System Integrator in Oil and Gas Market

System Integrator in Oil and Gas Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709828 | Last Updated : December 17, 2025 |

Format : ![]()

![]()

![]()

![]()

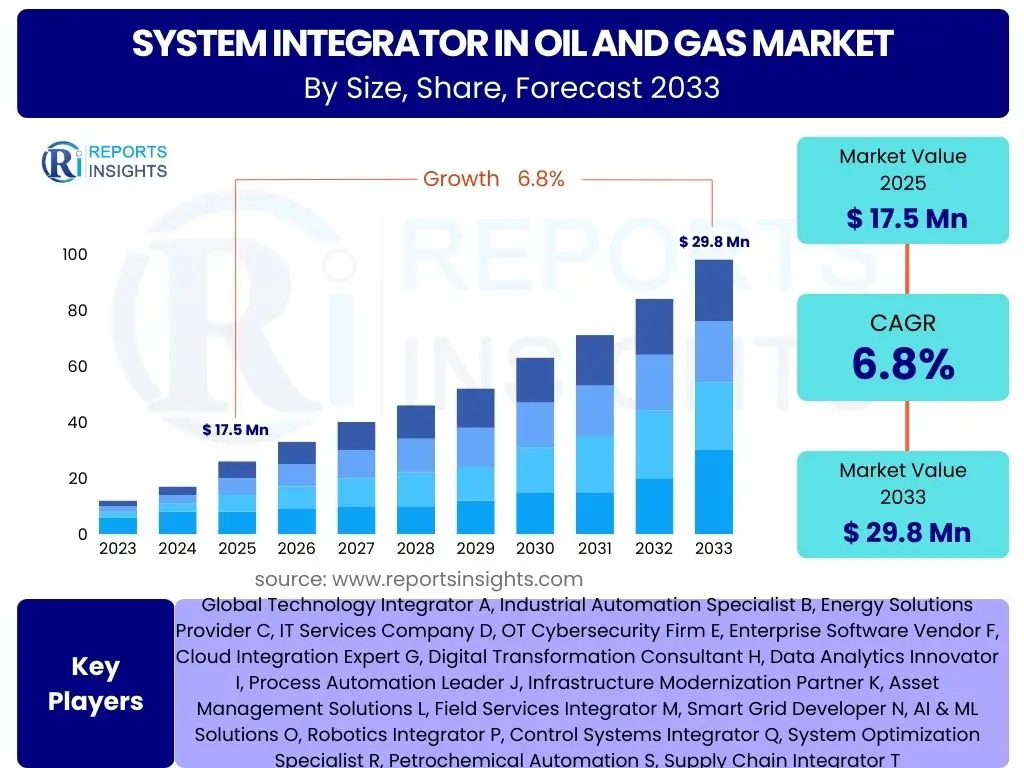

System Integrator in Oil and Gas Market Size

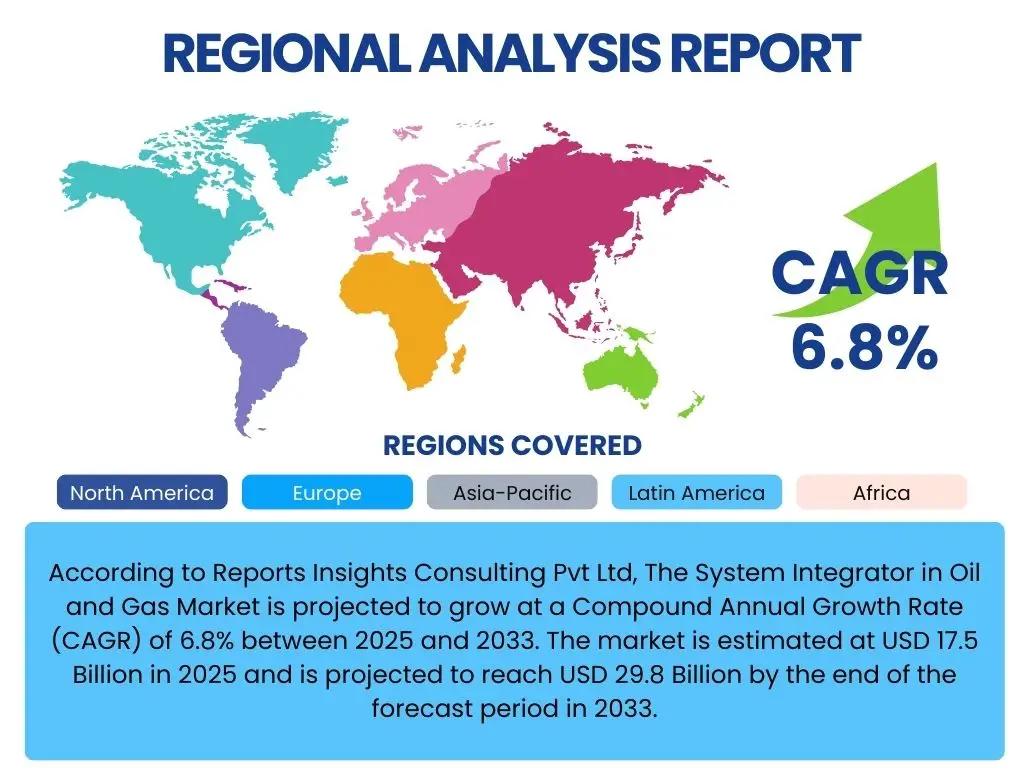

According to Reports Insights Consulting Pvt Ltd, The System Integrator in Oil and Gas Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 17.5 Billion in 2025 and is projected to reach USD 29.8 Billion by the end of the forecast period in 2033.

Key System Integrator in Oil and Gas Market Trends & Insights

The System Integrator in Oil and Gas market is currently experiencing significant transformative trends driven by the imperative for operational efficiency, cost reduction, and enhanced safety within a volatile global energy landscape. Industry stakeholders are increasingly prioritizing digital transformation initiatives, leading to a surge in demand for sophisticated integration services. These services encompass everything from the deployment of advanced analytics platforms to the modernization of legacy infrastructure, ensuring seamless data flow and process optimization across the entire oil and gas value chain.

Another prominent trend involves the growing emphasis on cybersecurity and data privacy. As operational technologies (OT) converge with information technologies (IT), the attack surface for cyber threats expands significantly. System integrators are therefore tasked with implementing robust, multi-layered security solutions that protect critical infrastructure from sophisticated attacks, ensuring business continuity and regulatory compliance. Furthermore, the push towards sustainability and decarbonization is influencing project scopes, with integrators increasingly involved in projects supporting renewable energy integration, carbon capture utilization and storage (CCUS), and energy management systems aimed at reducing the environmental footprint of oil and gas operations.

Finally, the adoption of cloud-based solutions and the Internet of Things (IoT) is fundamentally reshaping how data is collected, processed, and utilized. System integrators are crucial in migrating existing on-premise systems to secure cloud environments, enabling remote monitoring, predictive maintenance, and real-time decision-making. This shift not only improves agility and scalability but also facilitates greater collaboration and transparency across geographically dispersed assets.

- Enhanced Digitalization and Automation Across Upstream, Midstream, and Downstream Operations.

- Increasing Adoption of Cloud Computing and Edge Analytics for Data Processing and Storage.

- Heightened Focus on Cybersecurity Solutions for Operational Technology (OT) and Information Technology (IT) Convergence.

- Integration of Advanced Analytics and Artificial Intelligence (AI) for Predictive Maintenance and Operational Optimization.

- Growing Demand for Sustainable and Environmentally Compliant Solutions, Including Energy Management and Carbon Reduction Technologies.

- Expansion of IoT Devices and Sensors for Real-Time Monitoring and Data Collection.

- Strategic Partnerships and Collaborations Between Technology Providers and System Integrators to Offer Comprehensive Solutions.

AI Impact Analysis on System Integrator in Oil and Gas

Artificial intelligence is profoundly revolutionizing the System Integrator in Oil and Gas market, transforming how operations are managed, optimized, and secured. User inquiries frequently center on AI's capability to enhance predictive maintenance, automate complex processes, and derive actionable insights from vast datasets. The core expectation is that AI will significantly reduce unplanned downtime, optimize resource allocation, and improve safety protocols, thereby delivering substantial cost savings and operational efficiencies. System integrators are at the forefront of this shift, tasked with designing and implementing AI-driven solutions that integrate seamlessly with existing legacy infrastructure.

Concerns often raised by users include the complexity of integrating AI models into diverse operational technology (OT) environments, the need for specialized skillsets, and the ethical implications of autonomous decision-making. Data quality and availability are also significant considerations, as effective AI deployment relies heavily on clean, reliable data streams from sensors and operational systems. System integrators play a critical role in addressing these challenges by developing robust data governance frameworks, building scalable AI infrastructures, and ensuring proper validation and calibration of AI algorithms to meet industry-specific safety and performance standards.

Ultimately, the influence of AI extends beyond mere automation to creating more intelligent, adaptive, and resilient oil and gas operations. It enables real-time anomaly detection, optimizes drilling parameters, enhances reservoir management, and improves energy trading strategies. For system integrators, this translates into a growing demand for expertise in machine learning model development, data science, specialized AI platform integration, and ongoing AI system maintenance and optimization, positioning them as pivotal enablers of the industry's digital future.

- AI enhances predictive maintenance, reducing equipment downtime and operational costs.

- Automated data analysis and pattern recognition improve decision-making in exploration and production.

- Optimized supply chain and logistics through AI-driven forecasting and route optimization.

- Increased safety by identifying potential hazards and enabling autonomous monitoring.

- Real-time process optimization and control in refining and petrochemical operations.

- Cybersecurity enhancements through AI-powered threat detection and anomaly identification.

- Development of intelligent energy management systems for improved efficiency and reduced emissions.

Key Takeaways System Integrator in Oil and Gas Market Size & Forecast

A primary takeaway from the System Integrator in Oil and Gas market analysis is the robust growth trajectory, underscoring the indispensable role of integration services in the industry's ongoing digital transformation. The projected substantial increase in market valuation from USD 17.5 Billion in 2025 to USD 29.8 Billion by 2033, at a CAGR of 6.8%, highlights a sustained and expanding demand for specialized integration expertise. This growth is not merely incremental but reflective of a fundamental shift towards leveraging advanced technologies to achieve operational excellence, regulatory compliance, and competitive advantage in a complex global energy market.

Furthermore, the market's expansion is intrinsically linked to the imperative for enhanced efficiency, safety, and environmental stewardship. Companies are investing heavily in solutions that streamline processes, mitigate risks, and reduce their carbon footprint, all of which necessitate sophisticated system integration. The convergence of IT and OT, coupled with the widespread adoption of IoT, AI, and cloud technologies, mandates a comprehensive integration strategy that only specialized system integrators can effectively deliver. This strategic shift solidifies the market's long-term viability and importance.

Finally, a critical insight reveals that successful market penetration and growth for system integrators will hinge on their ability to offer highly specialized, scalable, and secure solutions tailored to the unique challenges of the oil and gas sector. This includes expertise in legacy system modernization, cybersecurity, and the integration of emerging technologies for data analytics and automation. The competitive landscape will favor integrators who can demonstrate a deep understanding of industry-specific operational complexities and deliver tangible value through innovative, integrated solutions.

- Significant market expansion expected, driven by digital transformation initiatives.

- Crucial role of system integrators in facilitating IT/OT convergence and data integration.

- Strong demand for solutions enhancing operational efficiency, safety, and environmental compliance.

- Increased investment in advanced technologies such as AI, IoT, and cloud computing.

- Cybersecurity and data integrity remain paramount concerns, driving specialized integration services.

- Market growth is global, with particular emphasis on regions with active oil and gas exploration and production.

- The need for customized and scalable integration solutions is a key determinant for market success.

System Integrator in Oil and Gas Market Drivers Analysis

The System Integrator in Oil and Gas market is significantly propelled by several powerful drivers, primarily the global push for digital transformation across all segments of the industry. As oil and gas companies seek to optimize complex operations, reduce costs, and enhance safety, the adoption of advanced technologies like IoT, AI, and cloud computing becomes imperative. System integrators are critical enablers in this journey, providing the expertise to seamlessly integrate these disparate technologies into existing infrastructure, thereby unlocking new efficiencies and capabilities.

Another major driver is the increasing focus on operational efficiency and asset performance management. Fluctuating commodity prices and rising operational costs compel companies to seek solutions that minimize downtime, optimize production, and extend asset lifecycles. System integrators offer tailored solutions for predictive maintenance, real-time monitoring, and data analytics, which are essential for achieving these objectives. By integrating sensor data with enterprise systems, they create comprehensive views of asset health, enabling proactive decision-making and preventing costly failures.

Furthermore, stringent regulatory requirements and growing environmental concerns are driving investments in more sustainable and compliant operations. Companies are under pressure to reduce emissions, manage waste effectively, and ensure worker safety, necessitating integrated systems for environmental monitoring, process control, and regulatory reporting. System integrators facilitate the implementation of these complex solutions, ensuring that oil and gas operations not only meet but exceed compliance standards, thus enhancing their social license to operate.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Digital Transformation Initiatives | +1.5% | Global, particularly North America, Europe, APAC | Short to Medium-Term (2025-2029) |

| Emphasis on Operational Efficiency & Cost Reduction | +1.2% | Global, all major oil & gas regions | Medium to Long-Term (2026-2033) |

| Rising Adoption of Industrial IoT and AI/ML | +1.0% | North America, Europe, Middle East, Asia Pacific | Short to Medium-Term (2025-2030) |

| Aging Infrastructure Modernization Needs | +0.8% | North America, Europe, Russia, China | Medium to Long-Term (2027-2033) |

| Increased Focus on Cybersecurity in OT/IT Environments | +0.7% | Global, all regions with critical infrastructure | Short to Long-Term (2025-2033) |

System Integrator in Oil and Gas Market Restraints Analysis

Despite the robust growth drivers, the System Integrator in Oil and Gas market faces several significant restraints that could temper its expansion. One primary restraint is the inherent complexity and high cost associated with integrating advanced digital solutions into existing legacy infrastructure. Many oil and gas assets are decades old, featuring proprietary systems and diverse data formats, making interoperability a substantial challenge. The capital expenditure required for such modernization projects, coupled with the potential for operational disruptions, often makes companies hesitant to fully commit to large-scale integration efforts.

Another key restraint is the acute shortage of specialized talent possessing both deep domain knowledge in oil and gas operations and expertise in cutting-edge digital technologies like AI, IoT, and cybersecurity. The convergence of IT and OT demands a unique skillset that is scarce in the market. This talent gap not only drives up the cost of hiring and retaining skilled professionals but also delays project timelines and impacts the quality of integrated solutions, thereby limiting the pace of technological adoption across the industry.

Furthermore, the volatile nature of oil and gas prices historically influences investment decisions. Periods of low crude oil prices can lead to significant cuts in capital expenditure, including allocations for digital transformation and system integration projects. While the long-term trend favors digital adoption, short-term market fluctuations introduce uncertainty and can cause project delays or cancellations, thereby acting as a significant restraint on market growth. Cybersecurity concerns, while also a driver for specific solutions, can also be a restraint due to the fear of sophisticated attacks on integrated critical infrastructure.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment & Integration Costs | -0.8% | Global, particularly in regions with legacy infrastructure | Short to Medium-Term (2025-2030) |

| Lack of Skilled Workforce & Expertise | -0.7% | Global, especially emerging markets | Medium to Long-Term (2026-2033) |

| Data Interoperability Challenges with Legacy Systems | -0.6% | North America, Europe, Asia Pacific | Short to Medium-Term (2025-2029) |

| Volatility in Oil & Gas Commodity Prices | -0.5% | Global, all oil-producing nations | Short to Medium-Term (2025-2028) |

| Perceived Risks of Cyberattacks on OT Systems | -0.4% | Global, highly regulated environments | Short to Long-Term (2025-2033) |

System Integrator in Oil and Gas Market Opportunities Analysis

The System Integrator in Oil and Gas market is ripe with opportunities driven by the industry's continuous evolution and the adoption of next-generation technologies. One significant avenue for growth lies in the expansion of advanced analytics and big data solutions. As oil and gas operations generate massive volumes of data, there is an increasing demand for integrators who can design and implement platforms that extract actionable insights from this data, optimizing everything from reservoir modeling to predictive maintenance and supply chain logistics. This capability allows companies to make more informed decisions, leading to substantial operational improvements and competitive advantages.

Another burgeoning opportunity arises from the accelerating energy transition and the growing focus on sustainability. Oil and gas companies are diversifying into renewable energy, carbon capture, utilization, and storage (CCUS), and hydrogen production. System integrators are uniquely positioned to facilitate the integration of these new energy systems with existing infrastructure, offering expertise in managing complex hybrid energy portfolios, optimizing energy consumption, and implementing environmental monitoring and reporting solutions. This shift broadens the scope of services for integrators beyond traditional oil and gas applications.

Furthermore, the increasing adoption of cloud and edge computing paradigms presents substantial opportunities for system integrators. Migrating critical applications and data to the cloud offers enhanced scalability, flexibility, and cost-effectiveness, while edge computing provides real-time data processing closer to the source, crucial for remote and time-sensitive operations. Integrators who can effectively design and implement hybrid cloud architectures, ensuring data security and regulatory compliance, will find significant demand. The ongoing modernization of aging infrastructure globally also creates a steady stream of projects for system integrators to upgrade and integrate new technologies.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration of Renewable Energy & Decarbonization Technologies | +1.3% | Europe, North America, Asia Pacific | Medium to Long-Term (2027-2033) |

| Expansion of Cloud-Based & Hybrid IT/OT Solutions | +1.1% | Global, particularly advanced economies | Short to Medium-Term (2025-2030) |

| Development of Digital Twins and Simulation Platforms | +0.9% | North America, Europe, Middle East | Medium to Long-Term (2028-2033) |

| Leveraging Advanced Data Analytics & AI for Enhanced Decision Making | +0.8% | Global, all major operators | Short to Medium-Term (2025-2029) |

| Growth in Greenfield Projects & Capacity Expansions | +0.6% | Africa, South America, Asia Pacific, Middle East | Medium to Long-Term (2027-2033) |

System Integrator in Oil and Gas Market Challenges Impact Analysis

The System Integrator in Oil and Gas market faces a unique set of challenges that require sophisticated solutions and strategic foresight. A primary challenge is managing the vast complexity of integrating diverse operational technologies (OT) with information technologies (IT) across heterogeneous environments. Oil and gas companies often operate with a patchwork of legacy systems, proprietary software, and varying hardware platforms, each with different protocols and data formats. This heterogeneity creates significant interoperability issues, demanding advanced expertise from integrators to ensure seamless communication and data exchange without compromising existing operations or data integrity.

Another significant hurdle revolves around data security and compliance. As more operational data moves to cloud environments and remote monitoring becomes prevalent, the exposure to cyber threats dramatically increases. Protecting critical infrastructure from sophisticated cyberattacks, ensuring data privacy, and adhering to stringent industry regulations (e.g., NIST, IEC 62443, GDPR for data protection) are paramount. System integrators are challenged to implement robust, multi-layered cybersecurity frameworks that are not only effective but also adaptable to evolving threat landscapes, often requiring continuous updates and vigilant monitoring, which adds to project complexity and cost.

Moreover, the highly specialized and capital-intensive nature of oil and gas projects presents unique project management and execution challenges. The long project cycles, remote and harsh operating environments, and the need for zero-downtime solutions require integrators to possess not only technical prowess but also exceptional risk management and logistical capabilities. Furthermore, the rapid pace of technological innovation means integrators must constantly update their skills and offerings to remain competitive, navigating a landscape where new tools and platforms emerge regularly, demanding continuous investment in training and R&D.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integrating Disparate Legacy Systems & Technologies | -0.9% | Global, particularly established regions | Short to Medium-Term (2025-2030) |

| Ensuring Robust Cybersecurity in Converged IT/OT Networks | -0.8% | Global, critical infrastructure zones | Short to Long-Term (2025-2033) |

| Talent Gap and Skill Shortages in Niche Technologies | -0.7% | Global, especially in developing markets | Medium to Long-Term (2026-2033) |

| Regulatory Compliance and Evolving Standards | -0.6% | Europe, North America, regions with strict environmental policies | Short to Medium-Term (2025-2029) |

| Managing Remote and Harsh Operating Environments | -0.5% | Arctic, Offshore, Desert regions | Medium to Long-Term (2027-2033) |

System Integrator in Oil and Gas Market - Updated Report Scope

This comprehensive market research report provides a detailed analysis of the System Integrator in Oil and Gas market, offering insights into market size, growth trends, segmentation, and competitive landscape. The scope includes an in-depth examination of market drivers, restraints, opportunities, and challenges, alongside an impact assessment of AI on the sector. The report aims to equip stakeholders with critical information for strategic decision-making and investment planning within this evolving industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 17.5 Billion |

| Market Forecast in 2033 | USD 29.8 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Technology Integrator A, Industrial Automation Specialist B, Energy Solutions Provider C, IT Services Company D, OT Cybersecurity Firm E, Enterprise Software Vendor F, Cloud Integration Expert G, Digital Transformation Consultant H, Data Analytics Innovator I, Process Automation Leader J, Infrastructure Modernization Partner K, Asset Management Solutions L, Field Services Integrator M, Smart Grid Developer N, AI & ML Solutions O, Robotics Integrator P, Control Systems Integrator Q, System Optimization Specialist R, Petrochemical Automation S, Supply Chain Integrator T |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The System Integrator in Oil and Gas market is meticulously segmented to provide a granular view of its diverse components and growth opportunities. This segmentation considers various dimensions, including the types of services offered, specific industry applications, underlying technologies deployed, and the scale of integration projects. Understanding these segments is crucial for stakeholders to identify niche markets, tailor solutions, and develop targeted strategies for growth and competitive advantage in a complex and evolving industry landscape.

- By Service Type: This segment includes Consulting & Advisory services, focusing on strategic planning and digital roadmaps; Implementation & Integration, covering the core execution of solutions; Maintenance & Support, ensuring ongoing system performance; Managed Services, offering outsourced operational management; and Digital Transformation Services, encompassing comprehensive modernization initiatives.

- By Application: The market is divided into Upstream (exploration, production, drilling), Midstream (pipelines, storage, logistics), and Downstream (refining, petrochemicals, distribution). Each sub-segment has unique integration needs, from field automation in upstream to supply chain optimization in downstream.

- By Technology: This vital segment categorizes integrators based on the advanced technologies they implement, such as Industrial Automation & Control Systems (SCADA, DCS, PLC, MES), Enterprise Resource Planning (ERP), Asset Performance Management (APM), robust Cybersecurity Solutions, Cloud Computing, Internet of Things (IoT) & Edge Computing, Artificial Intelligence (AI) & Machine Learning (ML), Data Analytics & Visualization tools, and Robotics & Autonomous Systems for enhanced efficiency and safety.

- By Project Size: Projects are classified as Small, Medium, or Large, reflecting the scale and complexity of integration efforts, which impacts resource allocation, timelines, and pricing models for system integrators.

Regional Highlights

- North America: This region is a dominant force in the System Integrator in Oil and Gas market, driven by significant investments in digital transformation, particularly in the US and Canada. The presence of major oil and gas companies, coupled with a robust technological infrastructure and early adoption of advanced analytics, IoT, and AI, positions North America as a key innovation hub. The focus on shale gas production and offshore drilling operations further fuels demand for sophisticated integration solutions to enhance efficiency and reduce operational costs.

- Europe: Europe is characterized by stringent environmental regulations and a strong emphasis on sustainability, which mandates the integration of advanced energy management systems and carbon reduction technologies. Countries like Norway, the UK, and Germany are leaders in adopting digital solutions for oil and gas, focusing on optimizing asset performance, enhancing cybersecurity, and facilitating the transition to cleaner energy sources. The region also sees significant investment in modernizing aging infrastructure and leveraging cloud technologies for operational agility.

- Asia Pacific (APAC): The APAC region is experiencing rapid growth in the System Integrator in Oil and Gas market, primarily due to increasing energy demand, expanding exploration and production activities in countries like China, India, and Indonesia, and a push for industrial modernization. While still facing challenges in legacy system integration, the region presents immense opportunities for new project developments and the adoption of cost-effective digital solutions to improve operational efficiency and competitiveness.

- Latin America: Latin America is a burgeoning market for system integrators, driven by the expansion of oil and gas production, particularly in Brazil and Mexico, and a growing need for modernizing existing infrastructure. Investments in offshore projects and a push for greater energy independence are fostering the adoption of integrated solutions for process automation, data management, and operational security, though economic volatility can sometimes impact project timelines.

- Middle East and Africa (MEA): The MEA region is a critical market, with significant oil and gas reserves and a strong strategic imperative to optimize production, enhance national energy security, and diversify economies. Countries like Saudi Arabia, UAE, and Qatar are making substantial investments in digital oilfields, smart drilling, and advanced analytics, creating a high demand for system integrators who can deliver cutting-edge IT/OT convergence solutions, often with a focus on large-scale, complex projects.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the System Integrator in Oil and Gas Market.- Company A

- Company B

- Company C

- Company D

- Company E

- Company F

- Company G

- Company H

- Company I

- Company J

- Company K

- Company L

- Company M

- Company N

- Company O

- Company P

- Company Q

- Company R

- Company S

- Company T

Frequently Asked Questions

What is the projected growth rate of the System Integrator in Oil and Gas Market?

The System Integrator in Oil and Gas Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, reaching an estimated USD 29.8 Billion by 2033.

How is AI impacting system integration in the oil and gas sector?

AI is significantly impacting the sector by enabling predictive maintenance, optimizing operational processes, enhancing safety protocols through intelligent monitoring, and improving data analytics for informed decision-making across the value chain.

What are the primary drivers for the System Integrator in Oil and Gas Market?

Key drivers include the global push for digital transformation, the imperative for operational efficiency and cost reduction, the increasing adoption of Industrial IoT and AI/ML technologies, and the need for modernization of aging infrastructure.

What are the main challenges faced by system integrators in the oil and gas industry?

Significant challenges include integrating disparate legacy systems, ensuring robust cybersecurity in converged IT/OT networks, addressing talent gaps in specialized technologies, and navigating complex regulatory compliance requirements.

Which regions are leading in the adoption of system integration solutions in oil and gas?

North America and Europe are leading regions due to strong technological infrastructure and early adoption, while the Middle East and Asia Pacific are experiencing rapid growth driven by significant investments in new projects and digital transformation initiatives.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted