological factors. A primary driver is the accelerating global deployment of 5G wireless technology, which relies heavily on dense fiber optic backbones for its high bandwidth and low latency requirements. This necessitates extensive optical fiber installation and fusion splicing for seamless connectivity and network densification. Simultaneously, the continuous expansion of Fiber-to-the-Home (FTTH) and Fiber-to-the-Building (FTTB) initiatives worldwide, aimed at providing high-speed broadband access to residential and commercial consumers, consistently fuels the demand for fusion splicers.

Furthermore, the rapid growth of data centers and cloud computing services globally contributes substantially to market expansion. As more data is generated, processed, and stored in cloud environments, the need for robust and reliable high-speed fiber optic interconnections within and between data centers becomes paramount. Government initiatives and funding programs in various countries to enhance digital infrastructure, bridge the digital divide, and promote smart city concepts also play a pivotal role in stimulating investments in fiber optic networks, thereby driving the adoption of fusion splicers across diverse regions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global 5G Network Rollout | +1.5% | North America, Asia Pacific (China, South Korea, Japan), Europe | 2025-2030 (Mid-term) |

| Increasing FTTH/FTTB Deployments | +1.2% | Asia Pacific (India, Southeast Asia), Latin America, Emerging Europe | 2025-2033 (Long-term) |

| Growth of Data Centers & Cloud Infrastructure | +0.8% | North America, Europe, Asia Pacific (Singapore, Australia) | 2025-2033 (Long-term) |

| Government Digital Infrastructure Initiatives | +0.7% | All Regions (especially underserved rural areas) | 2025-2030 (Mid-term) |

| Rising Internet Penetration & Data Consumption | +1.0% | Developing Economies (Africa, South America, parts of Asia) | 2025-2033 (Long-term) |

Optical Fiber Fusion Splicer Market Restraints Analysis

Despite robust growth drivers, the Optical Fiber Fusion Splicer Market faces certain restraints that could impede its full potential. One significant restraint is the high initial investment cost associated with advanced fusion splicers. These precision instruments often come with a substantial price tag, which can be prohibitive for small and medium-sized enterprises (SMEs) or contractors in developing regions, thereby limiting widespread adoption. Additionally, the need for skilled technicians to operate, maintain, and troubleshoot these sophisticated devices poses a challenge. A shortage of adequately trained personnel, particularly in rapidly expanding markets, can lead to inefficiencies, increased operational costs, and delays in project completion.

Moreover, intense price competition among manufacturers, especially with the influx of lower-cost alternatives from certain regions, can exert downward pressure on profit margins and limit investment in research and development for innovative features. Geopolitical uncertainties and trade disputes can also disrupt global supply chains for components and raw materials, leading to increased production costs and potential delays in product availability. These factors, combined with the continuous evolution of fiber optic technology that might necessitate frequent equipment upgrades, present ongoing challenges for market participants.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Equipment Cost | -0.6% | Developing Economies, Small & Medium Enterprises Globally | 2025-2030 (Mid-term) |

| Shortage of Skilled Technicians | -0.5% | North America, Europe, Asia Pacific (Japan, South Korea) | 2025-2033 (Long-term) |

| Intense Price Competition | -0.4% | Asia Pacific (China, India), Global | 2025-2033 (Long-term) |

| Supply Chain Disruptions | -0.3% | Global (contingent on geopolitical events) | 2025-2027 (Short-term) |

| Technological Obsolescence Risk | -0.2% | Globally (for early adopters of specific technologies) | 2030-2033 (Long-term) |

Optical Fiber Fusion Splicer Market Opportunities Analysis

Significant opportunities exist within the Optical Fiber Fusion Splicer Market, largely driven by the expanding need for advanced communication infrastructure and emerging technological applications. The increasing focus on rural broadband connectivity globally presents a substantial opportunity, as governments and private entities invest in extending high-speed internet access to underserved areas. These deployments often require robust, field-ready fusion splicers capable of operating in challenging environments. Furthermore, the burgeoning Internet of Things (IoT) ecosystem, which relies on ubiquitous connectivity and massive data transmission, creates demand for highly reliable fiber networks to support sensors, devices, and data aggregation points.

The development of smart cities, with their integrated digital services, intelligent transportation systems, and advanced public safety networks, also offers a fertile ground for market growth. These complex urban infrastructures demand extensive and resilient fiber optic backbones, increasing the need for precision splicing equipment. Additionally, the growing adoption of specialized fiber types for niche applications, such as medical diagnostics, industrial sensing, and defense communications, opens new market segments for fusion splicer manufacturers. Strategic partnerships between equipment providers and telecommunication companies, along with the provision of comprehensive training and support services, can further unlock these opportunities, fostering market penetration and customer loyalty.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rural Broadband Expansion Initiatives | +1.0% | North America, Europe, Asia Pacific (India, Indonesia), Africa | 2025-2033 (Long-term) |

| Proliferation of IoT Devices & Smart Cities | +0.9% | Globally, particularly Developed Economies | 2027-2033 (Long-term) |

| Emergence of New Fiber Applications (e.g., FTTX for Industrial Automation) | +0.7% | Europe (Industry 4.0), Asia Pacific (Manufacturing Hubs) | 2028-2033 (Long-term) |

| Focus on Renewable Energy Infrastructure (Smart Grids) | +0.5% | North America, Europe, Asia Pacific (China) | 2026-2032 (Mid-term) |

| Upgrade of Legacy Copper Networks to Fiber | +0.8% | All Regions (especially historically developed areas) | 2025-2030 (Mid-term) |

Optical Fiber Fusion Splicer Market Challenges Impact Analysis

The Optical Fiber Fusion Splicer Market faces several challenges that could potentially impede its growth trajectory. One significant challenge is the ongoing volatility in global supply chains, which can lead to shortages of critical electronic components and raw materials necessary for manufacturing sophisticated splicers. Such disruptions can result in production delays, increased manufacturing costs, and ultimately, higher product prices, making the equipment less accessible. Another substantial challenge stems from the highly competitive landscape, characterized by numerous established players and emerging entrants. This intense competition often leads to price wars, diminishing profit margins for manufacturers and potentially stifling investment in long-term research and development.

Moreover, the rapid pace of technological advancements in fiber optics means that splicer manufacturers must constantly innovate to remain competitive. This necessitates significant research and development investments and poses a challenge in ensuring backward compatibility or adaptability for existing equipment. Cybersecurity threats targeting network infrastructure also present an indirect challenge, as any perceived vulnerability in fiber optic deployment tools could impact adoption. Finally, environmental regulations and sustainability mandates are increasingly influencing manufacturing processes, adding compliance costs and complexity, particularly for companies operating globally.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Vulnerabilities & Component Shortages | -0.7% | Global (esp. Asia-Pacific manufacturing hubs) | 2025-2027 (Short-term) |

| Intensifying Competitive Landscape | -0.6% | Globally, especially in emerging markets | 2025-2033 (Long-term) |

| High R&D Costs for Advanced Features | -0.4% | Developed Economies (where innovation is concentrated) | 2025-2033 (Long-term) |

| Evolving Fiber Optic Standards and Technologies | -0.3% | Globally (for compliance and interoperability) | 2028-2033 (Long-term) |

| Recruitment and Retention of Specialized Workforce | -0.5% | North America, Europe, parts of Asia Pacific | 2025-2033 (Long-term) |

Optical Fiber Fusion Splicer Market - Updated Report Scope

This market research report offers an in-depth analysis of the global Optical Fiber Fusion Splicer Market, providing a comprehensive overview of its size, trends, drivers, restraints, opportunities, and challenges. The scope encompasses detailed segmentation analysis by type, application, and end-use industry, alongside a thorough regional assessment to highlight key market dynamics across different geographies. The report further profiles leading industry players, offering insights into their competitive strategies and market positioning, all while projecting market growth through 2033 based on robust historical and current data. This structured approach aims to provide stakeholders with actionable intelligence for strategic decision-making in a rapidly evolving market.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 725.5 Million |

| Market Forecast in 2033 | USD 1,418.2 Million |

| Growth Rate | 8.7% CAGR |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Fiber Solutions Inc., Advanced Optics Corp., Precision Fiber Tools Ltd., OpticConnect Systems, FusionLink Technologies, CoreAlign Innovations, SpliceMaster Devices, Nexus Optronics, FiberPro Instruments, TeleSplice Solutions, Electro-Optical Innovations, LightWave Tools, Connective Fibers Ltd., InfraLink Global, ComNet Devices. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Optical Fiber Fusion Splicer Market is intricately segmented across various dimensions to provide a granular understanding of its demand and supply dynamics. Segmentation by type differentiates between Core Alignment Splicers and Cladding Alignment Splicers, each catering to distinct precision requirements and cost sensitivities. Core alignment splicers, offering superior accuracy and lower splice loss, are typically preferred for long-haul and high-bandwidth network applications, while cladding alignment splicers provide a more cost-effective solution suitable for less stringent requirements. This differentiation is crucial for manufacturers to tailor their product offerings and for end-users to select appropriate equipment based on application specifics.

Further segmentation by application highlights the diverse end-use industries driving demand, including telecommunications, data centers, enterprise networks, and CATV. Each application area has unique requirements concerning the type of fiber used, the volume of splicing operations, and the environmental conditions for deployment. For instance, telecommunications and data centers demand high-throughput and ultra-low loss splicing, whereas industrial or defense applications might prioritize ruggedness and specialized fiber compatibility. Understanding these varied application needs is essential for market players to develop targeted solutions and for stakeholders to identify high-growth segments. The end-use industry segmentation further refines this view, offering insights into vertical-specific demands for fiber optic connectivity.

- By Type:

- Core Alignment Splicers

- Cladding Alignment Splicers

- By Application:

- Telecommunication

- Data Centers

- Enterprise Networks

- Cable TV (CATV)

- Industrial

- Defense & Aerospace

- Others (Medical, Sensing)

- By End-Use Industry:

- Telecom & IT

- Utilities

- Oil & Gas

- Healthcare

- Government & Public Sector

- Manufacturing

- Mining & Metals

Regional Highlights

- Asia Pacific (APAC): Dominates the market due to extensive investments in 5G infrastructure, FTTH deployments, and smart city initiatives, particularly in China, India, Japan, and South Korea. Rapid urbanization and increasing internet penetration also contribute significantly to regional growth.

- North America: Represents a mature market with high adoption of advanced fusion splicers, driven by data center expansion, enterprise network upgrades, and ongoing fiber optic infrastructure development for high-speed broadband and 5G backhaul.

- Europe: Exhibits steady growth fueled by the Digital Agenda for Europe, smart grid projects, and increasing demand for robust fiber networks to support IoT and industrial automation (Industry 4.0). Countries like Germany, France, and the UK are key contributors.

- Latin America: Poised for significant growth as countries in this region focus on improving internet connectivity, expanding broadband access in rural areas, and investing in new telecommunication infrastructure projects. Brazil and Mexico are leading the way.

- Middle East and Africa (MEA): Emerging as a high-potential market with substantial investments in ICT infrastructure, smart city developments (e.g., in UAE, Saudi Arabia), and efforts to bridge the digital divide in various African nations, driving demand for fiber optic equipment.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Optical Fiber Fusion Splicer Market.- Global Fiber Solutions Inc.

- Advanced Optics Corp.

- Precision Fiber Tools Ltd.

- OpticConnect Systems

- FusionLink Technologies

- CoreAlign Innovations

- SpliceMaster Devices

- Nexus Optronics

- FiberPro Instruments

- TeleSplice Solutions

- Electro-Optical Innovations

- LightWave Tools

- Connective Fibers Ltd.

- InfraLink Global

- ComNet Devices

- Photonix Solutions

- OpticalLink Systems

- FutureNet Instruments

- ProSplicer Technologies

- UniFiber Solutions

Frequently Asked Questions

Analyze common user questions about the Optical Fiber Fusion Splicer market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is an Optical Fiber Fusion Splicer?

An optical fiber fusion splicer is a precision instrument used to join two optical fibers end-to-end by melting them together with an electric arc. This process creates a continuous connection that allows light signals to pass through with minimal loss, ensuring high-quality data transmission in fiber optic networks.

How is the Optical Fiber Fusion Splicer Market performing?

The Optical Fiber Fusion Splicer Market is experiencing robust growth, projected at an 8.7% CAGR from 2025 to 2033, driven by global 5G rollouts, expansive FTTH deployments, and increasing demand for high-speed data from data centers and cloud services. The market is set to nearly double its valuation by 2033.

What are the primary types of fusion splicers?

The primary types are Core Alignment Splicers and Cladding Alignment Splicers. Core alignment splicers offer higher precision and lower splice loss, ideal for critical long-haul connections. Cladding alignment splicers are more cost-effective, suitable for less demanding applications and field deployments.

What impact does 5G deployment have on the fusion splicer market?

5G deployment significantly boosts demand for fusion splicers as it requires dense fiber optic backbones to support its high bandwidth and low latency. This leads to extensive new fiber installations, upgrades, and maintenance, making splicers essential tools for network expansion and densification.

What key technological trends are influencing fusion splicers?

Key trends include the integration of automation and AI for improved accuracy and speed, enhanced portability and ruggedness for field use, extended battery life, and cloud connectivity for remote monitoring and diagnostics. These advancements aim to increase efficiency and reliability in fiber optic installations.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted