Edge Computing in Manufacturing Market

Edge Computing in Manufacturing Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705855 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

Edge Computing in Manufacturing Market Size

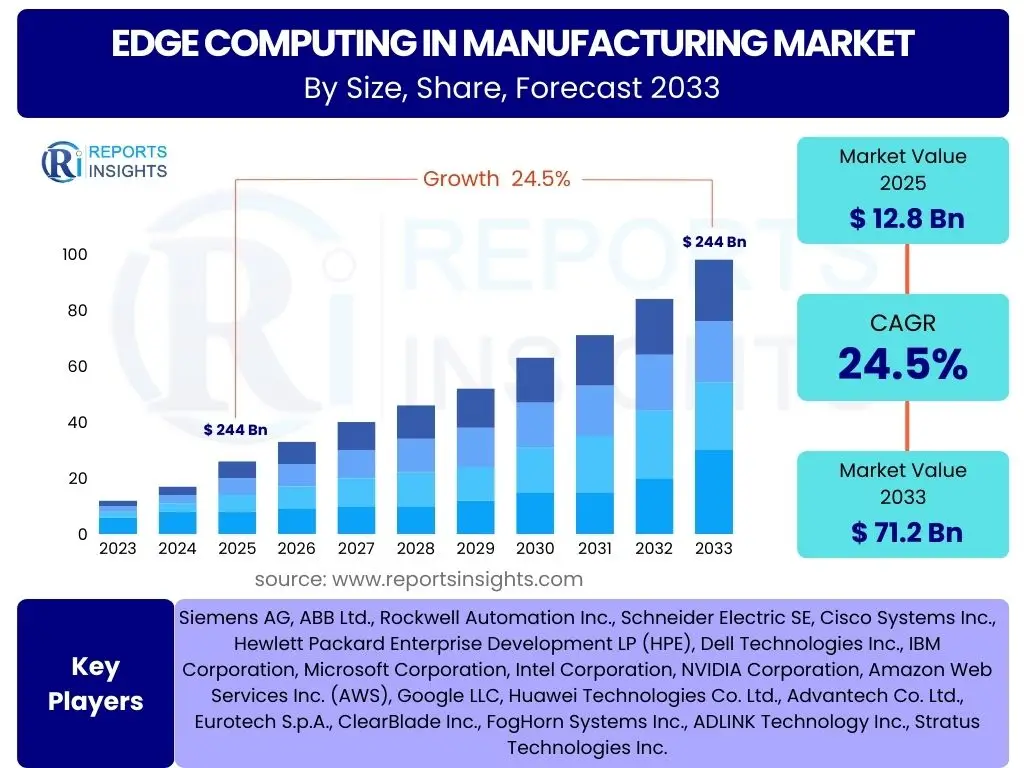

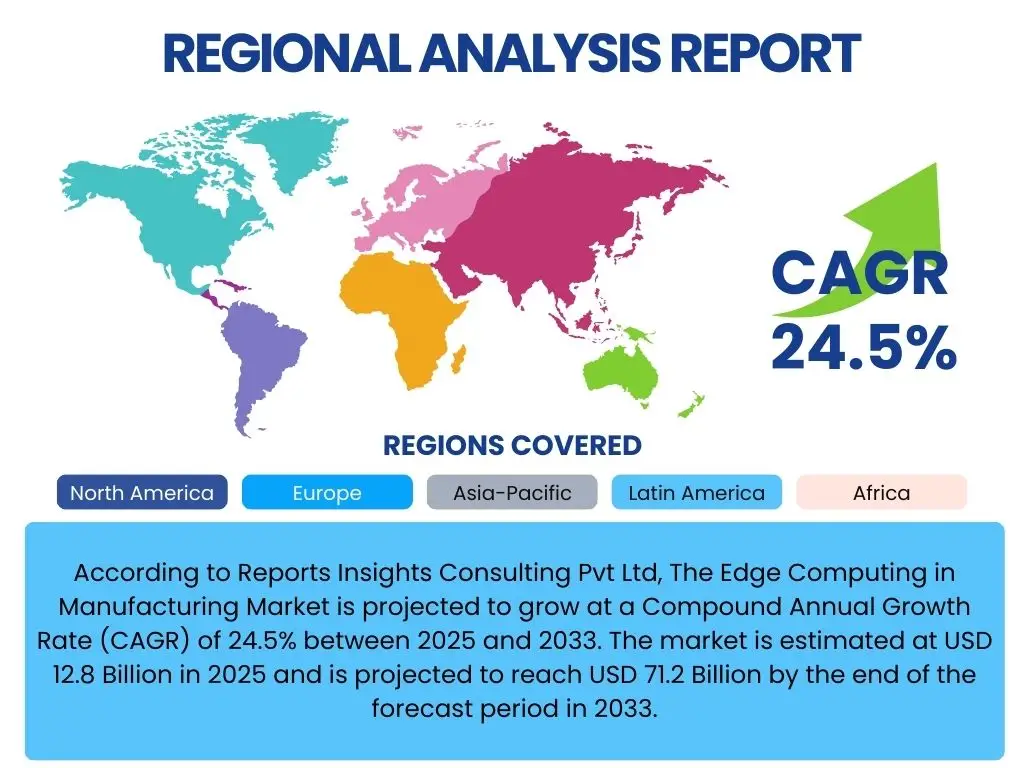

According to Reports Insights Consulting Pvt Ltd, The Edge Computing in Manufacturing Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 24.5% between 2025 and 2033. The market is estimated at USD 12.8 Billion in 2025 and is projected to reach USD 71.2 Billion by the end of the forecast period in 2033.

Key Edge Computing in Manufacturing Market Trends & Insights

User inquiries frequently revolve around the evolving landscape of industrial operations and the imperative for faster, more localized data processing. A significant trend identified is the increasing convergence of Information Technology (IT) and Operational Technology (OT) within manufacturing environments. This convergence is driving the adoption of edge computing solutions to bridge the gap between enterprise systems and shop floor operations, enabling seamless data flow and integrated decision-making. Manufacturers are actively seeking ways to leverage real-time data from diverse sources, including IoT sensors, robotics, and industrial machinery, to optimize processes and enhance productivity. The demand for immediate insights without the latency associated with cloud-only processing is a primary catalyst.

Another prominent trend observed is the growing emphasis on predictive maintenance and quality control facilitated by edge analytics. Companies are shifting from reactive maintenance to proactive strategies, using edge devices to analyze machine performance data in real time, identify potential failures, and schedule maintenance proactively. This not only minimizes downtime but also extends equipment lifespan and reduces operational costs. Furthermore, the integration of artificial intelligence and machine learning capabilities directly at the edge is emerging as a critical trend, allowing for advanced anomaly detection, automated decision-making, and optimized resource allocation without constant reliance on centralized cloud infrastructure. Security and data privacy concerns also shape adoption patterns, pushing for robust, localized data processing solutions.

- IT/OT convergence driving integrated operations

- Increased adoption of industrial IoT (IIoT) devices

- Growing demand for real-time data processing and analytics

- Shift towards predictive maintenance and quality control at the edge

- Emergence of AI and Machine Learning at the edge

- Enhanced focus on data security and privacy through localized processing

- Development of specialized edge hardware and software solutions

AI Impact Analysis on Edge Computing in Manufacturing

Common user questions regarding AI's impact on Edge Computing in Manufacturing highlight a keen interest in how artificial intelligence can amplify the capabilities of edge infrastructure. Manufacturers are particularly interested in AI's role in enabling more sophisticated automation, improving decision-making processes, and driving operational efficiency directly on the factory floor. AI at the edge allows for immediate analysis of vast quantities of sensor data, enabling real-time anomaly detection for equipment failure prediction, optimizing production lines, and ensuring stringent quality control without sending all data to a centralized cloud. This capability is crucial for time-sensitive applications where even milliseconds of latency can impact performance or safety.

The integration of AI models directly onto edge devices transforms raw data into actionable insights at the source, reducing bandwidth requirements and enhancing data privacy by minimizing the need for data transfer. Users are keen to understand how this facilitates autonomous systems, such as self-optimizing robotic arms or automated guided vehicles (AGVs), which can learn and adapt to changing conditions locally. While the benefits are clear, concerns often arise regarding the complexity of deploying and managing AI models at the edge, the need for specialized skills, and ensuring the reliability and accuracy of AI-driven decisions in critical manufacturing processes. Users also question the scalability of AI edge deployments and the interoperability with existing industrial systems, seeking solutions that offer seamless integration and robust performance.

- Enables real-time anomaly detection and predictive maintenance

- Optimizes production processes through immediate data analysis

- Facilitates autonomous operations and intelligent robotics

- Improves quality control and defect detection on the line

- Reduces data latency for critical decision-making

- Enhances data privacy and security by local processing

- Supports resource optimization and energy efficiency

- Drives adaptive and self-optimizing manufacturing systems

Key Takeaways Edge Computing in Manufacturing Market Size & Forecast

User queries regarding key takeaways from the Edge Computing in Manufacturing market size and forecast consistently point to the strategic importance of localized data processing for future industrial growth. A primary insight is the significant growth trajectory of this market, driven by the escalating volume of data generated by industrial IoT devices and the critical need for low-latency processing to support real-time applications. Manufacturers recognize that traditional cloud-centric architectures cannot always meet the stringent demands of modern industrial operations, particularly for applications like robotics, autonomous vehicles, and real-time quality inspection. Edge computing addresses these limitations by bringing computation closer to the data source, transforming operational efficiency and agility.

Another crucial takeaway is the increasing integration of advanced technologies like AI, machine learning, and 5G connectivity with edge infrastructure. This synergy is poised to unlock new capabilities, from highly accurate predictive maintenance to fully autonomous factories, positioning edge computing as an indispensable component of Industry 4.0 initiatives. The market's expansion signifies a fundamental shift in manufacturing IT strategy, moving towards more distributed and intelligent architectures that can adapt quickly to changing production demands and market conditions. While initial investment and integration complexity present challenges, the long-term benefits in terms of operational efficiency, cost reduction, and competitive advantage are compelling manufacturers to adopt these technologies at an accelerating pace, making it a critical area for strategic investment and development.

- Market poised for substantial growth due to IIoT proliferation

- Critical for low-latency, real-time industrial applications

- Enables enhanced operational efficiency and agility

- Strategic enabler for Industry 4.0 and smart factories

- Integration with AI, ML, and 5G accelerates adoption

- Addresses data security and privacy concerns through local processing

- Provides competitive advantage through optimized production processes

Edge Computing in Manufacturing Market Drivers Analysis

The Edge Computing in Manufacturing market is experiencing significant growth driven by several compelling factors that address the evolving needs of modern industrial environments. A primary driver is the exponential increase in data volume generated by industrial IoT (IIoT) sensors, smart machines, and connected devices on the factory floor. Processing this colossal amount of data efficiently at the edge, rather than sending it all to the cloud, significantly reduces bandwidth consumption and network latency. This localized processing capability is crucial for applications that require immediate decision-making, such as real-time quality control, predictive maintenance, and autonomous robotics.

Furthermore, the imperative for enhanced operational efficiency and cost reduction is pushing manufacturers towards edge solutions. By enabling real-time analytics and control at the source, edge computing minimizes downtime, optimizes resource utilization, and improves overall productivity. The growing demand for predictive maintenance, which relies heavily on timely data analysis to anticipate equipment failures, is another strong catalyst. Edge computing facilitates this by allowing continuous monitoring and analysis of machine health data directly at the machine. Lastly, heightened concerns around data security and privacy are accelerating edge adoption, as sensitive operational data can be processed and stored locally, reducing exposure to cyber threats associated with cloud transfers.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Volume of Industrial Data | +2.8% | Global | Long-term |

| Demand for Low Latency and Real-time Processing | +2.5% | Global | Short-term to Medium-term |

| Growing Adoption of IIoT Devices | +2.2% | Asia Pacific, North America, Europe | Medium-term |

| Need for Enhanced Operational Efficiency and Cost Reduction | +1.9% | Global | Ongoing |

| Emphasis on Data Security and Privacy | +1.5% | Europe (GDPR), North America, Asia Pacific | Medium-term |

Edge Computing in Manufacturing Market Restraints Analysis

Despite its significant growth potential, the Edge Computing in Manufacturing market faces several restraints that could temper its expansion. One major impediment is the high initial investment required for deploying edge infrastructure, including specialized hardware, software platforms, and integration services. Many manufacturers, especially small and medium-sized enterprises (SMEs), find these upfront costs prohibitive, limiting widespread adoption. The complexity involved in integrating new edge solutions with existing legacy operational technology (OT) systems also poses a significant challenge. This integration often requires extensive customization and can lead to compatibility issues, increasing deployment time and cost.

Another key restraint is the scarcity of skilled personnel with expertise in both IT and OT domains, specifically in deploying, managing, and maintaining edge computing environments. The convergence of these two distinct fields creates a talent gap that can hinder the effective implementation and optimization of edge solutions. Furthermore, concerns regarding data governance, standardization, and interoperability across various vendor platforms and industrial protocols present ongoing challenges. Manufacturers often struggle with managing data consistency and ensuring seamless communication between disparate edge devices and applications, which can slow down the adoption process and complicate scaled deployments. Addressing these multifaceted challenges is crucial for unlocking the full potential of edge computing in the manufacturing sector.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Deployment Costs | -1.2% | Global, particularly SMEs | Short-term to Medium-term |

| Complexity of Integration with Legacy Systems | -1.0% | Global | Medium-term |

| Lack of Skilled Workforce and Expertise | -0.8% | Global | Ongoing |

| Data Governance and Management Challenges | -0.7% | Global | Ongoing |

| Interoperability and Standardization Issues | -0.6% | Global | Medium-term |

Edge Computing in Manufacturing Market Opportunities Analysis

The Edge Computing in Manufacturing market is replete with significant opportunities poised to accelerate its growth and adoption. The rapid advancement and deployment of 5G technology represent a substantial opportunity, as 5G’s low latency and high bandwidth capabilities are perfectly complementary to edge computing. This synergy enables seamless, real-time data transfer and processing between edge devices and other parts of the network, unlocking new applications such as enhanced augmented reality (AR) for maintenance, more reliable autonomous guided vehicles (AGVs), and sophisticated real-time quality inspection systems. Manufacturers can leverage 5G to build highly agile and responsive factory environments, further optimizing production lines and enabling true Industry 4.0 capabilities.

Another major opportunity lies in the increasing convergence of edge computing with artificial intelligence (AI) and machine learning (ML). Deploying AI/ML models at the edge allows for intelligent automation, predictive analytics, and self-optimizing systems to operate autonomously on the factory floor without constant cloud connectivity. This capability enables more sophisticated anomaly detection, proactive maintenance scheduling, and adaptive process control. Furthermore, the development of specialized edge applications tailored to specific industrial verticals, such as smart manufacturing platforms for automotive or precision agriculture solutions, presents a fertile ground for innovation and market expansion. The growing interest in hybrid cloud-edge architectures, which combine the strengths of both centralized cloud processing and decentralized edge intelligence, also offers a flexible and scalable deployment model, appealing to a broader range of manufacturers looking for optimized IT infrastructure.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with 5G Technology | +2.0% | Global, particularly early 5G adopters like North America, Asia Pacific | Medium-term to Long-term |

| Synergy with AI and Machine Learning at the Edge | +1.8% | Global | Medium-term |

| Development of Customized Edge Applications for Verticals | +1.5% | Global | Long-term |

| Emergence of Hybrid Cloud-Edge Architectures | +1.3% | Global | Medium-term |

| Expansion into New Industrial Segments | +1.0% | Emerging Economies, Developing Regions | Long-term |

Edge Computing in Manufacturing Market Challenges Impact Analysis

The Edge Computing in Manufacturing market faces several significant challenges that require strategic navigation to sustain growth and widespread adoption. Cybersecurity stands out as a paramount concern; distributing computational power to numerous edge devices creates a broader attack surface, making securing these distributed assets complex. Protecting sensitive operational data and intellectual property at the edge from cyber threats, unauthorized access, and tampering requires robust security protocols, continuous monitoring, and effective threat detection mechanisms, adding layers of complexity to deployments. Manufacturers grapple with ensuring the integrity and confidentiality of data flowing through or stored at the edge, especially as more critical operations become edge-dependent.

Another substantial challenge involves the scalability and management of distributed edge infrastructure. As manufacturing operations expand, the number of edge devices and their geographical distribution can grow exponentially, posing difficulties in centralized management, software updates, and troubleshooting. Ensuring consistent performance, reliability, and uptime across a vast and varied fleet of edge devices is a complex undertaking that demands advanced orchestration and automation tools. Furthermore, achieving seamless interoperability between diverse hardware, software platforms, and legacy industrial systems remains a persistent hurdle. Manufacturers often deploy solutions from multiple vendors, leading to fragmentation and difficulties in data exchange and unified control. Addressing these challenges through standardized frameworks, robust security practices, and sophisticated management solutions will be critical for the continued maturity and widespread adoption of edge computing in manufacturing.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Cybersecurity Risks at the Edge | -0.9% | Global | Ongoing |

| Scalability and Management of Distributed Edge Infrastructure | -0.7% | Global | Medium-term |

| Interoperability and Standardization across Vendors | -0.6% | Global | Long-term |

| Data Consistency and Synchronization Issues | -0.5% | Global | Medium-term |

| Regulatory Compliance for Data Processing | -0.4% | Europe, North America | Ongoing |

Edge Computing in Manufacturing Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Edge Computing in Manufacturing market, offering a detailed understanding of its current size, historical performance, and future growth projections. It delves into the underlying market dynamics, including key drivers, significant restraints, emerging opportunities, and prevailing challenges that shape the industry landscape. The report segments the market extensively by component, application, industry vertical, and deployment model, providing granular insights into each category. Furthermore, it offers a thorough regional analysis, highlighting growth trends and key developments across major geographical areas. The competitive landscape is also critically examined, profiling leading companies and their strategic initiatives, enabling stakeholders to make informed decisions and identify potential areas for investment and partnership.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.8 Billion |

| Market Forecast in 2033 | USD 71.2 Billion |

| Growth Rate | 24.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Siemens AG, ABB Ltd., Rockwell Automation Inc., Schneider Electric SE, Cisco Systems Inc., Hewlett Packard Enterprise Development LP (HPE), Dell Technologies Inc., IBM Corporation, Microsoft Corporation, Intel Corporation, NVIDIA Corporation, Amazon Web Services Inc. (AWS), Google LLC, Huawei Technologies Co. Ltd., Advantech Co. Ltd., Eurotech S.p.A., ClearBlade Inc., FogHorn Systems Inc., ADLINK Technology Inc., Stratus Technologies Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Edge Computing in Manufacturing market is meticulously segmented to provide a granular view of its diverse components and applications, enabling a deeper understanding of market dynamics and growth opportunities across various dimensions. This comprehensive segmentation allows stakeholders to identify specific areas of investment, target promising customer segments, and develop tailored solutions that address particular industry needs. By breaking down the market based on its core elements, the report offers valuable insights into which technologies are gaining traction and where the most significant demand lies within the manufacturing sector.

The segmentation extends across key categories including components, which delineate between hardware, software, and services essential for edge deployments, providing clarity on the technological stack. Furthermore, the market is categorized by application, illustrating the diverse use cases where edge computing delivers tangible value, from enhancing operational efficiency to ensuring real-time quality control. Industry verticals are also a crucial segment, highlighting the adoption patterns and specific requirements of different manufacturing sectors. Lastly, deployment models distinguish between on-premises and hybrid approaches, reflecting varying preferences for infrastructure management and data processing architectures. This detailed segmentation offers a roadmap for navigating the complexities of the market and capitalizing on its evolving landscape.

- By Component:

- Hardware (Servers, Gateways, Sensors & Actuators, Storage, Networking Equipment)

- Software (Platform, Edge Analytics, Edge Security, Edge Orchestration, Data Management)

- Services (Consulting, System Integration & Deployment, Support & Maintenance, Managed Services)

- By Application:

- Predictive Maintenance

- Real-time Monitoring

- Asset Tracking & Management

- Quality Control & Inspection

- Supply Chain Optimization

- Autonomous Operations

- Workforce Safety & Compliance

- By Industry Vertical:

- Automotive & Transportation

- Aerospace & Defense

- Electronics & Semiconductor

- Food & Beverages

- Metals & Heavy Machinery

- Chemicals & Pharmaceuticals

- Energy & Utilities

- Others (Textile, Pulp & Paper)

- By Deployment:

- On-premises

- Hybrid

Regional Highlights

- North America: Leads the market due to early adoption of advanced technologies, high investment in industrial automation, and the presence of major technology providers. Emphasis on digital transformation and smart manufacturing initiatives drives significant growth.

- Europe: Driven by strong Industry 4.0 initiatives and government support for digitalizing manufacturing processes. Countries like Germany and the UK are at the forefront, focusing on operational efficiency, regulatory compliance, and sustainable production.

- Asia Pacific (APAC): Expected to witness the highest growth rate, fueled by rapid industrialization, increasing adoption of IoT and AI in manufacturing, and growing investments in smart factories, particularly in China, Japan, South Korea, and India.

- Latin America: Shows emerging potential with increasing industrial infrastructure development and a growing awareness of the benefits of edge computing for optimizing local operations and improving competitiveness.

- Middle East and Africa (MEA): Gradually adopting edge computing solutions, primarily in oil & gas, utilities, and process manufacturing sectors, driven by the need for remote monitoring, operational efficiency, and security in challenging environments.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Edge Computing in Manufacturing Market.- Siemens AG

- ABB Ltd.

- Rockwell Automation Inc.

- Schneider Electric SE

- Cisco Systems Inc.

- Hewlett Packard Enterprise Development LP (HPE)

- Dell Technologies Inc.

- IBM Corporation

- Microsoft Corporation

- Intel Corporation

- NVIDIA Corporation

- Amazon Web Services Inc. (AWS)

- Google LLC

- Huawei Technologies Co. Ltd.

- Advantech Co. Ltd.

- Eurotech S.p.A.

- ClearBlade Inc.

- FogHorn Systems Inc.

- ADLINK Technology Inc.

- Stratus Technologies Inc.

Frequently Asked Questions

Analyze common user questions about the Edge Computing in Manufacturing market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Edge Computing in Manufacturing?

Edge computing in manufacturing involves processing data closer to its source, such as on factory floors or within machinery, rather than sending it all to a centralized cloud. This minimizes latency, enables real-time decision-making, and enhances operational efficiency for industrial applications.

Why is Edge Computing important for the manufacturing industry?

It is crucial for manufacturing because it facilitates real-time data analysis for critical operations, improves responsiveness of automated systems, reduces network bandwidth usage, enhances data security by localizing sensitive information, and enables predictive maintenance and quality control without delay.

What are the primary benefits of implementing Edge Computing in factories?

Key benefits include reduced operational latency, improved real-time decision-making, enhanced data security and privacy, optimized bandwidth usage, increased operational efficiency, enablement of advanced applications like AI-driven automation, and a significant reduction in system downtime through predictive analytics.

What challenges does Edge Computing face in the manufacturing sector?

Challenges include high initial deployment costs, complexity of integrating new edge systems with legacy industrial infrastructure, a shortage of skilled personnel with combined IT/OT expertise, difficulties in managing distributed edge devices at scale, and ensuring robust cybersecurity across a wider attack surface.

How will Edge Computing impact the future of manufacturing?

Edge computing will be a cornerstone of Industry 4.0, enabling truly smart factories with highly autonomous operations, advanced predictive capabilities, and hyper-personalized production. It will drive unprecedented levels of efficiency, flexibility, and innovation by bringing intelligence directly to the point of action, transforming traditional manufacturing into a more responsive and intelligent ecosystem.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted