Ultrapure Water Equipment Market

Ultrapure Water Equipment Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707380 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

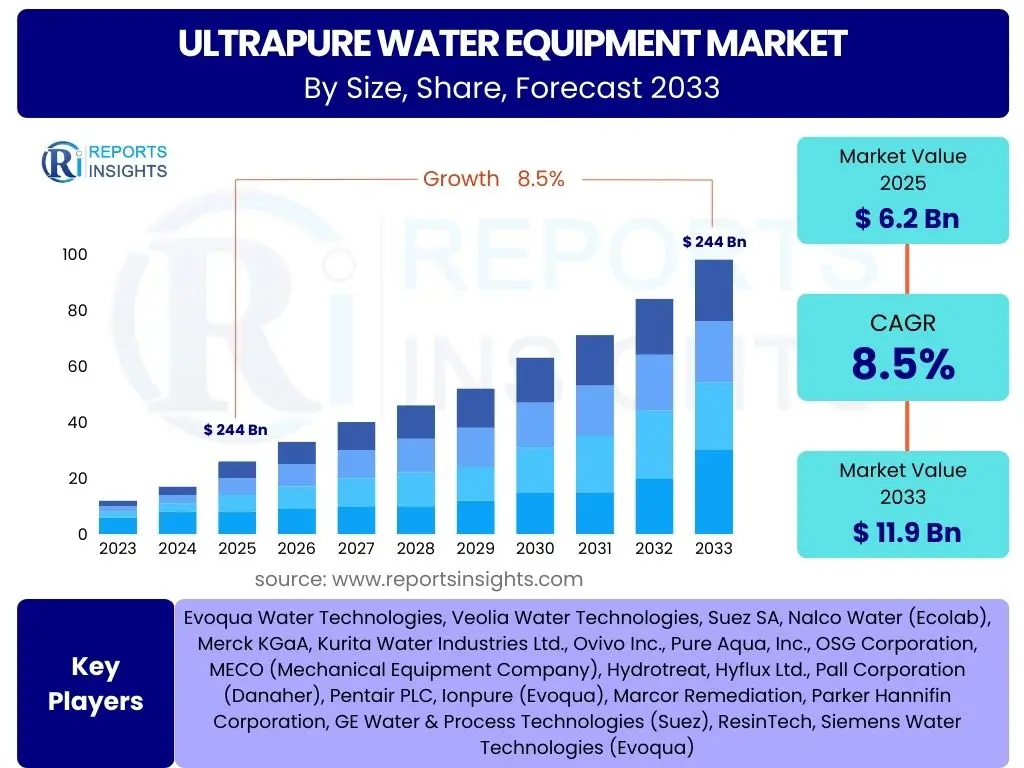

Ultrapure Water Equipment Market Size

The Ultrapure Water Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 6.2 billion in 2025 and is projected to reach USD 11.9 billion by the end of the forecast period in 2033.

Key Ultrapure Water Equipment Market Trends & Insights

The Ultrapure Water (UPW) equipment market is experiencing significant shifts driven by technological advancements and evolving industrial demands. Users frequently inquire about the latest innovations, how efficiency is being improved, and the adoption of smart technologies. There is a strong focus on solutions that reduce operational costs, minimize environmental impact, and ensure consistent water quality for highly sensitive applications. The integration of digital solutions for monitoring and control is becoming a prevalent theme.

Furthermore, inquiries often highlight the increasing importance of modular and compact UPW systems, especially for facilities with limited space or those requiring scalable solutions. The drive towards sustainability is also a key trend, with a rising interest in water recycling and reuse within UPW processes. This indicates a market moving towards more intelligent, efficient, and environmentally responsible water treatment methodologies.

- Growing adoption of modular and compact UPW systems for enhanced flexibility and scalability.

- Integration of advanced sensor technologies and real-time monitoring for precise quality control.

- Increased focus on water recycling and reclamation solutions within UPW generation to promote sustainability.

- Development of energy-efficient purification technologies to reduce operational expenditures.

- Customization of UPW systems to meet specific industry standards and evolving purity requirements.

AI Impact Analysis on Ultrapure Water Equipment

The integration of Artificial Intelligence (AI) in the Ultrapure Water (UPW) equipment sector is a rapidly emerging area of interest. Common user questions revolve around how AI can enhance the efficiency and reliability of UPW systems, the specific applications of machine learning in water treatment, and the potential for predictive maintenance. Users are keen to understand how AI can help optimize complex purification processes, reduce human error, and provide deeper insights into system performance. The expectation is that AI will move UPW systems beyond traditional automation to truly intelligent operations.

Concerns often include the initial investment costs associated with AI implementation, data security, and the need for specialized skills to manage AI-driven systems. However, the overarching expectation is that AI will revolutionize UPW production by enabling predictive analytics for component failure, optimizing chemical dosing, and fine-tuning filtration processes for maximum purity and minimal waste. This shift represents a move towards more proactive and adaptive UPW management.

- Predictive maintenance capabilities reducing downtime and optimizing equipment lifespan.

- Real-time process optimization for chemical dosing, filtration rates, and energy consumption.

- Enhanced data analytics for identifying subtle shifts in water quality and system performance.

- Automated fault detection and diagnostics, leading to faster problem resolution.

- Improved energy efficiency through intelligent control of pumps and purification stages.

Key Takeaways Ultrapure Water Equipment Market Size & Forecast

Analysis of user inquiries concerning the Ultrapure Water (UPW) equipment market size and forecast reveals a strong interest in understanding the primary growth catalysts and the longevity of market expansion. Users frequently ask about which industries are driving the most demand and how geopolitical factors or technological shifts might influence future market trajectories. The consensus points towards a robust market propelled by increasing stringency in purity standards across various high-tech industries.

The semiconductor and pharmaceutical sectors consistently emerge as the most significant contributors to market growth, with their continuous innovation and expansion necessitating ever-higher levels of water purity. Geographical expansion, particularly in emerging Asian markets, also presents a substantial growth avenue. Overall, the market is characterized by consistent demand for advanced purification technologies that can meet evolving requirements for product quality and operational efficiency.

- The market is poised for consistent growth, driven by escalating demands for high-purity water in critical industrial applications.

- Semiconductor manufacturing remains the largest and fastest-growing end-use sector, profoundly influencing market dynamics.

- Pharmaceutical and biotechnology industries are significant contributors, with stringent regulatory requirements fueling demand for advanced UPW systems.

- Technological advancements in filtration, ion exchange, and membrane separation are key enablers of market expansion.

- Asia Pacific is projected to be the leading region for market growth due to rapid industrialization and expansion of high-tech manufacturing.

Ultrapure Water Equipment Market Drivers Analysis

The Ultrapure Water (UPW) equipment market is primarily propelled by the exponential growth and technological advancements within key end-use industries. The semiconductor industry, with its continuous pursuit of smaller and more complex chip designs, demands water with virtually zero impurities, making UPW indispensable. This requirement extends to cleaning, etching, and rinsing processes where even trace contaminants can lead to defects and yield losses. Similarly, the pharmaceutical and biotechnology sectors rely heavily on UPW for drug formulation, active pharmaceutical ingredient (API) production, and equipment sterilization, where product purity directly impacts efficacy and patient safety.

Stringent regulatory frameworks globally, especially in healthcare and electronics, mandate the use of high-purity water, thereby compelling industries to invest in advanced UPW systems. These regulations are continually evolving, pushing equipment manufacturers to innovate and provide solutions capable of achieving ever-higher levels of purification. Furthermore, the expansion of research and development activities across various scientific fields, including nanotechnology and material science, also drives the demand for UPW as a critical reagent or solvent.

The increasing focus on sustainable practices and water conservation initiatives also subtly drives the market. Industries are looking for UPW systems that not only deliver purity but also optimize water usage and allow for effective wastewater management, including the potential for water reuse. This encourages investment in efficient and integrated UPW solutions that minimize environmental footprint while maximizing operational output.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Semiconductor Manufacturing | +1.5% | Asia Pacific (China, Taiwan, South Korea), North America | Long-term (2025-2033) |

| Increasing Demand from Pharmaceutical & Biotechnology Sectors | +1.0% | North America, Europe, Asia Pacific | Medium-term (2025-2030) |

| Strict Regulatory Standards for Water Purity | +0.8% | Global, particularly developed economies | Continuous |

| Technological Advancements in Material Science & Nanotechnology | +0.7% | Global Research Hubs | Long-term (2028-2033) |

| Growing Awareness of Water Conservation & Reuse | +0.5% | Global, especially water-stressed regions | Medium-term (2025-2030) |

Ultrapure Water Equipment Market Restraints Analysis

Despite the robust growth drivers, the Ultrapure Water (UPW) equipment market faces several significant restraints that can impede its expansion. One of the primary barriers is the high capital expenditure associated with establishing and upgrading UPW systems. These systems involve complex multi-stage purification processes, high-grade materials, and sophisticated instrumentation, all contributing to substantial upfront investment costs. For smaller or emerging industries, this initial financial burden can be a deterrent, limiting broader adoption.

Beyond the initial investment, the operational costs of UPW systems are also considerable. These expenses include significant energy consumption for pumps and membrane filtration, regular replacement of consumables such as resins and filters, and the need for highly skilled personnel for system operation and maintenance. The continuous monitoring and stringent quality control required to maintain UPW standards further add to the operational complexity and cost, making it a demanding long-term commitment for end-users.

Furthermore, the dependency on a reliable source of feed water and the challenges associated with managing the wastewater produced during the purification process present additional hurdles. Fluctuations in raw water quality can necessitate more intensive pre-treatment, increasing both capital and operational costs. The disposal of concentrated brine and spent resins also poses environmental and logistical challenges, requiring specialized waste management solutions that add to the overall expense and complexity of running UPW facilities.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Investment for System Setup | -0.8% | Global, particularly for new entrants | Continuous |

| Significant Operating and Maintenance Costs | -0.7% | Global | Continuous |

| Complexities in Wastewater Management and Disposal | -0.6% | Global, regions with strict environmental regulations | Continuous |

| Dependence on Consistent Raw Water Quality | -0.5% | Global, especially water-stressed areas | Continuous |

| Requirement for Highly Skilled Workforce | -0.4% | Global | Continuous |

Ultrapure Water Equipment Market Opportunities Analysis

The Ultrapure Water (UPW) equipment market is presented with numerous growth opportunities, particularly in emerging economies and through continuous technological innovation. Rapid industrialization and the expansion of manufacturing capabilities in regions like Asia Pacific, Latin America, and the Middle East offer vast untapped potential. As these regions develop their semiconductor, pharmaceutical, and power generation sectors, the demand for high-purity water systems is expected to surge, creating new market entry points and investment avenues for equipment providers.

Technological advancements, including the integration of IoT, AI, and advanced sensor technologies, are opening new frontiers for system optimization, predictive maintenance, and real-time quality assurance. This allows for the development of smarter, more efficient, and remotely manageable UPW systems that can adapt to changing operational parameters and purity requirements. The ongoing miniaturization of electronic components and the development of new biotechnological processes will continue to push the boundaries of water purity, creating opportunities for specialized and ultra-high-performance equipment.

Furthermore, the increasing global emphasis on environmental sustainability and circular economy principles is fostering opportunities for solutions that enable water reuse and waste minimization within UPW systems. Companies that can offer integrated solutions for water recycling, brine recovery, and energy-efficient purification will find significant market advantage. The shift towards modular and standardized UPW solutions also offers opportunities for manufacturers to reduce lead times, simplify installation, and cater to a wider range of facility sizes and operational needs.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Markets & Industrial Hubs | +1.2% | Asia Pacific, Latin America, Middle East & Africa | Long-term (2025-2033) |

| Integration of IoT, AI, and Automation in Systems | +1.0% | Global | Medium-term (2025-2030) |

| Increasing Adoption of Modular and Decentralized Systems | +0.9% | Global, particularly for smaller facilities | Medium-term (2025-2030) |

| Focus on Water Recycling and Sustainable UPW Solutions | +0.7% | Global, regions with water scarcity concerns | Long-term (2028-2033) |

| Growth in Niche Applications (e.g., Quantum Computing, Advanced Materials) | +0.6% | Global Research & Development Centers | Long-term (2028-2033) |

Ultrapure Water Equipment Market Challenges Impact Analysis

The Ultrapure Water (UPW) equipment market faces a complex array of challenges that can impact its growth trajectory and operational efficiency. One significant challenge is the continually evolving and increasingly stringent regulatory landscape for water purity, particularly in sensitive sectors like semiconductors and pharmaceuticals. Meeting these escalating standards requires constant investment in research and development, system upgrades, and sophisticated monitoring technologies, which can be a financial and technical burden for manufacturers and end-users alike.

Another major challenge pertains to supply chain disruptions and the volatility of raw material prices. The specialized components, membranes, and resins used in UPW systems often rely on global supply chains, making them vulnerable to geopolitical tensions, trade disputes, and unforeseen events. Such disruptions can lead to delays in manufacturing, increased production costs, and ultimately, higher prices for end-users, affecting market competitiveness and project timelines. Maintaining consistent quality and system reliability over long operational periods also presents a formidable technical challenge.

Furthermore, the scarcity of highly skilled technical personnel capable of designing, installing, operating, and maintaining advanced UPW systems poses a significant hurdle. The complexity of these systems demands specialized knowledge in water chemistry, filtration technologies, automation, and regulatory compliance. This talent gap can lead to operational inefficiencies, increased maintenance costs, and potential risks to water quality, highlighting the need for robust training programs and talent development within the industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Adherence to Evolving Purity Standards & Regulations | -0.9% | Global | Continuous |

| Supply Chain Volatility and Raw Material Price Fluctuations | -0.8% | Global | Medium-term (2025-2027) |

| Scarcity of Skilled Workforce for Operation & Maintenance | -0.7% | Global | Continuous |

| High Energy Consumption & Environmental Footprint | -0.6% | Global, especially regions with high energy costs | Continuous |

| Managing Biofouling and Membrane Degradation | -0.5% | Global | Continuous |

Ultrapure Water Equipment Market - Updated Report Scope

This report provides a comprehensive analysis of the Ultrapure Water Equipment Market, offering detailed insights into its current size, historical performance, and future growth projections. It delves into the critical factors influencing market dynamics, including key drivers, restraints, opportunities, and challenges. The scope encompasses an in-depth segmentation analysis across equipment types, applications, and end-user industries, complemented by a thorough regional assessment to identify major growth hubs and emerging market trends. The report also highlights the competitive landscape by profiling leading industry players and addressing frequently asked questions to provide a holistic market view.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.2 Billion |

| Market Forecast in 2033 | USD 11.9 Billion |

| Growth Rate | 8.5% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Evoqua Water Technologies, Veolia Water Technologies, Suez SA, Nalco Water (Ecolab), Merck KGaA, Kurita Water Industries Ltd., Ovivo Inc., Pure Aqua, Inc., OSG Corporation, MECO (Mechanical Equipment Company), Hydrotreat, Hyflux Ltd., Pall Corporation (Danaher), Pentair PLC, Ionpure (Evoqua), Marcor Remediation, Parker Hannifin Corporation, GE Water & Process Technologies (Suez), ResinTech, Siemens Water Technologies (Evoqua) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Ultrapure Water (UPW) equipment market is extensively segmented to provide a granular understanding of its diverse components and applications. This segmentation highlights the various technologies employed in UPW production, the specific processes where UPW is critical, and the industries that constitute the primary demand base. Each segment exhibits unique growth dynamics influenced by technological advancements, regulatory requirements, and industrial expansion trends, enabling a detailed market assessment and strategic planning for stakeholders.

Analyzing the market through these segments reveals that certain equipment types, such as Reverse Osmosis (RO) and Electrodeionization (EDI) systems, dominate due to their efficiency and effectiveness in achieving high purity levels. Similarly, the semiconductor and pharmaceutical industries consistently stand out as the largest end-users, driving innovation and investment in UPW technologies. This multi-dimensional segmentation provides a robust framework for identifying key market opportunities and challenges across the UPW ecosystem.

- By Equipment: This segment includes various technologies utilized in the multi-stage purification process to achieve ultrapure water.

- Filtration Systems (e.g., Cartridge Filters, Media Filters, Ultrafiltration/Microfiltration Membranes)

- Ion Exchange Systems (e.g., Mixed Bed Resins, Cation/Anion Exchangers)

- Reverse Osmosis (RO) Systems

- Electrodeionization (EDI) Systems

- UV Sterilizers

- Degasifiers

- Ozonation Systems

- Total Organic Carbon (TOC) Analyzers

- Other Treatment Components (e.g., pumps, piping, storage tanks, control systems)

- By Application: This segment categorizes the market based on the specific uses of ultrapure water across industries.

- Rinsing and Cleaning Processes (e.g., semiconductor wafer cleaning, medical device sterilization)

- Solution Preparation (e.g., chemical solutions for manufacturing, pharmaceutical formulations)

- Cooling Water Systems (e.g., sensitive industrial cooling)

- Laboratory Research and Analysis (e.g., analytical testing, reagent preparation)

- Product Formulation (e.g., cosmetics, specialized chemicals)

- Steam Generation (e.g., high-pressure boilers in power plants)

- Wastewater Treatment (e.g., as part of reuse loops in industrial facilities)

- Other Industrial Processes (e.g., advanced materials manufacturing, optical lens production)

- By End-User: This segment defines the major industries that consume ultrapure water.

- Semiconductor Industry (e.g., Wafer Fabrication, Integrated Circuit (IC) Manufacturing, Flat Panel Displays)

- Pharmaceutical and Biotechnology Industry (e.g., Drug Production, Biologics Manufacturing, Active Pharmaceutical Ingredients (APIs))

- Power Generation (e.g., Boiler Feed Water for nuclear, thermal, and concentrated solar power plants)

- Healthcare and Medical Devices (e.g., dialysis, sterile processing)

- Food and Beverage Industry (e.g., specialized beverage production, high-purity ingredient processing)

- Research and Academic Institutions (e.g., university laboratories, government research facilities)

- Chemical Industry (e.g., specialty chemicals production, reagent manufacturing)

- Automotive Industry (e.g., battery manufacturing, specialized painting processes)

- Other Industrial Sectors (e.g., aerospace, advanced metallurgy, solar panel manufacturing)

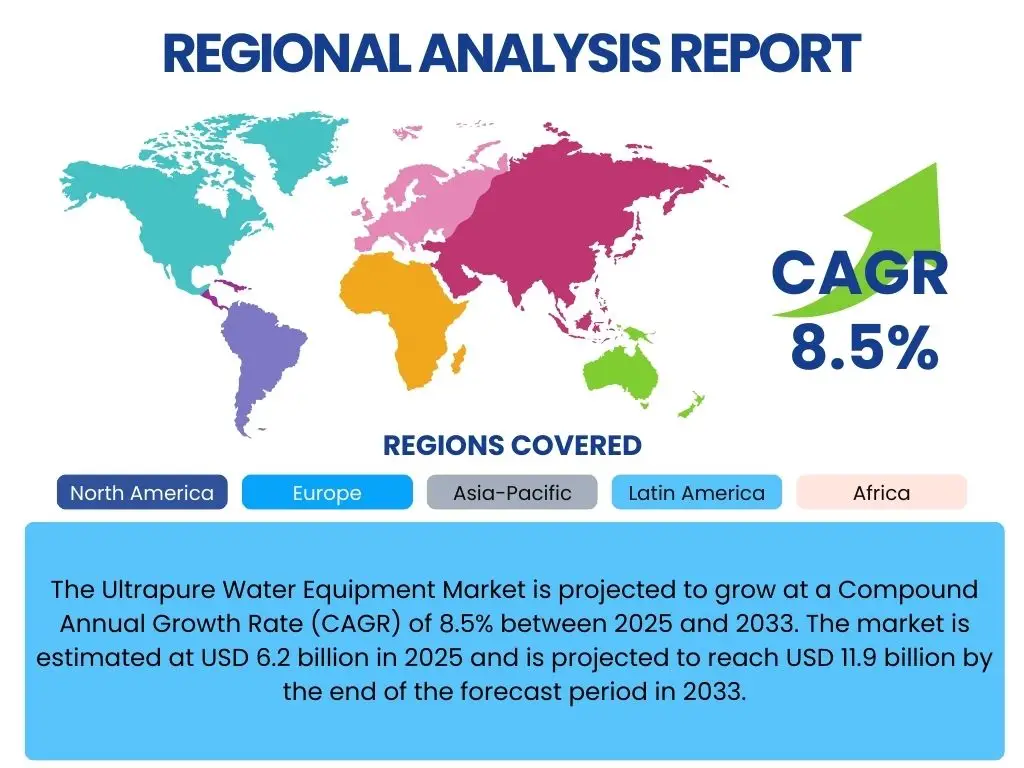

Regional Highlights

The global Ultrapure Water (UPW) equipment market demonstrates distinct regional growth patterns influenced by industrial concentration, technological adoption, and regulatory environments. Asia Pacific stands out as the dominant and fastest-growing region, primarily driven by the robust expansion of semiconductor manufacturing facilities in countries like China, South Korea, Taiwan, and Japan. The region's rapid industrialization, coupled with increasing investments in pharmaceutical and biotechnology sectors, further fuels the demand for advanced UPW solutions. Governments in this region are actively promoting high-tech manufacturing, creating a conducive environment for market expansion.

North America and Europe represent mature markets for UPW equipment, characterized by stringent quality standards in their well-established pharmaceutical, biotechnology, and electronics industries. While their growth rates may be more modest compared to Asia Pacific, these regions continue to invest in upgrading existing UPW infrastructure and adopting advanced, energy-efficient technologies. Innovation in these regions often focuses on smart systems, sustainability, and compliance with evolving environmental regulations.

Latin America and the Middle East & Africa (MEA) are emerging markets with significant growth potential, albeit from a smaller base. Industrial diversification, particularly in sectors like petrochemicals, food & beverage, and healthcare, is driving the nascent demand for UPW in these regions. Investments in infrastructure development and increasing foreign direct investment are expected to stimulate future market expansion, making these regions increasingly attractive for UPW equipment providers looking for new growth avenues.

- Asia Pacific (APAC): Dominates the market due to rapid expansion of the semiconductor and pharmaceutical industries in countries like China, South Korea, Taiwan, and Japan. India and Southeast Asian nations are also experiencing significant industrial growth.

- North America: A mature market with high demand from the pharmaceutical, biotechnology, and advanced electronics sectors. Strong focus on technological innovation and compliance with stringent purity standards.

- Europe: Characterized by a strong pharmaceutical industry, robust R&D activities, and increasing adoption of sustainable water treatment practices, particularly in Germany, France, and the UK.

- Latin America: Emerging market driven by growing industrialization in countries like Brazil and Mexico, with increasing investments in pharmaceutical and chemical manufacturing.

- Middle East & Africa (MEA): Demonstrating nascent growth fueled by economic diversification efforts, particularly in sectors like pharmaceuticals, food & beverage, and power generation in the UAE, Saudi Arabia, and South Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Ultrapure Water Equipment Market.- Evoqua Water Technologies

- Veolia Water Technologies

- Suez SA

- Nalco Water (Ecolab)

- Merck KGaA

- Kurita Water Industries Ltd.

- Ovivo Inc.

- Pure Aqua, Inc.

- OSG Corporation

- MECO (Mechanical Equipment Company)

- Hydrotreat

- Hyflux Ltd.

- Pall Corporation (Danaher)

- Pentair PLC

- Ionpure (Evoqua)

- Marcor Remediation

- Parker Hannifin Corporation

- GE Water & Process Technologies (Suez)

- ResinTech

- Siemens Water Technologies (Evoqua)

Frequently Asked Questions

What is Ultrapure Water (UPW) and why is it important?

Ultrapure water (UPW) is water that has been purified to extremely stringent specifications, containing virtually no dissolved minerals, organic compounds, particulate matter, or microorganisms. It is critical in industries such as semiconductor manufacturing, pharmaceuticals, and power generation where even trace impurities can severely impact product quality, process efficiency, or equipment integrity.

Which industries are the primary consumers of Ultrapure Water Equipment?

The semiconductor industry is the largest consumer of UPW equipment, requiring vast quantities of ultrapure water for cleaning and rinsing processes in microchip fabrication. Other major end-users include the pharmaceutical and biotechnology sectors for drug formulation and sterile environments, as well as power generation for boiler feed water, and certain specialized chemical and research applications.

What are the key technologies used in Ultrapure Water production?

Ultrapure water production typically involves a multi-stage purification process combining several technologies. These often include pre-treatment (filtration, carbon adsorption), primary purification (Reverse Osmosis), secondary purification (Electrodeionization, Ion Exchange), and final polishing (UV sterilization, ultrafiltration, degasification) to achieve the desired purity levels.

What are the main drivers for the growth of the Ultrapure Water Equipment market?

Key drivers include the continuous expansion and technological advancements in the semiconductor and pharmaceutical industries, which demand increasing volumes of high-purity water. Stricter regulatory standards for water quality, growing R&D activities in nanotechnology and biotechnology, and an increasing global emphasis on water conservation and reuse also significantly propel market growth.

What emerging trends are shaping the future of Ultrapure Water Equipment?

Emerging trends include the integration of AI and IoT for predictive maintenance and process optimization, leading to smarter and more efficient UPW systems. There is also a growing demand for modular and compact systems, an increased focus on sustainable solutions for water recycling and reclamation, and the development of advanced materials for improved filtration and purification technologies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted