Synchrophasor Market

Synchrophasor Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707693 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

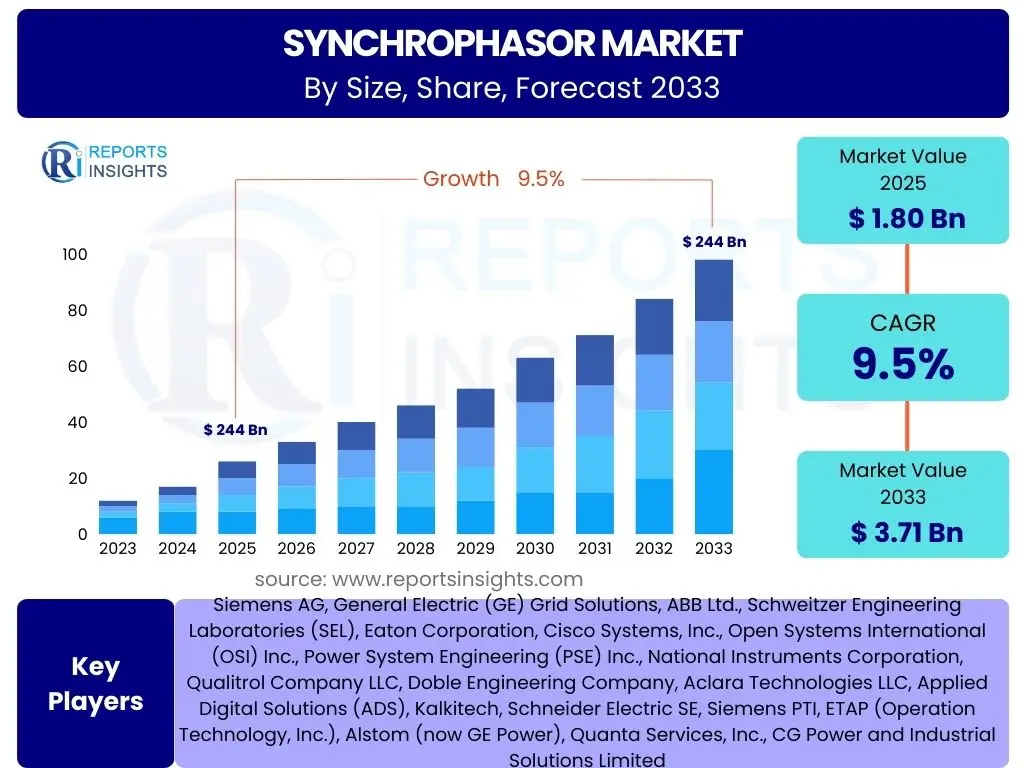

Synchrophasor Market Size

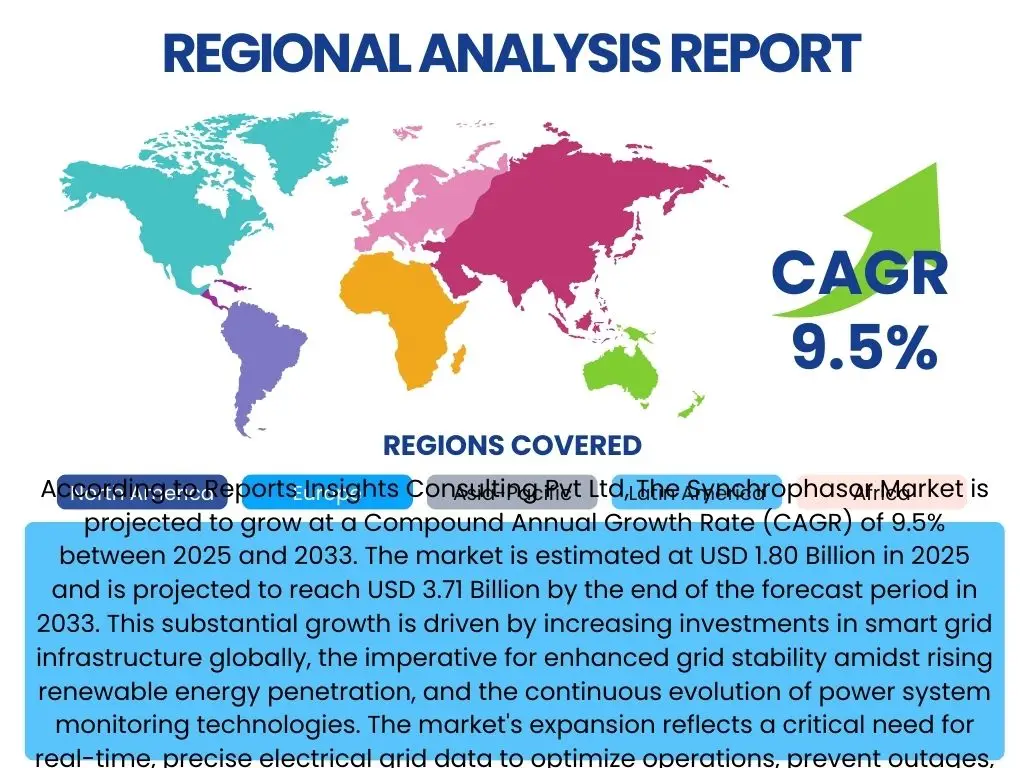

According to Reports Insights Consulting Pvt Ltd, The Synchrophasor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. The market is estimated at USD 1.80 Billion in 2025 and is projected to reach USD 3.71 Billion by the end of the forecast period in 2033. This substantial growth is driven by increasing investments in smart grid infrastructure globally, the imperative for enhanced grid stability amidst rising renewable energy penetration, and the continuous evolution of power system monitoring technologies. The market's expansion reflects a critical need for real-time, precise electrical grid data to optimize operations, prevent outages, and ensure a resilient energy supply.

The upward trajectory of the Synchrophasor Market is underpinned by the escalating complexity of modern power systems, which necessitate advanced monitoring solutions like Phasor Measurement Units (PMUs) and Phasor Data Concentrators (PDCs). Utilities and grid operators are increasingly recognizing the value of synchronized data for wide-area monitoring, fault detection, and proactive grid management. The projected growth rates indicate a strong market confidence in synchrophasor technology's ability to address the challenges posed by distributed energy resources, aging infrastructure, and the growing demand for reliable electricity.

Key Synchrophasor Market Trends & Insights

The Synchrophasor market is witnessing significant transformation driven by advancements in digital technology and the evolving energy landscape. Common user questions often revolve around how synchrophasors integrate with renewable energy sources, their role in enhancing grid resilience, and the impact of real-time data analytics. Insights indicate a strong trend towards the adoption of advanced analytics and artificial intelligence to process vast amounts of synchrophasor data, moving beyond basic monitoring to predictive and prescriptive grid management. Furthermore, there is a clear emphasis on enhancing cybersecurity measures for PMU data streams, recognizing the critical infrastructure role these systems play. The decentralization of energy generation also pushes the need for synchrophasors in microgrids and distributed energy resource management, fostering new applications and deployment models.

- Increased integration of Synchrophasors with Distributed Energy Resources (DERs) and Microgrids for enhanced local grid stability and control.

- Rising adoption of Artificial Intelligence (AI) and Machine Learning (ML) for advanced analytics of PMU data, enabling predictive maintenance, anomaly detection, and optimal grid operation.

- Growing focus on cybersecurity for Synchrophasor data communication and infrastructure to protect critical grid information from cyber threats.

- Development of cloud-based Synchrophasor data platforms for scalable data storage, processing, and accessibility, facilitating collaboration and remote monitoring.

- Standardization efforts for data formats and communication protocols (e.g., IEEE C37.118) to ensure interoperability among different vendors' devices and systems.

- Expansion of wide-area monitoring and control (WAMC) systems leveraging synchrophasor technology to prevent widespread blackouts and improve grid responsiveness.

AI Impact Analysis on Synchrophasor

User inquiries frequently address the transformative potential of Artificial Intelligence (AI) within the Synchrophasor domain, seeking to understand how AI can enhance the processing, analysis, and application of synchrophasor data. Common themes include AI's capacity for real-time anomaly detection, predictive analytics for grid stability, and intelligent decision-making in complex grid scenarios. There's a particular interest in how AI algorithms can filter noise, identify subtle patterns indicative of impending issues, and optimize grid operations more effectively than traditional methods. Concerns also emerge regarding the computational demands of AI, the need for robust data quality, and the ethical implications of autonomous grid management driven by AI, alongside the imperative for highly skilled professionals to manage these advanced systems.

The integration of AI into synchrophasor systems is expected to revolutionize grid management by moving beyond reactive responses to proactive and predictive operations. AI algorithms can analyze vast streams of synchronized data from PMUs to identify subtle deviations, predict potential system instabilities, and recommend corrective actions with unprecedented speed and accuracy. This capability is crucial for managing grids with high penetration of intermittent renewable energy sources, where rapid fluctuations can pose significant challenges. AI-powered synchrophasor applications will also significantly improve fault location, provide advanced situational awareness, and support dynamic line rating, thereby enhancing overall grid reliability and efficiency.

- AI enhances real-time anomaly detection in grid operations, identifying subtle deviations invisible to traditional systems.

- Machine Learning algorithms predict grid instability and potential outages, enabling proactive rather than reactive responses.

- AI optimizes power flow and resource allocation by analyzing synchrophasor data for dynamic grid management.

- Deep learning models improve fault location accuracy and speed, reducing outage durations and operational costs.

- AI facilitates advanced cybersecurity by detecting unusual patterns in data streams that could indicate cyber threats to PMU infrastructure.

- Automated decision support systems, powered by AI and synchrophasor data, assist operators in managing complex grid scenarios.

Key Takeaways Synchrophasor Market Size & Forecast

Common user questions regarding the Synchrophasor market size and forecast often focus on the primary drivers of growth, the segments expected to experience the most significant expansion, and the long-term viability of these technologies in the evolving energy landscape. Insights from market projections indicate that the market's robust growth is primarily fueled by global smart grid initiatives and the increasing demand for grid resilience in the face of climate change and distributed energy integration. The forecast highlights a sustained need for real-time, precise grid data, positioning synchrophasor technology as indispensable for modernizing power systems. Furthermore, the market's trajectory suggests a critical shift towards data-driven grid management, where advanced analytics and AI play an increasingly pivotal role in leveraging synchrophasor outputs for operational excellence and strategic planning.

The forecasted market growth underscores the foundational role of synchrophasors in transitioning to a smarter, more resilient, and sustainable power grid. Utilities worldwide are expected to continue their investments in PMU deployment and associated data infrastructure, driven by regulatory mandates and the economic benefits of improved grid efficiency and reduced downtime. This growth is not merely about installing more hardware but also about developing sophisticated software and services that extract actionable intelligence from synchrophasor data. The long-term outlook remains highly positive, with significant opportunities emerging in areas such as predictive analytics, cybersecurity integration, and the application of synchrophasor technology in emerging markets that are building new grid infrastructures or upgrading existing ones.

- The Synchrophasor market is poised for significant growth, driven by global smart grid investments and the imperative for grid modernization.

- Real-time data capabilities of synchrophasors are crucial for managing the increasing complexity of power systems, especially with renewable energy integration.

- The market forecast indicates strong demand for advanced analytics and AI solutions to derive actionable insights from PMU data.

- Investments in cybersecurity for synchrophasor systems will be paramount to ensure the integrity and reliability of grid operations.

- Emerging markets and regions undergoing rapid grid infrastructure development present substantial growth opportunities.

- Utilities are recognizing synchrophasors as a key enabler for enhanced grid reliability, efficiency, and proactive fault management.

Synchrophasor Market Drivers Analysis

The Synchrophasor Market is propelled by several robust drivers that underscore the critical need for advanced grid monitoring and control. The global push for smart grid initiatives stands as a primary catalyst, as utilities invest heavily in digitalizing their infrastructure to enhance reliability, efficiency, and sustainability. This includes deploying technologies capable of providing real-time, synchronized data across wide areas, which is precisely what synchrophasors offer. Another significant driver is the escalating integration of renewable energy sources, such as solar and wind power, into the grid. The intermittent nature of these sources necessitates sophisticated monitoring to maintain grid stability and balance, making synchrophasors indispensable for managing power fluctuations and ensuring smooth operations.

Furthermore, the increasing frequency and intensity of power outages due to aging infrastructure, extreme weather events, and cyber threats highlight the urgent need for enhanced grid resilience. Synchrophasors provide critical data for rapid fault detection, isolation, and restoration, significantly reducing downtime and economic losses. Regulatory mandates and government incentives also play a pivotal role, pushing utilities to adopt advanced monitoring technologies to meet performance standards and reduce carbon emissions. Lastly, the advent of advanced data analytics and Artificial Intelligence (AI) tools has amplified the value proposition of synchrophasor data, enabling utilities to move from reactive to predictive and prescriptive grid management, further driving demand for these precise measurement devices.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Smart Grid Initiatives & Modernization | +2.1% | North America, Europe, Asia Pacific (China, India) | Medium to Long-term (2025-2033) |

| Increasing Renewable Energy Integration | +1.8% | Europe, Asia Pacific, North America | Medium to Long-term (2025-2033) |

| Rising Demand for Grid Stability and Resilience | +1.5% | Global, particularly developed economies | Short to Medium-term (2025-2029) |

| Technological Advancements in PMUs & PDCs | +1.0% | Global | Short to Medium-term (2025-2030) |

| Government Regulations and Mandates for Grid Reliability | +0.8% | North America (FERC), Europe (EU Directives) | Medium-term (2026-2031) |

Synchrophasor Market Restraints Analysis

Despite the strong growth drivers, the Synchrophasor Market faces several restraints that could potentially impede its full potential. One significant challenge is the high initial investment cost associated with deploying PMUs, Phasor Data Concentrators (PDCs), and the necessary communication infrastructure. Utilities, especially smaller ones or those in developing regions, may find these upfront expenditures prohibitive, leading to slower adoption rates. This cost factor extends beyond hardware to include the software, integration services, and training required to effectively utilize synchrophasor data, posing a substantial financial barrier for some stakeholders.

Another critical restraint is the complexity of managing and processing the enormous volumes of data generated by synchrophasors. Real-time data streams from hundreds or thousands of PMUs require robust data storage, analysis, and communication capabilities, which can strain existing IT infrastructure and personnel resources. Furthermore, cybersecurity concerns are paramount. As synchrophasors are critical components of grid infrastructure, any breach in their data streams or control systems could have severe consequences, leading to operational disruptions or widespread outages. The lack of standardized protocols in some regions and the shortage of skilled personnel capable of deploying, maintaining, and analyzing synchrophasor systems also act as significant impediments to wider market adoption.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Deployment Costs | -1.5% | Developing Economies, Smaller Utilities | Short to Medium-term (2025-2028) |

| Cybersecurity Concerns and Data Privacy Risks | -1.2% | Global, particularly critical infrastructure | Medium to Long-term (2026-2033) |

| Complexity of Data Management and Analytics | -1.0% | Global | Short to Medium-term (2025-2029) |

| Lack of Standardized Protocols and Interoperability Issues | -0.7% | Specific Regions with fragmented systems | Medium-term (2027-2031) |

| Shortage of Skilled Workforce and Technical Expertise | -0.5% | Global | Long-term (2028-2033) |

Synchrophasor Market Opportunities Analysis

The Synchrophasor Market presents numerous compelling opportunities driven by technological advancements, evolving energy landscapes, and the increasing global emphasis on sustainable and resilient power systems. A significant opportunity lies in the burgeoning market for advanced analytics software and platforms that can derive deeper insights from the vast amounts of data generated by PMUs. As utilities accumulate more synchrophasor data, the demand for sophisticated tools capable of real-time analysis, predictive modeling, and AI-driven insights will grow exponentially, creating new revenue streams for software developers and data service providers. This includes opportunities for specialized applications in areas like voltage stability assessment, oscillation detection, and transient analysis.

Another promising avenue is the integration of synchrophasors with other smart grid technologies, such as Internet of Things (IoT) devices, edge computing, and distributed ledger technologies. This convergence can create more comprehensive and resilient monitoring ecosystems, enabling localized control and optimized management of distributed energy resources. Furthermore, the expansion into developing economies offers substantial growth potential. As these regions build out new grid infrastructures or upgrade existing ones, they have the opportunity to adopt state-of-the-art synchrophasor technology from the outset, bypassing older legacy systems. The increasing focus on microgrids, virtual power plants, and demand-side management also creates new niches for synchrophasor applications, particularly in ensuring stability and optimizing operations within localized energy networks.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Analytics & AI Platforms | +1.9% | Global, particularly developed economies | Medium to Long-term (2026-2033) |

| Integration with IoT, Edge Computing, and Cloud Services | +1.6% | Global | Medium-term (2027-2032) |

| Expansion into Developing Economies & Emerging Markets | +1.3% | Asia Pacific (Southeast Asia, India), Latin America, MEA | Long-term (2028-2033) |

| Application in Microgrids & Distributed Energy Resource Management | +1.0% | Global, particularly niche applications | Short to Medium-term (2025-2030) |

| Partnerships and Collaborations for R&D and Market Expansion | +0.7% | Global | Medium-term (2026-2031) |

Synchrophasor Market Challenges Impact Analysis

The Synchrophasor Market, while promising, contends with several significant challenges that necessitate strategic solutions for sustained growth and widespread adoption. One primary challenge is ensuring interoperability among various PMU and PDC vendors, as well as with existing legacy grid systems. Achieving seamless data exchange and compatibility across diverse hardware and software platforms is crucial for creating a cohesive wide-area monitoring system, but differing proprietary standards can hinder this integration. This issue often leads to complex and costly customization efforts, increasing deployment timelines and operational complexities for utilities.

Another major challenge revolves around the sheer volume of data generated by synchrophasors and the associated requirements for high-bandwidth communication networks and robust data storage solutions. Transmitting and processing terabytes of real-time synchronized data demands significant network infrastructure upgrades and advanced data management capabilities, which can be a substantial hurdle for many utilities. Furthermore, the inherent complexity of synchrophasor technology requires a highly specialized workforce, from installation and maintenance to data analysis and application development. The global shortage of engineers and technicians with expertise in power systems and advanced digital technologies poses a significant constraint. Lastly, regulatory hurdles and the need for new policy frameworks to fully leverage synchrophasor data for grid operations and market mechanisms also present an ongoing challenge, requiring collaborative efforts between industry, government, and regulatory bodies to facilitate innovation and adoption.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Interoperability Issues Between Different Vendors' Systems | -1.4% | Global | Medium-term (2026-2030) |

| Data Overload and Requirement for High-Bandwidth Networks | -1.1% | Global | Short to Medium-term (2025-2029) |

| Recruiting and Retaining Skilled Workforce | -0.9% | Global | Long-term (2028-2033) |

| Cybersecurity Threats and Evolving Attack Vectors | -0.8% | Global | Continuous |

| Regulatory Hurdles and Policy Framework Development | -0.6% | Specific Countries/Regions | Medium to Long-term (2027-2033) |

Synchrophasor Market - Updated Report Scope

This comprehensive market research report on the Synchrophasor Market provides an in-depth analysis of market size, trends, drivers, restraints, opportunities, and challenges across various segments and key regions. The scope encompasses detailed quantitative and qualitative insights, offering a strategic outlook for stakeholders interested in the evolution of power system monitoring and control technologies. It delves into the impact of emerging technologies like Artificial Intelligence and the integration of renewable energy sources, delivering a holistic view of the market's current landscape and future trajectory. The report also highlights competitive dynamics, profiling key market players and their strategic initiatives to provide a robust understanding of the industry ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.80 Billion |

| Market Forecast in 2033 | USD 3.71 Billion |

| Growth Rate | 9.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Siemens AG, General Electric (GE) Grid Solutions, ABB Ltd., Schweitzer Engineering Laboratories (SEL), Eaton Corporation, Cisco Systems, Inc., Open Systems International (OSI) Inc., Power System Engineering (PSE) Inc., National Instruments Corporation, Qualitrol Company LLC, Doble Engineering Company, Aclara Technologies LLC, Applied Digital Solutions (ADS), Kalkitech, Schneider Electric SE, Siemens PTI, ETAP (Operation Technology, Inc.), Alstom (now GE Power), Quanta Services, Inc., CG Power and Industrial Solutions Limited |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Synchrophasor Market is meticulously segmented to provide a granular understanding of its various facets, enabling stakeholders to identify specific areas of growth and investment. These segmentations are crucial for analyzing market dynamics, understanding demand patterns, and tailoring solutions to specific industry needs. The market is primarily broken down by component, distinguishing between the hardware (PMUs, PDCs, communication networks) essential for data acquisition and transmission, and the software and services critical for data processing, analysis, and system maintenance. Each component plays a unique and vital role in the overall synchrophasor ecosystem, with software and analytics segments experiencing particularly rapid innovation.

Further segmentation by application highlights the diverse uses of synchrophasor technology, ranging from fundamental grid monitoring and wide-area control to advanced functions like fault detection, asset management, and predictive maintenance. This breakdown illustrates how synchrophasor data is leveraged to improve various aspects of grid operations, enhancing reliability and efficiency. End-user segmentation categorizes the primary consumers of synchrophasor solutions, predominantly electric utilities, but also including industrial complexes, renewable energy developers, and research institutions. Finally, deployment models, whether on-premise or cloud-based, reflect the evolving architectural preferences for data management and accessibility, with a growing trend towards cloud solutions for scalability and flexibility. This comprehensive segmentation allows for targeted market strategies and a deeper comprehension of value chain contributions.

- By Component:

- Phasor Measurement Units (PMUs)

- Phasor Data Concentrators (PDCs)

- Communication Networks

- Software & Analytics

- Services (Consulting, Integration, Maintenance & Support)

- By Application:

- Grid Monitoring & Visualization

- Wide-Area Monitoring & Control (WAMC)

- Protection & Control

- Asset Management

- Fault Detection & Diagnosis

- Predictive Maintenance

- Power System Planning

- State Estimation

- By End-User:

- Electric Utilities

- Industrial

- Renewable Energy Developers

- Research & Academia

- Grid Operators & ISOs

- By Deployment:

- On-Premise

- Cloud-Based

Regional Highlights

- North America: This region is a leading market for synchrophasor technology, driven by extensive grid modernization initiatives, significant investments in smart grid infrastructure, and stringent regulatory mandates aimed at enhancing grid reliability and resilience. The presence of major utilities and technology providers, coupled with early adoption of advanced monitoring systems, contributes to its dominant share. Focus on renewable energy integration and cybersecurity further accelerates deployment.

- Europe: Characterized by ambitious renewable energy targets and a strong emphasis on smart grid deployment, Europe represents a robust market for synchrophasors. Countries like Germany, France, and the UK are actively investing in PMU deployment for improved grid stability and efficiency. Cross-border grid synchronization and the development of a unified European energy market also drive the adoption of wide-area monitoring solutions.

- Asia Pacific (APAC): Expected to be the fastest-growing market, APAC is witnessing rapid industrialization, urbanization, and significant investments in new power generation and transmission infrastructure. Countries such as China, India, Japan, and South Korea are at the forefront of adopting advanced grid technologies to manage increasing electricity demand and integrate large-scale renewable projects. Government support and large-scale smart city initiatives are key growth catalysts.

- Latin America: This region is an emerging market for synchrophasors, with increasing awareness and investment in grid modernization projects to address issues like aging infrastructure and power quality. Brazil and Mexico are leading the adoption, driven by the need for improved grid reliability and the integration of new renewable energy projects.

- Middle East and Africa (MEA): The MEA region is showing promising growth, particularly due to significant investments in smart city projects, renewable energy developments (especially solar), and the need to upgrade existing grid infrastructure to meet growing energy demands. Gulf Cooperation Council (GCC) countries are at the forefront of adopting advanced power system solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Synchrophasor Market.- Siemens AG

- General Electric (GE) Grid Solutions

- ABB Ltd.

- Schweitzer Engineering Laboratories (SEL)

- Eaton Corporation

- Cisco Systems, Inc.

- Open Systems International (OSI) Inc.

- Power System Engineering (PSE) Inc.

- National Instruments Corporation

- Qualitrol Company LLC

- Doble Engineering Company

- Aclara Technologies LLC

- Applied Digital Solutions (ADS)

- Kalkitech

- Schneider Electric SE

- Siemens PTI

- ETAP (Operation Technology, Inc.)

- Alstom (now GE Power)

- Quanta Services, Inc.

- CG Power and Industrial Solutions Limited

Frequently Asked Questions

What is a synchrophasor and why is it important for power grids?

A synchrophasor is a precise measurement of an electricity waveform, taken at high speed across a wide geographic area. It is vital for power grids because it provides synchronized, real-time data on voltage and current magnitudes and phase angles. This enables enhanced situational awareness, allowing grid operators to detect anomalies, predict instabilities, and optimize power flow with unprecedented accuracy, leading to improved grid reliability, efficiency, and resilience against disturbances.

How do Synchrophasors contribute to smart grid development?

Synchrophasors are fundamental to smart grid development by providing the granular, time-synchronized data necessary for advanced grid monitoring, control, and automation. They enable applications such as wide-area monitoring, dynamic line rating, state estimation, and rapid fault location. This real-time visibility and control empower smart grids to efficiently integrate renewable energy sources, prevent blackouts, and manage complex power flows, thereby enhancing overall grid performance and adaptability.

What role does AI play in the Synchrophasor market?

Artificial Intelligence (AI) plays a transformative role in the Synchrophasor market by processing and analyzing the vast amounts of data generated by Phasor Measurement Units (PMUs). AI algorithms can detect subtle anomalies, predict system instabilities, and identify potential faults far more effectively than traditional methods. This enhances predictive maintenance, optimizes grid operations, and supports automated decision-making, significantly improving grid reliability and efficiency.

What are the key challenges in Synchrophasor deployment?

Key challenges in Synchrophasor deployment include high initial investment costs for hardware and infrastructure, the complexity of managing and processing large volumes of data, ensuring interoperability between diverse vendor systems, and addressing significant cybersecurity concerns. Additionally, a shortage of skilled personnel capable of deploying, maintaining, and analyzing these advanced systems poses a notable hurdle for widespread adoption.

Which regions are leading in Synchrophasor adoption?

North America and Europe are currently leading in Synchrophasor adoption, driven by extensive smart grid initiatives, grid modernization efforts, and stringent regulatory mandates. The Asia Pacific region, particularly countries like China and India, is rapidly emerging as a fast-growing market due to significant investments in new grid infrastructure and large-scale renewable energy integration projects.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted