Fixed Line Broadband Access Equipment Market

Fixed Line Broadband Access Equipment Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707624 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

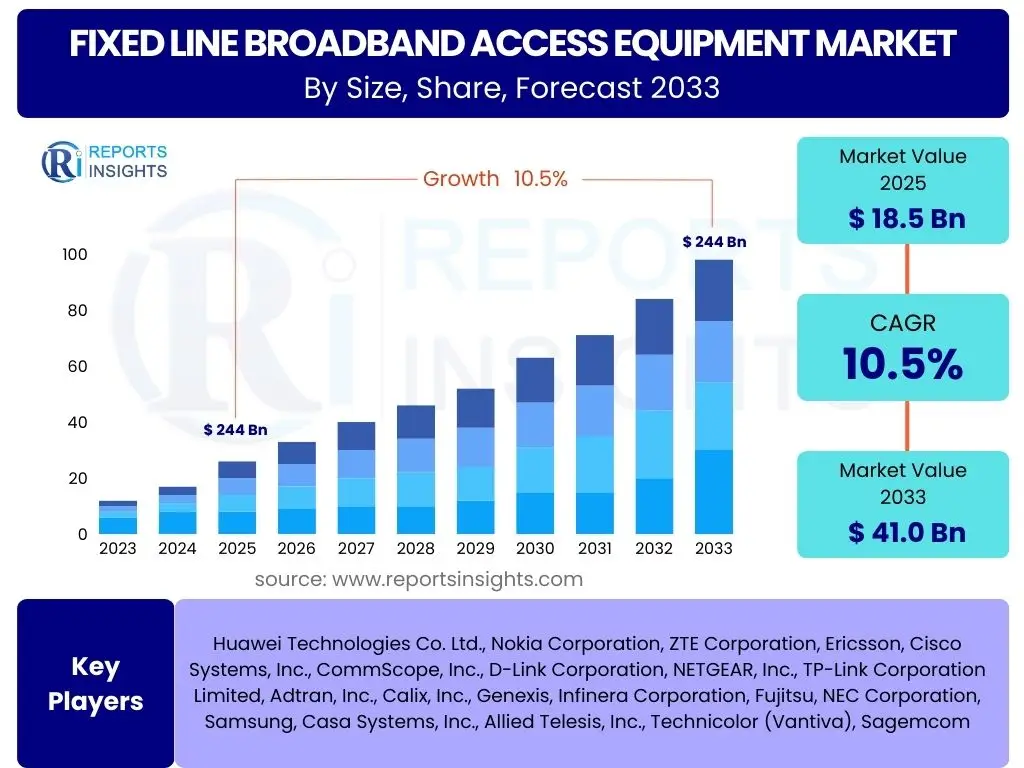

Fixed Line Broadband Access Equipment Market Size

According to Reports Insights Consulting Pvt Ltd, The Fixed Line Broadband Access Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2033. The market is estimated at USD 18.5 Billion in 2025 and is projected to reach USD 41.0 Billion by the end of the forecast period in 2033.

Key Fixed Line Broadband Access Equipment Market Trends & Insights

Current discussions and queries regarding the Fixed Line Broadband Access Equipment market reveal a strong focus on the rapid deployment of fiber optic networks globally, particularly Fiber-to-the-Home (FTTH) and Fiber-to-the-Building (FTTB). This push is driven by the escalating demand for ultra-high-speed internet services to support a growing array of bandwidth-intensive applications, including 4K/8K video streaming, cloud computing, and advanced online gaming. Another significant trend involves the integration of fixed-line broadband with 5G networks, where robust fixed infrastructure is essential for backhaul and fronthaul, enabling the full potential of next-generation wireless technologies.

The market is also witnessing a shift towards more sophisticated passive optical network (PON) technologies, such as XGS-PON and NG-PON2, which offer symmetric multi-gigabit speeds and enhanced capacity to meet future data demands. Furthermore, there is an increasing emphasis on energy-efficient equipment and sustainable deployment practices, reflecting broader environmental concerns and operational cost reduction efforts. The rise of smart home ecosystems and the proliferation of IoT devices further necessitate resilient and high-capacity fixed-line broadband, propelling innovations in equipment capable of handling diverse connectivity requirements and ensuring seamless user experiences.

- Accelerated global Fiber-to-the-X (FTTX) deployment.

- Rising demand for symmetric multi-gigabit broadband speeds.

- Increased convergence and integration with 5G backhaul infrastructure.

- Advancements in Passive Optical Network (PON) technologies (XGS-PON, NG-PON2).

- Growing adoption of cloud services and IoT devices driving bandwidth demand.

- Emphasis on energy efficiency and sustainable network solutions.

- Shift towards software-defined networking (SDN) and network function virtualization (NFV) for flexible network management.

AI Impact Analysis on Fixed Line Broadband Access Equipment

User inquiries about Artificial Intelligence's influence on Fixed Line Broadband Access Equipment frequently center on how AI can enhance network operational efficiency, predictive capabilities, and overall service quality. AI and Machine Learning (ML) are becoming instrumental in automating complex network management tasks, moving beyond traditional manual configurations to more dynamic and adaptive systems. This includes the use of AI algorithms for real-time traffic analysis, enabling intelligent routing and dynamic bandwidth allocation, which significantly improves network performance and reduces latency, particularly crucial for high-demand applications and critical services.

Furthermore, AI is transforming network maintenance and fault detection. By analyzing vast datasets of network performance and historical incidents, AI-powered systems can predict potential equipment failures, identify anomalies, and even pinpoint the root cause of issues before they impact end-users. This proactive approach to maintenance minimizes downtime, reduces operational costs, and enhances the reliability of fixed-line broadband services. AI also plays a crucial role in cybersecurity, employing advanced pattern recognition to detect and mitigate threats, thereby ensuring the integrity and security of the broadband infrastructure. The integration of AI tools is ultimately leading to more autonomous, self-optimizing, and resilient fixed-line networks, which can adapt to evolving demands and unexpected challenges with greater agility.

- Automated network optimization and resource allocation for improved performance.

- Predictive maintenance and fault detection, minimizing downtime and operational costs.

- Enhanced cybersecurity through AI-driven threat detection and anomaly recognition.

- Intelligent traffic management and load balancing for efficient bandwidth utilization.

- Proactive customer experience management through real-time issue identification.

- Development of self-healing and self-configuring broadband networks.

- Data analytics and insights for network planning and infrastructure upgrades.

Key Takeaways Fixed Line Broadband Access Equipment Market Size & Forecast

Common questions regarding the Fixed Line Broadband Access Equipment market size and forecast consistently highlight the robust growth trajectory driven by insatiable demand for high-speed internet connectivity. The market's expansion is not merely incremental but rather characterized by transformative technological shifts, such as the widespread adoption of fiber optics and advanced PON technologies, which are setting new benchmarks for broadband speeds and reliability. This fundamental driver is further amplified by global initiatives focused on digital inclusion and the increasing reliance on online services for work, education, and entertainment, underpinning a sustained need for resilient and high-capacity fixed infrastructure.

Furthermore, regional disparities in broadband penetration and infrastructure development present significant growth opportunities, particularly in emerging economies where significant investments are being made to bridge the digital divide. The competitive landscape is intensely focused on innovation, cost-efficiency, and the ability to deliver scalable solutions that can meet future demands, including the convergence with 5G. Stakeholders are keen on understanding how policy frameworks, government funding, and public-private partnerships will continue to shape the market's trajectory, making these factors critical determinants of future growth and market dynamics.

- The market is poised for substantial growth, driven by increasing global demand for high-speed internet.

- Fiber optic deployment remains the primary catalyst for market expansion.

- Technological advancements in PON and DOCSIS are key to sustaining growth and meeting future needs.

- Emerging economies offer significant untapped potential for infrastructure development.

- Government investments and digital transformation initiatives are crucial market enablers.

- Competitive differentiation hinges on innovation, service quality, and cost-effectiveness.

- Convergence with 5G and IoT ecosystems will drive further demand for fixed backhaul.

Fixed Line Broadband Access Equipment Market Drivers Analysis

The Fixed Line Broadband Access Equipment market is profoundly influenced by several key drivers, primarily centered around the pervasive and growing demand for high-speed, reliable internet connectivity. The global proliferation of fiber optic networks, fueled by governmental digital agendas and consumer expectations for superior online experiences, stands out as a paramount driver. This push towards Fiber-to-the-Home (FTTH) and other FTTx architectures necessitates significant investment in advanced optical line terminals (OLTs) and optical network units (ONUs).

Beyond basic connectivity, the increasing adoption of bandwidth-intensive applications such as 4K/8K streaming, virtual reality (VR), augmented reality (AR), cloud gaming, and extensive use of cloud computing services is pushing the boundaries of existing network capacities, thereby driving demand for next-generation broadband access equipment. The expansion of remote work and e-learning paradigms, solidified during recent global events, has further cemented the need for robust and high-performance fixed-line connections in residential and commercial settings. Additionally, the rapid rollout of 5G networks inherently relies on a strong fixed-line backhaul infrastructure to support high data throughput and low latency requirements, creating a symbiotic relationship that significantly boosts the market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for High-Speed Internet and Data Services | +3.0% | Global, particularly Asia Pacific & North America | Short to Long Term (2025-2033) |

| Government Initiatives and Funding for Broadband Expansion | +2.5% | Europe, North America, Developing Economies | Medium to Long Term (2026-2033) |

| Rapid Growth of FTTx Deployments (FTTH, FTTB) | +2.0% | Global, especially China, India, Western Europe | Short to Medium Term (2025-2030) |

| Proliferation of IoT Devices and Smart Home Ecosystems | +1.5% | Developed Regions (North America, Europe, East Asia) | Medium to Long Term (2027-2033) |

| Need for Robust Fixed Backhaul for 5G and Beyond | +1.0% | Global, particularly Urban Centers | Short to Medium Term (2025-2030) |

Fixed Line Broadband Access Equipment Market Restraints Analysis

Despite the strong growth drivers, the Fixed Line Broadband Access Equipment market faces several significant restraints that could temper its expansion. One primary concern is the substantial capital expenditure required for deploying and upgrading fixed-line broadband infrastructure, particularly for fiber optic networks. The high costs associated with civil works, trenching, labor, and the equipment itself can be prohibitive for smaller service providers and pose challenges even for larger players, especially in areas with difficult terrain or existing legacy infrastructure that needs to be replaced.

Another critical restraint is the complexity of regulatory environments across different regions and countries. Obtaining permits, navigating right-of-way issues, and complying with diverse local regulations can significantly delay deployment timelines and increase project costs. Intense competition among existing service providers and new entrants often leads to price erosion, impacting profitability margins for equipment manufacturers. Furthermore, the shortage of skilled labor for network design, installation, and maintenance, particularly for advanced fiber technologies, presents a bottleneck that can impede the pace of deployment and operational efficiency. Lastly, the cybersecurity risks associated with complex interconnected networks, including potential vulnerabilities in equipment, necessitate continuous investment in security measures, adding to the operational burden and costs for providers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure for Infrastructure Deployment | -1.5% | Global, particularly Developing Economies | Short to Medium Term (2025-2030) |

| Complex Regulatory Frameworks and Right-of-Way Issues | -1.0% | Europe, India, Latin America | Medium Term (2026-2031) |

| Skilled Labor Shortage for Fiber Network Installation and Maintenance | -0.8% | North America, Europe | Short to Medium Term (2025-2030) |

| Intense Competition and Price Erosion | -0.7% | Global | Short to Long Term (2025-2033) |

| Security Concerns and Cybersecurity Threats | -0.5% | Global | Short to Long Term (2025-2033) |

Fixed Line Broadband Access Equipment Market Opportunities Analysis

Numerous opportunities exist for growth and innovation within the Fixed Line Broadband Access Equipment market, stemming from both technological advancements and evolving connectivity needs. The ongoing global push for digital transformation and smart city initiatives presents a significant avenue for market expansion. Smart cities require ubiquitous, high-speed, and reliable fixed broadband infrastructure to support interconnected sensors, smart utilities, intelligent transportation systems, and public safety applications, driving demand for advanced access equipment capable of handling massive data volumes with low latency.

The expansion of broadband access to rural and underserved areas, often supported by government subsidies and public-private partnerships, represents a substantial untapped market. These initiatives aim to bridge the digital divide, providing connectivity to millions who currently lack adequate access, thereby creating new deployment opportunities for fiber and fixed wireless access solutions. Furthermore, the emergence of new technologies such as Wi-Fi 7 and beyond, which will rely heavily on robust fixed backhaul, along with the increasing adoption of Passive Optical LAN (POL) in enterprises and data centers, present niche but high-growth segments. The increasing demand for managed services, where equipment vendors and service providers offer end-to-end solutions including installation, maintenance, and network management, also creates significant revenue opportunities by providing value-added services beyond mere hardware sales.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Broadband Access in Rural and Underserved Areas | +2.0% | Global, particularly North America, Europe, Africa | Medium to Long Term (2026-2033) |

| Growth of Smart City and Smart Infrastructure Projects | +1.8% | Developed & Emerging Economies (China, Middle East, Europe) | Short to Long Term (2025-2033) |

| Rising Demand for Fixed-Mobile Convergence Solutions | +1.5% | Global | Medium Term (2026-2031) |

| Development of Next-Generation Access Technologies (e.g., 25G/50G PON) | +1.2% | Global, particularly Technology Hubs | Long Term (2028-2033) |

| Increased Adoption of Managed Services and Network Optimization Solutions | +1.0% | Global | Short to Long Term (2025-2033) |

Fixed Line Broadband Access Equipment Market Challenges Impact Analysis

The Fixed Line Broadband Access Equipment market faces several challenges that can impede its growth and operational efficiency. One significant hurdle is the rapid pace of technological evolution, which necessitates continuous research and development and frequent equipment upgrades. This constant need for innovation can lead to shorter product lifecycles and increased R&D expenditure for manufacturers, alongside higher capital expenditure for service providers struggling to keep up with the latest standards and ensure future-proof networks. Interoperability issues between equipment from different vendors also pose a challenge, leading to integration complexities and potential vendor lock-in scenarios.

Another major challenge involves managing the increasing complexity of network operations. As networks grow in size and sophistication, incorporating diverse technologies and services, their management becomes more intricate. This requires specialized skill sets and advanced automation tools, adding to operational overheads. The environmental impact of deploying and maintaining extensive physical infrastructure, including energy consumption of equipment and disposal of electronic waste, is gaining scrutiny, pushing companies to adopt more sustainable practices, which can incur additional costs. Furthermore, the global supply chain vulnerabilities, as evidenced by recent disruptions, can lead to component shortages and delays in equipment delivery, impacting deployment timelines and market supply.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence and Upgrade Cycles | -1.2% | Global | Short to Long Term (2025-2033) |

| Complexities in Network Integration and Interoperability | -1.0% | Global | Medium Term (2026-2031) |

| Supply Chain Disruptions and Component Shortages | -0.9% | Global | Short to Medium Term (2025-2028) |

| Ensuring Network Resiliency and Cybersecurity Against Evolving Threats | -0.8% | Global | Short to Long Term (2025-2033) |

| High Energy Consumption and Environmental Impact of Network Infrastructure | -0.7% | Global, particularly Developed Economies | Medium to Long Term (2027-2033) |

Fixed Line Broadband Access Equipment Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Fixed Line Broadband Access Equipment market, covering market size, growth forecasts, key trends, drivers, restraints, opportunities, and challenges. It offers detailed segmentation analysis by technology, component, end-user, and application, alongside a thorough regional assessment to identify prominent growth areas. The report includes profiles of key market players, competitive landscape insights, and an impact analysis of Artificial Intelligence on the sector, equipping stakeholders with actionable intelligence for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 41.0 Billion |

| Growth Rate | 10.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Huawei Technologies Co. Ltd., Nokia Corporation, ZTE Corporation, Ericsson, Cisco Systems, Inc., CommScope, Inc., D-Link Corporation, NETGEAR, Inc., TP-Link Corporation Limited, Adtran, Inc., Calix, Inc., Genexis, Infinera Corporation, Fujitsu, NEC Corporation, Samsung, Casa Systems, Inc., Allied Telesis, Inc., Technicolor (Vantiva), Sagemcom |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Fixed Line Broadband Access Equipment market is comprehensively segmented to provide granular insights into its diverse dynamics. These segmentations are critical for understanding market demand patterns, technological preferences, and end-user adoption rates across various applications and geographies. By dissecting the market based on technology, component, end-user, and application, stakeholders can identify key growth areas and tailor their strategies to capitalize on specific market niches.

Technological segmentation highlights the shift from traditional DSL and older PON versions towards advanced fiber optic technologies like XGS-PON and NG-PON2, driven by the need for higher bandwidth and symmetric speeds. Component-wise, the market is characterized by the demand for sophisticated Optical Line Terminals (OLTs) and Optical Network Units (ONUs), which form the backbone of fiber networks. End-user segmentation reveals the dominant residential sector, but also significant growth in commercial, industrial, and government applications, as these sectors increasingly rely on robust fixed broadband for operations and digital transformation. Finally, application segmentation underscores the pervasive need for high-speed internet access, coupled with burgeoning demand for Voice over IP (VoIP), Video on Demand (VoD), smart home services, and cloud connectivity, all necessitating advanced fixed-line infrastructure.

- By Technology:

- GPON (Gigabit Passive Optical Network)

- EPON (Ethernet Passive Optical Network)

- XGS-PON (10 Gigabit Symmetric Passive Optical Network)

- NG-PON2 (Next-Generation Passive Optical Network 2)

- DOCSIS (Data Over Cable Service Interface Specification)

- DOCSIS 3.1

- DOCSIS 4.0

- G.fast

- Other Access Technologies

- By Component:

- Optical Line Terminal (OLT)

- Optical Network Unit (ONU/ONT)

- Cable Modem Termination System (CMTS)

- DSL Access Multiplexer (DSLAM)

- Optical Amplifiers

- Fiber Optic Cables and Accessories

- Broadband Routers and Gateways

- Other Network Equipment

- By End-User:

- Residential

- Commercial

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- Industrial

- Government and Public Sector

- Data Centers

- By Application:

- High-Speed Internet Access

- Voice over IP (VoIP)

- Video on Demand (VoD) and IPTV

- Smart Home Services and IoT Connectivity

- Cloud Connectivity and Enterprise Services

- Remote Work and E-learning

Regional Highlights

- North America: A mature market characterized by ongoing fiber rollouts, particularly in rural areas, and continuous upgrades to existing cable and DSL infrastructure. High demand for multi-gigabit speeds for advanced residential and commercial applications drives significant investment. The region is a hub for technological innovation and early adoption of next-generation PON technologies.

- Europe: Witnessing robust growth driven by national broadband plans and EU digital agenda initiatives aimed at increasing fiber penetration. Countries like France, Spain, and Germany are rapidly deploying FTTH, while Eastern European nations are also making significant strides. Emphasis on open access networks and sustainable infrastructure is notable.

- Asia Pacific (APAC): The largest and fastest-growing market, led by China, India, Japan, and South Korea. Massive fiber deployments, government-led digital inclusion programs, and a vast population with increasing internet adoption rates fuel the demand for fixed-line broadband equipment. Rapid urbanization and the expansion of smart cities further propel market growth.

- Latin America: An emerging market with considerable growth potential, driven by increasing internet penetration, governmental efforts to bridge the digital divide, and a growing middle class. Brazil and Mexico are leading the charge in fiber optic expansion, though challenges related to regulatory frameworks and high deployment costs persist.

- Middle East and Africa (MEA): Experiencing significant investments in broadband infrastructure, especially in the Gulf Cooperation Council (GCC) countries for smart city projects and economic diversification. Africa is a nascent market with immense potential, with initiatives focused on expanding basic internet access and leveraging fixed-line for mobile backhaul.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Fixed Line Broadband Access Equipment Market.- Huawei Technologies Co. Ltd.

- Nokia Corporation

- ZTE Corporation

- Ericsson

- Cisco Systems, Inc.

- CommScope, Inc.

- D-Link Corporation

- NETGEAR, Inc.

- TP-Link Corporation Limited

- Adtran, Inc.

- Calix, Inc.

- Genexis

- Infinera Corporation

- Fujitsu

- NEC Corporation

- Samsung

- Casa Systems, Inc.

- Allied Telesis, Inc.

- Technicolor (Vantiva)

- Sagemcom

Frequently Asked Questions

What is Fixed Line Broadband Access Equipment?

Fixed Line Broadband Access Equipment refers to the hardware components and systems used to provide high-speed internet connectivity over physical cables, such as fiber optic cables, copper wires (DSL), or coaxial cables (DOCSIS). This includes devices like Optical Line Terminals (OLTs), Optical Network Units (ONUs), Cable Modem Termination Systems (CMTS), and DSL Access Multiplexers (DSLAMs), which facilitate the connection between internet service providers (ISPs) and end-users.

What are the primary drivers of the Fixed Line Broadband Access Equipment market growth?

The market's growth is primarily driven by the surging global demand for high-speed internet due to increased data consumption, the widespread deployment of fiber-to-the-X (FTTX) infrastructure, supportive government initiatives for broadband expansion, and the escalating need for robust fixed backhaul for 5G networks and IoT proliferation.

How does AI impact the Fixed Line Broadband Access Equipment sector?

AI significantly impacts the sector by enabling advanced network automation, predictive maintenance, and optimized resource allocation, leading to improved operational efficiency and reduced downtime. It also enhances cybersecurity, intelligent traffic management, and aids in proactive customer service by predicting potential network issues.

Which regions present the most significant growth opportunities for Fixed Line Broadband Access Equipment?

Asia Pacific, particularly countries like China and India, represents the largest and fastest-growing region due to extensive fiber deployments and rising internet penetration. North America and Europe also offer substantial growth, driven by upgrades to multi-gigabit fiber networks and rural broadband initiatives.

What are the key technologies shaping the Fixed Line Broadband Access Equipment market?

The market is increasingly shaped by advanced Passive Optical Network (PON) technologies such as XGS-PON and NG-PON2, which offer multi-gigabit symmetric speeds. Other key technologies include DOCSIS 3.1 and 4.0 for cable networks, and G.fast for copper-based high-speed broadband, alongside continuous innovations in optical fiber and network management software.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted