Satellite Launch and Space Insurance Market

Satellite Launch and Space Insurance Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703178 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Satellite Launch and Space Insurance Market Size

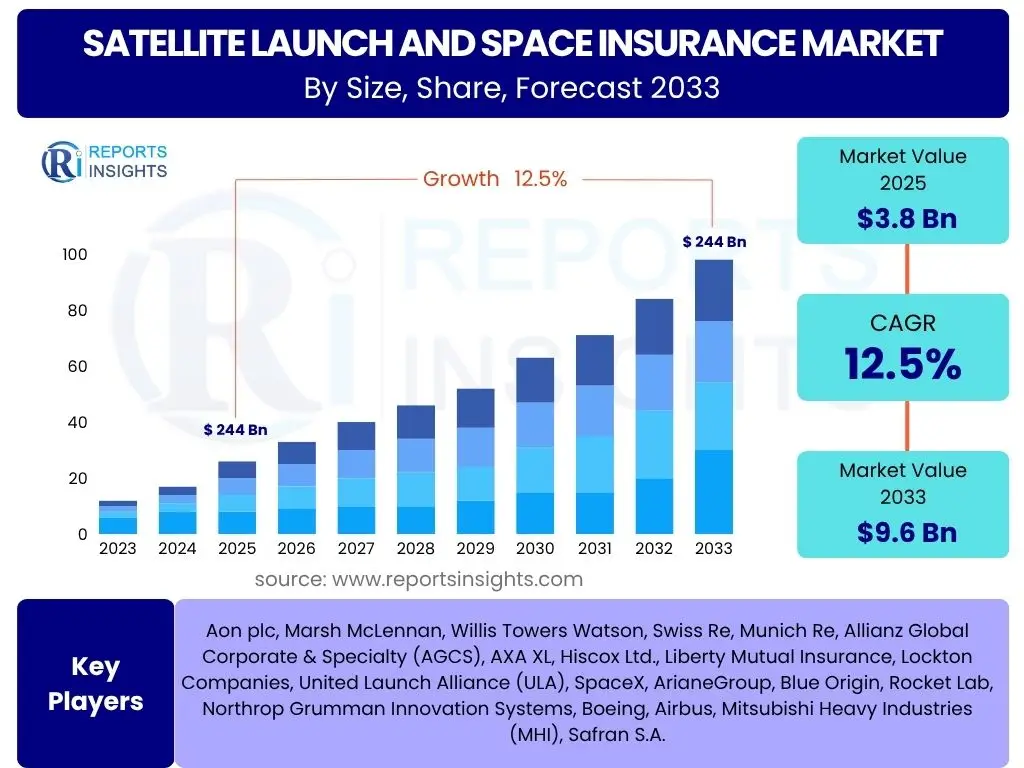

According to Reports Insights Consulting Pvt Ltd, The Satellite Launch and Space Insurance Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2025 and 2033. The market is estimated at USD 3.8 Billion in 2025 and is projected to reach USD 9.6 Billion by the end of the forecast period in 2033.

Key Satellite Launch and Space Insurance Market Trends & Insights

The satellite launch and space insurance market is currently navigating a period of rapid transformation, primarily driven by a surge in commercial space activities and technological advancements. User interest frequently centers on how evolving launch methodologies, such as reusable rockets and the proliferation of mega-constellations in low Earth orbit (LEO), are reshaping traditional risk assessment models. The industry is witnessing a significant shift from bespoke, high-value geostationary (GEO) satellite launches to a volume-driven market characterized by smaller, more frequent LEO deployments, each presenting unique actuarial challenges related to launch vehicle reliability, in-orbit longevity, and potential for collision.

Another prominent area of inquiry involves the increasing sophistication of satellite technology and its implications for insurance coverage. Trends such as on-orbit servicing, satellite life extension, and the deployment of complex interconnected satellite networks introduce new categories of risk, including cybersecurity vulnerabilities and potential supply chain disruptions. Furthermore, the growing number of private entities entering the space domain, often with innovative but unproven technologies, necessitates flexible and adaptive insurance solutions that can account for novel risks while fostering industry growth.

The market also grapples with the escalating concern over space debris, which poses a significant threat to operational satellites and future missions. Insurers are increasingly factoring in the risks associated with orbital congestion and the potential for collisions, prompting discussions around liability, mitigation strategies, and the development of new insurance products tailored to address these environmental challenges. The interplay between technological innovation, commercial expansion, and regulatory evolution is continuously shaping the landscape of satellite launch and space insurance.

- Proliferation of LEO and MEO mega-constellations transforming risk profiles and underwriting.

- Increased adoption of reusable launch vehicle technology impacting premium structures and liability.

- Rising demand for in-orbit servicing and life extension missions creating new insurance product categories.

- Integration of advanced data analytics and predictive modeling for enhanced risk assessment.

- Growing concerns over space debris and orbital congestion driving demand for liability and mitigation insurance.

- Emergence of new private space companies and nations diversifying the client base.

- Development of specialized cybersecurity insurance for satellite systems and ground infrastructure.

AI Impact Analysis on Satellite Launch and Space Insurance

The integration of Artificial intelligence (AI) is anticipated to profoundly impact the satellite launch and space insurance sector, fundamentally altering how risks are assessed, policies are underwritten, and claims are processed. Common user inquiries often revolve around AI's capacity to enhance the precision of risk modeling, leveraging vast datasets from past launches, in-orbit performance, and telemetry to predict potential failures with greater accuracy. This allows insurers to move beyond historical actuarial tables towards more dynamic, real-time risk evaluations, potentially leading to more competitive and tailored premium structures.

Furthermore, AI-driven solutions are expected to streamline operational efficiencies across the insurance value chain. This includes automated underwriting processes that can rapidly analyze complex proposals, intelligent claims systems capable of expediting damage assessment and payout, and predictive maintenance algorithms for satellites that could proactively mitigate in-orbit risks. The ability of AI to process and interpret complex sensor data from space assets will be crucial for monitoring satellite health, detecting anomalies, and providing evidentiary support for claims, thereby reducing disputes and improving transparency for all stakeholders.

However, the adoption of AI also raises critical considerations regarding data privacy, algorithmic bias, and the need for robust cybersecurity measures to protect sensitive operational data. Stakeholders are keen to understand how AI will manage the inherent uncertainties of space operations, particularly for novel technologies with limited historical data. The challenge lies in developing explainable AI models that can build trust and provide clear justifications for decisions, ensuring that the benefits of AI in terms of enhanced risk management and operational efficiency are fully realized without compromising ethical standards or introducing unforeseen vulnerabilities.

- Enhanced risk modeling and predictive analytics for launch success and in-orbit longevity.

- Automated underwriting processes for faster policy generation and tailored premiums.

- Improved anomaly detection and fault diagnosis for in-orbit satellites using machine learning.

- Streamlined claims processing through AI-powered data analysis and damage assessment.

- Predictive maintenance for space assets, reducing the likelihood of insured events.

- Development of sophisticated fraud detection mechanisms in claims assessment.

- Challenges related to data privacy, algorithmic transparency, and cybersecurity in AI implementation.

Key Takeaways Satellite Launch and Space Insurance Market Size & Forecast

The Satellite Launch and Space Insurance Market is poised for substantial growth over the forecast period, reflecting the escalating pace of innovation and investment within the global space economy. A primary takeaway is the significant expansion driven by the commercialization of space, particularly the proliferation of LEO mega-constellations for broadband internet and Earth observation. This shift from government-centric, high-value assets to a volume-driven market necessitates a complete rethinking of insurance products and risk assessment methodologies, creating both opportunities for specialized coverage and challenges in managing aggregate risk across thousands of smaller satellites.

Another crucial insight is the dynamic interplay between technological advancements, such as reusable rockets and on-orbit servicing capabilities, and the evolving insurance landscape. These innovations, while reducing operational costs and extending satellite lifespans, also introduce new risk paradigms that require sophisticated underwriting expertise. The market's future trajectory is heavily influenced by the ability of insurers to adapt quickly to these technological shifts, offering flexible and comprehensive coverage that supports the industry's growth while maintaining profitability amidst increasing complexity and competition.

Finally, the market forecast underscores the growing importance of global collaboration and regulatory clarity in mitigating pervasive risks like space debris and cyber threats. Stakeholders are increasingly aware that the sustainability of the space environment directly impacts the insurability of assets. Therefore, the market's long-term health is intertwined with the development of international norms, traffic management protocols, and robust cybersecurity frameworks that ensure the safety and security of space operations for all participants, making these factors central to future market strategies and investment decisions.

- Significant market expansion driven by increased commercial space activities and satellite deployments.

- Transition from traditional, high-value GEO satellite coverage to a volume-driven market for LEO/MEO constellations.

- Technological advancements like reusability and on-orbit servicing necessitate evolving insurance models.

- Growing focus on risk mitigation for space debris and cybersecurity threats.

- Increased private sector investment and participation diversifying the insurance client base.

- Demand for customized and flexible insurance policies adapting to rapid industry changes.

- Importance of regulatory frameworks and international cooperation for market stability and growth.

Satellite Launch and Space Insurance Market Drivers Analysis

The Satellite Launch and Space Insurance Market is primarily propelled by the exponential growth in global space activities, particularly the increasing frequency of satellite launches across various orbits. The burgeoning demand for satellite-based services, including broadband internet, Earth observation, navigation, and telecommunications, has spurred significant investment from both government agencies and private enterprises. This surge in deployment volume naturally escalates the demand for comprehensive insurance coverage, mitigating the financial risks associated with complex and costly space missions, from pre-launch preparations to in-orbit operations and potential liabilities.

Technological advancements in satellite manufacturing and launch vehicle capabilities also serve as a significant market driver. Innovations such as miniaturization of satellites, the development of reusable rocket technology, and the advent of mega-constellations have made space access more affordable and frequent. While these innovations introduce new risk profiles, they also expand the addressable market for insurance by making space endeavors accessible to a wider array of commercial players and start-ups, who often require robust financial protection to secure investments and manage unforeseen circumstances in an inherently high-risk environment.

Furthermore, the increasing awareness and concern regarding in-orbit risks, including space debris, solar radiation, and potential collisions, are driving demand for specialized in-orbit insurance policies. As the orbital environment becomes more congested, the need for robust liability coverage and comprehensive asset protection becomes paramount for satellite operators. This evolving risk landscape, coupled with growing private sector participation and the development of new space applications, creates a fertile ground for the expansion and diversification of the satellite launch and space insurance market, encouraging innovation in insurance product offerings.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Commercial Satellite Launches | +3.5% | Global, particularly North America, Europe, Asia Pacific | 2025-2033 |

| Growing Demand for Satellite-Based Services | +2.8% | Global, emerging economies | 2025-2033 |

| Technological Advancements in Space Industry | +2.3% | Developed space nations | 2025-2033 |

| Rising Private Sector Investment in Space | +1.9% | Global | 2025-2033 |

Satellite Launch and Space Insurance Market Restraints Analysis

Despite significant growth prospects, the Satellite Launch and Space Insurance Market faces several critical restraints that can temper its expansion. One primary impediment is the inherently high cost associated with space missions, including launch services, satellite manufacturing, and operational expenses. This elevated cost translates directly into high insurance premiums, which can be prohibitive for smaller space companies or start-ups with limited capital. The substantial upfront investment required for comprehensive coverage often deters potential clients, leading some to self-insure or opt for partial coverage, thereby limiting the overall market size and premium volume.

Another significant restraint stems from the complex and evolving regulatory landscape governing space activities. International treaties, national space laws, and varying liability regimes across different jurisdictions create a challenging environment for insurers to standardize policies and assess risks consistently. Uncertainty surrounding responsibility in the event of accidents, especially those involving space debris or cross-border operations, can lead to reluctance among insurers to offer broad coverage or result in more stringent terms and higher deductibles, thereby impacting market accessibility and growth.

Furthermore, the relatively limited number of catastrophic events in space, while positive for the industry's safety record, can also pose a unique challenge for actuarial science. The lack of extensive historical claims data, particularly for novel technologies or emerging launch providers, makes it difficult for insurers to accurately model risk and set appropriate premium rates. This data scarcity can lead to conservative underwriting practices, higher reserves, and a more cautious approach to embracing new entrants or innovative mission profiles, ultimately restricting the market's ability to fully capitalize on new opportunities.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Space Missions and Premiums | -2.0% | Global, particularly emerging markets | 2025-2030 |

| Complex and Evolving Regulatory Environment | -1.5% | Global, highly regulated regions | 2025-2033 |

| Limited Historical Claims Data for New Tech | -1.2% | Global, particularly for innovative ventures | 2025-2030 |

Satellite Launch and Space Insurance Market Opportunities Analysis

The Satellite Launch and Space Insurance Market is ripe with opportunities driven by the rapid expansion and diversification of the global space economy. The emergence of new space nations and a growing number of private sector entities, ranging from small satellite developers to aspiring lunar mission providers, presents a significant opportunity for market expansion. These new entrants often lack established risk management protocols and require specialized insurance solutions tailored to their unique operational profiles and varying scales of investment, opening avenues for insurers to develop niche products and expand their client base beyond traditional aerospace giants.

Another key opportunity lies in the development and proliferation of innovative insurance products designed to address evolving risks and market needs. This includes policies for in-orbit servicing, satellite life extension, active debris removal missions, and dedicated cybersecurity insurance for space assets. As the complexity of space operations increases, so does the demand for comprehensive coverage that extends beyond typical launch and in-orbit failure policies. Insurers that can proactively design and offer flexible, modular policies capable of adapting to these new mission types will gain a competitive advantage and capture significant market share.

Furthermore, the increasing integration of satellite technology with terrestrial applications such as 5G networks, the Internet of Things (IoT), and autonomous vehicles creates new interdependencies and associated risks, thus generating new demand for integrated insurance solutions. The financial implications of satellite service disruptions are broadening, extending to various commercial sectors that rely on space-based connectivity and data. This broadening scope provides insurers with the opportunity to cross-sell and develop broader risk management portfolios that encompass the entire space-enabled value chain, solidifying their role as indispensable partners in the burgeoning space economy.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of New Space Nations and Commercial Players | +2.5% | Asia Pacific, Middle East & Africa, Latin America | 2025-2033 |

| Development of Innovative and Niche Insurance Products | +2.0% | Global | 2025-2033 |

| Integration of Space Tech with Terrestrial Applications (5G, IoT) | +1.8% | Global | 2028-2033 |

Satellite Launch and Space Insurance Market Challenges Impact Analysis

The Satellite Launch and Space Insurance Market confronts several significant challenges that could impede its growth and stability. A paramount challenge is the increasing threat of cyber risks targeting satellite ground infrastructure, command and control systems, and in-orbit assets. As satellites become more interconnected and integral to critical terrestrial services, they present attractive targets for malicious actors. A successful cyberattack could lead to data loss, system malfunction, or even loss of control over a satellite, resulting in substantial financial losses and complex liability disputes that are difficult to quantify and insure effectively within traditional frameworks.

Another key challenge arises from the rapid introduction of unproven or nascent space technologies, such as advanced propulsion systems, experimental satellite components, or novel mission profiles (e.g., asteroid mining). Insurers often lack sufficient historical data and established risk models to accurately assess the probability of failure for these cutting-edge innovations. This uncertainty can lead to highly conservative underwriting, exceedingly high premiums, or even a reluctance to provide coverage, potentially stifling technological advancement and investment in the nascent stages of new space ventures. The balance between fostering innovation and managing unquantifiable risk is delicate.

Furthermore, the escalating issue of space debris and the growing congestion in popular orbital paths present a significant and long-term challenge. The risk of collision, even with small debris fragments, can render expensive satellites inoperable, leading to substantial claims. While efforts are underway to mitigate debris, the sheer volume of existing fragments and the continuous deployment of new satellites heighten the probability of incidents. This necessitates a re-evaluation of current liability frameworks and potentially new insurance mechanisms that account for collective risk and the long-term sustainability of the space environment, adding complexity to policy design and claims management.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Escalating Cyber Risks in Space Operations | -1.8% | Global | 2025-2033 |

| Unproven Technologies and Lack of Historical Data | -1.4% | Global, particularly for startups | 2025-2030 |

| Increasing Space Debris and Orbital Congestion | -1.0% | Global | 2025-2033 |

Satellite Launch and Space Insurance Market - Updated Report Scope

This comprehensive market research report on the Satellite Launch and Space Insurance Market offers an in-depth analysis of the industry's current landscape, historical performance, and future growth trajectory. The scope includes a detailed examination of market size, trends, drivers, restraints, opportunities, and challenges across various segments and key geographical regions. It provides actionable insights for stakeholders, aiding in strategic decision-making and investment planning within the dynamic global space economy.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.8 Billion |

| Market Forecast in 2033 | USD 9.6 Billion |

| Growth Rate | 12.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Aon plc, Marsh McLennan, Willis Towers Watson, Swiss Re, Munich Re, Allianz Global Corporate & Specialty (AGCS), AXA XL, Hiscox Ltd., Liberty Mutual Insurance, Lockton Companies, United Launch Alliance (ULA), SpaceX, ArianeGroup, Blue Origin, Rocket Lab, Northrop Grumman Innovation Systems, Boeing, Airbus, Mitsubishi Heavy Industries (MHI), Safran S.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Satellite Launch and Space Insurance Market is comprehensively segmented to provide a granular understanding of its diverse components and evolving risk landscapes. This segmentation allows for precise analysis of market dynamics across different service types, launch vehicle technologies, satellite orbits, and end-use applications. Understanding these segments is crucial for insurers to tailor their offerings effectively and for operators to identify appropriate coverage solutions, reflecting the varied needs and risk profiles inherent in the global space industry.

The market is broadly categorized by the stage of the mission (Pre-launch, Launch, In-orbit, Third-party Liability, and Decommissioning), recognizing that different phases of a space mission entail distinct risk factors and require specialized insurance products. Further differentiation occurs based on the type of launch vehicle, acknowledging the unique risks associated with Expendable versus Reusable Launch Vehicles. The rapidly expanding satellite market is also segmented by orbital class—Geosynchronous Equatorial Orbit (GEO), Low Earth Orbit (LEO), and Medium Earth Orbit (MEO)—each presenting varying degrees of congestion, debris risk, and operational challenges that influence insurance policy design and pricing.

Finally, the market is segmented by end-use application, distinguishing between commercial operators, government and military entities, and academic/research institutions. Each end-user group has specific risk tolerances, regulatory compliance requirements, and budget constraints, which shape their demand for insurance products. This detailed segmentation provides a holistic view of the market, enabling stakeholders to identify high-growth areas, assess competitive landscapes, and formulate targeted strategies for engagement and investment in this complex and critical sector.

- By Service Type:

- Pre-launch Insurance: Covers risks during satellite manufacturing, testing, and transportation to the launch site.

- Launch Insurance: Protects against risks from ignition through successful orbital insertion.

- In-orbit Insurance: Covers satellite malfunction, degradation, or damage once operational in space.

- Third-Party Liability Insurance: Addresses damage or injury to third parties from launch or in-orbit activities.

- Decommissioning Insurance: Emerging segment for ensuring safe de-orbiting or disposal of satellites.

- By Launch Vehicle Type:

- Expendable Launch Vehicles (ELV) Insurance: Coverage for single-use rocket launches.

- Reusable Launch Vehicles (RLV) Insurance: Policies adapting to the unique risks of re-flight and refurbishment.

- By Satellite Type:

- Geosynchronous Equatorial Orbit (GEO) Satellite Insurance: For large, high-value satellites in geostationary orbit.

- Low Earth Orbit (LEO) Satellite Insurance: For constellations of smaller satellites, often with volume-based policies.

- Medium Earth Orbit (MEO) Satellite Insurance: Coverage for navigation and communication satellites in MEO.

- By End-Use Application:

- Commercial Insurance: Tailored for private operators, including telecommunications, Earth observation, and space tourism.

- Government & Military Insurance: For defense, intelligence, and scientific missions with specific national security considerations.

- Academic & Research Insurance: For university and research institution projects, often smaller satellites or experimental missions.

Regional Highlights

- North America: This region dominates the Satellite Launch and Space Insurance Market, largely due to the presence of major space agencies, leading commercial launch service providers, and innovative satellite manufacturers. The United States, in particular, boasts a robust private space industry with companies pioneering reusable launch technologies and large-scale satellite constellations, driving significant demand for comprehensive insurance coverage. The mature regulatory framework and a strong culture of risk management further solidify its leading position, making it a critical hub for both space operations and insurance underwriting.

- Europe: Europe represents a significant market, characterized by established state-backed space programs, a growing private space sector, and strong collaborative initiatives like the European Space Agency (ESA). Countries such as France, Germany, and the UK are key contributors, with robust manufacturing capabilities and increasing investment in satellite broadband and Earth observation. The region focuses on fostering a competitive launch market and addressing space debris, driving demand for both launch and in-orbit insurance, with a strong emphasis on international compliance and sustainable space practices.

- Asia Pacific (APAC): The APAC region is projected to be the fastest-growing market, propelled by ambitious national space programs in China, India, Japan, and South Korea, coupled with rapidly expanding commercial space ventures. Increasing satellite deployments for telecommunications, navigation, and remote sensing are fueling the demand for insurance. Government initiatives supporting local space industries and growing private sector investment are creating substantial opportunities for both domestic and international insurance providers to offer tailored solutions across the diverse and dynamic regional landscape.

- Latin America: While smaller in market share, Latin America is an emerging region with growing interest in satellite technology for connectivity, disaster management, and resource monitoring. Countries like Brazil, Mexico, and Argentina are developing their space capabilities, leading to an incremental but steady demand for launch and in-orbit insurance. The region's focus on bridging digital divides and enhancing national security through satellite applications presents long-term growth potential for space insurance providers willing to engage with nascent space programs and evolving risk profiles.

- Middle East and Africa (MEA): The MEA region is experiencing increasing investment in space infrastructure, driven by national ambitions for technological advancement, resource management, and secure communication. Countries such as the UAE, Saudi Arabia, and South Africa are launching their own satellites and developing indigenous space capabilities, consequently generating new demand for insurance products. As these nations establish and expand their space sectors, they represent an important, albeit developing, market for satellite launch and space insurance, focusing on fostering partnerships and knowledge transfer.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Satellite Launch and Space Insurance Market.- Aon plc

- Marsh McLennan

- Willis Towers Watson

- Swiss Re

- Munich Re

- Allianz Global Corporate & Specialty (AGCS)

- AXA XL

- Hiscox Ltd.

- Liberty Mutual Insurance

- Lockton Companies

- United Launch Alliance (ULA)

- SpaceX

- ArianeGroup

- Blue Origin

- Rocket Lab

- Northrop Grumman Innovation Systems

- Boeing

- Airbus

- Mitsubishi Heavy Industries (MHI)

- Safran S.A.

Frequently Asked Questions

What is the projected growth rate for the Satellite Launch and Space Insurance Market?

The Satellite Launch and Space Insurance Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2025 and 2033, driven by increasing commercial space activities and technological advancements.

How is AI impacting risk assessment in space insurance?

AI is transforming risk assessment by enabling more precise modeling, leveraging vast datasets for predicting failures, and automating underwriting processes. This leads to more dynamic, real-time risk evaluations and tailored premium structures.

What are the key drivers of growth in the Satellite Launch and Space Insurance Market?

Key drivers include the surge in commercial satellite launches, growing demand for satellite-based services, continuous technological advancements in the space industry, and increasing private sector investment in space ventures globally.

What challenges does the space insurance market face from unproven technologies?

The market faces challenges from a lack of historical data for nascent space technologies, leading to difficulties in accurate risk modeling. This can result in conservative underwriting, higher premiums, or reluctance to provide coverage for innovative missions.

Which region is expected to lead market growth and why?

North America is expected to lead the market due to the presence of major space agencies, leading commercial launch providers, and a robust private space industry, particularly in the United States, driving significant demand for comprehensive insurance.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted