Polyvinyl Chloride Resin Market

Polyvinyl Chloride Resin Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704433 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Polyvinyl Chloride Resin Market Size

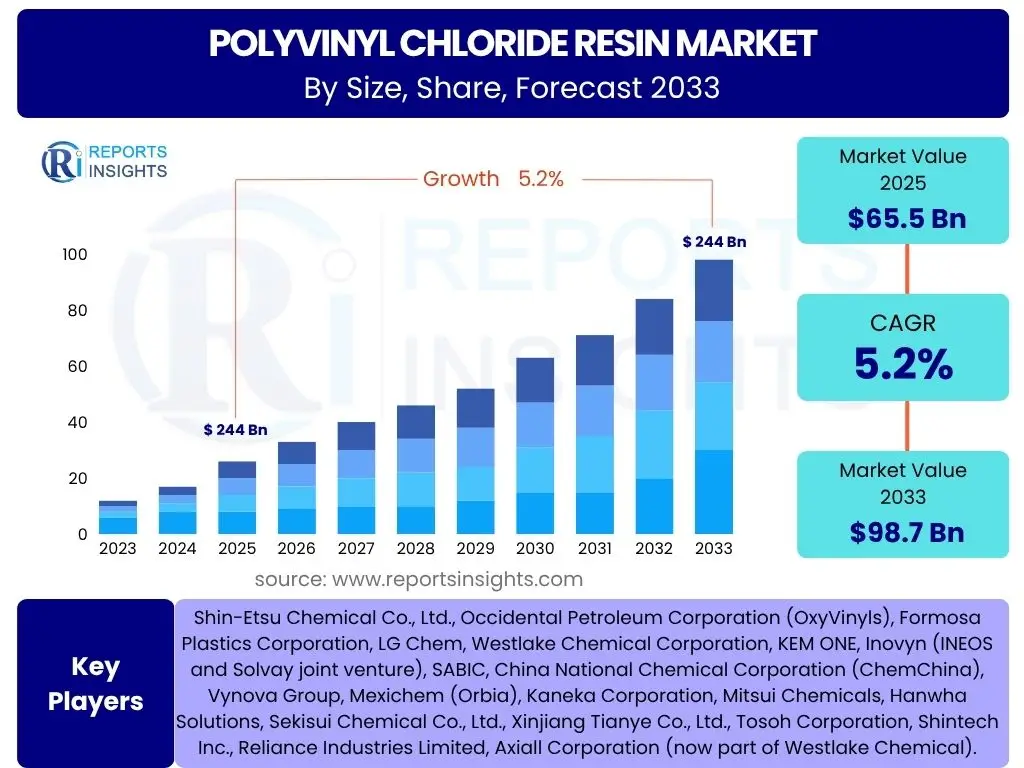

According to Reports Insights Consulting Pvt Ltd, The Polyvinyl Chloride Resin Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.2% between 2025 and 2033. The market is estimated at USD 65.5 Billion in 2025 and is projected to reach USD 98.7 Billion by the end of the forecast period in 2033.

Key Polyvinyl Chloride Resin Market Trends & Insights

The Polyvinyl Chloride (PVC) resin market is currently experiencing significant transformative trends driven by evolving consumer demands, stringent environmental regulations, and advancements in material science. Key areas of focus include the increasing adoption of sustainable practices, the development of specialized PVC grades for high-performance applications, and the impact of digitalization on manufacturing and supply chain efficiencies. Stakeholders are particularly interested in how recycling initiatives and bio-based PVC alternatives will reshape the industry landscape, alongside the ongoing expansion in critical end-use sectors such as construction and infrastructure.

Furthermore, there is a growing emphasis on product innovation, with manufacturers exploring new formulations that offer enhanced durability, flexibility, and fire resistance, catering to diverse application requirements. The regional shifts in manufacturing capabilities and consumption patterns also play a crucial role, with emerging economies driving substantial demand. These trends collectively indicate a market moving towards greater efficiency, environmental responsibility, and application versatility, responding to global imperatives for sustainable development and optimized resource utilization.

- Increasing demand for sustainable and recyclable PVC solutions, including mechanically and chemically recycled PVC.

- Development of bio-based PVC and phthalate-free plasticizers to address environmental and health concerns.

- Growth in infrastructure and construction projects globally, particularly in developing economies.

- Rising adoption of specialized PVC grades for enhanced performance in applications such as medical devices and automotive components.

- Focus on lightweighting and durability in end-use applications, driving innovation in PVC compounds.

- Integration of smart manufacturing and automation technologies in PVC production for improved efficiency.

AI Impact Analysis on Polyvinyl Chloride Resin

The integration of Artificial Intelligence (AI) into the Polyvinyl Chloride (PVC) resin sector is poised to revolutionize various aspects of its value chain, from raw material procurement to end-product delivery. Common inquiries highlight user interest in AI's potential to optimize production processes, enhance quality control, and streamline supply chain management. AI algorithms can analyze vast datasets from manufacturing plants to predict equipment failures, optimize energy consumption, and fine-tune polymerization parameters, leading to improved yield and reduced operational costs. This predictive capability directly addresses the industry's need for greater efficiency and reliability in production, reducing downtime and waste.

Beyond manufacturing, AI is also expected to significantly impact research and development (R&D) by accelerating the discovery and formulation of new PVC compounds with desired properties, such as enhanced sustainability or specific performance characteristics. Supply chain optimization, a critical concern for global industries, can benefit from AI-driven demand forecasting, inventory management, and logistics planning, mitigating disruptions and improving responsiveness. While the initial investment in AI infrastructure may be substantial, the long-term benefits in terms of operational excellence, material innovation, and market responsiveness are anticipated to drive significant competitive advantages for early adopters in the PVC resin market.

- Optimization of manufacturing processes through predictive analytics, reducing energy consumption and waste.

- Enhanced quality control and defect detection using machine learning algorithms for real-time monitoring.

- Improved supply chain efficiency and resilience via AI-driven demand forecasting and logistics optimization.

- Acceleration of new PVC compound development and material innovation through AI-powered R&D.

- Predictive maintenance for production equipment, minimizing downtime and increasing operational reliability.

- Data-driven market analysis and trend prediction for strategic decision-making and product positioning.

Key Takeaways Polyvinyl Chloride Resin Market Size & Forecast

The Polyvinyl Chloride (PVC) resin market is on a trajectory of steady growth, driven by resilient demand from the construction, infrastructure, and packaging sectors, particularly in emerging economies. A key insight from the market forecast is the increasing importance of sustainability, with a clear shift towards recycled and bio-based PVC solutions in response to regulatory pressures and heightened environmental consciousness among consumers and industries. This sustainability imperative is not merely a compliance issue but a significant driver of innovation and competitive differentiation within the market.

Furthermore, the forecast underscores the criticality of technological advancements in manufacturing processes and material science, which are enabling the production of PVC with enhanced performance characteristics and a reduced environmental footprint. Regional dynamics, especially the rapid urbanization and industrialization in Asia Pacific, will continue to play a pivotal role in shaping market demand and supply. Overall, the market's future is characterized by a balance between conventional application growth and transformative shifts towards more sustainable and technologically advanced PVC solutions, necessitating strategic adaptations from industry players to capitalize on emerging opportunities and mitigate evolving challenges.

- The Polyvinyl Chloride Resin market is projected for robust growth, largely fueled by ongoing infrastructure development and construction activities globally.

- Sustainability initiatives, including increased recycling rates and the development of bio-based PVC, are central to the market's long-term viability and growth.

- Asia Pacific is anticipated to remain the dominant and fastest-growing region, driven by rapid industrialization and urbanization.

- Technological advancements in PVC formulation and processing are critical for meeting evolving performance demands and environmental standards.

- Diversification into specialized applications, such as medical and automotive, will contribute significantly to market expansion.

Polyvinyl Chloride Resin Market Drivers Analysis

The Polyvinyl Chloride (PVC) resin market is propelled by a confluence of macroeconomic and industry-specific factors that consistently stimulate demand across various end-use sectors. A primary driver is the robust growth in the construction and infrastructure industry, particularly in developing economies. PVC's versatility, durability, and cost-effectiveness make it an indispensable material for pipes, fittings, window profiles, and flooring, all of which are critical components of urban development and infrastructure projects. The global push for improved sanitation, water supply networks, and affordable housing further underpins this demand, ensuring a steady consumption of PVC resin.

Additionally, the burgeoning packaging industry and the consistent demand from the automotive and electrical & electronics sectors contribute significantly to market expansion. PVC is used in flexible packaging films, wire and cable insulation, and various interior components in automobiles due to its excellent insulation properties, chemical resistance, and ease of processing. The continuous innovation in PVC compounding to meet specific performance requirements, such as fire retardancy or enhanced flexibility, also acts as a driver, opening new application avenues and sustaining existing ones. These drivers collectively create a strong foundation for sustained growth in the PVC resin market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Construction and Infrastructure Spending | +1.8-2.5% | Asia Pacific (China, India), North America, Middle East & Africa | Medium-to-Long Term (2025-2033) |

| Increasing Demand from Packaging Industry | +0.9-1.3% | Global, particularly Asia Pacific & Latin America | Medium Term (2025-2029) |

| Expansion of Automotive Sector | +0.7-1.1% | Asia Pacific (China, Japan), Europe, North America | Medium Term (2025-2030) |

| Rise in Electrical & Electronics Applications | +0.6-1.0% | Global, especially Southeast Asia, China | Short-to-Medium Term (2025-2028) |

| Cost-Effectiveness and Versatility of PVC | +1.0-1.5% | Global | Long Term (2025-2033) |

Polyvinyl Chloride Resin Market Restraints Analysis

Despite its widespread utility, the Polyvinyl Chloride (PVC) resin market faces significant restraints, primarily stemming from environmental concerns and increasing regulatory scrutiny. The perception of PVC as an environmentally problematic material due to its chlorine content, the release of dioxins during incineration, and issues with plasticizers (like phthalates) has led to bans or restrictions in various applications and regions. This negative public perception and the associated regulatory pressures drive industries and consumers towards alternative materials, thereby limiting PVC's market penetration and growth, especially in developed economies with strong environmental movements.

Furthermore, the volatility of raw material prices, particularly ethylene and chlorine, which are key feedstocks for PVC production, poses a considerable challenge. Fluctuations in crude oil prices and global supply chain disruptions can directly impact production costs and profit margins for PVC manufacturers, leading to price instability in the market. Competition from substitute materials such as polyethylene (PE), polypropylene (PP), and alternative piping materials like concrete and ductile iron, also acts as a restraint. These substitutes often gain favor where sustainability concerns are high or specific performance requirements can be met more effectively by non-PVC options, compelling PVC producers to innovate continually to maintain competitiveness.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Environmental Concerns and Regulations | -1.5-2.0% | Europe, North America, Japan | Long Term (2025-2033) |

| Volatile Raw Material Prices (Ethylene, Chlorine) | -0.8-1.2% | Global | Short-to-Medium Term (2025-2028) |

| Competition from Substitute Materials | -0.6-1.0% | Global | Medium-to-Long Term (2025-2033) |

| Health Concerns Related to Additives (e.g., Phthalates) | -0.5-0.9% | Europe, North America, select Asian countries | Long Term (2025-2033) |

| High Energy Consumption in Production | -0.4-0.7% | Global, particularly regions with high energy costs | Long Term (2025-2033) |

Polyvinyl Chloride Resin Market Opportunities Analysis

The Polyvinyl Chloride (PVC) resin market is rich with emerging opportunities driven by innovation, sustainability trends, and the expansion into niche applications. A significant opportunity lies in the burgeoning demand for sustainable PVC solutions, including recycled PVC and bio-based alternatives. As environmental regulations tighten and corporate sustainability goals become more ambitious, investments in advanced recycling technologies, such as chemical recycling, and the development of PVC derived from renewable feedstocks offer manufacturers a strategic avenue for growth and market differentiation. This shift caters to a growing segment of environmentally conscious consumers and industries, providing a competitive edge.

Moreover, the continuous expansion of application areas, particularly in lightweighting for the automotive industry, durable materials for renewable energy infrastructure (e.g., solar panel components), and specialized medical devices, presents substantial growth prospects. The demand for compact, durable, and cost-effective materials in these advanced applications aligns perfectly with PVC's inherent properties when properly formulated. Furthermore, growth in emerging economies, coupled with significant investments in smart city projects and digitalization initiatives, creates new avenues for PVC applications in advanced building materials, connectivity infrastructure, and smart consumer goods. These opportunities require strategic foresight and investment in research and development to fully capitalize on market shifts and technological advancements.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Recycling Technologies for PVC | +1.0-1.5% | Europe, North America, Japan | Long Term (2028-2033) |

| Increasing Adoption of Bio-based and Sustainable PVC | +0.8-1.2% | Europe, North America, Global industries | Medium-to-Long Term (2026-2033) |

| Expansion into New Applications (e.g., Medical, Renewable Energy) | +0.7-1.0% | Global | Medium Term (2025-2030) |

| Growth in Emerging Markets and Urbanization Initiatives | +0.9-1.4% | Asia Pacific, Latin America, Middle East & Africa | Long Term (2025-2033) |

| Innovation in PVC Compounding for Enhanced Performance | +0.6-0.9% | Global | Short-to-Medium Term (2025-2028) |

Polyvinyl Chloride Resin Market Challenges Impact Analysis

The Polyvinyl Chloride (PVC) resin market faces several inherent and evolving challenges that can impede its growth and sustainability. A significant challenge is the persistent negative public perception and health concerns associated with PVC, particularly regarding plasticizers like phthalates and the potential for harmful emissions during PVC product disposal or incineration. This perception issue necessitates substantial industry efforts in communication, research into safer additives, and investment in environmentally sound disposal and recycling infrastructure to regain public trust and avoid further regulatory tightening.

Furthermore, managing the complex waste stream of PVC products, especially long-life applications like pipes and window profiles, presents a logistical and technological hurdle. While recycling initiatives are gaining traction, the sheer volume and diversity of PVC waste require advanced sorting and processing capabilities that are not yet universally available or economically viable at scale. Energy intensity of PVC production also remains a challenge, as manufacturers grapple with rising energy costs and the imperative to reduce carbon footprints. Addressing these challenges effectively requires collaborative efforts across the value chain, significant capital investment in green technologies, and continuous innovation in sustainable manufacturing practices to ensure the long-term competitiveness and acceptance of PVC.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Overcoming Negative Public Perception and Health Concerns | -1.2-1.8% | Global, particularly developed economies | Long Term (2025-2033) |

| Development of Robust PVC Waste Management & Recycling Infrastructure | -0.7-1.1% | Global, especially Europe & North America | Long Term (2028-2033) |

| Compliance with Evolving Environmental Regulations | -0.6-0.9% | Europe, North America, Japan | Medium-to-Long Term (2025-2033) |

| High Energy Consumption and Carbon Footprint of Production | -0.5-0.8% | Global | Medium-to-Long Term (2025-2033) |

| Ensuring Consistent Quality Amidst Supply Chain Disruptions | -0.4-0.7% | Global | Short-to-Medium Term (2025-2028) |

Polyvinyl Chloride Resin Market - Updated Report Scope

This comprehensive report delves into the Polyvinyl Chloride (PVC) Resin market, providing an in-depth analysis of its current size, historical trends, and future growth projections from 2025 to 2033. It meticulously examines key market drivers, restraints, opportunities, and challenges influencing the industry landscape, offering strategic insights for stakeholders. The report segments the market by type, application, and end-use industry, providing a granular view of market dynamics across various categories and geographies. Furthermore, it includes a detailed competitive analysis of leading market players, their strategies, and recent developments, ensuring a holistic understanding of the global PVC resin market for informed decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 65.5 Billion |

| Market Forecast in 2033 | USD 98.7 Billion |

| Growth Rate | 5.2% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Shin-Etsu Chemical Co., Ltd., Occidental Petroleum Corporation (OxyVinyls), Formosa Plastics Corporation, LG Chem, Westlake Chemical Corporation, KEM ONE, Inovyn (INEOS and Solvay joint venture), SABIC, China National Chemical Corporation (ChemChina), Vynova Group, Mexichem (Orbia), Kaneka Corporation, Mitsui Chemicals, Hanwha Solutions, Sekisui Chemical Co., Ltd., Xinjiang Tianye Co., Ltd., Tosoh Corporation, Shintech Inc., Reliance Industries Limited, Axiall Corporation (now part of Westlake Chemical). |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Polyvinyl Chloride (PVC) resin market is comprehensively segmented to provide a granular understanding of its diverse applications and product types, allowing for precise market analysis and strategic planning. These segmentations enable stakeholders to identify key growth areas, understand demand drivers for specific PVC forms, and tailor their product offerings to meet industry-specific requirements. The market is primarily categorized by the type of PVC resin, which dictates its processing characteristics and end-use suitability. Further segmentation by application highlights the vast array of products manufactured using PVC, from industrial components to consumer goods.

Additionally, the segmentation by end-use industry provides crucial insights into the sectors that are the primary consumers of PVC resin. This detailed breakdown helps in assessing the impact of sectoral growth trends, regulatory changes, and technological advancements on PVC demand. Understanding these intricate segmentations is vital for manufacturers, suppliers, and investors to navigate the complexities of the global PVC market, identify lucrative opportunities, and develop targeted strategies for market penetration and expansion.

- By Type:

- Suspension PVC (S-PVC): Dominant type, widely used in pipes, profiles, and general-purpose applications.

- Emulsion PVC (E-PVC): Used for paste applications, coatings, and specialized products requiring fine particles.

- Paste PVC: Utilized in artificial leather, flooring, and certain automotive parts due to its processability into pastes.

- By Application:

- Pipes & Fittings: Extensive use in construction, plumbing, irrigation, and drainage systems.

- Profiles: Employed in window frames, door frames, and other architectural elements.

- Films & Sheets: Used for packaging, stationery, medical bags, and decorative films.

- Wires & Cables: Critical for insulation and jacketing in electrical and communication cables.

- Flooring: Durable and water-resistant option for residential, commercial, and industrial flooring.

- Bottles: Used for packaging various liquids, though less common than PET in some regions.

- Medical Devices: Applications in blood bags, tubing, and medical disposables due to flexibility and sterilization capabilities.

- Others: Includes coated fabrics, consumer goods, footwear components, and automotive parts.

- By End-use Industry:

- Construction: The largest end-use sector, encompassing pipes, profiles, flooring, and roofing.

- Packaging: Flexible and rigid packaging applications, including films and blister packs.

- Automotive: Interior components, wire harnesses, and under-the-hood applications.

- Electrical & Electronics: Wire and cable insulation, conduits, and electronic component housings.

- Healthcare: Medical tubing, blood bags, and other disposable medical equipment.

- Consumer Goods: Toys, footwear, sporting goods, and household items.

- Agriculture: Irrigation pipes, greenhouse films, and various agricultural equipment.

- Others: Furniture, textiles, and various industrial applications.

Regional Highlights

- Asia Pacific (APAC): Dominates the global Polyvinyl Chloride (PVC) Resin market, driven by rapid urbanization, extensive infrastructure development projects, and booming construction activities, especially in China, India, and Southeast Asian countries. The region is also a major manufacturing hub for various PVC-consuming industries, leading to high consumption rates.

- North America: A mature market characterized by steady demand from the construction, automotive, and electrical & electronics sectors. Focus on sustainable building materials and advanced recycling initiatives is gaining traction, influencing market trends.

- Europe: Exhibits moderate growth, with strong emphasis on circular economy principles and stringent environmental regulations driving the adoption of recycled PVC and bio-based alternatives. Germany, France, and the UK are key markets within the region, with significant R&D in sustainable PVC solutions.

- Latin America: Expected to witness significant growth, fueled by increasing investment in infrastructure development and housing projects in countries like Brazil and Mexico. The region offers opportunities for market expansion due to industrial growth and urbanization.

- Middle East and Africa (MEA): Emerging as a promising market due to ongoing large-scale construction projects, diversification of economies, and increasing demand for basic infrastructure. Investment in industrial development and a growing population base contribute to the market's potential.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Polyvinyl Chloride Resin Market.- Shin-Etsu Chemical Co., Ltd.

- Occidental Petroleum Corporation (OxyVinyls)

- Formosa Plastics Corporation

- LG Chem

- Westlake Chemical Corporation

- KEM ONE

- Inovyn (INEOS and Solvay joint venture)

- SABIC

- China National Chemical Corporation (ChemChina)

- Vynova Group

- Mexichem (Orbia)

- Kaneka Corporation

- Mitsui Chemicals

- Hanwha Solutions

- Sekisui Chemical Co., Ltd.

- Xinjiang Tianye Co., Ltd.

- Tosoh Corporation

- Shintech Inc.

- Reliance Industries Limited

- Axiall Corporation (now part of Westlake Chemical)

Frequently Asked Questions

What is Polyvinyl Chloride Resin (PVC) and its primary uses?

Polyvinyl Chloride Resin (PVC) is a widely used synthetic plastic polymer known for its durability, versatility, and cost-effectiveness. It is primarily used in the construction sector for pipes, fittings, window profiles, and flooring, as well as in packaging, electrical wires, medical devices, and automotive components due to its excellent insulation properties, chemical resistance, and flexibility.

What are the key drivers of growth in the Polyvinyl Chloride Resin market?

The key growth drivers for the PVC resin market include robust expansion in the global construction and infrastructure industries, increasing demand from the packaging sector, steady growth in automotive and electrical & electronics applications, and the inherent cost-effectiveness and versatility of PVC as a material. Rapid urbanization, particularly in Asia Pacific, also significantly contributes to demand.

What are the major environmental concerns associated with PVC and how is the industry addressing them?

Major environmental concerns linked to PVC include its chlorine content, the potential release of dioxins during incineration, and the use of certain plasticizers like phthalates. The industry is actively addressing these by investing in advanced recycling technologies, developing bio-based PVC, phasing out problematic additives, and promoting sustainable manufacturing practices to improve PVC's environmental profile.

Which region dominates the Polyvinyl Chloride Resin market, and why?

The Asia Pacific region dominates the Polyvinyl Chloride Resin market. This dominance is attributed to rapid industrialization, extensive infrastructure development, high rates of urbanization, and significant construction activities, particularly in countries like China, India, and other Southeast Asian nations, leading to substantial demand across various end-use industries.

How is Artificial Intelligence (AI) impacting the Polyvinyl Chloride Resin industry?

AI is impacting the PVC industry by optimizing manufacturing processes through predictive analytics, enhancing quality control and defect detection, streamlining supply chain management via demand forecasting, and accelerating the development of new PVC compounds. AI integration aims to improve operational efficiency, reduce costs, and foster material innovation within the sector.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted