Internal Audit Management Software Market

Internal Audit Management Software Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707483 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

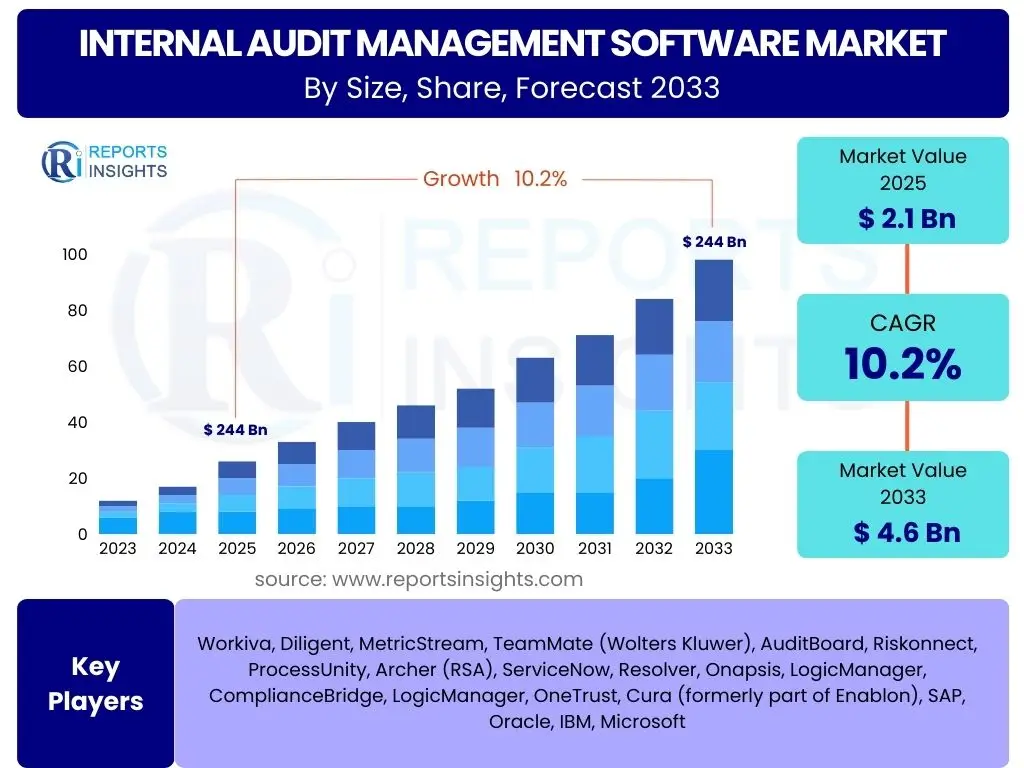

Internal Audit Management Software Market Size

According to Reports Insights Consulting Pvt Ltd, The Internal Audit Management Software Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.2% between 2025 and 2033. The market is estimated at USD 2.1 Billion in 2025 and is projected to reach USD 4.6 Billion by the end of the forecast period in 2033.

Key Internal Audit Management Software Market Trends & Insights

The Internal Audit Management Software market is witnessing significant transformation, largely driven by the increasing complexity of business environments, evolving regulatory landscapes, and the rapid adoption of digital technologies. Organizations are increasingly seeking solutions that offer not only compliance management but also strategic insights into risk and performance. This shift necessitates integrated platforms capable of handling diverse data sources, providing real-time analytics, and supporting continuous auditing methodologies. The focus is moving towards proactive risk mitigation and value creation, rather than merely reactive compliance.

Furthermore, the demand for cloud-based internal audit solutions is escalating, offering enhanced accessibility, scalability, and cost-effectiveness. Automation, particularly through Robotic Process Automation (RPA), is becoming integral to streamline repetitive audit tasks, thereby freeing up auditors to focus on more complex, judgment-intensive areas. There is also a growing emphasis on connecting internal audit findings with broader enterprise risk management (ERM) and governance, risk, and compliance (GRC) frameworks, fostering a more holistic approach to organizational oversight and resilience.

- Shift to cloud-based and Software-as-a-Service (SaaS) deployment models.

- Integration of advanced data analytics and visualization tools for deeper insights.

- Increased adoption of Robotic Process Automation (RPA) for routine audit tasks.

- Convergence of Internal Audit, Risk Management, and Compliance (GRC).

- Emphasis on continuous auditing and monitoring for real-time risk assessment.

- Development of predictive analytics capabilities for proactive risk identification.

- Enhanced focus on cybersecurity audit and data privacy compliance functionalities.

AI Impact Analysis on Internal Audit Management Software

Artificial Intelligence (AI) is poised to fundamentally reshape the internal audit function, addressing common user concerns regarding efficiency, accuracy, and the ability to process vast amounts of data. Users anticipate AI will automate mundane tasks, allowing auditors to focus on critical thinking, strategic analysis, and consultative roles. The primary expectations revolve around AI's capacity to identify anomalies, predict risks, and unearth insights that human auditors might miss, thereby enhancing the overall effectiveness and scope of audits. There are also queries about how AI will improve audit planning, evidence collection, and reporting.

However, alongside these positive expectations, users also express concerns about data integrity, algorithmic bias, the 'black box' nature of some AI models, and the potential impact on audit jobs. The market is therefore focused on developing transparent and explainable AI solutions that can augment, rather than replace, human judgment. The goal is to leverage AI for pattern recognition, trend analysis, and predictive modeling, transforming internal audit from a reactive compliance function into a proactive, value-adding strategic partner for organizations.

- Enhanced data analysis and anomaly detection in large datasets.

- Automated identification of patterns and trends indicative of risk or fraud.

- Predictive risk assessment and early warning systems for emerging threats.

- Streamlined collection and processing of audit evidence.

- Development of intelligent dashboards and reporting for actionable insights.

- Augmentation of audit judgment rather than full replacement of human auditors.

- Personalized audit planning and scope definition based on real-time data.

Key Takeaways Internal Audit Management Software Market Size & Forecast

The Internal Audit Management Software market is poised for robust expansion, driven primarily by an escalating global focus on corporate governance, stringent regulatory requirements, and the imperative for organizations to manage an increasingly complex risk landscape effectively. The projected growth underscores a fundamental shift in how businesses perceive internal audit, moving beyond a mere compliance necessity to a strategic function that delivers tangible value through enhanced oversight and risk mitigation. This growth trajectory is significantly supported by technological advancements, particularly in cloud computing and artificial intelligence, which are transforming the capabilities and efficiency of audit processes.

Organizations are recognizing the critical need for sophisticated software solutions that can automate routine tasks, provide deeper insights through advanced analytics, and facilitate continuous monitoring. The forecast indicates that investment in these tools will accelerate as companies strive for greater transparency, operational resilience, and the ability to adapt swiftly to market changes and emerging threats. The market's future will be characterized by solutions that offer greater integration, scalability, and intelligence, enabling auditors to provide more timely, relevant, and strategic advice to management and boards.

- Strong market growth fueled by increasing regulatory demands and risk complexity.

- Significant adoption of cloud-based solutions for scalability and accessibility.

- AI and advanced analytics are becoming central to effective internal auditing.

- Emphasis on continuous monitoring and real-time insights for proactive risk management.

- Convergence with GRC platforms to provide a holistic view of organizational health.

- Growing investment in solutions that enhance audit efficiency and strategic value.

Internal Audit Management Software Market Drivers Analysis

The Internal Audit Management Software market is significantly driven by a confluence of factors that compel organizations to adopt more sophisticated and automated audit solutions. The escalating complexity of global regulations, such as GDPR, SOX, and various industry-specific compliance mandates, necessitates robust systems that can ensure adherence and mitigate legal and financial penalties. Simultaneously, the growing awareness of enterprise-wide risks, including cyber threats, supply chain disruptions, and financial misconduct, is pushing companies to invest in tools that offer comprehensive risk identification, assessment, and monitoring capabilities. These drivers collectively create an environment where traditional, manual audit processes are no longer sufficient, leading to increased demand for specialized software.

Moreover, the ongoing digital transformation across industries, marked by the widespread adoption of cloud computing, big data analytics, and mobile technologies, profoundly impacts audit functions. This digital shift generates massive volumes of data, which manual methods cannot efficiently process or analyze for audit insights, thus creating a strong demand for software solutions equipped with advanced analytical capabilities. The continuous pressure on organizations to enhance operational efficiency and reduce costs also serves as a crucial driver; internal audit software automates repetitive tasks, streamlines workflows, and allows auditors to focus on high-value activities, leading to improved productivity and resource optimization.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Regulatory Compliance Burden | +2.5% | Global, particularly North America, Europe, and Asia-Pacific | Short to Mid-term (2025-2029) |

| Growing Demand for Enhanced Risk Management | +2.0% | Global, across all industries | Mid to Long-term (2027-2033) |

| Digital Transformation and Cloud Adoption | +1.8% | North America, Europe, Emerging APAC Markets | Short to Mid-term (2025-2030) |

| Need for Operational Efficiency and Cost Reduction | +1.5% | Global, particularly for large enterprises and SMEs | Short to Mid-term (2025-2029) |

| Rise in Corporate Governance Standards | +1.2% | Global, with strong emphasis in developed economies | Mid to Long-term (2027-2033) |

Internal Audit Management Software Market Restraints Analysis

Despite the strong growth drivers, the Internal Audit Management Software market faces several significant restraints that can impede its full potential. One primary concern is the high initial implementation cost associated with sophisticated audit management systems, which can be prohibitive for small and medium-sized enterprises (SMEs) or organizations with limited IT budgets. This cost includes not only the software license but also expenses related to customization, integration with existing legacy systems, and professional services for deployment and training, creating a substantial upfront investment barrier for many potential adopters.

Another critical restraint involves data privacy and security concerns, especially with the increasing adoption of cloud-based solutions. Organizations handling sensitive financial and operational data are highly cautious about storing this information on third-party servers, fearing data breaches or non-compliance with data protection regulations. This apprehension can slow down cloud adoption. Furthermore, the resistance to change within traditional organizations, often characterized by a preference for established manual processes or an aversion to new technologies, poses a significant challenge. Overcoming this cultural inertia and ensuring user adoption requires extensive change management efforts, which can prolong implementation timelines and increase costs.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Implementation Costs | -1.8% | Global, particularly affecting SMEs and budget-constrained organizations | Short to Mid-term (2025-2029) |

| Data Privacy and Security Concerns | -1.5% | Global, especially in highly regulated sectors like BFSI and Healthcare | Short to Mid-term (2025-2030) |

| Lack of Skilled Personnel for Advanced Solutions | -1.2% | Global, more pronounced in developing regions | Mid to Long-term (2027-2033) |

| Resistance to Change within Traditional Organizations | -1.0% | Global, particularly in established industries | Short to Mid-term (2025-2028) |

| Integration Complexities with Legacy Systems | -0.8% | Global, prevalent in large, mature enterprises | Mid-term (2026-2031) |

Internal Audit Management Software Market Opportunities Analysis

The Internal Audit Management Software market is ripe with opportunities, primarily driven by the ongoing evolution of technology and the expanding scope of internal audit functions. The emergence of Artificial Intelligence (AI) and Machine Learning (ML) presents a significant avenue for growth, enabling predictive auditing, automated anomaly detection, and continuous monitoring at a scale previously unimaginable. This technological integration allows audit teams to move beyond traditional sampling methods to analyze entire datasets, thus providing more comprehensive and accurate insights. Vendors who successfully embed these advanced analytics capabilities into their platforms will gain a competitive edge by offering solutions that enhance efficiency and proactive risk identification.

Furthermore, the untapped potential within Small and Medium-sized Enterprises (SMEs) represents a substantial growth opportunity. As SMEs increasingly face similar regulatory pressures and risks as larger corporations, but often lack the resources for extensive manual audit processes, there is a growing demand for scalable, cost-effective, and user-friendly internal audit software. Cloud-based SaaS models, offering lower upfront costs and easier deployment, are particularly attractive to this segment. Additionally, the increasing convergence of internal audit with broader Governance, Risk, and Compliance (GRC) platforms creates opportunities for integrated solutions that provide a holistic view of organizational health, streamlining processes and reducing duplication across various oversight functions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of AI and ML for Predictive Auditing | +2.8% | Global, highly impactful in technologically advanced regions | Mid to Long-term (2027-2033) |

| Expansion into SMEs with Scalable Cloud Solutions | +2.2% | Global, particularly in emerging and established markets | Short to Mid-term (2025-2030) |

| Demand for Continuous Auditing and Real-time Insights | +1.9% | Global, especially among large and complex organizations | Mid-term (2026-2031) |

| Integration with GRC Platforms for Holistic Oversight | +1.7% | Global, across all industry verticals | Short to Mid-term (2025-2029) |

| Growth in Emerging Economies with Digitalization Initiatives | +1.5% | Asia Pacific, Latin America, Middle East & Africa | Long-term (2028-2033) |

Internal Audit Management Software Market Challenges Impact Analysis

The Internal Audit Management Software market faces a complex array of challenges that can hinder its growth and the successful adoption of advanced solutions. One significant hurdle is ensuring data integrity and security within cloud environments, particularly as more organizations migrate sensitive audit data to off-premise infrastructure. This necessitates robust cybersecurity measures and strict adherence to global data protection regulations, which can be a significant technical and compliance burden for both vendors and users. Maintaining trust and demonstrating impenetrable security is paramount for market acceptance.

Another persistent challenge is the talent gap within internal audit teams. As software capabilities advance, particularly with the integration of AI and sophisticated data analytics, there is a growing need for auditors with hybrid skill sets combining traditional auditing expertise with data science, IT acumen, and cybersecurity knowledge. The shortage of such skilled professionals can limit the effective utilization of advanced software features and slow down implementation. Furthermore, the dynamic nature of regulatory landscapes globally poses a continuous challenge; software providers must constantly update their solutions to ensure compliance with evolving standards, requiring significant ongoing R&D investment and agility to respond to rapid changes, thus impacting product development cycles and maintenance costs.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ensuring Data Integrity and Security in Cloud Environments | -1.7% | Global, high relevance in highly regulated industries | Short to Mid-term (2025-2030) |

| Keeping Pace with Evolving Regulatory Landscapes | -1.4% | Global, particularly in jurisdictions with frequent regulatory updates | Continuous, Short to Long-term |

| Talent Gap in Data Analytics and AI for Internal Audit | -1.1% | Global, more pronounced in regions with developing tech education | Mid to Long-term (2027-2033) |

| Cost-effectiveness for Smaller Enterprises | -0.9% | Global, specific to SMEs and non-profit organizations | Short to Mid-term (2025-2029) |

| Standardization and Interoperability Issues | -0.7% | Global, affecting integration with diverse IT ecosystems | Mid-term (2026-2031) |

Internal Audit Management Software Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Internal Audit Management Software market, offering a detailed segmentation by component, deployment, organization size, and industry vertical. It covers historical data from 2019 to 2023, establishes 2024 as the base year, and presents a forward-looking forecast up to 2033. The report meticulously examines market trends, drivers, restraints, opportunities, and challenges, along with a thorough regional analysis and competitive landscape assessment to provide a holistic understanding of the market dynamics.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.1 Billion |

| Market Forecast in 2033 | USD 4.6 Billion |

| Growth Rate | 10.2% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Workiva, Diligent, MetricStream, TeamMate (Wolters Kluwer), AuditBoard, Riskonnect, ProcessUnity, Archer (RSA), ServiceNow, Resolver, Onapsis, LogicManager, ComplianceBridge, LogicManager, OneTrust, Cura (formerly part of Enablon), SAP, Oracle, IBM, Microsoft |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Internal Audit Management Software market is meticulously segmented to provide a granular view of its various facets, enabling a deeper understanding of market dynamics and growth opportunities across different dimensions. This segmentation is crucial for stakeholders to identify specific market niches, tailor their strategies, and allocate resources effectively. The analysis covers the market from several perspectives, including the type of components offered, deployment models, target organization sizes, and the diverse industry verticals that utilize these solutions, reflecting the varied needs and preferences of end-users.

Each segment presents unique growth patterns and demands. For instance, the transition from on-premise to cloud-based deployment signifies a major trend driven by scalability and cost-efficiency benefits, while the increasing complexity across industries fuels demand for specialized software features. Understanding these distinct segments helps in comprehending how different parts of the market contribute to the overall growth and where future innovations are likely to emerge, supporting strategic planning and competitive positioning for market participants.

- By Component: This segment is bifurcated into Software and Services.

- Software: Further categorized into On-premise and Cloud-based solutions, reflecting the delivery models chosen by organizations.

- Services: Encompasses Consulting, Implementation, and Support services, which are critical for successful software adoption and ongoing operation.

- By Deployment: Divided into On-premise and Cloud (SaaS) deployments, highlighting the shift towards flexible and accessible cloud solutions.

- By Organization Size: Segregated into Large Enterprises and Small and Medium-sized Enterprises (SMEs), acknowledging the different scale and complexity of audit needs.

- By Industry Vertical: Includes BFSI (Banking, Financial Services, and Insurance), Healthcare, IT & Telecom, Manufacturing, Retail & Consumer Goods, Government, and Others, each with unique regulatory and operational requirements influencing software adoption.

Regional Highlights

- North America: This region is a dominant force in the Internal Audit Management Software market, primarily due to the presence of a large number of established enterprises, stringent regulatory frameworks like Sarbanes-Oxley (SOX), and high adoption rates of advanced technologies such as cloud computing and AI. The United States and Canada are key contributors, with robust investments in digital transformation and a strong emphasis on corporate governance and risk management. The region also benefits from a well-developed IT infrastructure and a culture of early technology adoption.

- Europe: Europe represents a significant market share, driven by a complex web of regional regulations (e.g., GDPR, MiFID II) and a growing focus on data privacy and cybersecurity. Countries like Germany, the United Kingdom, and France are leading the adoption of internal audit software, propelled by the need for enhanced transparency, compliance, and efficiency across diverse industries. The region is actively integrating AI and advanced analytics into audit practices, albeit with strong considerations for data protection.

- Asia Pacific (APAC): The APAC region is projected to exhibit the highest growth rate, fueled by rapid digitalization, increasing foreign investments, and evolving regulatory landscapes in emerging economies such as China, India, and Japan. The burgeoning number of SMEs, coupled with a rising awareness of corporate governance and risk management, contributes significantly to market expansion. Governments and businesses in this region are increasingly investing in sophisticated software to manage growing compliance demands and enhance operational resilience.

- Latin America: This region is experiencing steady growth in the internal audit management software market, driven by increasing foreign direct investment, expanding digital infrastructure, and a push for greater financial transparency and regulatory compliance across various sectors. Countries like Brazil, Mexico, and Argentina are gradually adopting these solutions as local enterprises seek to modernize their internal controls and risk management frameworks to align with international standards.

- Middle East and Africa (MEA): The MEA region is witnessing a gradual but consistent adoption of internal audit management software, primarily influenced by ongoing economic diversification efforts, large-scale infrastructure projects, and a growing emphasis on governance and compliance within the oil & gas, financial, and government sectors. Nations like UAE, Saudi Arabia, and South Africa are leading the charge, driven by the need to combat fraud, enhance operational efficiency, and meet international regulatory requirements.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Internal Audit Management Software Market.- Workiva

- Diligent

- MetricStream

- TeamMate (Wolters Kluwer)

- AuditBoard

- Riskonnect

- ProcessUnity

- Archer (RSA)

- ServiceNow

- Resolver

- Onapsis

- LogicManager

- ComplianceBridge

- OneTrust

- Cura (formerly part of Enablon)

- SAP

- Oracle

- IBM

- Microsoft

- GRC-Maestro

Frequently Asked Questions

What is Internal Audit Management Software?

Internal Audit Management Software is a specialized digital tool designed to streamline, automate, and centralize internal audit processes. It assists organizations in managing audit planning, risk assessment, fieldwork, issue tracking, reporting, and follow-up activities, enhancing efficiency, consistency, and compliance across the audit function.

Why is Internal Audit Management Software important for businesses?

It is crucial for businesses as it improves audit efficiency, enhances the accuracy of risk assessments, ensures regulatory compliance, provides real-time insights into organizational health, and transforms the internal audit function from reactive to proactive, ultimately aiding in better decision-making and safeguarding assets.

How does AI impact Internal Audit Management Software?

AI significantly impacts Internal Audit Management Software by enabling advanced data analytics, automated anomaly detection, predictive risk assessment, and continuous monitoring. It automates routine tasks, allows auditors to process vast datasets more effectively, and generates deeper, more timely insights, thereby augmenting the capabilities of human auditors.

What are the key benefits of adopting cloud-based Internal Audit Software?

Key benefits include enhanced accessibility from anywhere, scalability to adapt to organizational growth, reduced infrastructure costs (no need for on-premise servers), automatic updates and maintenance, and improved collaboration among audit teams, leading to greater flexibility and efficiency.

What factors should an organization consider when choosing Internal Audit Management Software?

Organizations should consider factors such as scalability, integration capabilities with existing systems, ease of use, security features, reporting and analytics functionalities, vendor reputation, compliance with industry-specific regulations, and the total cost of ownership, including implementation and support services.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted