Ultraviolet LED Market

Ultraviolet LED Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707225 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Ultraviolet LED Market Size

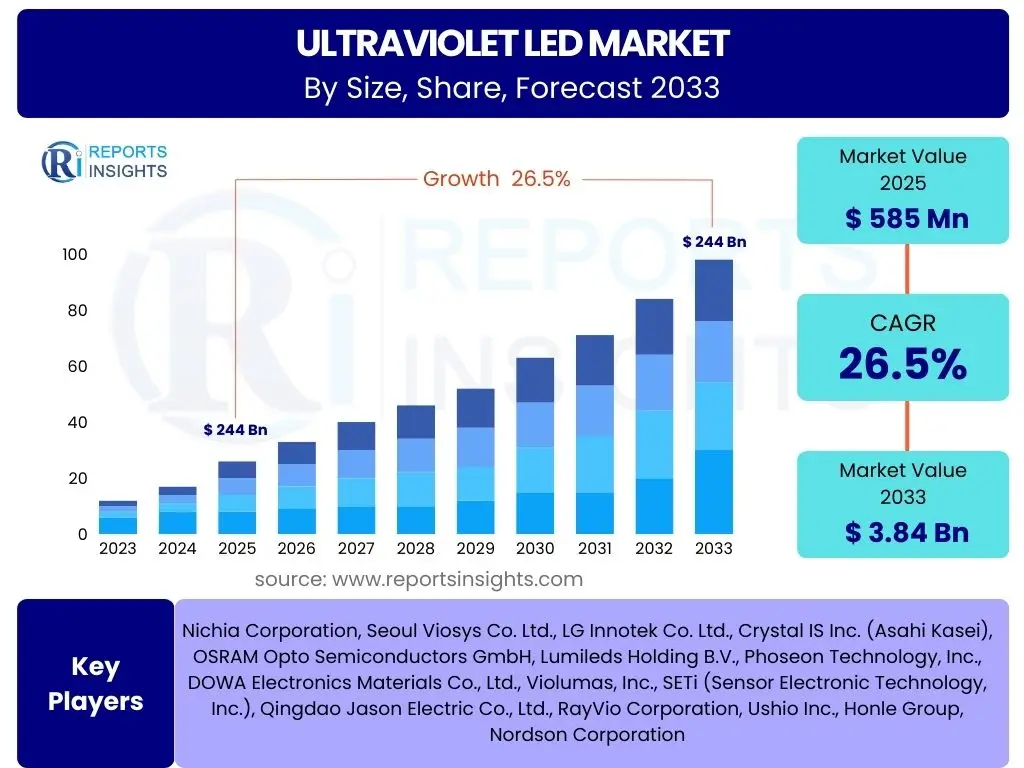

According to Reports Insights Consulting Pvt Ltd, The Ultraviolet LED Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 26.5% between 2025 and 2033. The market is estimated at USD 585 Million in 2025 and is projected to reach USD 3.84 Billion by the end of the forecast period in 2033.

Key Ultraviolet LED Market Trends & Insights

The Ultraviolet LED market is undergoing significant transformation, driven by technological advancements and increasing application diversity. Key trends indicate a strong shift towards mercury-free solutions, miniaturization, and enhanced energy efficiency. Users are primarily concerned with understanding how these innovations are expanding the utility of UV LEDs beyond traditional applications and what the long-term implications are for various industries. The market is witnessing a surge in demand for sterilization and disinfection, accelerated by global health concerns, leading to greater adoption in healthcare, consumer goods, and public infrastructure. Furthermore, the integration of smart features and connectivity into UV LED systems is gaining traction, allowing for more precise control and optimized performance.

Another prominent trend is the continuous improvement in UV LED power output and lifespan, addressing historical limitations and making them more viable for high-intensity industrial applications such as curing and water purification. The cost-effectiveness of these solutions is also improving over time, making them more competitive against conventional UV lamp technologies. There is a notable emphasis on developing specific wavelength UV LEDs (UVA, UVB, UVC) to cater to specialized applications, such as horticulture, medical phototherapy, and advanced sensing, showcasing the versatility and adaptable nature of the technology. The market is becoming increasingly fragmented, with various players focusing on niche applications and delivering customized solutions.

- Growing adoption of mercury-free UV solutions across industries.

- Increasing integration of UVC LEDs in disinfection and purification systems.

- Advancements in UV LED power output, efficiency, and lifespan.

- Miniaturization enabling new applications in consumer electronics and portable devices.

- Rising demand for UV LED technology in medical and healthcare sectors.

- Expansion into horticulture lighting and advanced material curing.

- Development of smart UV LED systems with IoT and connectivity features.

AI Impact Analysis on Ultraviolet LED

The integration of Artificial Intelligence (AI) is poised to significantly enhance the capabilities and efficiency of Ultraviolet LED systems. Common user questions often revolve around how AI can make UV LED applications smarter, more autonomous, and more effective. Users are interested in whether AI can optimize disinfection processes, improve energy consumption, or enable predictive maintenance. AI's impact is expected to manifest through intelligent control systems that can dynamically adjust UV intensity and exposure duration based on real-time environmental data or contamination levels, leading to more precise and energy-efficient operations. For instance, in water purification, AI could monitor water quality parameters and modulate UV LED output accordingly, rather than operating at a fixed, potentially excessive, level.

Furthermore, AI can revolutionize quality control and manufacturing processes for UV LEDs themselves. Through machine learning algorithms, production lines can identify defects, predict equipment failures, and optimize material usage, thereby improving the yield and reliability of UV LED components. In curing applications, AI can analyze material properties and cure rates to fine-tune UV exposure, ensuring optimal bonding and minimizing energy waste. This level of intelligent automation not only enhances performance but also contributes to greater cost-effectiveness and scalability of UV LED solutions across various industries. The potential for AI to drive more adaptive, predictive, and responsive UV LED systems represents a significant leap forward in their functionality and market appeal.

- Enabling intelligent, real-time control for optimized disinfection and purification.

- Facilitating predictive maintenance for UV LED systems, extending operational lifespan.

- Optimizing energy consumption through dynamic adjustment of UV intensity based on sensor data.

- Improving manufacturing processes and quality control for UV LED components.

- Automating precise UV curing and bonding applications based on material analysis.

- Enhancing diagnostic capabilities in medical and analytical instruments using UV LEDs.

Key Takeaways Ultraviolet LED Market Size & Forecast

The Ultraviolet LED market is on a trajectory of robust growth, primarily fueled by the increasing global emphasis on health, hygiene, and environmental sustainability. Key takeaways from the market size and forecast analysis reveal a significant shift from traditional mercury lamps to safer, more efficient UV LED alternatives across diverse applications. Users frequently inquire about the primary drivers of this growth and where the most significant opportunities lie. The market’s substantial projected CAGR underscores strong investor confidence and expanding adoption rates, signaling a pivotal period of innovation and market penetration. The forecast indicates that applications such as disinfection, water purification, and industrial curing will be major revenue contributors, alongside emerging sectors like horticulture and medical phototherapy.

This projected expansion is further supported by continuous advancements in UV LED technology, leading to higher power output, longer lifespans, and improved cost-efficiency. The market's resilience, demonstrated by accelerated demand during recent global health crises, highlights its essential role in public health and industrial processes. The strong growth anticipated through 2033 suggests a broad-based adoption across both developed and developing economies, driven by stricter environmental regulations and growing consumer awareness regarding germicidal solutions. Companies looking to capitalize on this trend are focusing on innovation, strategic partnerships, and expanding their product portfolios to meet specialized application demands.

- Market projected for substantial growth, driven by health, environmental, and technological factors.

- Shift towards mercury-free UV LED solutions is a primary growth catalyst.

- Disinfection, purification, and industrial curing remain dominant application areas.

- Emerging applications in horticulture, medical, and consumer electronics contribute to diversification.

- Technological advancements in efficiency, lifespan, and cost are key enablers.

- Strong demand across both developed and developing regions is expected.

Ultraviolet LED Market Drivers Analysis

The Ultraviolet LED market is primarily driven by a global push towards environmentally sustainable technologies and an escalating demand for advanced disinfection solutions. The increasing awareness regarding the hazards of mercury, coupled with stringent environmental regulations such as the Minamata Convention on Mercury, is compelling industries to adopt mercury-free UV LED alternatives. This regulatory pressure is a significant force, accelerating the transition from traditional mercury lamps, particularly in applications like water purification, air sterilization, and surface disinfection. As industries and governments seek cleaner and safer technologies, UV LEDs offer a viable and superior solution for various germicidal needs.

Furthermore, the growing demand for efficient and effective sterilization and purification across healthcare, consumer goods, and industrial sectors is a major market driver. The recent global focus on hygiene has significantly boosted the adoption of UVC LEDs in everyday products and public spaces. Technological advancements leading to improved power output, enhanced energy efficiency, and extended lifespan of UV LED devices have made them more competitive and appealing for high-volume applications. The miniaturization capabilities of UV LEDs also enable their integration into compact and portable devices, opening new avenues in consumer electronics and personal hygiene products. These combined factors create a robust growth environment for the Ultraviolet LED market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Mercury-Free Solutions | +5.2% | Global, especially Europe, North America, APAC | 2025-2033 |

| Growing Awareness of Hygiene and Disinfection | +4.8% | Global, particularly healthcare-intensive regions | 2025-2030 |

| Technological Advancements and Efficiency Improvements | +4.5% | Global, particularly leading R&D hubs (e.g., Japan, South Korea, US) | 2025-2033 |

| Miniaturization and Integration into Portable Devices | +3.9% | Global, prominent in consumer electronics markets | 2025-2030 |

Ultraviolet LED Market Restraints Analysis

Despite the promising growth trajectory, the Ultraviolet LED market faces several restraints that could impede its expansion. One significant challenge is the relatively high initial cost of UV LED systems compared to traditional mercury-vapor lamps, especially for high-power industrial applications. While the long-term operational benefits, such as energy efficiency and extended lifespan, can offset this cost, the upfront investment can be a barrier for some businesses, particularly small and medium-sized enterprises or those in developing regions with budget constraints. This cost disparity can slow down the rate of adoption, even when the technological advantages are clear.

Another restraint is the limited power output of some UV LEDs, historically making them less suitable for very large-scale or high-flux applications where conventional UV lamps still hold an advantage. While advancements are continually addressing this, achieving the same intensity and coverage as large traditional lamps, particularly for broad-area disinfection or rapid, high-volume curing, remains a development hurdle. Additionally, a lack of widespread standardization across different UV LED products and applications can lead to compatibility issues and complicate integration for end-users. The specific wavelength requirements for diverse applications (UVA for curing, UVC for germicidal) necessitate specialized product lines, adding complexity to manufacturing and distribution. These factors, combined with a persistent, albeit diminishing, lack of awareness or misperception about UV LED capabilities in certain sectors, can collectively moderate market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Cost Compared to Traditional Lamps | -3.5% | Global, particularly price-sensitive markets (e.g., Southeast Asia, Latin America) | 2025-2030 |

| Limited Power Output for Certain High-Intensity Applications | -2.8% | Industrial, large-scale purification sectors globally | 2025-2028 |

| Lack of Standardization and Varied Wavelength Requirements | -2.1% | Global, impacting market fragmentation and interoperability | 2025-2033 |

Ultraviolet LED Market Opportunities Analysis

The Ultraviolet LED market is poised to capitalize on several significant opportunities, driven by evolving technological landscapes and burgeoning application areas. A major opportunity lies in the expanding demand for point-of-use water purification systems, especially in regions with concerns about water quality. UV LEDs offer compact, efficient, and reliable solutions for on-demand water disinfection, making them ideal for consumer appliances, portable purifiers, and remote community water systems. This segment presents substantial untapped potential, particularly in developing economies where access to clean water is a critical issue and decentralized solutions are highly valued.

Another compelling opportunity emerges from the growing adoption of UV LEDs in horticultural lighting. Specific UV wavelengths can positively influence plant growth, disease resistance, and nutrient content, creating a niche but rapidly expanding market within controlled environment agriculture and vertical farming. As food security and sustainable farming practices become more crucial, the integration of UV LEDs into smart agricultural systems offers significant growth prospects. Furthermore, the increasing integration of UV LEDs into medical devices for diagnostics, phototherapy, and sterilization of medical instruments represents a high-value opportunity. The compact size, precise wavelength control, and immediate on/off capability of UV LEDs are highly advantageous for sensitive medical applications. The continuous development of novel materials and packaging techniques for UV LEDs is also opening doors for improved performance and new form factors, further expanding their application versatility.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Point-of-Use Water Purification Systems | +4.5% | Asia Pacific, Latin America, Africa, North America | 2025-2033 |

| Growing Applications in Horticultural Lighting | +3.8% | North America, Europe, Asia Pacific (vertical farming hubs) | 2025-2033 |

| Integration into Medical Devices and Diagnostics | +3.2% | North America, Europe, Japan, South Korea | 2025-2030 |

| Development of Novel Materials and Packaging Technologies | +2.9% | Global, particularly R&D intensive regions | 2025-2033 |

Ultraviolet LED Market Challenges Impact Analysis

The Ultraviolet LED market faces several challenges that require innovative solutions to sustain long-term growth. A primary challenge is effective thermal management. UV LEDs generate significant heat during operation, which can degrade performance and drastically reduce their lifespan if not dissipated efficiently. Overheating can lead to wavelength shift, decreased light output, and premature failure, thereby impacting reliability and return on investment for end-users. Addressing this requires sophisticated thermal design in product development, which can add to manufacturing complexity and cost.

Another significant challenge is ensuring public perception of safety regarding UV radiation. While UVC LEDs are highly effective for disinfection, improper exposure can be harmful to human skin and eyes. Educating users and implementing fail-safe mechanisms are crucial for broad consumer acceptance and responsible deployment, particularly in public and household applications. This necessitates clear safety guidelines, smart sensor integration, and user-friendly designs that prevent accidental exposure. Furthermore, the market is challenged by the need for continuous research and development to improve efficiency and power output across the entire UV spectrum, especially for UVC and UVB LEDs. Advancements in chip design, epitaxial growth, and packaging materials are vital to overcome current limitations and expand the applicability of UV LEDs into more demanding industrial and medical fields. Overcoming these technical and perception challenges is essential for the market to fully realize its potential.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Thermal Management and Heat Dissipation Issues | -3.0% | Global, particularly high-power applications | 2025-2033 |

| Ensuring Public Perception of Safety for UV Radiation | -2.5% | Global, especially consumer and public sector applications | 2025-2030 |

| Need for Continuous R&D to Improve Efficiency and Power Output | -2.0% | Global, particularly for UVC and UVB applications | 2025-2033 |

Ultraviolet LED Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the global Ultraviolet LED market, offering detailed insights into market size, growth drivers, restraints, opportunities, and challenges. It encompasses historical data from 2019 to 2023, with projections extending to 2033, enabling a thorough understanding of market dynamics and future trends. The report segments the market extensively by type, application, end-use industry, and geography, offering granular data for strategic decision-making. Key competitive landscape analysis, including profiles of leading companies, further enhances the report's value, presenting a holistic view of the industry for stakeholders and investors.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 585 Million |

| Market Forecast in 2033 | USD 3.84 Billion |

| Growth Rate | 26.5% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Nichia Corporation, Seoul Viosys Co. Ltd., LG Innotek Co. Ltd., Crystal IS Inc. (Asahi Kasei), OSRAM Opto Semiconductors GmbH, Lumileds Holding B.V., Phoseon Technology, Inc., DOWA Electronics Materials Co., Ltd., Violumas, Inc., SETi (Sensor Electronic Technology, Inc.), Qingdao Jason Electric Co., Ltd., RayVio Corporation, Ushio Inc., Honle Group, Nordson Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Ultraviolet LED market is broadly segmented to provide a granular view of its diverse applications and technological variations. This segmentation helps in understanding specific growth pockets and competitive landscapes within the broader market. The primary segmentation includes categorization by type, application, end-use industry, and power, each revealing unique market dynamics and contributing significantly to the overall market growth. Understanding these segments is crucial for stakeholders to identify key areas for investment, product development, and market penetration strategies. The versatility of UV LED technology allows for its tailored application across a wide array of sectors, necessitating detailed sub-segmentation to capture market nuances effectively.

The By Type segment differentiates between UVA, UVB, and UVC LEDs, each serving distinct purposes based on their unique wavelengths. UVA LEDs are predominantly used for curing and counterfeit detection, while UVB LEDs find applications in phototherapy and horticulture. UVC LEDs, with their germicidal properties, are crucial for disinfection and purification. The By Application segment highlights the major uses such as disinfection, curing, and medical, which are further broken down into specific sub-applications like water purification, air sterilization, and dental curing. Similarly, the By End-Use Industry segment categorizes the market based on the sectors adopting UV LEDs, including healthcare, consumer electronics, and industrial manufacturing, showcasing the broad industry impact. The By Power segment distinguishes between low-power and high-power solutions, reflecting different performance needs across applications. This multi-dimensional segmentation provides a robust framework for comprehensive market analysis and strategic planning.

- By Type:

- UV-A LED

- UV-B LED

- UV-C LED

- By Application:

- Disinfection & Purification (Water, Air, Surface)

- Curing (Adhesives, Inks, Coatings)

- Medical & Healthcare (Phototherapy, Diagnostics, Sterilization)

- Horticulture Lighting

- Sensing & Monitoring

- Others (Counterfeit Detection, Analytical Instruments)

- By End-Use Industry:

- Healthcare & Medical

- Consumer Electronics

- Automotive

- Industrial (Printing, Manufacturing)

- Water & Wastewater Treatment

- Air Purification

- Research & Development

- Others

- By Power:

- Low-Power UV LED

- High-Power UV LED

Regional Highlights

- North America: This region is characterized by early adoption of advanced technologies, strong healthcare infrastructure, and stringent environmental regulations. High demand for water and air purification solutions, coupled with significant R&D investments in UV LED technology, particularly for medical and industrial curing applications, drives market growth. The presence of key market players and a robust consumer electronics market also contributes significantly.

- Europe: Europe exhibits strong growth driven by increasing environmental awareness and regulations phasing out mercury-containing products. The region focuses heavily on sustainable technologies and smart city initiatives, leading to increased adoption of UV LEDs for water treatment, industrial curing, and disinfection in public spaces. Germany, France, and the UK are key contributors to market expansion due to their strong industrial and research bases.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, owing to rapid industrialization, burgeoning population, and increasing awareness of hygiene and public health. Countries like China, Japan, South Korea, and India are major manufacturing hubs for electronics and automotive, driving demand for UV LEDs in curing and sterilization applications. The urgent need for clean water and air solutions in highly populated urban areas further fuels market growth.

- Latin America: This region shows promising growth, primarily driven by increasing investments in infrastructure development and growing concerns over public health and waterborne diseases. The adoption of UV LED technology for point-of-use water purification and healthcare facilities is on the rise, though market penetration is still emerging compared to developed regions.

- Middle East and Africa (MEA): The MEA region is experiencing gradual adoption of UV LED technology, mainly driven by growing investments in healthcare infrastructure, industrial expansion, and water scarcity issues. Countries in the GCC are increasingly adopting advanced purification systems, while South Africa and other developing nations are exploring cost-effective disinfection solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Ultraviolet LED Market.- Nichia Corporation

- Seoul Viosys Co. Ltd.

- LG Innotek Co. Ltd.

- Crystal IS Inc. (Asahi Kasei)

- OSRAM Opto Semiconductors GmbH

- Lumileds Holding B.V.

- Phoseon Technology, Inc.

- DOWA Electronics Materials Co., Ltd.

- Violumas, Inc.

- SETi (Sensor Electronic Technology, Inc.)

- Qingdao Jason Electric Co., Ltd.

- RayVio Corporation

- Ushio Inc.

- Honle Group

- Nordson Corporation

Frequently Asked Questions

What is Ultraviolet LED technology primarily used for?

Ultraviolet LED technology is primarily used for disinfection and purification of water, air, and surfaces, industrial curing of inks, adhesives, and coatings, and various medical applications like phototherapy and diagnostics. Its compact size and mercury-free nature make it ideal for a growing range of applications.

How does UV LED differ from traditional UV lamps?

UV LEDs differ from traditional UV lamps primarily in their operational mechanism, environmental impact, and physical characteristics. UV LEDs are solid-state devices that are mercury-free, offer instant on/off capabilities, precise wavelength control, and a longer lifespan. Traditional UV lamps contain mercury, require warm-up time, and are fragile.

Is UV LED technology safe for human exposure?

While UV-A and UV-B LEDs have applications in tanning and medical phototherapy with controlled exposure, UV-C LEDs, used for germicidal purposes, are harmful to human skin and eyes with direct exposure. Products utilizing UV-C LEDs are designed with safety features to prevent direct exposure, such as automatic shut-offs or enclosed systems, ensuring safe operation.

What is the future outlook for the Ultraviolet LED market?

The future outlook for the Ultraviolet LED market is highly positive, driven by increasing demand for mercury-free solutions, advancements in technology leading to higher efficiency and lower costs, and expanding applications in disinfection, medical, and horticulture sectors. The market is projected for substantial growth through 2033.

What are the main types of Ultraviolet LEDs available?

The main types of Ultraviolet LEDs are categorized by their wavelength range: UV-A (315-400 nm) used for curing and counterfeit detection; UV-B (280-315 nm) for medical phototherapy and horticulture; and UV-C (100-280 nm), known for its germicidal properties in disinfection and purification applications.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted