America SLI Battery Market

America SLI Battery Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705056 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

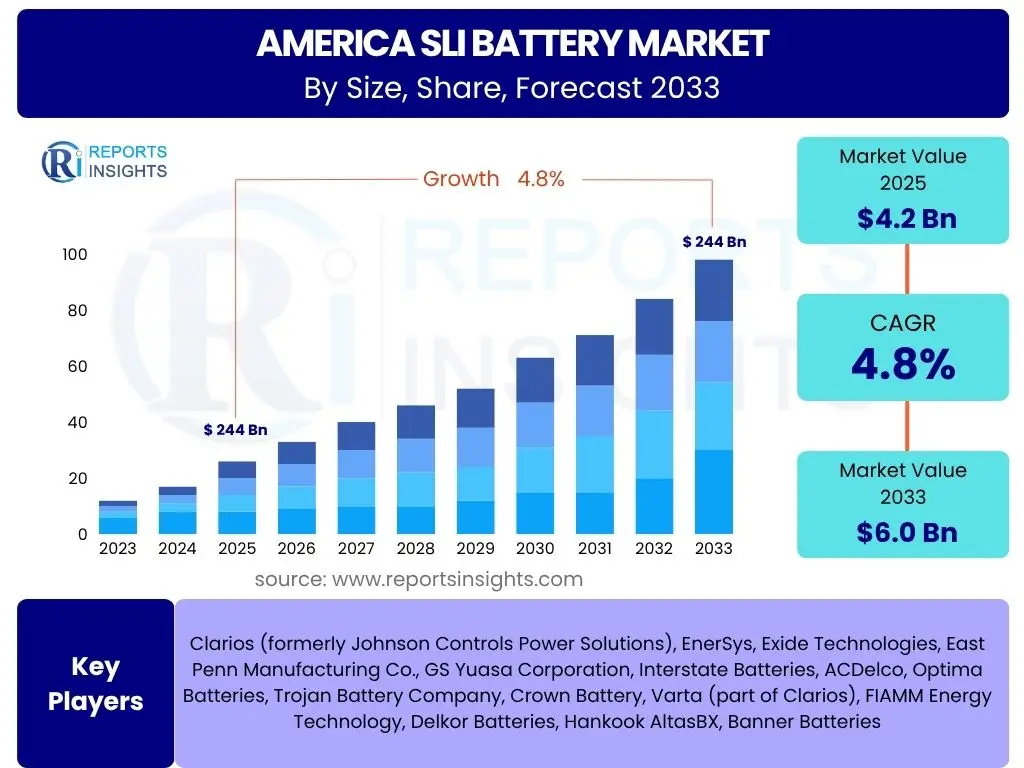

America SLI Battery Market Size

According to Reports Insights Consulting Pvt Ltd, The America SLI Battery Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033. The market is estimated at USD 4.2 Billion in 2025 and is projected to reach USD 6.0 Billion by the end of the forecast period in 2033. This growth is primarily driven by the consistent demand from the automotive sector, particularly for replacement batteries, and the increasing adoption of advanced Start-Stop vehicle technologies that require more sophisticated SLI battery types.

The resilience of the internal combustion engine (ICE) vehicle fleet, coupled with the steady expansion of the overall vehicle parc across North and South America, underpins this market expansion. While the long-term trend towards electric vehicles (EVs) is present, traditional SLI batteries retain a critical role in 12V auxiliary systems even within electrified powertrains, ensuring their continued relevance in the evolving automotive landscape. The market's stability is also bolstered by predictable replacement cycles and ongoing technological enhancements in lead-acid battery design, which improve performance and longevity.

Key America SLI Battery Market Trends & Insights

Common user inquiries regarding America SLI Battery market trends often revolve around the impact of vehicle electrification, technological advancements in lead-acid chemistries, the role of the aftermarket, and sustainability initiatives. Analysis reveals a market in transition, balancing established demand with innovative adaptations. While the rise of electric vehicles might suggest a decline, the persistent need for 12V power in all vehicle types, coupled with significant improvements in lead-acid technology, ensures ongoing relevance and growth in specific segments.

A notable trend is the increasing adoption of advanced lead-acid batteries, such as Absorbed Glass Mat (AGM) and Enhanced Flooded Battery (EFB), driven by the proliferation of vehicles equipped with Start-Stop systems and regenerative braking. These technologies place higher demands on batteries, requiring greater cycling capability and charge acceptance. Furthermore, the aftermarket segment continues to be a crucial driver, as SLI batteries are consumables with defined lifespans, necessitating regular replacements across the vast existing vehicle fleet. Sustainability is also gaining prominence, with efforts focused on improving recycling rates and reducing the environmental footprint of lead-acid battery production and disposal.

- Growing adoption of Start-Stop vehicle technology driving demand for AGM and EFB batteries.

- Consistent and robust growth in the aftermarket replacement segment.

- Continued relevance of 12V lead-acid batteries for auxiliary systems even in electric and hybrid vehicles.

- Emphasis on advanced lead-acid technologies for enhanced performance and longevity.

- Increasing focus on circular economy principles and higher recycling rates for lead-acid batteries.

- Market consolidation and strategic partnerships among key manufacturers.

AI Impact Analysis on America SLI Battery

User questions regarding the impact of Artificial Intelligence (AI) on the America SLI Battery market often explore its potential to revolutionize manufacturing, optimize battery performance, enhance supply chain efficiency, and accelerate research and development. The consensus suggests that AI is not a direct threat but rather a transformative tool capable of significant improvements across the battery lifecycle. AI's primary influence is seen in making existing processes smarter, more efficient, and predictive, thereby enhancing the competitive edge of traditional SLI battery manufacturers.

AI's application in manufacturing processes, such as predictive maintenance for machinery and quality control, can lead to reduced downtime and improved product consistency. In battery management, AI algorithms can analyze real-time performance data to optimize charging cycles, predict battery lifespan, and identify potential failures, extending battery life and improving reliability for end-users. Furthermore, AI tools can streamline complex supply chains by forecasting demand more accurately, managing inventory levels, and optimizing logistics, leading to cost reductions and greater responsiveness to market fluctuations. The integration of AI also promises to accelerate material discovery and design optimization in R&D, potentially leading to more efficient and environmentally friendly SLI battery formulations.

- Enhanced manufacturing efficiency and quality control through AI-driven automation and predictive analytics.

- Optimization of battery performance and lifespan via AI-powered Battery Management Systems (BMS).

- Streamlined supply chain management, including demand forecasting and logistics optimization.

- Accelerated research and development for new materials and battery designs.

- Improved predictive maintenance capabilities for both manufacturing equipment and in-vehicle batteries.

Key Takeaways America SLI Battery Market Size & Forecast

Common user questions about key takeaways from the America SLI Battery market size and forecast often focus on understanding the market's longevity, its primary growth drivers, and its resilience in the face of emerging automotive technologies. The analysis indicates that while significant shifts are occurring in the broader automotive landscape, the SLI battery market demonstrates robust stability and targeted growth, primarily driven by the indispensable role of 12V power in vehicles and continuous innovation within lead-acid technology.

A principal insight is the enduring necessity for SLI batteries across all vehicle types, including hybrids and electric vehicles, for functions like ignition, lighting, and powering onboard electronics. This fundamental requirement ensures a baseline demand irrespective of powertrain evolution. Another critical takeaway is the strong aftermarket cycle, which consistently fuels a significant portion of the market's revenue, driven by regular battery replacement needs. Furthermore, technological advancements, such as the widespread adoption of AGM and EFB batteries for Start-Stop vehicles, represent significant pockets of growth, demonstrating the lead-acid industry's capacity for innovation and adaptation to meet evolving automotive demands. The market is not merely sustaining but evolving, with specific segments experiencing notable expansion.

- The America SLI Battery market exhibits stable growth, largely propelled by aftermarket replacements and the increasing fleet of Start-Stop vehicles.

- Lead-acid batteries maintain their critical role in 12V auxiliary systems across traditional, hybrid, and electric vehicle architectures.

- Technological advancements in AGM and EFB battery types are key drivers of market value and product differentiation.

- Market resilience is observed despite the long-term automotive shift towards electrification, due to the inherent demand for dependable starting, lighting, and ignition functions.

- Sustainability initiatives, particularly in recycling, are becoming increasingly important for the long-term viability and public perception of the market.

America SLI Battery Market Drivers Analysis

The America SLI Battery market is primarily driven by several fundamental factors rooted in the automotive sector's dynamics and the essential nature of battery technology in modern vehicles. These drivers collectively contribute to a stable and growing demand, particularly within the vast existing vehicle fleet and the continuous introduction of new vehicles requiring reliable power sources. Understanding these drivers is crucial for forecasting market trajectory and identifying lucrative investment opportunities within the sector.

The consistent growth in vehicle production and sales across the American continent directly translates into a rising demand for SLI batteries as original equipment. Simultaneously, the inherent lifespan of lead-acid batteries necessitates periodic replacement, fueling a robust aftermarket segment that forms a substantial portion of the market. Furthermore, the increasing integration of advanced automotive features, such as Start-Stop systems and regenerative braking, demands more sophisticated and durable battery solutions like AGM and EFB technologies, driving premium product sales. The continued dominance of internal combustion engine (ICE) vehicles in many parts of the Americas, alongside the enduring need for 12V auxiliary power in hybrid and electric vehicles, further solidifies the foundational demand for SLI batteries, making the market resilient to rapid shifts in powertrain technology.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Vehicle Parc and New Vehicle Sales | +1.5% | North America, Latin America | 2025-2033 |

| Robust Aftermarket Replacement Demand | +1.2% | United States, Canada, Brazil, Mexico | 2025-2033 |

| Increasing Adoption of Start-Stop Vehicle Systems | +0.8% | United States, Canada | 2025-2030 |

| Continued Need for 12V Systems in All Vehicle Types | +0.7% | All American Countries | 2025-2033 |

| Technological Advancements in Lead-Acid Batteries | +0.6% | Global, particularly North America | 2025-2033 |

America SLI Battery Market Restraints Analysis

Despite a generally stable growth trajectory, the America SLI Battery market faces several restraints that could temper its expansion. These limiting factors often stem from technological evolution in the automotive industry, environmental considerations, and market dynamics that favor alternative solutions or create cost pressures. Manufacturers and stakeholders must strategically address these challenges to mitigate their impact on market potential.

A primary restraint is the accelerating global shift towards Battery Electric Vehicles (BEVs), which significantly reduce or alter the traditional need for large SLI batteries, although a 12V auxiliary battery is typically still required. This transition, particularly prominent in North America, poses a long-term challenge to the volume growth of traditional SLI products. Furthermore, advancements in lithium-ion battery technology, while currently more expensive for SLI applications, present a competitive threat for future integration into 12V systems. Stringent environmental regulations concerning lead use and disposal also impose compliance costs and operational complexities on manufacturers, potentially limiting investment or innovation in lead-acid solutions. Lastly, fluctuating raw material prices, particularly for lead, can impact manufacturing costs and profit margins, introducing volatility into the market and potentially leading to price increases for consumers or reduced profitability for producers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Accelerated Adoption of Electric Vehicles (BEVs) | -1.0% | United States, Canada | 2028-2033 |

| Advancements in Lithium-Ion Battery Technology | -0.7% | Global, especially North America | 2025-2033 |

| Stringent Environmental Regulations | -0.5% | United States, Mexico | 2025-2033 |

| Fluctuating Raw Material Prices (e.g., Lead) | -0.4% | Global Supply Chains | 2025-2033 |

| Potential for Longer Battery Lifespan Due to Quality Improvements | -0.3% | North America | 2030-2033 |

America SLI Battery Market Opportunities Analysis

Despite existing restraints, the America SLI Battery market presents various opportunities for growth and innovation. These opportunities arise from evolving automotive needs, sustainability imperatives, and untapped market segments. Capitalizing on these areas can provide manufacturers with new revenue streams and strengthen their market position amidst changing industry dynamics.

A significant opportunity lies in the expanding market for advanced lead-acid batteries, specifically AGM and EFB types, driven by the increasing integration of Start-Stop systems and mild-hybrid technologies in new vehicles. These systems require batteries capable of deeper cycling and faster recharge, which advanced lead-acid designs effectively provide. The burgeoning market for hybrid vehicles also offers a distinct opportunity, as these vehicles still rely on robust 12V SLI batteries for their essential auxiliary systems, complementing the high-voltage traction battery. Furthermore, enhancing recycling infrastructure and promoting a circular economy for lead-acid batteries can not only address environmental concerns but also create new business models and reduce reliance on virgin lead. Lastly, niche applications such as marine, powersports, and certain industrial backup power systems continue to rely heavily on SLI technology, offering stable and specialized demand. Exploring underserved regions within Latin America with growing vehicle fleets also presents considerable expansion potential for manufacturers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Advanced Lead-Acid (AGM/EFB) Market | +1.0% | United States, Canada, Mexico | 2025-2033 |

| Growth in Hybrid Electric Vehicle (HEV) Sales | +0.8% | United States, Canada | 2025-2033 |

| Enhanced Recycling and Circular Economy Initiatives | +0.7% | North America, Brazil | 2025-2033 |

| Diversification into Niche Applications (Marine, Powersports) | +0.6% | Coastal Regions, Recreational Areas (North America) | 2025-2033 |

| Untapped Market Potential in Emerging Latin American Economies | +0.5% | Brazil, Argentina, Colombia | 2025-2033 |

America SLI Battery Market Challenges Impact Analysis

The America SLI Battery market faces several significant challenges that require strategic planning and adaptation from industry participants. These challenges, distinct from market restraints, often relate to operational complexities, competitive pressures, and evolving consumer and regulatory landscapes. Successfully navigating these hurdles is essential for sustained growth and profitability in the long term.

One of the foremost challenges is the intensifying competition from alternative battery chemistries, particularly lithium-ion, which is rapidly evolving and becoming more cost-effective for various automotive applications beyond just traction batteries. While not directly replacing SLI in all current uses, this competition can limit expansion into new vehicle segments or specific 12V auxiliary power needs. Environmental concerns surrounding lead, despite high recycling rates, continue to pose a public perception challenge and necessitate ongoing investment in cleaner manufacturing processes and responsible disposal. Furthermore, maintaining manufacturing efficiencies amidst rising labor costs and energy prices, especially in regions with stringent environmental controls, remains a constant operational challenge. Supply chain disruptions, often driven by geopolitical events or global material shortages, can significantly impact production schedules and raw material availability, leading to cost increases and delivery delays. Lastly, adapting to evolving vehicle architectures and electronic demands, which require increasingly sophisticated battery designs, presents a continuous technological challenge for manufacturers striving to meet future automotive requirements.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intensifying Competition from Lithium-Ion Technologies | -0.9% | North America | 2025-2033 |

| Persistent Environmental Concerns and Regulations for Lead | -0.6% | United States, Canada | 2025-2033 |

| Maintaining Manufacturing Efficiencies Amidst Rising Costs | -0.5% | United States, Mexico | 2025-2033 |

| Vulnerability to Global Supply Chain Disruptions | -0.4% | All American Countries | 2025-2030 |

| Adapting to Rapidly Evolving Vehicle Architectures | -0.3% | Global Automotive Hubs | 2025-2033 |

America SLI Battery Market - Updated Report Scope

This market research report provides an in-depth analysis of the America SLI Battery Market, covering historical data, current market dynamics, and future projections. It offers a comprehensive overview of market size, trends, drivers, restraints, opportunities, and challenges affecting the industry across various segments and key geographies within the American continent. The report aims to equip stakeholders with actionable insights for strategic decision-making in a dynamic automotive battery landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.2 Billion |

| Market Forecast in 2033 | USD 6.0 Billion |

| Growth Rate | 4.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Clarios (formerly Johnson Controls Power Solutions), EnerSys, Exide Technologies, East Penn Manufacturing Co., GS Yuasa Corporation, Interstate Batteries, ACDelco, Optima Batteries, Trojan Battery Company, Crown Battery, Varta (part of Clarios), FIAMM Energy Technology, Delkor Batteries, Hankook AltasBX, Banner Batteries |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The America SLI Battery market is segmented across various critical dimensions, providing a granular view of its structure and opportunities. These segments help in understanding the distinct demands and growth patterns within the industry, allowing for targeted strategies and product development. Each segment plays a unique role in shaping the overall market landscape, driven by specific consumer needs, technological requirements, and distribution dynamics.

Segmentation by Vehicle Type is crucial, distinguishing between the demands of passenger cars, commercial vehicles, and two-wheelers, each with varying battery specifications and replacement cycles. By Battery Type, the market is differentiated into traditional flooded lead-acid, Absorbed Glass Mat (AGM), and Enhanced Flooded Batteries (EFB), reflecting the shift towards more advanced technologies for modern vehicle systems. The Distribution Channel segmentation, comprising OEM and aftermarket, highlights the two primary routes through which batteries reach end-users, with the aftermarket representing a significant and consistent revenue stream. Further analysis by End-Use Application covers the primary automotive sector along with niche segments like marine and powersports, showcasing diversified demand. Understanding these intricate segmentations is key to identifying high-growth areas and tailoring market approaches effectively.

- By Vehicle Type:

- Passenger Cars

- Commercial Vehicles (Light, Medium, Heavy-Duty)

- Two-wheelers

- Recreational Vehicles

- Powersports Vehicles

- By Battery Type:

- Flooded Lead-Acid Batteries

- Absorbed Glass Mat (AGM) Batteries

- Enhanced Flooded Batteries (EFB)

- By Distribution Channel:

- OEM (Original Equipment Manufacturer)

- Aftermarket

- By End-Use Application:

- Automotive

- Marine

- Industrial (Selected Backup Power for Automotive Ancillaries)

- By Sales Channel:

- Online

- Offline (Retailers, Service Stations)

Regional Highlights

The America SLI Battery market exhibits distinct regional dynamics driven by varying levels of economic development, vehicle parc maturity, and regulatory environments. North America, encompassing the United States and Canada, represents the largest and most technologically advanced segment, characterized by a high adoption rate of Start-Stop vehicles and a robust aftermarket. This region benefits from a well-established automotive industry and high consumer awareness regarding battery maintenance and replacement, driving consistent demand for both conventional and advanced SLI batteries.

Latin America, including countries such as Brazil, Mexico, and Argentina, represents a significant growth opportunity. While often dominated by more cost-sensitive flooded lead-acid batteries, the expanding middle class, increasing vehicle ownership, and ongoing infrastructure development are fueling demand. Mexico's strong ties to the North American automotive manufacturing sector also contribute substantially to its SLI battery market. Brazil, with its large vehicle fleet and domestic production capabilities, is another key market in the region. These countries offer potential for market expansion, particularly as vehicle fleets continue to grow and modern vehicle technologies gradually diffuse into their markets. The diverse economic conditions and vehicle preferences across the American continent necessitate tailored strategies for market penetration and product offerings.

- United States: Largest market within America, characterized by high adoption of advanced SLI technologies (AGM, EFB) for Start-Stop vehicles and a dominant aftermarket. Strong emphasis on quality and brand reputation.

- Canada: Similar market characteristics to the U.S., with consistent demand driven by vehicle parc and replacement cycles. Gradual shift towards more energy-efficient battery solutions.

- Mexico: Significant automotive manufacturing hub, leading to strong OEM demand. Growing aftermarket driven by an expanding vehicle fleet. Price sensitivity is a key factor.

- Brazil: Largest market in Latin America, with a substantial and growing vehicle parc. Domestic production plays a significant role. Opportunities for both conventional and, increasingly, advanced SLI batteries.

- Argentina: Developing market with increasing vehicle penetration. Demand primarily for traditional flooded batteries, with gradual uptake of advanced technologies in newer vehicle models.

- Other Latin American Countries: Emerging markets with potential for growth, often influenced by local economic conditions and vehicle import trends.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the America SLI Battery Market.- Clarios (formerly Johnson Controls Power Solutions)

- EnerSys

- Exide Technologies

- East Penn Manufacturing Co.

- GS Yuasa Corporation

- Interstate Batteries

- ACDelco

- Optima Batteries

- Trojan Battery Company

- Crown Battery

- Varta (part of Clarios)

- FIAMM Energy Technology

- Delkor Batteries

- Hankook AltasBX

- Banner Batteries

- C&D Technologies (part of EnerSys)

- Leoch International Technology Limited

- Furukawa Battery Co., Ltd.

- Chloride Batteries S.E. Asia Pte Ltd.

- Midac SpA

Frequently Asked Questions

Analyze common user questions about the America SLI Battery market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is an SLI battery and its primary function in vehicles?

An SLI (Starting, Lighting, Ignition) battery is a lead-acid rechargeable battery designed to supply electric current to a motor vehicle. Its primary functions are to deliver a high burst of power to the starter motor for engine cranking, provide power for vehicle lights, and operate other electrical accessories when the engine is not running.

How large is the America SLI Battery market expected to grow by 2033?

The America SLI Battery Market is projected to reach an estimated USD 6.0 Billion by the end of 2033, growing at a Compound Annual Growth Rate (CAGR) of 4.8% from USD 4.2 Billion in 2025.

What are the key drivers propelling the America SLI Battery market?

Key drivers include the continuous growth in the overall vehicle parc and new vehicle sales, the robust and consistent demand from the aftermarket for battery replacements, and the increasing adoption of vehicles equipped with Start-Stop technology, which require more advanced battery types like AGM and EFB.

Is the America SLI Battery market declining due to the rise of electric vehicles?

While the long-term trend towards electric vehicles (BEVs) presents a challenge, the America SLI Battery market is not declining. Traditional SLI batteries continue to be essential for 12V auxiliary systems in all vehicle types, including hybrids and BEVs, for critical functions like lighting, infotainment, and safety systems. This ensures their continued relevance and a stable market, complemented by strong aftermarket demand.

What role does recycling play in the America SLI Battery market?

Recycling plays a crucial role in the America SLI Battery market, as lead-acid batteries are one of the most highly recycled consumer products, with rates exceeding 99% in many regions. This high recycling rate significantly contributes to the sustainability of the industry, reduces reliance on virgin lead, mitigates environmental impact, and supports the circular economy model by reintroducing materials into the manufacturing cycle.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted