Micro LED Market

Micro LED Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707005 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

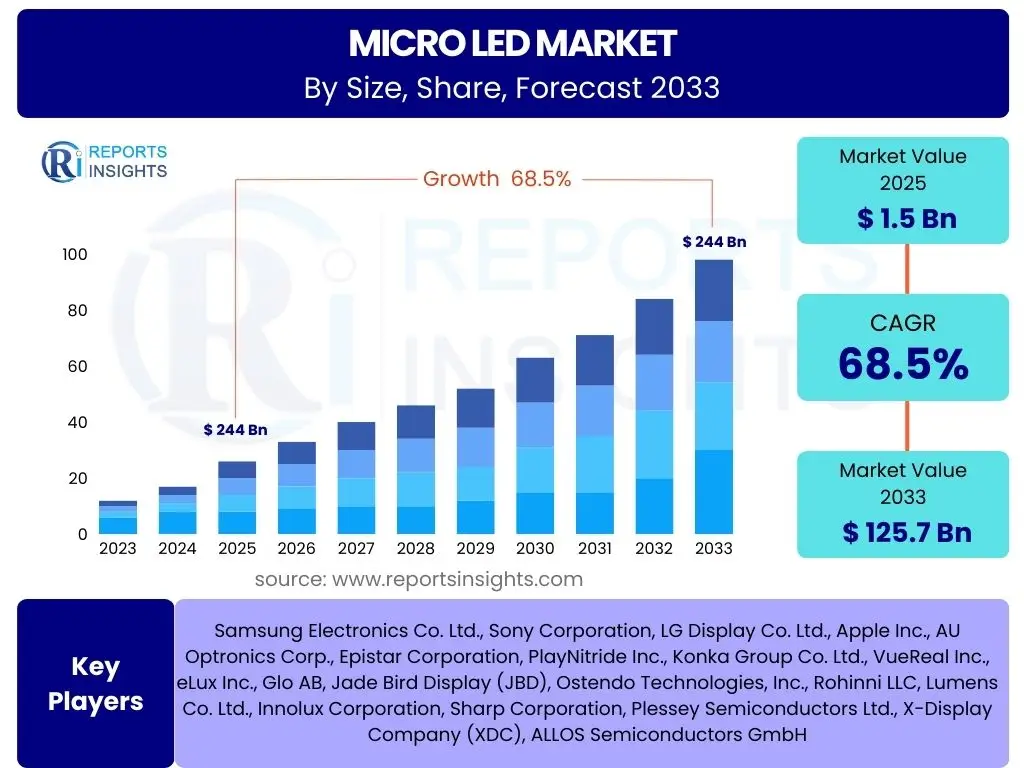

Micro LED Market Size

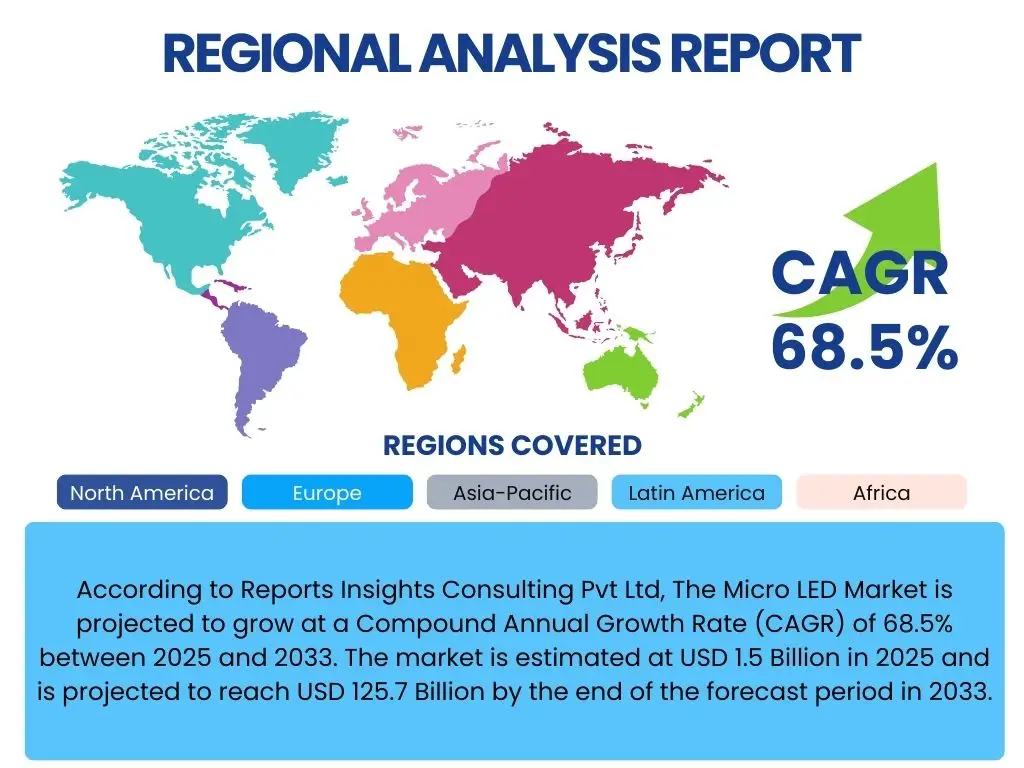

According to Reports Insights Consulting Pvt Ltd, The Micro LED Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 68.5% between 2025 and 2033. The market is estimated at USD 1.5 Billion in 2025 and is projected to reach USD 125.7 Billion by the end of the forecast period in 2033.

Key Micro LED Market Trends & Insights

The Micro LED market is witnessing significant transformative trends, primarily driven by the relentless pursuit of superior display performance and energy efficiency across various industries. Users are keenly interested in understanding how this nascent technology is evolving, particularly regarding its practical applications, manufacturing feasibility, and potential to displace existing display technologies. Key inquiries revolve around the progress in miniaturization, improvements in pixel density, and breakthroughs in mass transfer techniques that are crucial for scaling production.

Current insights suggest a strong momentum towards developing Micro LED displays for high-end consumer electronics, including augmented reality (AR) and virtual reality (VR) headsets, smartwatches, and premium televisions, where its unparalleled brightness, contrast, and response times offer a distinct advantage. Additionally, the automotive sector and specialized commercial displays are emerging as significant growth areas, capitalizing on Micro LED's durability and superior visual quality. The industry is also focused on overcoming manufacturing complexities and reducing production costs to facilitate broader market adoption, signaling a shift from niche luxury items to more mainstream applications in the long term.

- Miniaturization of LED chips enabling ultra-high pixel densities.

- Advancements in mass transfer technology to improve manufacturing yield and scalability.

- Increasing adoption in augmented reality (AR) and virtual reality (VR) devices.

- Expansion into large-format displays for commercial and home cinema applications.

- Growing interest from the automotive sector for advanced display solutions.

- Focus on energy efficiency and extended display lifespan.

- Development of flexible and transparent Micro LED displays for novel applications.

- Strategic collaborations and increased investment in R&D to accelerate innovation.

AI Impact Analysis on Micro LED

The integration of Artificial Intelligence (AI) is set to profoundly impact the Micro LED market, addressing some of its most persistent challenges, particularly in manufacturing and quality control. Common user questions often explore how AI can enhance the precision of micro-transfer processes, improve defect detection, and optimize overall production efficiency. There is a strong expectation that AI will be a critical enabler for scaling Micro LED production, moving it from a highly specialized, manual process to a more automated and high-volume manufacturing paradigm.

AI's influence extends beyond the production line, impacting material science research, display performance optimization, and even supply chain management within the Micro LED ecosystem. Users anticipate AI algorithms will accelerate the discovery of new materials, predict and prevent failures in complex display architectures, and dynamically adjust display characteristics for optimal viewing experiences. While concerns about the initial investment in AI infrastructure exist, the overwhelming sentiment points towards AI as an indispensable tool for achieving the performance, reliability, and cost-effectiveness required for Micro LED technology to reach its full market potential.

- Enhanced precision and speed in mass transfer processes through AI-driven robotics and vision systems.

- Automated defect detection and classification on microscopic scales, significantly improving yield rates.

- Optimization of display performance parameters (brightness, color uniformity, power consumption) using AI algorithms.

- Predictive maintenance for manufacturing equipment, minimizing downtime and increasing operational efficiency.

- Accelerated material discovery and characterization for new Micro LED components using AI-powered simulations.

- Intelligent supply chain management for sourcing specialized materials and components.

- Personalization of display content and adaptive display technologies based on user preferences and environmental conditions.

Key Takeaways Micro LED Market Size & Forecast

Analyzing common inquiries about the Micro LED market's trajectory reveals a strong desire to understand its long-term viability, investment potential, and eventual market penetration against established display technologies. Users are particularly interested in whether the projected growth rates are sustainable and what specific factors will underpin the transition of Micro LED from a niche, high-cost technology to a more broadly accessible solution. The consensus among market analysts points towards a period of exponential growth, driven by continuous technological breakthroughs and expanding application diversity.

The primary insights suggest that while initial adoption will remain concentrated in premium and specialized segments due to current cost structures, ongoing advancements in manufacturing efficiency and economies of scale are expected to significantly drive down prices over the forecast period. This will unlock opportunities in mainstream consumer electronics and beyond, positioning Micro LED as a formidable competitor to OLED and LCD. The market's future is heavily reliant on sustained R&D investment, successful resolution of remaining technical hurdles, and the establishment of robust supply chains, all of which contribute to a highly optimistic yet challenging growth outlook.

- The Micro LED market is poised for exceptional growth, driven by technological maturity and increasing demand for superior displays.

- High-end consumer electronics and specialized industrial applications will drive initial revenue.

- Significant investments in R&D and manufacturing scale-up are crucial for cost reduction and market expansion.

- Overcoming technical challenges such as mass transfer efficiency and yield rates is key to unlocking broader adoption.

- Strategic partnerships among component suppliers, display manufacturers, and end-product developers will accelerate market development.

- The long-term outlook suggests Micro LED could become a dominant display technology across various sectors.

Micro LED Market Drivers Analysis

The Micro LED market is propelled by a confluence of technological advancements and evolving consumer and industrial demands. A primary driver is the escalating requirement for displays offering superior performance characteristics, including higher brightness, exceptional contrast ratios, faster response times, and increased energy efficiency, particularly in portable and immersive devices. The inherent advantages of Micro LED technology over traditional display types like LCD and OLED in these areas make it highly attractive for next-generation applications.

Furthermore, the increasing miniaturization of electronic components and the growing popularity of augmented reality (AR), virtual reality (VR), and wearable devices are creating a robust demand for ultra-small, high-resolution displays where Micro LED excels. Significant investments in research and development by leading technology companies and governments are also accelerating the commercialization of Micro LED, pushing innovations in manufacturing processes and material science. This strong foundational support, coupled with the drive for energy-efficient and long-lasting display solutions, acts as a powerful catalyst for market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Premium Displays | +15.0% | North America, Europe, Asia Pacific | 2025-2033 |

| Growing Adoption in AR/VR and Wearable Devices | +12.5% | Global, particularly North America, APAC | 2025-2033 |

| Advancements in Manufacturing Technology | +10.0% | Asia Pacific (South Korea, Taiwan, Japan), Europe | 2025-2033 |

| Focus on Energy Efficiency and Durability | +8.0% | Global | 2025-2033 |

| Rising R&D Investments and Strategic Partnerships | +7.5% | Global | 2025-2033 |

Micro LED Market Restraints Analysis

Despite its significant potential, the Micro LED market faces several formidable restraints that could impede its rapid widespread adoption. A primary challenge is the prohibitively high manufacturing cost associated with current production techniques, particularly the precise mass transfer of millions of microscopic LEDs onto a substrate. This complexity significantly increases production expenses, making Micro LED products considerably more expensive than competing display technologies like OLED and LCD, thereby limiting their market to ultra-premium segments.

Another critical restraint is the technical complexity involved in achieving high yield rates and uniform pixel density across large display panels. The process demands extreme precision and cleanliness, and even minor imperfections can lead to significant material waste and production losses. Furthermore, the nascent stage of the Micro LED supply chain, characterized by limited availability of specialized equipment and raw materials, adds to the production bottleneck. Competition from established and continuously evolving display technologies, which offer comparable performance at a lower cost, also presents a substantial barrier to Micro LED's market penetration, requiring significant technological breakthroughs to overcome.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs | -18.0% | Global | 2025-2029 (Higher initial impact) |

| Technical Complexities (Mass Transfer, Yield Rates) | -15.0% | Global | 2025-2030 |

| Limited Supply Chain Maturity | -10.0% | Global | 2025-2028 |

| Intense Competition from Established Display Technologies | -8.0% | Global | 2025-2033 |

| Power Efficiency and Heat Dissipation Challenges for Smaller Pixels | -5.0% | Global | 2025-2033 |

Micro LED Market Opportunities Analysis

The Micro LED market is rife with significant opportunities that promise to unlock substantial growth and market expansion over the forecast period. A key opportunity lies in the burgeoning demand for immersive technologies like augmented reality (AR) and virtual reality (VR), where Micro LED's ability to deliver extremely high pixel densities, brightness, and fast refresh rates is unparalleled. This positions the technology as a crucial enabler for next-generation headsets and smart glasses, offering experiences that current display technologies struggle to match.

Furthermore, the automotive sector presents a compelling opportunity, with Micro LED poised to revolutionize in-car displays, heads-up displays (HUDs), and even exterior lighting. Its superior brightness and wide operating temperature range make it ideal for demanding automotive environments, enhancing both safety and user experience. Beyond these, the potential for Micro LED in flexible, transparent, and even rollable displays opens up entirely new product categories and form factors across various consumer and industrial applications, offering significant differentiation. As manufacturing processes mature and costs decline, these novel applications will become increasingly viable, driving substantial market penetration.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Advanced AR/VR Applications | +16.0% | Global, especially North America, Asia Pacific | 2025-2033 |

| Integration into Automotive Displays and Lighting | +13.5% | Europe, North America, Asia Pacific | 2026-2033 |

| Development of Flexible and Transparent Displays | +11.0% | Global | 2027-2033 |

| Growing Demand for Large-Format Commercial Displays | +9.0% | Asia Pacific, North America, Europe | 2025-2033 |

| Potential for Cost Reduction through Mass Production | +8.5% | Global, especially Asia Pacific | 2028-2033 |

Micro LED Market Challenges Impact Analysis

The Micro LED market, while promising, faces significant technical and economic challenges that demand innovative solutions for widespread adoption. One of the most critical technical hurdles is the "mass transfer" process, which involves precisely picking and placing millions of microscopic LED chips onto a substrate. Achieving this with high speed, accuracy, and an acceptable yield rate is exceedingly complex and directly impacts manufacturing costs and scalability. Failures in this process can lead to dead pixels or imperfect displays, making it a major bottleneck.

Economically, the current high cost of production remains a substantial barrier. This is driven not only by the intricate manufacturing processes but also by the specialized equipment and materials required, which are currently produced in limited volumes. Additionally, ensuring uniform color and brightness across a vast array of tiny LEDs presents a significant optoelectronic challenge, requiring sophisticated calibration and control mechanisms. Addressing these challenges effectively will be paramount for Micro LED technology to transition from high-end niche products to mainstream consumer devices and achieve its projected growth trajectory.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Mass Transfer Technology Limitations | -17.0% | Global | 2025-2029 (Significant initial impact) |

| Achieving High Yield Rates and Reliability | -14.5% | Global | 2025-2030 |

| High Research and Development Investment Requirements | -10.0% | Global | 2025-2033 |

| Color and Brightness Uniformity Across Pixels | -8.0% | Global | 2025-2033 |

| Developing Robust and Scalable Manufacturing Infrastructure | -7.0% | Global | 2025-2033 |

Micro LED Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Micro LED market, offering insights into its current state, key trends, drivers, restraints, opportunities, and future growth projections. The scope encompasses detailed segmentation analysis by application, panel size, end-use, and type, alongside a thorough regional assessment to provide a holistic understanding of market dynamics and competitive landscapes.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.5 Billion |

| Market Forecast in 2033 | USD 125.7 Billion |

| Growth Rate | 68.5% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Samsung Electronics Co. Ltd., Sony Corporation, LG Display Co. Ltd., Apple Inc., AU Optronics Corp., Epistar Corporation, PlayNitride Inc., Konka Group Co. Ltd., VueReal Inc., eLux Inc., Glo AB, Jade Bird Display (JBD), Ostendo Technologies, Inc., Rohinni LLC, Lumens Co. Ltd., Innolux Corporation, Sharp Corporation, Plessey Semiconductors Ltd., X-Display Company (XDC), ALLOS Semiconductors GmbH |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Micro LED market is segmented across various dimensions to provide a granular view of its diverse applications and technological manifestations. This segmentation helps in understanding specific market dynamics, identifying high-growth areas, and recognizing the particular requirements of different end-user industries. The key segments include applications in display and lighting, categorized further by the end-product, as well as by the physical dimensions of the panels and the type of Micro LED technology deployed.

By dissecting the market into these specific segments, stakeholders can gain precise insights into where Micro LED technology is gaining the most traction and where future opportunities lie. For instance, the demand for Micro LED in AR/VR devices underscores its role in immersive experiences, while its application in automotive displays highlights its robustness and superior visual performance in demanding environments. This structured analysis is crucial for strategic planning and investment decisions within the evolving Micro LED landscape.

- By Application:

- Display: Smartwatch, Television, Smartphone & Tablet, AR/VR Devices, Automotive Display, Laptops & Monitors, Digital Signage

- Lighting: General Lighting, Automotive Lighting, Others

- By Panel Size:

- Micro Displays (Under 2 inches)

- Small & Medium Displays (2-12 inches)

- Large Displays (Over 12 inches)

- By End-Use:

- Consumer Electronics

- Automotive

- Healthcare

- Retail & Hospitality

- Aerospace & Defense

- Others

- By Type:

- Chip-scale Micro LED

- Module-based Micro LED

Regional Highlights

- North America: Leads in Micro LED research and development, particularly for AR/VR devices and high-end consumer electronics. Strong presence of key technology innovators and early adopters. Significant investments in next-generation display technologies.

- Europe: Emerging as a significant market, driven by the automotive sector's demand for advanced display solutions and strong industrial automation. Growing focus on high-quality and energy-efficient displays for various applications.

- Asia Pacific (APAC): The dominant region in terms of manufacturing capabilities and consumer electronics production. Countries like South Korea, Taiwan, Japan, and China are at the forefront of Micro LED panel fabrication and supply chain development. High demand for consumer electronics, including smartphones, TVs, and wearables, fuels market growth.

- Latin America: A nascent but growing market with increasing interest in adopting advanced display technologies as disposable incomes rise and technology penetration expands. Opportunities for Micro LED in large format displays and premium consumer electronics.

- Middle East and Africa (MEA): Represents a developing market with potential growth in luxury consumer goods and commercial display applications. Increasing government initiatives for smart city development and technological infrastructure improvements are expected to drive demand.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Micro LED Market.- Samsung Electronics Co. Ltd.

- Sony Corporation

- LG Display Co. Ltd.

- Apple Inc.

- AU Optronics Corp.

- Epistar Corporation

- PlayNitride Inc.

- Konka Group Co. Ltd.

- VueReal Inc.

- eLux Inc.

- Glo AB

- Jade Bird Display (JBD)

- Ostendo Technologies, Inc.

- Rohinni LLC

- Lumens Co. Ltd.

- Innolux Corporation

- Sharp Corporation

- Plessey Semiconductors Ltd.

- X-Display Company (XDC)

- ALLOS Semiconductors GmbH

Frequently Asked Questions

Analyze common user questions about the Micro LED market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Micro LED technology?

Micro LED is an emerging display technology that uses microscopic light-emitting diodes, typically less than 100 micrometers, to form individual pixel elements. Each pixel generates its own light, offering superior brightness, contrast, color accuracy, and energy efficiency compared to traditional LCD or OLED displays. This technology eliminates the need for backlights, enabling thinner, more flexible, and potentially transparent display designs.

What are the primary advantages of Micro LED over OLED?

Micro LED displays offer several key advantages over OLED, including significantly higher brightness (up to 10,000 nits or more), greater energy efficiency at high brightness levels, longer lifespan without risk of burn-in, and superior durability. They also boast faster response times and the potential for greater pixel density, making them ideal for high-demanding applications like AR/VR headsets and outdoor digital signage.

When will Micro LED displays become widely available for consumers?

While Micro LED displays are currently available in niche, high-end segments such as ultra-premium televisions and specialized commercial displays, widespread consumer availability, particularly for smartphones and mainstream TVs, is anticipated to occur in the late 2020s to early 2030s. This timeline is contingent upon significant advancements in mass transfer technology, improvements in manufacturing yield rates, and substantial cost reductions through economies of scale.

What are the main applications driving the Micro LED market?

The primary applications driving the Micro LED market include high-end televisions and large-format commercial displays, where its superior visual performance is highly valued. Additionally, its compact size and high brightness make it ideal for augmented reality (AR) and virtual reality (VR) headsets, smartwatches, and other wearable devices. The automotive industry is also a significant driver, with Micro LED poised to enhance in-car displays and heads-up displays (HUDs).

What are the key challenges in Micro LED manufacturing?

The key challenges in Micro LED manufacturing revolve around the mass transfer process, which requires precise placement of millions of microscopic LEDs onto a substrate with high accuracy and speed. Other significant challenges include achieving high yield rates, ensuring uniform color and brightness across all pixels, reducing overall production costs, and developing a mature and robust supply chain for specialized materials and equipment. Overcoming these hurdles is essential for scalable and cost-effective production.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted