Thermoplastic Resin Market

Thermoplastic Resin Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704379 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

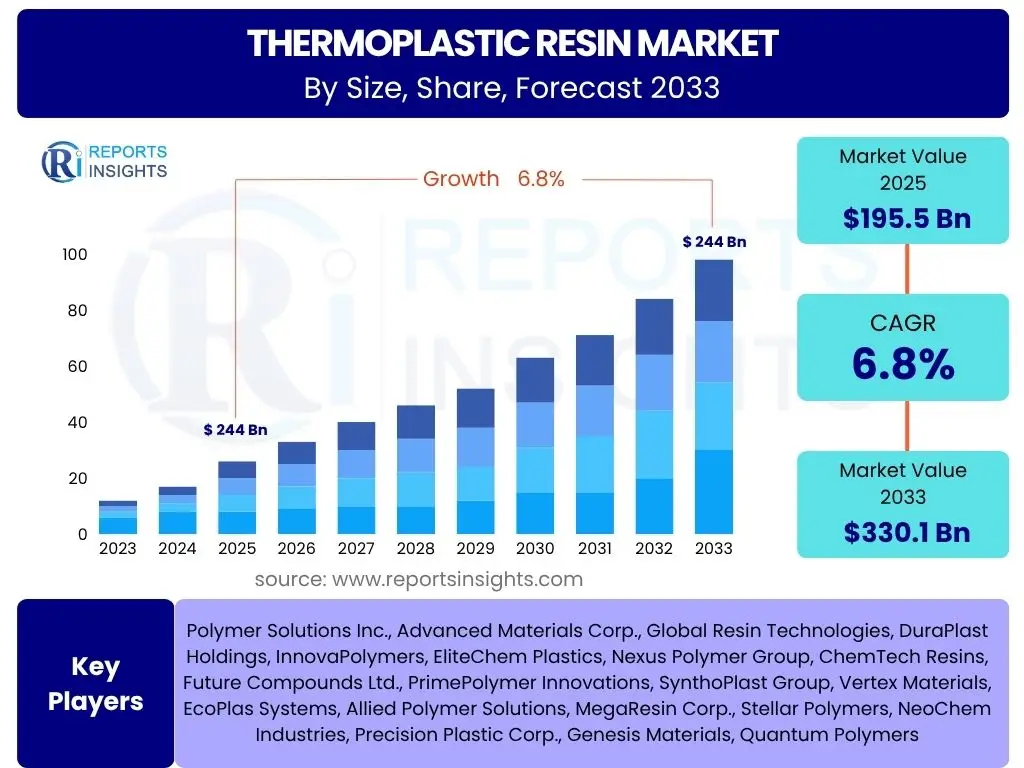

Thermoplastic Resin Market Size

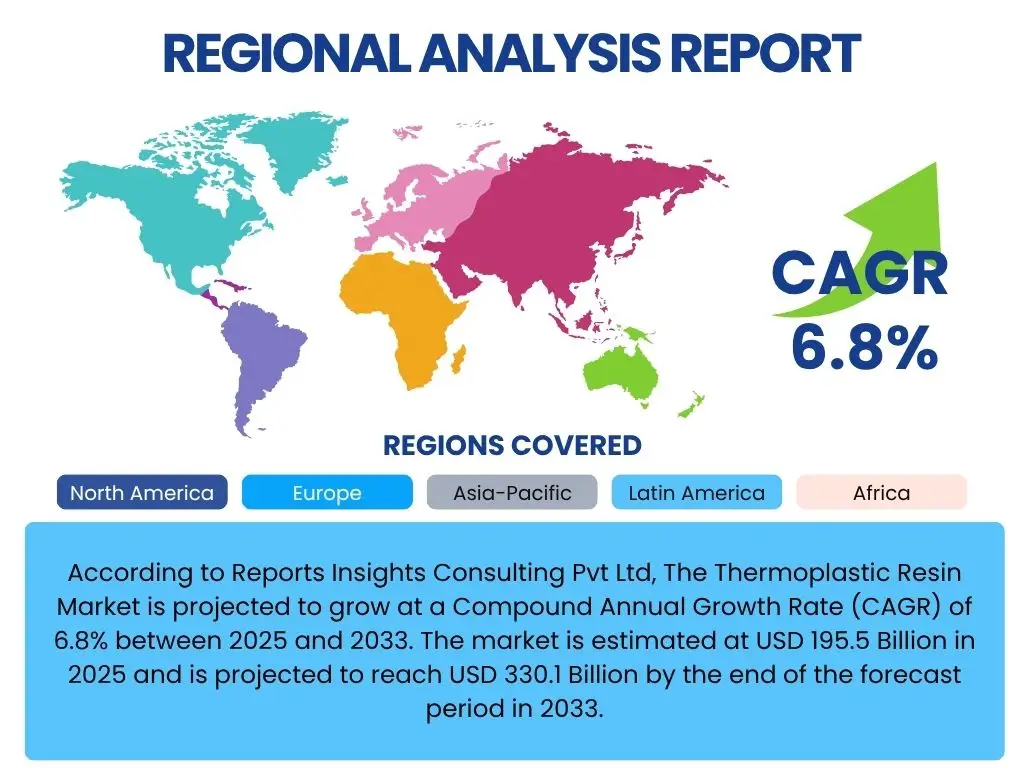

According to Reports Insights Consulting Pvt Ltd, The Thermoplastic Resin Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 195.5 Billion in 2025 and is projected to reach USD 330.1 Billion by the end of the forecast period in 2033.

Key Thermoplastic Resin Market Trends & Insights

The Thermoplastic Resin market is undergoing significant transformation, driven by a confluence of technological advancements, evolving consumer demands, and increasing regulatory pressure for sustainability. A primary trend observed is the growing emphasis on sustainable and circular economy principles, leading to intensified research and development into bio-based resins, recycled content integration, and advanced recycling technologies. This shift is not merely compliance-driven but also a response to brand commitment and consumer preference for environmentally responsible products.

Furthermore, the market is experiencing a rising demand for high-performance and specialty thermoplastics, particularly from industries such as automotive, aerospace, healthcare, and electrical and electronics. These sectors require materials with superior properties like lightweight characteristics, enhanced mechanical strength, thermal stability, and chemical resistance. Innovations in material science are enabling the creation of advanced thermoplastic composites and polymers that can withstand extreme conditions, pushing the boundaries of traditional applications.

The integration of advanced manufacturing techniques, including additive manufacturing (3D printing) and smart manufacturing processes, is also shaping the market. These technologies allow for greater design flexibility, reduced material waste, and faster prototyping, which are critical for accelerating product development cycles and meeting bespoke application requirements. The digitalization of the value chain, from material design to production and distribution, is creating more efficient and responsive supply networks.

- Growing adoption of sustainable and bio-based thermoplastic resins.

- Increasing demand for high-performance and specialty thermoplastics in critical applications.

- Expansion of additive manufacturing (3D printing) applications for custom parts.

- Focus on lightweighting solutions across various industries, particularly automotive and aerospace.

- Implementation of advanced recycling technologies to support circular economy initiatives.

AI Impact Analysis on Thermoplastic Resin

Artificial Intelligence (AI) is poised to significantly revolutionize the Thermoplastic Resin market by enhancing efficiency, accelerating innovation, and optimizing complex processes across the value chain. User inquiries often center on how AI can streamline R&D, improve manufacturing precision, and contribute to sustainability efforts within the industry. AI's capabilities in data analysis and pattern recognition are being leveraged to predict material properties, simulate performance under various conditions, and expedite the discovery of novel resin formulations, drastically reducing the time and cost associated with traditional experimentation.

In manufacturing, AI-powered systems are enabling predictive maintenance, optimizing process parameters for energy efficiency and reduced waste, and ensuring consistent product quality through real-time monitoring and control. This leads to higher yield rates, lower operational costs, and improved resource utilization. The ability of AI to analyze vast datasets from production lines allows for immediate identification of anomalies and optimization opportunities, moving towards more autonomous and intelligent manufacturing facilities.

Furthermore, AI is instrumental in enhancing supply chain resilience and responsiveness for thermoplastic resins. It can optimize logistics, manage inventory more effectively, and forecast demand with greater accuracy, thereby mitigating risks associated with raw material price volatility and supply chain disruptions. The application of AI also extends to sustainability, assisting in the development of more efficient recycling processes and the identification of optimal material compositions for end-of-life circularity. The collective impact is expected to lead to a more agile, efficient, and environmentally responsible thermoplastic resin industry.

- Accelerated material R&D through AI-driven property prediction and formulation optimization.

- Enhanced manufacturing efficiency and quality control via predictive analytics and process automation.

- Optimized supply chain management and demand forecasting for improved resilience.

- Support for sustainable practices by optimizing recycling processes and material life cycles.

- Facilitation of personalized material development and rapid prototyping.

Key Takeaways Thermoplastic Resin Market Size & Forecast

The Thermoplastic Resin market is set for robust growth over the forecast period, driven by its indispensable role across a multitude of end-use industries. A key takeaway is the sustained expansion expected from sectors such as packaging, automotive, construction, and electrical & electronics, which continually seek lighter, more durable, and cost-effective material solutions. The versatility and adaptability of thermoplastic resins to diverse application requirements underpin this strong market trajectory.

Another significant insight is the increasing emphasis on innovation, particularly in the development of high-performance and sustainable resin types. As industries strive for greater efficiency and reduced environmental footprint, the demand for advanced, eco-friendly thermoplastic solutions will escalate. This necessitates continuous investment in research and development to introduce new grades of resins that offer superior mechanical properties, improved processability, and enhanced recyclability or biodegradability, securing future market competitiveness.

Moreover, the market outlook is shaped by regional manufacturing trends and geopolitical factors. While Asia Pacific is anticipated to remain the dominant market due to rapid industrialization and burgeoning production capacities, North America and Europe will drive innovation in specialty and sustainable resins, leveraging stringent environmental regulations and technological advancements. Navigating the evolving regulatory landscape and adapting to regional market dynamics will be crucial for stakeholders aiming to capitalize on the projected growth opportunities within this dynamic industry.

- Consistent and significant market growth driven by diverse industrial applications.

- Critical importance of continuous innovation in high-performance and sustainable resin technologies.

- Increasing demand for lightweight and durable materials across key end-use sectors.

- Strong regional growth in Asia Pacific, coupled with innovation leadership in North America and Europe.

- Growing industry focus on circular economy principles and enhanced recyclability of thermoplastic products.

Thermoplastic Resin Market Drivers Analysis

The global Thermoplastic Resin market is significantly propelled by the escalating demand from the automotive and transportation sectors. As manufacturers strive for enhanced fuel efficiency and reduced emissions, the adoption of lightweight materials becomes paramount. Thermoplastic resins offer an excellent strength-to-weight ratio, contributing to vehicle weight reduction without compromising structural integrity or safety. This trend is further intensified by the rapid growth in electric vehicle (EV) production, where thermoplastics are used extensively in battery casings, interior components, and structural parts, driving down overall vehicle mass and extending range.

The expansion of the packaging industry worldwide also serves as a robust driver for thermoplastic resins. These materials are indispensable for a wide array of packaging applications, ranging from food and beverage containers to industrial packaging. The demand for flexible, durable, and protective packaging solutions, which also offer convenience and aesthetic appeal, continues to grow with urbanization and changing consumer lifestyles. Innovations in barrier properties, recyclability, and reusability of thermoplastic packaging are also contributing to their sustained market penetration.

Furthermore, the global construction industry's consistent growth, particularly in emerging economies, significantly boosts the demand for thermoplastic resins. These materials are widely utilized in pipes, fittings, insulation, roofing, window profiles, and various other building components due to their durability, corrosion resistance, ease of installation, and cost-effectiveness compared to traditional materials. Infrastructure development projects, coupled with a rising emphasis on sustainable and energy-efficient building practices, ensure a steady uptake of thermoplastic resin products in this sector.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand from Automotive & Aerospace Industries | +1.8% | Global, particularly North America, Europe, Asia Pacific | Medium to Long Term (2025-2033) |

| Growth in the Packaging Sector | +1.5% | Asia Pacific, North America, Europe | Short to Long Term (2025-2033) |

| Expansion of Construction Activities and Infrastructure Development | +1.2% | Asia Pacific, Latin America, Middle East | Medium to Long Term (2025-2033) |

| Technological Advancements in Material Science | +0.8% | Global, primarily Developed Economies | Long Term (2027-2033) |

Thermoplastic Resin Market Restraints Analysis

The Thermoplastic Resin market faces significant headwinds from the volatility of raw material prices, primarily crude oil and natural gas, which are key feedstocks for many conventional thermoplastics. Fluctuations in global energy markets and geopolitical instabilities can lead to unpredictable pricing of monomers and polymers, directly impacting manufacturing costs and profit margins for resin producers. This price instability makes long-term planning challenging for both producers and downstream industries, potentially deterring new investments and stifling market growth.

Another substantial restraint is the increasing stringency of environmental regulations concerning plastic waste and pollution. Governments and international bodies are imposing stricter rules on plastic production, use, and disposal, including bans on single-use plastics and mandates for recycled content. While these regulations drive innovation towards sustainable solutions, they also pose significant challenges for manufacturers in terms of compliance costs, material redesign, and the establishment of robust recycling infrastructure, particularly for virgin plastic producers.

Furthermore, competition from alternative materials, such as metals, glass, ceramics, and thermosets, presents a continuous restraint for the thermoplastic resin market. While thermoplastics offer distinct advantages in many applications, other materials may be preferred for specific properties like extreme temperature resistance, high rigidity, or specific aesthetic requirements. For instance, in certain high-stress structural applications or high-heat environments, metals or composites might be chosen over thermoplastics, limiting market penetration in those niches. The ongoing development of advanced materials across different classes continually influences material selection decisions across industries.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices | -1.0% | Global, particularly regions dependent on imported feedstocks | Short to Medium Term (2025-2029) |

| Stringent Environmental Regulations and Plastic Bans | -0.9% | Europe, North America, parts of Asia Pacific | Medium to Long Term (2025-2033) |

| Competition from Alternative Materials | -0.7% | Global, specific high-performance applications | Long Term (2027-2033) |

Thermoplastic Resin Market Opportunities Analysis

Significant growth opportunities exist in the development and widespread adoption of bio-based and biodegradable thermoplastic resins. With increasing consumer awareness regarding environmental sustainability and governmental push for eco-friendly materials, the demand for plastics derived from renewable resources or those designed to degrade naturally is on the rise. This creates a vast market for innovative polymer solutions that can offer comparable performance to traditional plastics while addressing end-of-life concerns. Companies investing in research and development of these next-generation materials are well-positioned to capture a substantial share of future market growth.

The expanding application of thermoplastic resins in the healthcare and medical devices sector presents another promising opportunity. These resins are increasingly preferred for medical implants, diagnostic equipment, surgical instruments, and pharmaceutical packaging due to their biocompatibility, sterilizability, chemical resistance, and ease of fabrication. As the global population ages and healthcare expenditures continue to rise, the demand for advanced, safe, and reliable medical devices made from high-grade thermoplastic resins is expected to surge, driving market expansion in this specialized segment.

Furthermore, the rapid industrialization and urbanization in emerging economies, particularly in Asia Pacific and Latin America, offer considerable market opportunities. These regions are experiencing booming growth in construction, automotive, packaging, and consumer goods industries, leading to a substantial increase in the consumption of various thermoplastic resins. As these economies continue to develop, the demand for durable, versatile, and cost-effective material solutions will accelerate, providing fertile ground for market expansion for thermoplastic resin manufacturers and suppliers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Bio-based and Recycled Thermoplastic Resins | +1.3% | Global, especially Europe, North America | Medium to Long Term (2025-2033) |

| Increasing Application in Healthcare & Medical Devices | +1.1% | North America, Europe, parts of Asia Pacific | Medium to Long Term (2026-2033) |

| Market Penetration in Emerging Economies | +0.9% | Asia Pacific, Latin America, Middle East & Africa | Short to Long Term (2025-2033) |

Thermoplastic Resin Market Challenges Impact Analysis

The significant challenge of plastic waste management and the associated environmental concerns pose a considerable hurdle for the Thermoplastic Resin market. The accumulation of plastic waste in landfills and oceans has led to widespread public outcry and stricter regulations, creating negative perceptions around plastic use. While thermoplastics are theoretically recyclable, the complexities of collection, sorting, and processing different resin types, coupled with limitations in infrastructure, mean a substantial portion still ends up as waste. Addressing this requires significant investment in advanced recycling technologies and circular economy models, which are still in nascent stages for many regions.

Another critical challenge is the high capital investment required for establishing new production facilities or upgrading existing ones, especially for specialty and high-performance resins. The manufacturing processes for many advanced thermoplastics involve complex polymerization techniques and expensive equipment, necessitating substantial upfront financial commitments. This acts as a barrier to entry for new players and can slow down capacity expansion even for established manufacturers, potentially limiting the market's ability to meet surging demand in certain segments.

Furthermore, the industry faces challenges related to supply chain disruptions and geopolitical instability. As the production of raw materials for thermoplastics is often concentrated in a few regions or countries, geopolitical events, trade disputes, or natural disasters can severely impact the global supply chain. Such disruptions can lead to material shortages, increased freight costs, and delays in product delivery, affecting manufacturing schedules and overall market stability. Diversifying raw material sources and building more resilient supply chains are ongoing efforts to mitigate these risks.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Plastic Waste Management and Environmental Concerns | -1.1% | Global | Long Term (2025-2033) |

| High Capital Investment for New Production Capacities | -0.8% | Global, particularly for specialty resins | Medium to Long Term (2026-2033) |

| Supply Chain Volatility and Geopolitical Risks | -0.6% | Global, particularly import-dependent regions | Short to Medium Term (2025-2029) |

Thermoplastic Resin Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Thermoplastic Resin market, offering a detailed scope that covers historical data, current market dynamics, and future projections. It delivers critical insights into market size, growth drivers, restraints, opportunities, and challenges affecting the industry. The report segments the market by various types, applications, and geographic regions, providing a granular view of market performance and potential. It also includes an extensive competitive landscape analysis, profiling key players and their strategic initiatives, alongside an AI impact assessment to highlight technological influences.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 195.5 Billion |

| Market Forecast in 2033 | USD 330.1 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Polymer Solutions Inc., Advanced Materials Corp., Global Resin Technologies, DuraPlast Holdings, InnovaPolymers, EliteChem Plastics, Nexus Polymer Group, ChemTech Resins, Future Compounds Ltd., PrimePolymer Innovations, SynthoPlast Group, Vertex Materials, EcoPlas Systems, Allied Polymer Solutions, MegaResin Corp., Stellar Polymers, NeoChem Industries, Precision Plastic Corp., Genesis Materials, Quantum Polymers |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Thermoplastic Resin market is meticulously segmented to provide a granular understanding of its diverse components and drivers. This segmentation allows for targeted analysis of market dynamics across different material types, end-use applications, and geographical regions, offering a comprehensive view of consumption patterns, growth pockets, and competitive landscapes. Understanding these segments is crucial for stakeholders to identify lucrative opportunities and formulate effective market strategies tailored to specific product categories or industry verticals.

The market is primarily segmented by type, differentiating between various chemical compositions and their specific properties, such as polyethylene, polypropylene, and polyvinyl chloride, along with a range of engineering and high-performance thermoplastics. Each type possesses unique characteristics that make it suitable for particular applications. The application-based segmentation further categorizes the market by end-use industries, including packaging, automotive, construction, and electrical and electronics, reflecting how different sectors utilize these versatile materials. This multi-dimensional segmentation highlights the broad applicability of thermoplastic resins and their critical role in modern industrial ecosystems, influencing design, manufacturing, and consumer product development.

- By Type: Polyethylene (HDPE, LDPE, LLDPE), Polypropylene, Polyvinyl Chloride, Polystyrene, Polyethylene Terephthalate, Acrylonitrile Butadiene Styrene, Polycarbonate, Polyamide, Polyoxymethylene, Polymethyl Methacrylate, Polybutylene Terephthalate, Others.

- By Application: Packaging, Automotive & Transportation, Construction, Electrical & Electronics, Consumer Goods, Medical & Healthcare, Industrial & Machinery, Textiles, Agriculture, Others.

- By Region: North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA).

Regional Highlights

- Asia Pacific (APAC): Dominates the Thermoplastic Resin market in terms of consumption and production, driven by rapid industrialization, burgeoning manufacturing sectors in China and India, and increasing demand from packaging, automotive, and construction industries. The region is a global manufacturing hub, leading to high material consumption.

- North America: A significant market characterized by high adoption of specialty and high-performance thermoplastics, particularly in the automotive, aerospace, and medical sectors. The region emphasizes technological innovation, lightweighting trends, and sustainable solutions, driving demand for advanced resin types.

- Europe: Exhibits a strong focus on sustainability, stringent environmental regulations, and the circular economy. This drives demand for recycled and bio-based thermoplastic resins. The automotive, construction, and packaging industries are key consumers, with a strong emphasis on eco-friendly and high-quality materials.

- Latin America: Expected to show steady growth due to increasing industrialization, infrastructure development, and growing consumer demand for packaged goods. Brazil and Mexico are key contributors, with rising investment in manufacturing and construction.

- Middle East and Africa (MEA): Emerging as a growth market, particularly in the construction, packaging, and automotive sectors. Significant investments in infrastructure development, economic diversification efforts, and an expanding consumer base are fueling the demand for thermoplastic resins.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Thermoplastic Resin Market.- Polymer Solutions Inc.

- Advanced Materials Corp.

- Global Resin Technologies

- DuraPlast Holdings

- InnovaPolymers

- EliteChem Plastics

- Nexus Polymer Group

- ChemTech Resins

- Future Compounds Ltd.

- PrimePolymer Innovations

- SynthoPlast Group

- Vertex Materials

- EcoPlas Systems

- Allied Polymer Solutions

- MegaResin Corp.

- Stellar Polymers

- NeoChem Industries

- Precision Plastic Corp.

- Genesis Materials

- Quantum Polymers

Frequently Asked Questions

What are the primary types of thermoplastic resins and their common uses?

Thermoplastic resins are a broad category of polymers that become moldable when heated and solidify upon cooling, a process that can be repeated. Key types include Polyethylene (PE) for packaging films and pipes, Polypropylene (PP) for automotive parts and containers, Polyvinyl Chloride (PVC) for pipes and window frames, Polyethylene Terephthalate (PET) for bottles and fibers, and engineering plastics like Polyamide (PA) and Polycarbonate (PC) for high-performance applications in electronics and automotive.

How do thermoplastic resins differ from thermoset resins?

The fundamental difference lies in their behavior when heated. Thermoplastic resins can be melted and reshaped multiple times without significant degradation, making them recyclable. Thermoset resins, once cured through heating or chemical reaction, form irreversible chemical bonds and cannot be remelted or reshaped, often making them more challenging to recycle but providing superior heat and chemical resistance in their final form.

What is driving the demand for thermoplastic resins in the automotive industry?

The automotive industry's demand for thermoplastic resins is primarily driven by the need for lightweighting to improve fuel efficiency and reduce emissions, especially in the context of electric vehicles. Thermoplastics offer an excellent strength-to-weight ratio, enabling manufacturers to reduce vehicle mass while maintaining structural integrity and safety. They are also used for interior components, battery housings, and various under-the-hood applications due to their design flexibility and cost-effectiveness.

What are the key sustainability trends impacting the thermoplastic resin market?

Key sustainability trends include the increasing adoption of bio-based resins derived from renewable resources, the integration of recycled content into new products, and the development of advanced recycling technologies to facilitate a circular economy. There is also a strong focus on designing products for easier recycling and reducing overall plastic waste through improved material selection and lifecycle management.

What role does AI play in the future of thermoplastic resin manufacturing?

AI is increasingly vital in thermoplastic resin manufacturing, enhancing areas such as material discovery and formulation optimization through predictive modeling, improving process efficiency and quality control via real-time data analysis, and optimizing supply chain logistics and demand forecasting. AI's capabilities lead to reduced waste, accelerated innovation cycles, and more resilient and responsive production systems, contributing significantly to operational excellence and sustainability goals.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted