Lead Acid Stationary Battery Market

Lead Acid Stationary Battery Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705146 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

Lead Acid Stationary Battery Market Size

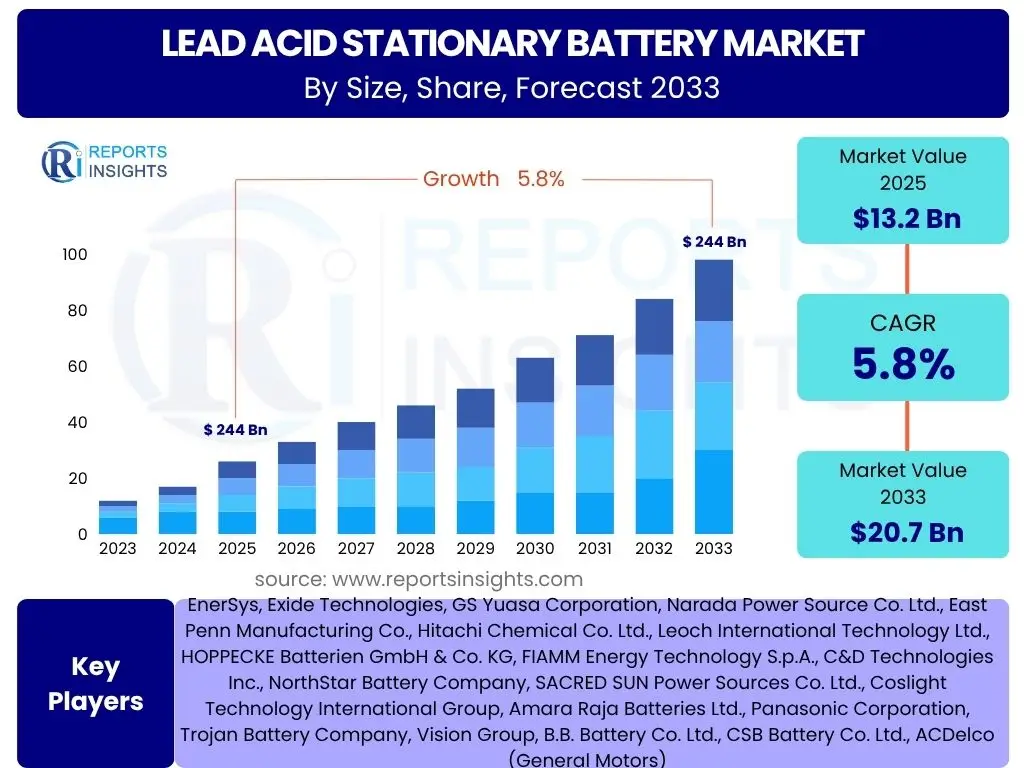

According to Reports Insights Consulting Pvt Ltd, The Lead Acid Stationary Battery Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 13.2 Billion in 2025 and is projected to reach USD 20.7 Billion by the end of the forecast period in 2033.

Key Lead Acid Stationary Battery Market Trends & Insights

The Lead Acid Stationary Battery market is currently experiencing several pivotal trends, largely driven by the increasing global demand for reliable backup power solutions and advancements in battery technology. Users frequently inquire about the evolving applications, specific technological improvements, and the market's response to environmental concerns. Key insights reveal a sustained relevance for lead acid batteries in critical infrastructure due to their cost-effectiveness and proven reliability, particularly in sectors such as telecommunications and data centers.

There is a notable shift towards Valve Regulated Lead Acid (VRLA) battery types, including AGM and Gel technologies, which offer lower maintenance and enhanced safety features. Furthermore, the integration of stationary batteries into hybrid renewable energy systems is emerging as a significant trend, especially in off-grid and rural electrification projects. Sustainability and circular economy principles are also gaining traction, with increased focus on efficient recycling programs to mitigate environmental impact.

- VRLA Battery Dominance: Increasing preference for VRLA types (AGM, Gel) due to their sealed, maintenance-free operation and suitability for indoor critical applications.

- Increased Demand from Telecom & Data Centers: Consistent growth in demand driven by expanding 5G networks, cloud computing infrastructure, and the necessity for uninterrupted power.

- Focus on Recycling & Sustainability: Growing emphasis on robust recycling programs and responsible disposal to address environmental concerns and promote resource efficiency.

- Hybrid Renewable Energy Systems: Rising adoption of lead acid batteries in conjunction with solar and wind power for stable and cost-effective energy storage solutions.

- Enhanced Performance & Lifespan: Ongoing research and development leading to improved battery designs that offer extended cycle life and enhanced performance characteristics.

AI Impact Analysis on Lead Acid Stationary Battery

Common user questions related to AI's influence on Lead Acid Stationary Batteries often revolve around how artificial intelligence can enhance battery performance, prolong lifespan, and optimize operational efficiency. The analysis indicates that AI is poised to revolutionize battery management and maintenance, moving from reactive to proactive strategies. Users are particularly interested in AI's role in predictive failure analysis, optimizing charging protocols, and streamlining supply chain logistics within the battery industry.

AI algorithms can analyze vast datasets from battery performance metrics, enabling highly accurate predictive maintenance schedules and reducing unexpected failures. This not only minimizes downtime for critical applications but also extends the useful life of battery assets, leading to significant cost savings. Furthermore, AI's application in manufacturing processes can enhance quality control and optimize production lines, ensuring higher consistency and reliability of lead acid stationary batteries. The integration of AI into broader energy management systems also allows for smarter power distribution and utilization, maximizing the efficiency of stationary battery installations.

- Predictive Maintenance: AI algorithms analyze battery data to predict potential failures, enabling proactive maintenance and extending battery lifespan.

- Optimized Charging/Discharging Cycles: AI dynamically adjusts charging and discharging parameters based on usage patterns and environmental conditions, enhancing efficiency and battery health.

- Supply Chain & Logistics Optimization: AI improves demand forecasting, inventory management, and logistics for raw materials and finished products, leading to cost reductions and improved responsiveness.

- Quality Control in Manufacturing: AI-powered vision systems and data analytics enhance quality assurance in battery production, identifying defects early and improving product consistency.

- Energy Management System Integration: AI enables smarter integration of lead acid batteries into grid-scale and localized energy management systems for optimized power flow and reliability.

Key Takeaways Lead Acid Stationary Battery Market Size & Forecast

User inquiries about the Lead Acid Stationary Battery market size and forecast frequently highlight concerns about its future amidst the rise of alternative battery chemistries. A key insight is that while competition from lithium-ion batteries is significant, the lead acid stationary battery market maintains a steady growth trajectory, primarily due to its entrenched position in specific critical applications where cost-effectiveness and proven reliability are paramount. The forecast indicates continued moderate expansion, underscoring its enduring relevance in the global energy storage landscape.

The market's resilience is largely attributed to sustained demand from the telecommunications sector, growing data center infrastructure, and the increasing need for reliable backup power in various industrial and commercial settings. Furthermore, advancements in lead acid battery technology, coupled with a robust established recycling infrastructure, contribute to its stability. Stakeholders should recognize that while growth may not be as explosive as in emerging battery technologies, the market offers consistent opportunities in its core segments, emphasizing operational efficiency and sustainable practices.

- Steady Growth Trajectory: The market is projected to grow consistently, driven by essential applications despite competition.

- Resilience in Critical Applications: Lead acid batteries remain the preferred choice for cost-sensitive, high-reliability backup power in telecom and UPS.

- Cost-Effectiveness as a Key Differentiator: Their lower upfront cost continues to be a significant advantage over alternative battery technologies.

- Importance of Sustainability Initiatives: Growing focus on circular economy models, including robust recycling and responsible manufacturing practices, is crucial for market acceptance.

- Niche Market Dominance: Lead acid batteries continue to dominate specific market niches where their characteristics offer a superior value proposition.

Lead Acid Stationary Battery Market Drivers Analysis

The Lead Acid Stationary Battery market is predominantly driven by the escalating demand for uninterrupted power supply across various critical sectors. The rapid expansion of digital infrastructure globally, including data centers and telecommunication networks, necessitates reliable and cost-effective backup power solutions, a role traditionally fulfilled by stationary lead acid batteries. Their proven durability and relatively low acquisition cost make them an attractive option for large-scale deployments, especially in regions undergoing rapid industrialization and urbanization.

Moreover, the increasing frequency of power outages and grid instability in many parts of the world accentuates the need for dependable energy storage. This drives demand for stationary batteries in emergency lighting, industrial processes, and renewable energy integration, where they serve as crucial components in ensuring energy security. The inherent advantages of lead acid technology, such as robust performance in varying temperatures and ease of recycling, continue to underpin its market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Telecom Infrastructure Expansion, including 5G Rollouts | +1.2% | Asia Pacific, Middle East & Africa, Latin America | Short-Medium Term (2025-2029) |

| Growth of Data Centers and Uninterruptible Power Supply (UPS) Systems | +1.0% | North America, Europe, Asia Pacific | Medium Term (2025-2031) |

| Increasing Demand for Reliable Backup Power in Commercial & Industrial Sectors | +0.8% | Global | Ongoing (2025-2033) |

| Cost-Effectiveness and Established Recycling Infrastructure | +0.7% | Global | Long Term (2025-2033) |

Lead Acid Stationary Battery Market Restraints Analysis

Despite its steady growth, the Lead Acid Stationary Battery market faces significant restraints, primarily stemming from the rapid advancements and increasing adoption of alternative battery technologies. The escalating competition from lithium-ion batteries, which offer higher energy density, longer cycle life, and lighter weight, poses a substantial challenge to market share, particularly in new and emerging energy storage applications. This intense rivalry often pushes lead acid manufacturers to innovate rapidly or focus more intensely on their traditional, cost-sensitive niches.

Environmental concerns associated with lead-acid batteries also act as a notable restraint. The toxicity of lead and the environmental impact of improper disposal lead to stringent regulations and increased public scrutiny, especially in developed economies. While recycling infrastructure for lead acid batteries is well-established, continuous pressure to enhance sustainability and reduce hazardous waste handling costs can impact market expansion and operational profitability. These factors necessitate ongoing investment in greener manufacturing processes and more efficient recycling solutions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intensifying Competition from Lithium-Ion and Other Advanced Batteries | -1.5% | Global, particularly North America, Europe, China | Medium-Long Term (2025-2033) |

| Environmental Concerns and Stringent Regulations on Lead Usage & Disposal | -0.9% | Europe, North America | Ongoing (2025-2033) |

| Relatively Lower Energy Density and Shorter Cycle Life Compared to Alternatives | -0.7% | Global | Long Term (2025-2033) |

| Raw Material Price Volatility (Lead, Plastics, Acids) | -0.5% | Global, especially Import-Reliant Regions | Short-Medium Term (2025-2029) |

Lead Acid Stationary Battery Market Opportunities Analysis

The Lead Acid Stationary Battery market presents several significant opportunities for growth, particularly through geographical expansion and technological refinement. Emerging economies, especially in Asia Pacific, Latin America, and Africa, offer vast untapped potential due to their rapidly expanding telecommunications infrastructure, increasing urbanization, and growing demand for reliable power solutions in areas with nascent grid development. These regions often prioritize cost-effective and robust solutions, where lead acid batteries hold a competitive edge.

Furthermore, advancements in recycling technologies and the broader push towards a circular economy represent a substantial opportunity. Improving the efficiency and sustainability of lead acid battery recycling not only addresses environmental concerns but also reduces reliance on virgin raw materials, potentially stabilizing costs and enhancing the industry's green credentials. The continued development of enhanced lead acid chemistries, such as advanced VRLA designs or hybrid solutions, also offers avenues for improving performance characteristics and extending market applicability, even in the face of competition from other battery types.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand in Emerging Economies for Telecom and Backup Power | +1.1% | Asia Pacific, Middle East & Africa, Latin America | Medium-Long Term (2025-2033) |

| Advancements in Recycling Technologies and Circular Economy Initiatives | +0.9% | Europe, North America, Global | Long Term (2028-2033) |

| Integration into Hybrid Renewable Energy Systems (Solar, Wind) | +0.8% | Global, especially regions with high RE penetration | Medium Term (2025-2031) |

| Development of Enhanced Lead-Acid Chemistries (e.g., carbon-enhanced, thin plate) | +0.6% | Global, R&D Hubs | Long Term (2028-2033) |

Lead Acid Stationary Battery Market Challenges Impact Analysis

The Lead Acid Stationary Battery market faces several persistent challenges that impact its growth trajectory and competitive standing. One primary challenge is navigating the increasingly stringent environmental compliance requirements and the complexities associated with the safe disposal and recycling of lead-based products. These regulations, while necessary for public health and environmental protection, can increase operational costs for manufacturers and necessitate continuous investment in cleaner production processes and advanced recycling facilities.

Another significant challenge is maintaining a competitive edge against the rapid technological advancements and market penetration of alternative battery chemistries, particularly lithium-ion. While lead acid batteries offer cost advantages, their lower energy density and shorter cycle life compared to newer technologies can limit their adoption in certain high-performance or space-constrained applications. This forces lead acid manufacturers to innovate strategically, focusing on niche markets where their unique value proposition remains strong, while also contending with potential supply chain disruptions and price fluctuations of essential raw materials like lead.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Strict Environmental Compliance and Waste Management Regulations | -0.8% | Global, particularly developed economies | Ongoing (2025-2033) |

| Maintaining Competitive Edge Against Rapidly Evolving Advanced Batteries | -0.7% | Global | Long Term (2025-2033) |

| Supply Chain Disruptions and Fluctuations in Lead and Other Raw Material Prices | -0.6% | Global | Short-Medium Term (2025-2029) |

| Limited Investment in R&D Compared to Lithium-Ion Technologies | -0.5% | Global | Long Term (2025-2033) |

Lead Acid Stationary Battery Market - Updated Report Scope

This report provides a comprehensive analysis of the Lead Acid Stationary Battery Market, offering detailed insights into market dynamics, segmentation, regional trends, and competitive landscape. The scope includes an in-depth examination of market drivers, restraints, opportunities, and challenges, providing a holistic view of the industry's current state and future potential. It incorporates historical data from 2019-2023 and provides forecasts up to 2033, enabling stakeholders to make informed strategic decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 13.2 Billion |

| Market Forecast in 2033 | USD 20.7 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | EnerSys, Exide Technologies, GS Yuasa Corporation, Narada Power Source Co. Ltd., East Penn Manufacturing Co., Hitachi Chemical Co. Ltd., Leoch International Technology Ltd., HOPPECKE Batterien GmbH & Co. KG, FIAMM Energy Technology S.p.A., C&D Technologies Inc., NorthStar Battery Company, SACRED SUN Power Sources Co. Ltd., Coslight Technology International Group, Amara Raja Batteries Ltd., Panasonic Corporation, Trojan Battery Company, Vision Group, B.B. Battery Co. Ltd., CSB Battery Co. Ltd., ACDelco (General Motors) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Lead Acid Stationary Battery market is extensively segmented by various parameters, including battery type, application, and end-use industry. This segmentation provides a granular view of market dynamics, revealing specific growth drivers and competitive landscapes within each category. The differing technical requirements and operational environments of each segment dictate the preference for specific battery types, influencing market share distribution and strategic investments by manufacturers. Understanding these segments is crucial for identifying key growth areas and developing targeted market strategies.

- By Type:

- VRLA Battery (Valve Regulated Lead Acid): These are sealed, maintenance-free batteries that are widely adopted due to their versatility and safety.

- AGM (Absorbed Glass Mat): Known for their efficiency in high-current applications and deep cycling capabilities.

- Gel: Offers superior performance in extreme temperatures and deep discharge, making them suitable for renewable energy storage.

- Flooded Battery (Wet Cell/Vented): Traditional lead acid batteries requiring regular maintenance, often preferred for large-scale, long-life applications.

- OPzS: High-performance tubular plate cells with long design life, used in telecom and utility applications.

- GroE: Generally used in standby power applications and power plants due to their robustness and reliability.

- Flat Plate: Common in various industrial and standby power applications.

- VRLA Battery (Valve Regulated Lead Acid): These are sealed, maintenance-free batteries that are widely adopted due to their versatility and safety.

- By Application:

- Telecommunications: Critical for base stations, switching centers, and data transmission equipment.

- Uninterruptible Power Supply (UPS): Essential for data centers, hospitals, and financial institutions to ensure continuous power.

- Emergency Lighting: Provides backup power for safety lighting in commercial and public buildings.

- Renewable Energy Storage: Used in solar and wind power systems for energy storage and grid stabilization.

- Industrial: Various applications including industrial control systems, forklifts, and railway signaling.

- Oil & Gas: Provides backup power for critical equipment in remote and harsh environments.

- Healthcare: Ensures uninterrupted power for medical equipment and life support systems in hospitals and clinics.

- By End-Use Industry:

- Commercial: Offices, retail establishments, and other businesses requiring backup power.

- Residential: Home backup power systems and small-scale renewable energy storage.

- Industrial: Manufacturing plants, power generation facilities, and mining operations.

- Utilities: Substations, power grids, and transmission systems for energy security.

Regional Highlights

- North America: Characterized by significant demand from the expanding data center industry and robust telecommunications infrastructure. The region exhibits a strong preference for VRLA technology due to its maintenance-free benefits and stringent safety standards. Investment in renewable energy storage is also driving demand for reliable, cost-effective battery solutions.

- Europe: Driven by a strong focus on renewable energy integration and stringent environmental regulations promoting sustainable practices and efficient recycling. Germany, the UK, and France are key markets with established industrial sectors and a growing need for reliable backup power for critical infrastructure and smart grid initiatives.

- Asia Pacific (APAC): Represents the largest and fastest-growing market, propelled by rapid industrialization, urbanization, and significant investments in telecommunications infrastructure, especially 5G deployment. Countries like China and India are experiencing exponential growth in data centers, telecom networks, and off-grid power solutions, making them lucrative markets for lead acid stationary batteries.

- Latin America: Exhibits emerging growth in its telecommunications sector and increasing adoption of off-grid and hybrid energy solutions in remote areas. Economic development and infrastructure expansion are key drivers for stationary battery demand, with a focus on cost-efficient and reliable solutions.

- Middle East & Africa (MEA): Witnessing substantial growth due to the expansion of telecommunications networks, particularly in underserved rural areas, and increasing investments in critical infrastructure projects. The demand for reliable backup power solutions in challenging environmental conditions makes lead acid batteries a suitable choice.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Lead Acid Stationary Battery Market.- EnerSys

- Exide Technologies

- GS Yuasa Corporation

- Narada Power Source Co. Ltd.

- East Penn Manufacturing Co.

- Hitachi Chemical Co. Ltd.

- Leoch International Technology Ltd.

- HOPPECKE Batterien GmbH & Co. KG

- FIAMM Energy Technology S.p.A.

- C&D Technologies Inc.

- NorthStar Battery Company

- SACRED SUN Power Sources Co. Ltd.

- Coslight Technology International Group

- Amara Raja Batteries Ltd.

- Panasonic Corporation

- Trojan Battery Company

- Vision Group

- B.B. Battery Co. Ltd.

- CSB Battery Co. Ltd.

- ACDelco (General Motors)

Frequently Asked Questions

Analyze common user questions about the Lead Acid Stationary Battery market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are Lead Acid Stationary Batteries primarily used for?

Lead acid stationary batteries are crucial for providing reliable backup power in critical applications such as telecommunications networks, data centers, uninterruptible power supplies (UPS), renewable energy storage systems, and emergency lighting. Their primary function is to ensure continuous power supply during grid outages or fluctuations, maintaining essential operations.

How do VRLA and Flooded Lead Acid Batteries differ in stationary applications?

Valve Regulated Lead Acid (VRLA) batteries, including AGM and Gel types, are sealed, maintenance-free, and can be installed in various orientations, making them suitable for indoor applications like UPS and telecom sites. Flooded lead acid batteries require regular maintenance and ventilation due to gas emissions but offer longer design life and are often preferred for large-scale utility and renewable energy storage where maintenance is manageable.

What factors drive the growth of the Lead Acid Stationary Battery market?

Key drivers include the exponential growth of data centers and digital infrastructure, the continuous expansion of telecommunications networks (including 5G rollouts), increasing demand for reliable backup power across commercial and industrial sectors, and the inherent cost-effectiveness of lead acid batteries compared to alternative storage technologies.

What challenges does the Lead Acid Stationary Battery market face?

Significant challenges include intense competition from advanced battery technologies like lithium-ion, stringent environmental regulations concerning lead content and recycling, the relatively lower energy density and cycle life compared to newer chemistries, and the volatility of raw material prices.

What is the long-term outlook for Lead Acid Stationary Batteries in the energy storage landscape?

Despite competition, lead acid stationary batteries are expected to maintain a significant presence due to their proven reliability, cost efficiency, and established recycling infrastructure. Continued technological advancements, particularly in VRLA formulations, and sustained demand from critical infrastructure and specific niche applications will ensure stable, albeit moderate, growth.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted