Variable life Insurance Market

Variable life Insurance Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702280 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

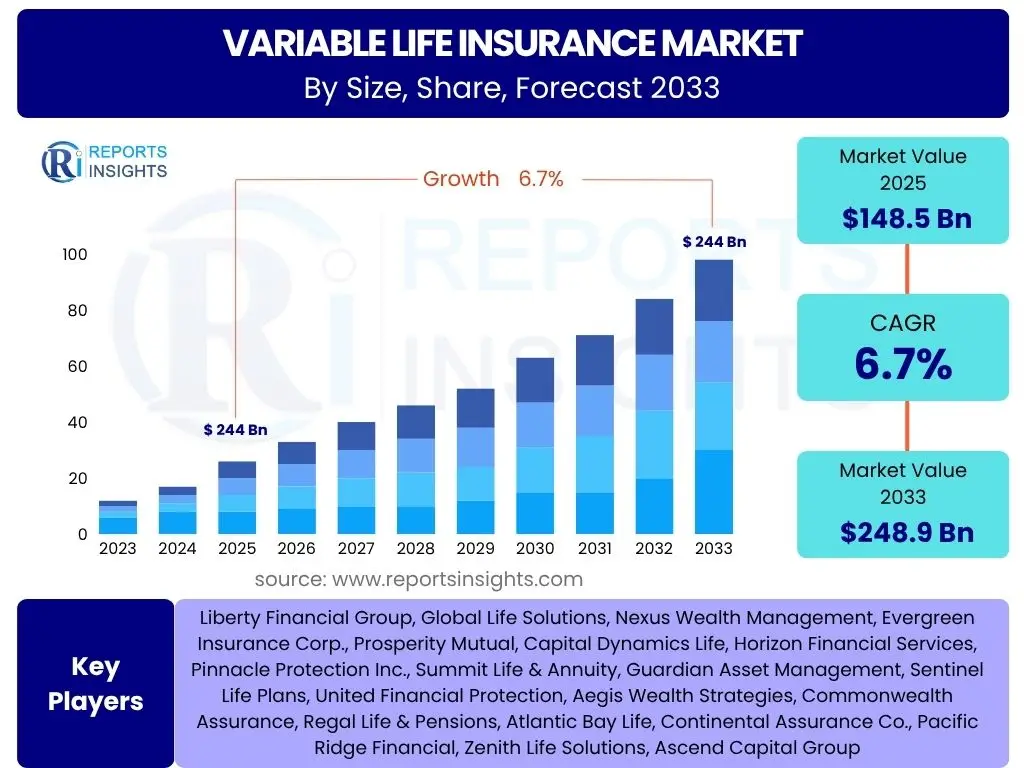

Variable life Insurance Market Size

According to Reports Insights Consulting Pvt Ltd, The Variable life Insurance Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033. The market is estimated at USD 148.5 Billion in 2025 and is projected to reach USD 248.9 Billion by the end of the forecast period in 2033.

This robust growth trajectory reflects the increasing demand for sophisticated financial instruments that offer both wealth accumulation and risk protection benefits. Variable life insurance policies, with their investment component, appeal to individuals and families seeking to leverage market upside while securing a death benefit. The projected expansion indicates a strong underlying confidence in the product's ability to adapt to evolving economic landscapes and investor preferences.

The market's expansion is further fueled by rising global wealth, increasing financial literacy among consumers, and the search for tax-efficient savings vehicles. As interest rates fluctuate and traditional savings options yield less attractive returns, variable life insurance stands out as a viable alternative for long-term financial planning. The growth forecast underscores a strategic shift in consumer behavior towards products that offer flexibility and potential for higher returns, albeit with associated risks.

Key Variable life Insurance Market Trends & Insights

Common user inquiries about Variable life Insurance market trends often revolve around product innovation, digitalization, regulatory changes, and how these factors influence policy design and distribution. Users are particularly interested in understanding how policies are adapting to contemporary financial needs, the impact of technological advancements on accessibility, and the ongoing shift towards more personalized and transparent offerings. There is also significant curiosity regarding the integration of environmental, social, and governance (ESG) factors into investment options within these policies.

- Increased Customization and Flexibility: Policyholders increasingly seek variable life insurance products that offer greater flexibility in terms of premium payments, death benefit options, and investment choices, allowing for tailored financial strategies.

- Digital Transformation of Distribution and Servicing: The adoption of digital platforms, online sales channels, and self-service portals is streamlining the purchasing process and enhancing customer experience, making variable life insurance more accessible.

- Emphasis on ESG-Integrated Investment Options: Growing awareness and demand for sustainable investing are leading insurers to incorporate ESG-focused funds and investment strategies within their variable life insurance portfolios.

- Integration with Holistic Financial Planning: Variable life insurance is increasingly positioned as a core component of comprehensive financial and estate planning, moving beyond just a death benefit to serve broader wealth management objectives.

- Heightened Regulatory Scrutiny and Consumer Protection: Regulators worldwide are intensifying their focus on ensuring transparency, fair practices, and adequate disclosure for variable life insurance products, influencing product design and sales practices.

- Focus on Living Benefits and Riders: Insurers are offering more riders and living benefits, such as chronic illness or long-term care riders, to enhance the value proposition of variable life insurance and address broader client needs during their lifetime.

- Global Expansion into Emerging Markets: Insurers are exploring opportunities in developing economies where rising disposable incomes and nascent financial markets present significant potential for growth in the variable life insurance sector.

AI Impact Analysis on Variable life Insurance

User questions related to the impact of AI on Variable life Insurance frequently center on its role in underwriting, personalized policy offerings, claims processing, and enhancing customer service. There is considerable interest in how AI can streamline operations, reduce costs, and improve accuracy in risk assessment, while also concerns exist regarding data privacy, algorithmic bias, and the potential for job displacement. Users are keen to understand how AI can lead to more dynamic and responsive insurance solutions, balancing technological advancement with ethical considerations and regulatory compliance.

- Enhanced Underwriting and Risk Assessment: AI algorithms can analyze vast datasets, including health records, lifestyle data, and financial history, to provide more accurate and personalized risk assessments for variable life insurance applicants, potentially leading to fairer premiums and faster approvals.

- Personalized Policy Customization: AI-driven analytics enable insurers to offer highly customized variable life insurance policies that align with individual client needs, risk tolerance, and financial goals, improving product relevance and customer satisfaction.

- Automated Customer Service and Support: AI-powered chatbots and virtual assistants can provide instant support for policy inquiries, investment updates, and administrative tasks, improving efficiency and availability of customer service.

- Fraud Detection and Prevention: AI systems can identify suspicious patterns and anomalies in applications and claims, significantly improving fraud detection capabilities and reducing financial losses for insurers.

- Optimized Investment Strategy and Portfolio Management: AI tools can analyze market trends, predict investment performance, and suggest optimal asset allocations within variable life insurance policies, helping policyholders and advisors make more informed decisions.

- Streamlined Claims Processing: Automation and AI can accelerate the claims processing workflow by verifying information, assessing validity, and facilitating payouts, leading to quicker resolutions for beneficiaries.

- Predictive Analytics for Lapsed Policies: AI can predict the likelihood of policy lapses or surrenders, allowing insurers to proactively engage with policyholders and offer retention strategies, thereby improving policy persistency.

Key Takeaways Variable life Insurance Market Size & Forecast

User queries regarding key takeaways from the Variable life Insurance market size and forecast often focus on the market's long-term viability, primary growth drivers, and potential shifts in investment preferences. Insights reveal that sustained growth is anticipated, driven by a confluence of demographic factors, technological advancements, and a growing consumer appetite for flexible wealth management solutions. The market is poised for significant expansion, but will also navigate complexities related to regulatory oversight and market volatility, demanding agility from industry participants.

- Sustained Growth Trajectory: The Variable life Insurance market is set for continuous expansion, driven by increasing global wealth and the need for comprehensive financial planning solutions.

- Demand for Hybrid Products: There is a clear market preference for products that combine the benefits of life insurance protection with flexible investment opportunities and wealth accumulation potential.

- Digitalization as a Growth Catalyst: The adoption of digital channels and advanced technologies is crucial for market penetration, efficiency gains, and enhancing customer engagement, particularly among younger demographics.

- Regulatory Adaptation is Key: The evolving regulatory landscape, focused on consumer protection and transparency, will significantly shape product design and distribution strategies.

- Importance of Financial Advisor Role: Despite digital advancements, the complexity of variable life insurance products necessitates the continued vital role of financial advisors in guiding consumers.

- Investment Performance Sensitivity: Market performance remains a critical determinant of policyholder satisfaction and product attractiveness, underscoring the need for robust investment management.

- Focus on ESG Factors: The integration of environmental, social, and governance considerations into investment portfolios is becoming a significant factor influencing consumer choice and product development.

Variable life Insurance Market Drivers Analysis

The Variable life Insurance market is significantly driven by several macroeconomic and demographic factors that underpin its appeal as a comprehensive financial solution. The increasing awareness among individuals about the importance of wealth accumulation alongside life protection, especially in an era of fluctuating economic conditions, acts as a primary catalyst. Furthermore, the search for tax-efficient investment vehicles and the growing financial sophistication of consumers contribute to the rising demand for these products. These drivers collectively foster an environment conducive to the sustained expansion of the variable life insurance sector.

Technological advancements also play a crucial role, particularly in enhancing the accessibility and appeal of variable life insurance products. Digitalization of distribution channels, coupled with advanced data analytics for personalized product offerings, has made it easier for consumers to understand and acquire these complex instruments. Moreover, the aging global population and the resultant need for robust retirement planning solutions further bolster the market, as variable life insurance offers a flexible avenue for long-term savings and legacy planning.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Disposable Incomes & Wealth Accumulation Needs | +0.8% | Global, particularly North America, Asia Pacific | Long-term (2025-2033) |

| Increasing Financial Literacy & Investment Awareness | +0.6% | Global, with emphasis on emerging economies | Medium-term (2025-2029) |

| Demand for Tax-Efficient Savings & Estate Planning Tools | +0.7% | North America, Europe, high-tax jurisdictions | Long-term (2025-2033) |

| Product Innovation & Customization | +0.5% | Global | Ongoing |

| Digitalization of Distribution & Service Channels | +0.4% | Global | Short-to-Medium term (2025-2027) |

Variable life Insurance Market Restraints Analysis

Despite its growth potential, the Variable life Insurance market faces several significant restraints that can impede its expansion. One of the primary concerns is the inherent complexity of these products, which often makes them difficult for the average consumer to understand. This complexity, coupled with the potential for high fees and charges associated with active investment management and policy administration, can deter prospective buyers who prefer simpler, more transparent financial instruments. Misconceptions about variable life insurance, often stemming from past mis-selling scandals or a lack of clear communication, also contribute to consumer skepticism and hesitancy.

Furthermore, the performance of variable life insurance policies is directly tied to the volatility of underlying investment markets. Economic downturns, periods of high inflation, or significant market corrections can lead to reduced policy values and diminished returns, impacting consumer confidence and demand. The stringent regulatory environment, while aimed at consumer protection, can also pose a restraint by increasing compliance costs for insurers and potentially limiting product innovation due to extensive approval processes. These factors collectively necessitate careful navigation by market participants to mitigate their impact on growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Market Volatility & Investment Risk | -0.9% | Global | Cyclical |

| High Fees & Charges | -0.7% | Global | Ongoing |

| Regulatory Complexity & Compliance Burden | -0.6% | North America, Europe | Ongoing |

| Lack of Product Transparency & Consumer Misconceptions | -0.5% | Global | Long-term |

| Intense Competition from Alternative Investments | -0.4% | Global | Ongoing |

Variable life Insurance Market Opportunities Analysis

Significant opportunities exist within the Variable life Insurance market, particularly stemming from the evolving financial needs of different consumer segments. The increasing demand for comprehensive wealth management solutions, especially among high-net-worth individuals and affluent families, presents a fertile ground for market expansion. These segments often seek sophisticated tools that integrate investment growth, tax efficiency, and estate planning, all of which are core components of variable life insurance. Product innovation focused on incorporating additional living benefits, such as riders for long-term care or critical illness, can also broaden the appeal of these policies to a wider demographic concerned about future health expenses.

The digitalization of financial services offers another substantial avenue for growth. Leveraging advanced analytics, artificial intelligence, and machine learning can lead to more personalized product offerings, streamlined underwriting processes, and enhanced customer engagement. This technological integration can also reduce operational costs and improve efficiency, making products more competitive. Furthermore, expanding into underserved emerging markets, where disposable incomes are rising and financial literacy is improving, represents a long-term growth opportunity for insurers capable of adapting their offerings to local regulatory and cultural contexts.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Digital Transformation & Fintech Integration | +0.8% | Global | Medium-term (2025-2029) |

| Untapped Markets in Emerging Economies | +0.7% | Asia Pacific, Latin America, MEA | Long-term (2027-2033) |

| Product Diversification (e.g., ESG options, living benefits) | +0.6% | Global | Ongoing |

| Focus on High Net-Worth Individuals & Wealth Management | +0.5% | Global | Long-term (2025-2033) |

| Strategic Partnerships & Collaborations | +0.4% | Global | Medium-term (2025-2029) |

Variable life Insurance Market Challenges Impact Analysis

The Variable life Insurance market faces several critical challenges that demand strategic responses from industry players. Economic downturns and periods of high market volatility pose a significant risk, as they can directly impact the investment performance of policies, leading to reduced policy values and potential surrenders. This sensitivity to market fluctuations can erode consumer confidence and make variable life insurance less attractive compared to more stable financial instruments. Furthermore, the inherent complexity of these products continues to be a hurdle, requiring extensive client education and skilled financial advisors, which adds to distribution costs and complexity.

Another substantial challenge is the intense competition from a wide array of alternative investment products and traditional life insurance options. Mutual funds, exchange-traded funds (ETFs), annuities, and even direct stock market investments offer varying degrees of risk and return, forcing variable life insurance providers to constantly innovate and justify their value proposition. Moreover, stringent and evolving regulatory frameworks across different jurisdictions require continuous adaptation in product design, disclosure requirements, and sales practices, adding significant compliance burdens. Cybersecurity threats and data privacy concerns also present an ongoing challenge, as insurers handle sensitive financial and personal information, necessitating robust security measures to maintain client trust.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Economic Downturns & Market Volatility | -1.0% | Global | Short-to-Medium term (Cyclical) |

| Intense Competitive Landscape | -0.8% | Global | Ongoing |

| Talent Acquisition & Retention of Skilled Advisors | -0.6% | North America, Europe, Asia Pacific | Long-term |

| Cybersecurity Risks & Data Privacy Concerns | -0.5% | Global | Ongoing |

| Evolving Consumer Expectations & Digital Demands | -0.4% | Global | Medium-term (2025-2029) |

Variable life Insurance Market - Updated Report Scope

This report offers an in-depth analysis of the global Variable life Insurance market, providing a comprehensive overview of its size, growth trajectory, key trends, and future outlook from 2025 to 2033. It incorporates detailed segmentation analysis, regional insights, and an assessment of the competitive landscape, equipping stakeholders with actionable intelligence to navigate market complexities and capitalize on emerging opportunities.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 148.5 Billion |

| Market Forecast in 2033 | USD 248.9 Billion |

| Growth Rate | 6.7% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Liberty Financial Group, Global Life Solutions, Nexus Wealth Management, Evergreen Insurance Corp., Prosperity Mutual, Capital Dynamics Life, Horizon Financial Services, Pinnacle Protection Inc., Summit Life & Annuity, Guardian Asset Management, Sentinel Life Plans, United Financial Protection, Aegis Wealth Strategies, Commonwealth Assurance, Regal Life & Pensions, Atlantic Bay Life, Continental Assurance Co., Pacific Ridge Financial, Zenith Life Solutions, Ascend Capital Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Variable life Insurance market is segmented across several key dimensions to provide a granular view of its dynamics and growth drivers. These segmentations allow for a detailed analysis of consumer preferences, distribution efficacy, and product utility across diverse applications. Understanding these segments is crucial for insurers to tailor their offerings, optimize their distribution strategies, and effectively target specific demographic and financial needs. The market's diverse segmentation reflects the multifaceted nature of variable life insurance as a financial tool.

Further analysis within these segments highlights the growing importance of digital channels and personalized offerings, particularly within the individual and high net worth segments. The application-based segmentation underscores the shift from mere death benefit provision to a broader role in wealth and estate planning. This comprehensive segmentation framework provides a robust foundation for strategic decision-making and market positioning within the variable life insurance industry.

- By Product Type: This segment categorizes policies based on their premium payment structure and flexibility, including Universal Variable Life (flexible premiums, flexible death benefits), Scheduled Premium Variable Life (fixed premium schedule), and Single Premium Variable Life (one-time lump sum premium).

- By Distribution Channel: This segment analyzes how policies reach consumers, encompassing traditional channels like Agency and Bancassurance, as well as evolving channels such as Brokers and the increasingly significant Digital/Online platforms.

- By Application: This segment identifies the primary financial objectives policyholders aim to achieve, including Wealth Accumulation, Estate Planning, Retirement Planning, and Legacy Planning, reflecting the versatile utility of these products.

- By End-User: This segment delineates the types of clients procuring these policies, distinguishing between Individuals (general consumers), High Net Worth Individuals (HNWIs) (affluent clients with complex financial needs), and Small & Medium Enterprises (SMEs) (for key person insurance or executive benefits).

Regional Highlights

- North America: This region holds a significant share in the Variable life Insurance market, driven by a high concentration of high-net-worth individuals, sophisticated financial markets, and strong awareness of wealth management and estate planning. The presence of major financial advisory firms and a mature regulatory framework further support market growth. The region sees continuous innovation in product design, adapting to evolving tax laws and investment preferences.

- Europe: Characterized by diverse economies and regulatory environments, Europe's Variable life Insurance market is influenced by varying national preferences for investment-linked products and the impact of Solvency II regulations. Countries like the UK, Germany, and France are key contributors, with increasing demand for wealth transfer solutions and retirement planning products that offer investment flexibility. The region is also witnessing a growing interest in ESG-compliant investment options within variable life policies.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, fueled by rapidly expanding economies, a burgeoning middle class, and increasing disposable incomes, particularly in China, India, and Southeast Asian nations. Rising financial literacy and the shift from traditional savings to investment-oriented insurance products are driving demand. Digital adoption and innovative distribution models are pivotal in reaching a vast and diverse consumer base across the region.

- Latin America: This region presents emerging opportunities for the Variable life Insurance market, driven by economic development, urbanization, and a growing affluent population seeking diversified investment and protection solutions. Political and economic stability remains a factor influencing market penetration, but increasing awareness about long-term financial security is fostering growth in countries like Brazil and Mexico.

- Middle East and Africa (MEA): The MEA region is experiencing gradual growth in the Variable life Insurance market, largely supported by robust economic diversification initiatives and wealth creation in Gulf Cooperation Council (GCC) countries. The demand for sharia-compliant financial products and innovative wealth management solutions is contributing to market development, albeit from a relatively smaller base. Regulatory reforms aimed at enhancing market transparency and investor protection are expected to catalyze further expansion.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Variable life Insurance Market.- Liberty Financial Group

- Global Life Solutions

- Nexus Wealth Management

- Evergreen Insurance Corp.

- Prosperity Mutual

- Capital Dynamics Life

- Horizon Financial Services

- Pinnacle Protection Inc.

- Summit Life & Annuity

- Guardian Asset Management

- Sentinel Life Plans

- United Financial Protection

- Aegis Wealth Strategies

- Commonwealth Assurance

- Regal Life & Pensions

- Atlantic Bay Life

- Continental Assurance Co.

- Pacific Ridge Financial

- Zenith Life Solutions

- Ascend Capital Group

Frequently Asked Questions

Analyze common user questions about the Variable life Insurance market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Variable life Insurance and how does it work?

Variable life insurance is a permanent life insurance policy with an investment component, offering both a death benefit and cash value accumulation. Policyholders direct their premiums into various investment sub-accounts, such as stocks, bonds, and money market funds. The cash value and death benefit can fluctuate based on the performance of these chosen investments, providing potential for growth but also exposing policyholders to market risk.

What are the main advantages of Variable life Insurance?

The primary advantages include the potential for significant cash value growth through investment returns, tax-deferred growth on the cash value, a tax-free death benefit, and flexibility in premium payments and death benefit options. It also offers a wide range of investment choices, allowing policyholders to tailor their portfolios to their risk tolerance and financial goals, making it a powerful tool for wealth accumulation and estate planning.

What are the risks associated with Variable life Insurance?

The main risks stem from the investment component; poor market performance can lead to a decrease in cash value and potentially the death benefit. Policyholders also face various fees and charges, including mortality and expense charges, administrative fees, and investment management fees, which can reduce overall returns. There is also the risk of policy lapse if the cash value declines too much and premiums are not sufficient to cover costs.

How is Variable life Insurance different from Universal life Insurance?

While both are flexible permanent life insurance policies with cash value components, the key difference lies in the investment control and risk. Variable life insurance allows policyholders to choose specific investment sub-accounts, bearing the investment risk and potential for higher returns. Universal life insurance, conversely, typically invests in a general account, with the insurer bearing the investment risk and offering a guaranteed minimum interest rate, providing more stability but often less growth potential.

Who is Variable life Insurance best suited for?

Variable life insurance is typically best suited for individuals with a higher risk tolerance, a long-term investment horizon, and a desire for potential growth beyond what traditional policies offer. It appeals to those seeking wealth accumulation, estate planning benefits, and tax-deferred growth, who are comfortable managing their investment choices or have a trusted financial advisor to assist them. It is often favored by high-net-worth individuals and those with significant disposable income.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted