Transformer Manufacturing Market

Transformer Manufacturing Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704384 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

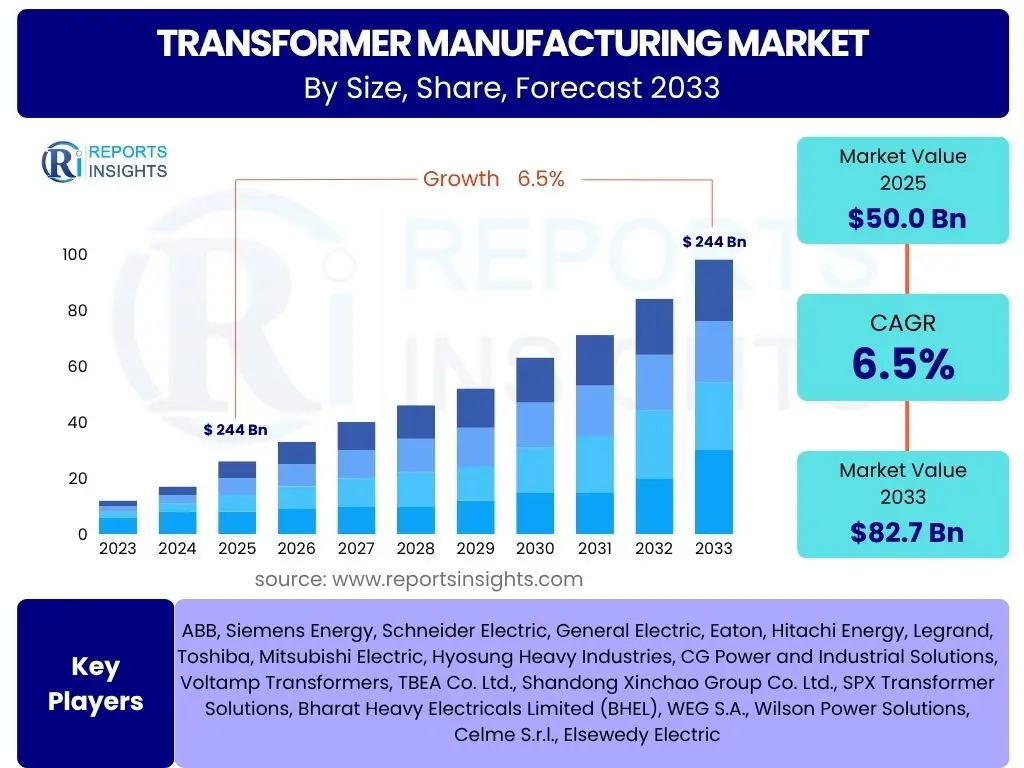

Transformer Manufacturing Market Size

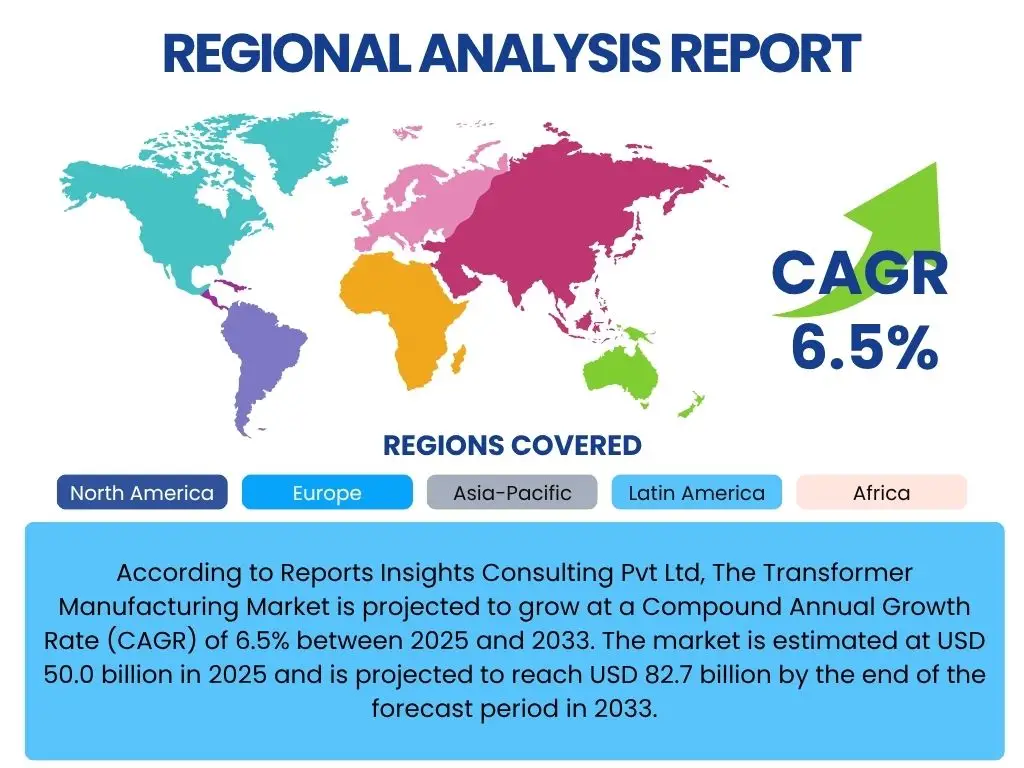

According to Reports Insights Consulting Pvt Ltd, The Transformer Manufacturing Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 50.0 billion in 2025 and is projected to reach USD 82.7 billion by the end of the forecast period in 2033.

Key Transformer Manufacturing Market Trends & Insights

Common user inquiries regarding market trends in transformer manufacturing frequently revolve around technological advancements, sustainability initiatives, and the integration of smart grid solutions. Users are keenly interested in how the industry is adapting to the global energy transition, particularly the rise of renewable energy sources and the increasing demand for energy efficiency. There is a clear focus on understanding the shift towards more compact, reliable, and intelligent transformer solutions that can support modern power infrastructure. Additionally, questions often arise concerning the impact of digitalization and automation on manufacturing processes and product design.

The market is witnessing a significant paradigm shift driven by the imperative for grid modernization and the accelerated adoption of clean energy. This has spurred innovation in transformer design, leading to the development of highly efficient, low-loss transformers that minimize energy wastage. Furthermore, the integration of sensors and communication technologies is transforming traditional transformers into smart, connected assets capable of real-time monitoring and predictive maintenance. This evolution is crucial for enhancing grid stability, optimizing power distribution, and reducing operational costs across various end-use sectors.

- Digitalization and Smart Grid Integration: Increasing adoption of digital technologies for enhanced monitoring, control, and automation in transformers, enabling smart grid functionalities and improving operational efficiency.

- Emphasis on Energy Efficiency and Sustainability: Growing demand for energy-efficient and eco-friendly transformers, driven by stringent environmental regulations and the global push for reduced carbon emissions.

- Growth in Renewable Energy Projects: Significant market expansion fueled by the rapid deployment of solar and wind power generation, necessitating specialized transformers for grid integration.

- Adoption of Advanced Materials and Manufacturing Processes: Utilization of new materials like amorphous metals and advanced manufacturing techniques such as additive manufacturing for lighter, more durable, and higher-performance transformers.

- Demand for Compact and Modular Transformers: Rising need for smaller, more flexible transformer designs that can be easily deployed in confined urban spaces or for specialized industrial applications.

- Focus on Predictive Maintenance and Asset Management: Leveraging IoT and data analytics to enable proactive maintenance strategies, extending asset lifespan, and minimizing unplanned downtime.

AI Impact Analysis on Transformer Manufacturing

User questions concerning the impact of Artificial Intelligence (AI) on transformer manufacturing typically center on themes of operational efficiency, quality control, design optimization, and supply chain management. There is considerable interest in how AI can automate complex processes, enhance decision-making through data analytics, and contribute to the development of next-generation smart transformers. Users seek to understand the practical applications of AI, from predictive maintenance and fault diagnosis to automated design parameters and intelligent production scheduling. The overarching expectation is that AI will streamline manufacturing workflows, reduce costs, and accelerate innovation within the sector.

AI is profoundly reshaping the transformer manufacturing landscape by introducing unprecedented levels of precision, automation, and intelligence across the value chain. In design and engineering, AI algorithms can optimize transformer parameters for specific applications, rapidly iterating through thousands of designs to achieve peak efficiency and cost-effectiveness. In the production phase, AI-powered vision systems are enhancing quality control, detecting defects with superior accuracy and speed, while predictive maintenance algorithms are minimizing equipment downtime on the factory floor. Furthermore, AI is revolutionizing post-sale operations through advanced monitoring systems that predict potential failures and optimize maintenance schedules for installed transformers, thereby improving reliability and extending operational life for utilities and industrial clients.

- Enhanced Predictive Maintenance: AI algorithms analyze operational data from transformers to predict potential failures, enabling proactive maintenance and reducing unscheduled downtime for assets.

- Optimized Design and Engineering: AI-driven simulations and generative design tools accelerate the development of new transformer models, optimizing for efficiency, size, and material usage.

- Improved Quality Control: AI-powered vision systems and data analytics enhance defect detection during manufacturing, ensuring higher product quality and reducing rework.

- Automated Production Processes: Integration of AI in robotic systems and manufacturing lines leads to increased automation, precision, and efficiency in assembly and testing.

- Supply Chain Optimization: AI algorithms optimize raw material procurement, inventory management, and logistics, reducing costs and lead times.

- Energy Efficiency Enhancements: AI-driven insights can inform improvements in transformer core and winding designs, leading to greater energy efficiency and reduced losses in operation.

Key Takeaways Transformer Manufacturing Market Size & Forecast

Common user questions regarding key takeaways from the Transformer Manufacturing market size and forecast often focus on the primary growth drivers, the segments showing the most promising expansion, and the overall resilience of the market against economic fluctuations. Users are interested in understanding the long-term viability of the industry given the global energy transition and infrastructure development goals. There is a strong desire for concise insights into which regions are leading growth and what technological innovations are crucial for future market dominance. The essence of these inquiries is to grasp the fundamental forces shaping the market's trajectory and profitability.

The Transformer Manufacturing market is poised for significant and sustained growth, primarily propelled by massive investments in renewable energy infrastructure and the urgent need for grid modernization worldwide. This growth is not merely incremental but transformative, driven by the shift towards smart grids, increased electrification, and the expansion of industrial and commercial sectors in developing economies. The forecast indicates robust expansion across all transformer types, with a particular emphasis on high-efficiency and specialized units required for new energy systems and complex industrial applications. Geographically, Asia Pacific is expected to remain a dominant force, while North America and Europe will see consistent growth driven by aging infrastructure replacement and smart grid initiatives.

- Robust Growth Trajectory: The market is set for substantial growth through 2033, driven by global energy transition and infrastructure development.

- Grid Modernization as a Core Driver: Investments in upgrading aging power grids and building new, intelligent networks are central to market expansion.

- Renewable Energy Integration: The accelerating adoption of solar, wind, and other renewable sources is a critical catalyst for transformer demand.

- Technological Innovation is Key: Advancements in smart transformers, energy-efficient designs, and sustainable materials are pivotal for future market competitiveness.

- Asia Pacific Leads Regional Growth: High industrialization, urbanization, and electrification projects in emerging economies are propelling the APAC market.

Transformer Manufacturing Market Drivers Analysis

The transformer manufacturing market is experiencing robust growth fueled by several interconnected global trends. Primary among these is the escalating demand for electricity driven by rapid industrialization, urbanization, and population growth, particularly in developing economies. This necessitates continuous expansion and upgrading of power generation, transmission, and distribution infrastructure. Coupled with this, the global push towards renewable energy sources like solar and wind power inherently requires a significant number of transformers for grid integration and efficient power conversion. Furthermore, governments worldwide are investing heavily in modernizing aging grid infrastructure to enhance reliability, reduce transmission losses, and integrate smart grid technologies, directly boosting demand for advanced transformers. The increasing adoption of electric vehicles and the resultant need for charging infrastructure also contributes to the demand for specialized transformers.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Grid Modernization and Expansion | +2.0% | North America, Europe, Asia Pacific | 2025-2033 |

| Integration of Renewable Energy Sources | +1.8% | Europe, Asia Pacific, North America | 2025-2033 |

| Rising Electricity Demand from Industrialization & Urbanization | +1.5% | Asia Pacific, Latin America, MEA | 2025-2033 |

| Growth in Electric Vehicle (EV) Charging Infrastructure | +0.8% | North America, Europe, Asia Pacific | 2026-2033 |

Transformer Manufacturing Market Restraints Analysis

Despite significant growth drivers, the transformer manufacturing market faces several notable restraints that could temper its expansion. One major challenge is the volatility in raw material prices, particularly for core components like copper, aluminum, and electrical steel. Fluctuations in these commodity prices can directly impact manufacturing costs and profit margins, making long-term planning difficult for manufacturers. Additionally, the high upfront capital expenditure required for establishing and upgrading transformer manufacturing facilities can be a barrier to entry for new players and limit expansion for existing ones. Stringent environmental regulations, while promoting sustainable solutions, can also increase production costs due to the need for specialized materials, processes, and waste management. The lengthy lead times for custom-built transformers and the intense competition among established players further contribute to market complexities, sometimes leading to price wars that erode profitability. Furthermore, the aging infrastructure in some developed regions, while needing replacement, can be slow to upgrade due to budgetary constraints and complex regulatory approval processes.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices | -0.9% | Global | 2025-2033 |

| High Capital Expenditure for Manufacturing | -0.6% | Global | 2025-2033 |

| Stringent Environmental Regulations | -0.5% | Europe, North America | 2025-2033 |

| Intense Market Competition and Price Pressures | -0.4% | Global | 2025-2033 |

Transformer Manufacturing Market Opportunities Analysis

The transformer manufacturing market presents substantial opportunities for innovation and growth, driven by evolving energy landscapes and technological advancements. A significant avenue for expansion lies in the burgeoning smart grid initiatives worldwide, which necessitate intelligent, connected transformers capable of real-time monitoring, fault detection, and optimized power flow. The rapid global deployment of electric vehicle charging infrastructure is creating a new niche for specialized power transformers. Furthermore, the increasing demand for high-voltage direct current (HVDC) transmission systems, particularly for long-distance power transmission and grid interconnections, offers a lucrative segment for manufacturers of specialized HVDC transformers. The growing focus on energy efficiency across all sectors, spurred by rising energy costs and environmental concerns, creates sustained demand for advanced, low-loss transformers. Emerging markets, especially in Asia Pacific and Latin America, with their ongoing infrastructure development and electrification projects, offer untapped potential for market penetration and expansion.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Adoption of Smart Grid Technologies | +1.5% | North America, Europe, Asia Pacific | 2025-2033 |

| Expansion of Electric Vehicle Charging Infrastructure | +1.2% | Global | 2026-2033 |

| Increasing Demand for HVDC Transmission Systems | +1.0% | Asia Pacific, Europe | 2025-2033 |

| Focus on Energy Efficiency and Eco-Friendly Transformers | +0.8% | Global | 2025-2033 |

Transformer Manufacturing Market Challenges Impact Analysis

The transformer manufacturing market, despite its growth prospects, confronts several critical challenges that demand strategic responses from industry participants. One significant hurdle is the persistent issue of supply chain disruptions, which can lead to delays in raw material procurement and delivery of finished products, impacting production schedules and profitability. The global shortage of skilled labor, particularly engineers and technicians specialized in transformer design, manufacturing, and maintenance, poses a significant operational challenge. Furthermore, the intense competition within the market, coupled with the long product lifecycles of transformers, can lead to aggressive pricing strategies and reduced profit margins. The increasing complexity of modern transformers, driven by smart grid integration and higher efficiency requirements, necessitates continuous R&D investments, which can be a financial burden. Cybersecurity risks, as smart transformers become more connected, represent an emerging challenge that requires robust protection measures to ensure grid integrity and data security. Adapting to rapidly evolving technology standards and regulatory frameworks across diverse geographies also remains a persistent challenge for global manufacturers.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Disruptions and Raw Material Scarcity | -1.0% | Global | 2025-2028 |

| Shortage of Skilled Workforce | -0.7% | Global | 2025-2033 |

| Intensifying Competition and Price Erosion | -0.6% | Global | 2025-2033 |

| Cybersecurity Risks for Smart Transformers | -0.4% | Global | 2026-2033 |

Transformer Manufacturing Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Transformer Manufacturing Market, offering critical insights into its current state and future trajectory. The scope encompasses detailed market sizing, forecast projections, and a thorough examination of key growth drivers, formidable restraints, emerging opportunities, and significant challenges impacting the industry landscape. The report delves into the intricate dynamics of market segmentation across various dimensions, providing a granular view of demand and supply trends. Furthermore, it highlights regional market performance, identifying key growth pockets and strategic implications for stakeholders. The competitive landscape analysis includes profiles of leading market players, assessing their strategies, product portfolios, and market positioning. This report serves as an invaluable resource for manufacturers, suppliers, investors, and policymakers seeking to make informed strategic decisions in this evolving market.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 50.0 Billion |

| Market Forecast in 2033 | USD 82.7 Billion |

| Growth Rate | 6.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ABB, Siemens Energy, Schneider Electric, General Electric, Eaton, Hitachi Energy, Legrand, Toshiba, Mitsubishi Electric, Hyosung Heavy Industries, CG Power and Industrial Solutions, Voltamp Transformers, TBEA Co. Ltd., Shandong Xinchao Group Co. Ltd., SPX Transformer Solutions, Bharat Heavy Electricals Limited (BHEL), WEG S.A., Wilson Power Solutions, Celme S.r.l., Elsewedy Electric |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Transformer Manufacturing market is meticulously segmented to provide a granular understanding of its diverse components and sub-sectors. This comprehensive segmentation allows for a detailed analysis of demand patterns, technological preferences, and regional disparities across various transformer types, insulation methods, power ratings, applications, and end-use industries. Understanding these segments is crucial for identifying specific growth opportunities, tailoring product development strategies, and optimizing market entry approaches for different customer needs. The segmentation highlights the market's adaptability to a wide range of operational environments and power requirements, from large-scale utility grids to specialized industrial applications, ensuring a precise and actionable market overview.

- By Type: This segment categorizes transformers based on their design and primary function.

- Power Transformers: Utilized in transmission networks to step up or step down voltage, typically found in generation stations and transmission substations.

- Distribution Transformers: Employed in distribution networks to reduce high voltage electricity to lower voltage for direct consumption by end-users.

- Instrument Transformers: Used for measurement and protection in AC power systems, including current transformers (CTs) and potential transformers (PTs).

- Specialty Transformers: Designed for specific applications such as industrial furnaces, rectifiers, or highly specialized electronic equipment, often with unique voltage or isolation requirements.

- By Insulation Type: This segmentation differentiates transformers based on the insulating medium used.

- Oil-immersed Transformers: Utilize mineral oil or synthetic fluids as both coolant and electrical insulator, widely used due to their efficiency and cooling capabilities.

- Dry-type Transformers: Employ air, resin, or other solid insulation, requiring no fluid and thus suitable for indoor or environmentally sensitive installations.

- By Application: This segment focuses on the primary end-user sectors where transformers are deployed.

- Utilities: Encompasses power generation, transmission, and distribution companies responsible for delivering electricity to consumers.

- Industrial: Includes manufacturing plants, heavy industries, and other large-scale commercial operations requiring robust and specialized power solutions.

- Commercial: Covers transformers used in office buildings, shopping centers, data centers, and other commercial establishments.

- Residential: Pertains to transformers used in residential complexes or individual homes for local power distribution.

- By Power Rating: This segmentation categorizes transformers based on their power handling capacity (MVA - Mega Volt Ampere).

- Small Power Transformers (Up to 5 MVA): Typically used in distribution networks or smaller industrial applications.

- Medium Power Transformers (5 MVA - 100 MVA): Common in substations for industrial and commercial distribution.

- Large Power Transformers (Above 100 MVA): Primarily used in high-voltage transmission networks and large power generation plants.

- By End-Use Sector: This segment provides a more detailed breakdown of the specific industries or functions utilizing transformers.

- Power Generation: Transformers within power plants to step up generated voltage for transmission.

- Transmission & Distribution: Transformers facilitating voltage changes across utility grids.

- Railways & Metro: Specialized transformers for railway electrification and metro systems.

- Automotive: Including charging infrastructure transformers for electric vehicles.

- Data Centers: Critical for ensuring stable power supply to IT infrastructure.

- Mining: Robust transformers designed for harsh mining environments.

- Oil & Gas: Transformers for onshore and offshore drilling, refining, and pipeline operations.

- Others: Encompassing applications in renewable energy, marine, medical, and various niche industrial sectors.

Regional Highlights

- North America: This region is characterized by significant investments in grid modernization and the replacement of aging infrastructure. The growing adoption of renewable energy, particularly solar and wind power, and the expansion of electric vehicle charging networks are key drivers for transformer demand. Regulatory initiatives promoting energy efficiency also bolster the market.

- Europe: Driven by ambitious decarbonization targets and robust investments in renewable energy integration, Europe exhibits a strong demand for highly efficient and smart transformers. The region's focus on sustainable energy solutions and the replacement of outdated power grids are pivotal for market growth. Stringent environmental regulations also favor eco-friendly transformer designs.

- Asia Pacific (APAC): Expected to be the largest and fastest-growing market due to rapid industrialization, urbanization, and electrification projects in emerging economies like China, India, and Southeast Asian countries. Massive infrastructure development, coupled with increasing electricity demand and significant investments in renewable energy, fuels the demand for all types of transformers.

- Latin America: The region is witnessing steady growth primarily due to increasing industrial activities, urbanization, and efforts to expand electricity access to underserved areas. Investments in grid infrastructure upgrades and the development of renewable energy projects contribute to market expansion.

- Middle East and Africa (MEA): Growth in MEA is largely influenced by substantial infrastructure investments, particularly in power generation and transmission, to support economic diversification and population growth. The region's rich oil and gas sector also drives demand for specialized industrial transformers, alongside emerging renewable energy projects.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Transformer Manufacturing Market.- ABB

- Siemens Energy

- Schneider Electric

- General Electric

- Eaton

- Hitachi Energy

- Legrand

- Toshiba

- Mitsubishi Electric

- Hyosung Heavy Industries

- CG Power and Industrial Solutions

- Voltamp Transformers

- TBEA Co. Ltd.

- Shandong Xinchao Group Co. Ltd.

- SPX Transformer Solutions

- Bharat Heavy Electricals Limited (BHEL)

- WEG S.A.

- Wilson Power Solutions

- Celme S.r.l.

- Elsewedy Electric

Frequently Asked Questions

What is the primary driver of growth in the Transformer Manufacturing market?

The primary driver of growth in the Transformer Manufacturing market is the global imperative for grid modernization and the increasing integration of renewable energy sources such as solar and wind power into national grids. This necessitates new and upgraded transformers for efficient power transmission and distribution.

How does AI impact the Transformer Manufacturing industry?

AI significantly impacts the Transformer Manufacturing industry by enabling enhanced predictive maintenance, optimizing design and engineering processes, improving quality control through advanced inspection systems, and streamlining supply chain management. AI adoption leads to greater operational efficiency, reduced downtime, and accelerated innovation in product development.

What are the key challenges faced by Transformer Manufacturers?

Key challenges faced by Transformer Manufacturers include volatility in raw material prices, persistent supply chain disruptions, a shortage of skilled labor, intense market competition leading to price pressures, and managing the emerging cybersecurity risks associated with smart, connected transformers.

Which region holds the largest market share in Transformer Manufacturing?

Asia Pacific (APAC) currently holds the largest market share in Transformer Manufacturing. This dominance is driven by rapid industrialization, extensive urbanization, and substantial investments in power infrastructure and renewable energy projects across countries like China and India.

What emerging opportunities exist in the Transformer Manufacturing market?

Emerging opportunities in the Transformer Manufacturing market include the increasing adoption of smart grid technologies, the rapid expansion of electric vehicle (EV) charging infrastructure, growing demand for specialized HVDC (High Voltage Direct Current) transformers, and the rising global focus on energy efficiency leading to demand for eco-friendly and low-loss transformer designs.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted