Synchronou Condenser Market

Synchronou Condenser Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701500 | Last Updated : July 30, 2025 |

Format : ![]()

![]()

![]()

![]()

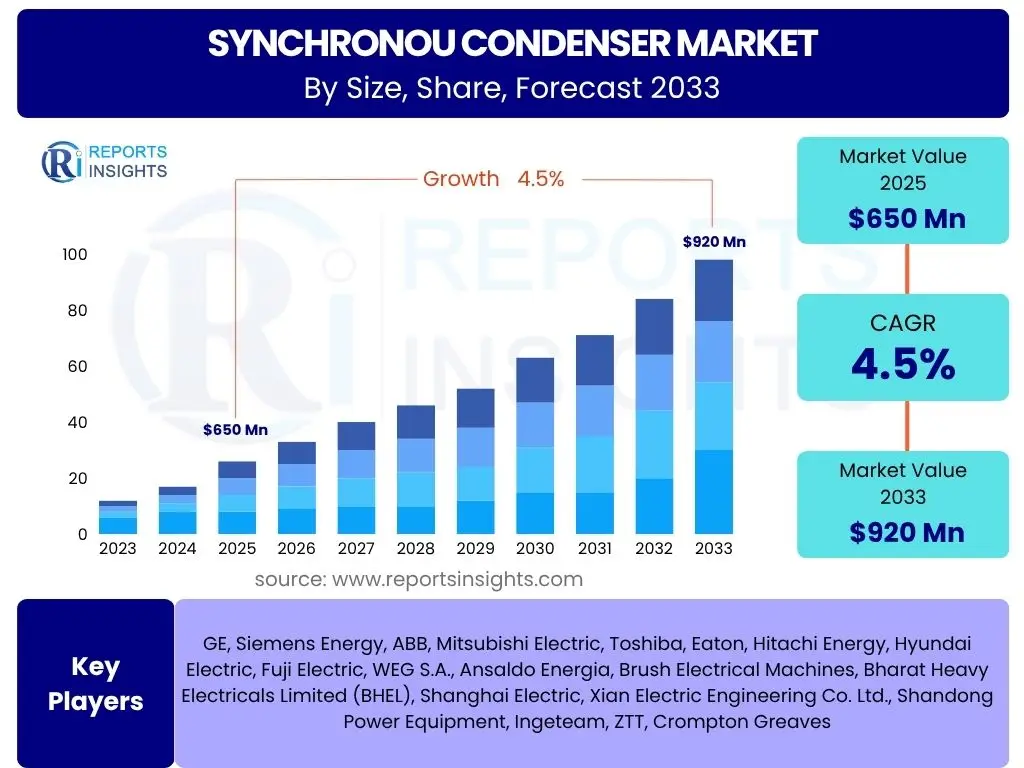

Synchronou Condenser Market Size

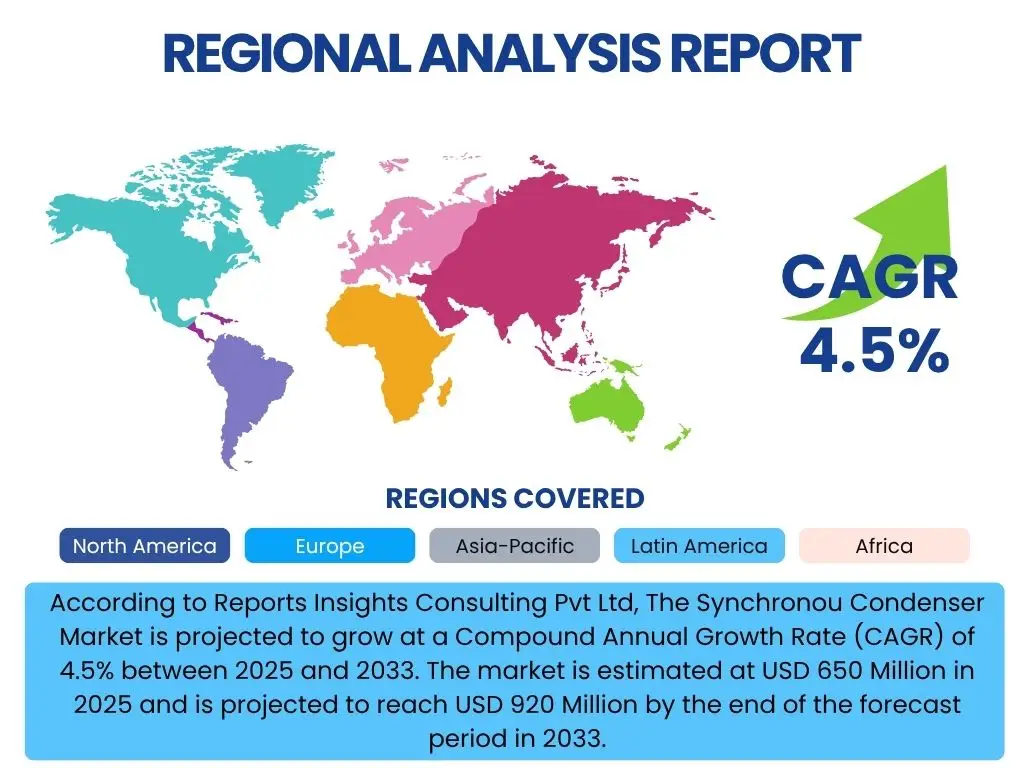

According to Reports Insights Consulting Pvt Ltd, The Synchronou Condenser Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2025 and 2033. The market is estimated at USD 650 Million in 2025 and is projected to reach USD 920 Million by the end of the forecast period in 2033.

Key Synchronou Condenser Market Trends & Insights

The synchronous condenser market is currently experiencing significant shifts driven by the global energy transition and increasing demands for grid stability. A primary trend involves the intensified integration of renewable energy sources, such as solar and wind power, which inherently lack the synchronous inertia and reactive power capabilities of traditional fossil fuel-based generation. This deficiency necessitates solutions like synchronous condensers to maintain grid frequency, voltage stability, and short-circuit strength, ensuring reliable power delivery.

Another crucial trend is the widespread modernization of aging grid infrastructure across developed economies. As grids become more complex and decentralized, there is a growing imperative to enhance their resilience and adaptability. Synchronous condensers play a vital role in providing the foundational grid support required for these advanced grid architectures, including smart grids and microgrids. Furthermore, the increasing focus on decarbonization and the decommissioning of conventional power plants underscore the sustained demand for synchronous condensers as essential tools for grid operators worldwide.

The market also observes a trend towards larger capacity units and the development of hybrid solutions that combine synchronous condensers with other grid stabilization technologies, such as STATCOMs (Static Synchronous Compensators) or battery energy storage systems. These integrated solutions offer enhanced flexibility and performance, catering to diverse and evolving grid requirements. The geographical expansion of grid interconnections, particularly in regions aiming to enhance energy security and cross-border power transfer capabilities, further contributes to the market's positive trajectory, creating new opportunities for synchronous condenser deployment.

- Increased integration of intermittent renewable energy sources into the grid.

- Rising demand for grid stability and voltage support in modern power systems.

- Modernization and expansion of aging transmission and distribution infrastructure.

- Decentralization of power generation and the growth of distributed energy resources.

- Development of larger capacity and more efficient synchronous condenser units.

- Emphasis on energy transition and decommissioning of conventional thermal power plants.

- Emergence of hybrid grid stabilization solutions combining synchronous condensers with other technologies.

AI Impact Analysis on Synchronou Condenser

The integration of Artificial Intelligence (AI) is set to significantly influence the synchronous condenser market, primarily by enhancing operational efficiency, predictive maintenance capabilities, and overall grid management. Users frequently inquire about how AI can optimize the performance of these critical assets, particularly in dynamic grid environments. AI algorithms can analyze vast amounts of real-time data from synchronous condensers, including vibration, temperature, voltage, and current readings, to predict potential failures long before they occur, thereby reducing unplanned downtime and optimizing maintenance schedules. This shift from reactive to proactive maintenance minimizes operational costs and extends the lifespan of the equipment.

Furthermore, AI-driven solutions are expected to revolutionize the control and optimization of synchronous condensers. By leveraging machine learning, grid operators can more accurately forecast reactive power demand and voltage fluctuations, allowing synchronous condensers to respond precisely and rapidly to maintain grid stability. This intelligent control can lead to more efficient utilization of the condensers' capabilities, improving overall grid resilience and power quality, especially as grids become more complex with bidirectional power flows and distributed generation. The application of AI also extends to advanced analytics for site selection and system design, ensuring optimal deployment for future grid requirements.

The role of AI is also anticipated in enhancing the cybersecurity of synchronous condenser systems, safeguarding against potential digital threats to critical infrastructure. As these systems become more connected, AI can detect anomalous behaviors that might indicate a cyberattack, enabling quicker responses and mitigation. Moreover, AI can support the integration of synchronous condensers into broader smart grid frameworks, facilitating seamless communication and coordination with other grid assets. This holistic approach, driven by AI, will contribute to a more autonomous, resilient, and optimized electrical grid, where synchronous condensers play an even more intelligent and responsive role.

- Predictive maintenance and fault detection through AI-driven analytics.

- Optimized reactive power control and voltage support using machine learning algorithms.

- Enhanced operational efficiency and reduced unplanned downtime.

- Improved grid resilience and stability through AI-assisted real-time data analysis.

- Automated performance monitoring and anomaly detection for proactive intervention.

- Integration into smart grid systems for intelligent coordination with other assets.

- Cybersecurity enhancements through AI-powered threat detection and response.

Key Takeaways Synchronou Condenser Market Size & Forecast

The synchronous condenser market is poised for steady growth through 2033, driven by the increasing need for robust grid stability in the face of evolving energy landscapes. A key takeaway is the foundational role synchronous condensers play in supporting grids that are transitioning away from conventional, inertia-rich power generation towards variable renewable energy sources. This transition mandates reliable sources of inertia and reactive power, making synchronous condensers indispensable for maintaining grid frequency and voltage within acceptable limits and ensuring overall system resilience. The forecast highlights a sustained demand for these assets, emphasizing their critical contribution to modern power systems.

Another significant insight is the market's resilience despite the emergence of alternative grid support technologies like STATCOMs. While these alternatives offer flexibility, synchronous condensers continue to be preferred for their unique ability to provide rotational inertia, which is crucial for handling large disturbances and ensuring short-circuit strength. This inherent capability positions synchronous condensers as a complementary, rather than merely competitive, solution within the broader spectrum of grid stabilization technologies. The market's growth is therefore not solely dependent on new installations but also on the retrofitting of existing infrastructure and strategic deployments in regions undergoing rapid grid expansion and modernization.

The projected financial growth reflects the global investment in grid infrastructure upgrades and the commitment to integrating higher penetrations of renewable energy. This includes both developed regions, which are modernizing aging grids, and developing economies, which are building out new, resilient power networks. The sustained CAGR indicates a healthy market outlook, underpinned by technological advancements that enhance the efficiency and operational flexibility of synchronous condensers. Ultimately, the market forecast underscores the strategic importance of synchronous condensers as a cornerstone technology for enabling a stable and sustainable future energy system.

- The synchronous condenser market demonstrates consistent growth, driven by grid modernization.

- Essential for maintaining grid stability and inertia in systems with high renewable energy penetration.

- Provides critical reactive power compensation and short-circuit strength.

- Sustained demand observed across developed and emerging economies.

- Technological advancements are enhancing efficiency and operational flexibility.

- Complements other grid stabilization technologies rather than being fully replaced.

Synchronou Condenser Market Drivers Analysis

The synchronous condenser market is significantly influenced by several key drivers that stem from global energy transitions and evolving grid requirements. The rapid expansion of renewable energy capacity, particularly wind and solar power, is a primary catalyst. These intermittent sources inherently lack the inertia provided by traditional synchronous generators, leading to increased demand for synchronous condensers to stabilize grid frequency and provide voltage support. Grid operators are increasingly reliant on these devices to ensure reliable operation amidst the variability introduced by renewables, thereby maintaining power quality and preventing blackouts.

Another major driver is the ongoing modernization and expansion of aging grid infrastructure worldwide. Many developed nations possess power grids built decades ago, which are now struggling to cope with increased power demand, bidirectional power flows, and the integration of distributed energy resources. Synchronous condensers offer a cost-effective solution for enhancing the stability, robustness, and fault-ride-through capabilities of these legacy grids. Additionally, the increasing demand for electricity globally, fueled by industrialization, urbanization, and digitalization, necessitates robust grid infrastructure, creating a sustained need for power quality solutions like synchronous condensers.

The market also benefits from the rising focus on energy security and the development of cross-border grid interconnections. As countries seek to diversify energy sources and enhance resilience against supply disruptions, integrating national grids requires strong synchronous support at interconnection points. Synchronous condensers facilitate smooth power transfer and prevent cascading failures across interconnected systems. Furthermore, regulatory frameworks and incentives promoting grid stability and renewable energy integration often indirectly stimulate the adoption of synchronous condensers, reinforcing their market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Renewable Energy Integration | +1.5% | Global, particularly Europe, North America, APAC | Long-term (2025-2033) |

| Grid Modernization & Stability Needs | +1.2% | North America, Europe, China, India | Medium to Long-term (2025-2033) |

| Aging Power Infrastructure | +0.8% | Developed Economies (North America, Europe, Japan) | Medium-term (2025-2029) |

| Increasing Global Electricity Demand | +0.5% | Asia Pacific, Africa, Latin America | Long-term (2025-2033) |

| Cross-border Grid Interconnections | +0.3% | Europe, Southeast Asia, South America | Medium-term (2027-2033) |

Synchronou Condenser Market Restraints Analysis

Despite the positive growth trajectory, the synchronous condenser market faces certain restraints that could temper its expansion. One significant challenge is the high upfront capital investment required for the procurement, installation, and commissioning of synchronous condenser units. These systems involve substantial costs for large rotating machinery, civil works, and associated electrical infrastructure, which can be a deterrent for utilities and independent power producers, especially in regions with limited financial resources or alternative investment priorities. The long project timelines associated with these large-scale infrastructure developments also add to the investment hurdle, making financial planning more complex for stakeholders.

The increasing adoption of alternative grid stabilization technologies, such as Static Synchronous Compensators (STATCOMs) and other Flexible AC Transmission System (FACTS) devices, poses another restraint. While synchronous condensers offer unique benefits like inertia and short-circuit contribution, STATCOMs provide faster response times and compact footprints, making them attractive for certain applications, especially where land availability is a concern or where very rapid reactive power compensation is the primary requirement. The continuous technological advancements in these alternative solutions can potentially divert investment away from synchronous condensers in specific scenarios, creating a competitive landscape.

Furthermore, the physical footprint and land requirements for synchronous condenser installations can be a constraint, particularly in densely populated urban areas or regions with high land costs. These large rotating machines require significant space for the units themselves, as well as for ancillary equipment, cooling systems, and maintenance access. Environmental considerations, such as noise pollution from the rotating machinery and the potential need for extensive cooling systems, can also introduce regulatory hurdles and public resistance, further delaying or preventing projects. The need for specialized civil engineering and construction further complicates deployment in challenging geographical areas.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Upfront Capital Investment | -1.0% | Global, particularly developing economies | Medium to Long-term (2025-2033) |

| Availability of Alternative Technologies (e.g., STATCOMs) | -0.7% | Global | Medium to Long-term (2025-2033) |

| Large Footprint and Land Requirements | -0.4% | Densely Populated Urban Areas, Europe, parts of Asia | Long-term (2028-2033) |

| Environmental and Permitting Challenges | -0.2% | Developed Countries with Strict Regulations | Medium-term (2025-2030) |

Synchronou Condenser Market Opportunities Analysis

Despite existing restraints, the synchronous condenser market is rich with opportunities, particularly driven by evolving energy landscapes and technological advancements. One significant opportunity lies in emerging economies, where rapid industrialization and urbanization are fueling substantial growth in electricity demand. Many of these regions are simultaneously investing in grid expansion and modernization, often bypassing older generation technologies in favor of modern, efficient systems. Synchronous condensers can provide the essential grid foundation in these burgeoning power systems, ensuring stability as new renewable and conventional generation assets come online, offering a greenfield market for new installations.

Another promising avenue is the increasing integration of energy storage systems, especially large-scale battery energy storage, into the grid. While storage systems can provide rapid reactive power and frequency response, their interaction with the grid can sometimes benefit from the inertia provided by synchronous condensers. Hybrid solutions, combining synchronous condensers with battery storage, could offer a comprehensive approach to grid stability, leveraging the strengths of both technologies. This creates opportunities for innovation in system design and new product offerings that cater to a more dynamic and flexible grid architecture, particularly in regions aiming for high renewable energy penetration.

The opportunity for retrofitting and upgrading existing power plants and industrial facilities also presents a substantial market segment. As older thermal power plants are decommissioned or repurposed, their connection points to the grid can be utilized for synchronous condenser installations, avoiding the need for new substation development. This is particularly relevant in developed markets where coal or nuclear plants are being phased out. Furthermore, the push towards smart grids and digital transformation offers new functionalities for synchronous condensers, allowing for more intelligent control, remote monitoring, and integration into advanced grid management systems. This digital integration opens doors for value-added services and enhanced operational efficiency, extending the lifecycle and utility of these assets.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Grid Development in Emerging Economies | +1.0% | Asia Pacific (India, Southeast Asia), Africa, Latin America | Long-term (2025-2033) |

| Integration with Energy Storage Systems | +0.8% | Global, particularly North America, Europe | Long-term (2028-2033) |

| Retrofitting & Decommissioning of Old Power Plants | +0.6% | Developed Economies (Europe, North America) | Medium-term (2025-2030) |

| Advancements in Smart Grid Technologies | +0.5% | Global | Medium to Long-term (2026-2033) |

| Increased Cross-Sector Industrial Demand | +0.3% | Heavy Industries (Steel, Mining, Chemical) | Medium-term (2025-2030) |

Synchronou Condenser Market Challenges Impact Analysis

The synchronous condenser market faces several challenges that necessitate strategic approaches from manufacturers and grid operators. One primary challenge is the complexity associated with the installation, commissioning, and long-term maintenance of these large, rotating electrical machines. These processes require highly specialized engineering expertise and skilled labor, which can be scarce in certain regions. The precision involved in balancing and aligning large rotors, coupled with the intricate electrical connections, demands significant technical proficiency, contributing to higher project risks and potentially longer deployment times. Ongoing maintenance, including bearing lubrication, stator winding inspection, and cooling system management, adds to operational complexities and costs throughout the asset's lifecycle.

Another significant challenge pertains to regulatory and policy uncertainties, particularly concerning grid code requirements for inertia and reactive power support. As energy policies evolve to promote decarbonization and renewable energy, grid codes are frequently updated, sometimes creating ambiguity for investors and project developers regarding the specific technical specifications and contributions expected from synchronous condensers. Inconsistent or evolving regulatory landscapes across different countries can impede market growth by increasing investment risks and requiring adaptive designs. Additionally, the lengthy approval processes for large infrastructure projects can further delay the deployment of synchronous condensers, impacting project feasibility and timelines.

Furthermore, the global supply chain for large electrical machinery components can be prone to disruptions, posing a challenge for timely project delivery. Dependencies on specialized materials, components, and manufacturing capabilities from a limited number of global suppliers can lead to delays, increased costs, and vulnerabilities in the project lifecycle. Geopolitical events, trade policies, and natural disasters can exacerbate these supply chain issues, making it difficult for manufacturers to meet demand and for operators to complete installations on schedule. Attracting and retaining a skilled workforce capable of designing, installing, and maintaining these complex systems also remains a persistent challenge, particularly as the demand for such expertise grows globally.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex Installation & Maintenance Requirements | -0.6% | Global, particularly in remote areas | Medium-term (2025-2030) |

| Regulatory & Policy Uncertainties | -0.5% | Varies by Region (e.g., EU, North America, APAC) | Medium-term (2025-2030) |

| Skilled Workforce Shortage | -0.4% | Global | Long-term (2025-2033) |

| Supply Chain Disruptions | -0.3% | Global | Short to Medium-term (2025-2027) |

| Cost Competitiveness against Alternatives | -0.2% | Global | Medium-term (2025-2030) |

Synchronou Condenser Market - Updated Report Scope

This report provides a comprehensive analysis of the Synchronous Condenser Market, covering historical data from 2019 to 2023, current market estimates for 2024, and detailed forecasts spanning 2025 to 2033. The study meticulously examines market size, growth drivers, restraints, opportunities, and challenges affecting the industry. It includes a thorough segmentation analysis by various parameters, offering granular insights into market dynamics across different types, reactive power capacities, applications, and end-use sectors. Furthermore, the report delves into regional market trends, highlighting key growth areas and competitive landscapes. A dedicated section profiles leading market players, assessing their strategies, product portfolios, and market positions. The scope also encompasses the impact of emerging technologies like Artificial Intelligence on market evolution and future outlook. The report aims to furnish stakeholders with actionable intelligence for strategic decision-making in the evolving power infrastructure domain.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 650 Million |

| Market Forecast in 2033 | USD 920 Million |

| Growth Rate | 4.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | GE, Siemens Energy, ABB, Mitsubishi Electric, Toshiba, Eaton, Hitachi Energy, Hyundai Electric, Fuji Electric, WEG S.A., Ansaldo Energia, Brush Electrical Machines, Bharat Heavy Electricals Limited (BHEL), Shanghai Electric, Xian Electric Engineering Co. Ltd., Shandong Power Equipment, Ingeteam, ZTT, Crompton Greaves |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Synchronous Condenser Market is comprehensively segmented to provide granular insights into its diverse applications and technological specifications. This segmentation allows for a detailed analysis of market dynamics, identifying key growth areas and niche opportunities across different product types, power capacities, end-use applications, and geographical regions. Understanding these segments is crucial for stakeholders to tailor their strategies, product development, and market penetration efforts to specific industry requirements and emerging trends.

By categorizing the market based on the type of cooling system, the report distinguishes between hydrogen-cooled, air-cooled, and water-cooled synchronous condensers. Each cooling method offers distinct advantages in terms of efficiency, footprint, and maintenance, catering to varying operational environments and power ratings. The segmentation by reactive power capacity provides insights into the demand for smaller units (Less than 100 MVAr), medium-sized units (100-200 MVAr), and large-scale installations (More than 200 MVAr), reflecting the diverse needs for grid support from local distribution networks to high-voltage transmission systems. This allows for a precise understanding of where the bulk of investment is occurring and which capacity ranges are experiencing the highest growth.

Further segmentation by application highlights the primary functions synchronous condensers serve, including grid stability, reactive power compensation, voltage control, and frequency regulation. While all these functions contribute to overall grid health, the relative importance of each can vary by region and grid characteristics. The end-use segmentation reveals the main sectors driving demand, encompassing utility companies (power transmission and distribution), renewable power generation facilities (wind, solar farms), heavy industrial complexes, and data centers. Each end-user segment has unique requirements and purchasing behaviors, which are critical for market participants to understand for effective targeting and solution development. This multi-faceted segmentation ensures a holistic view of the market, identifying critical growth vectors and strategic imperatives across the value chain.

- By Type: Hydrogen-Cooled, Air-Cooled, Water-Cooled

- By Reactive Power: Less than 100 MVAr, 100-200 MVAr, More than 200 MVAr

- By Application: Grid Stability, Reactive Power Compensation, Voltage Control, Frequency Regulation

- By End-Use: Utility, Renewable Power Generation, Industrial, Data Centers

Regional Highlights

- North America: This region is a significant market for synchronous condensers, primarily driven by the ongoing modernization of aging grid infrastructure and the increasing integration of renewable energy sources, particularly wind power in the Midwest and solar in the Southwest. Utilities in the U.S. and Canada are investing heavily in grid stability solutions to maintain reliability amidst evolving generation mixes. Regulatory mandates for grid resilience and the decommissioning of conventional thermal power plants further stimulate demand for synchronous condensers to provide essential inertia and reactive power support.

- Europe: Europe represents a mature yet dynamic market, propelled by ambitious renewable energy targets and the increasing complexity of cross-border electricity trading. Countries like Germany, the UK, and Nordic nations are at the forefront of renewable energy integration, necessitating robust grid stabilization technologies. The retirement of coal and nuclear power plants across the continent creates a critical need for synchronous condensers to compensate for lost inertia and short-circuit capability, ensuring the secure operation of the interconnected European grid. Strong policy support for energy transition and grid infrastructure upgrades reinforces market growth.

- Asia Pacific (APAC): The APAC region is projected to be the fastest-growing market, characterized by rapid industrialization, urbanization, and a surging demand for electricity. Countries such as China, India, and Southeast Asian nations are undergoing massive grid expansion and investing in new power generation capacity, including both conventional and renewable sources. This rapid development creates a substantial demand for synchronous condensers to ensure grid stability, manage voltage fluctuations, and support the integration of large-scale renewable energy projects. Government initiatives to improve power quality and reduce transmission losses also contribute significantly to market expansion in this region.

- Latin America: This region is witnessing steady growth, driven by investments in renewable energy projects (hydro, wind, solar) and the need to enhance grid stability in developing economies. Countries like Brazil, Chile, and Mexico are expanding their power grids and grappling with challenges related to voltage support and reactive power management, particularly in long-distance transmission lines. As these nations strive to improve energy access and reliability, synchronous condensers play a crucial role in providing the necessary grid reinforcement.

- Middle East & Africa (MEA): The MEA region presents emerging opportunities for synchronous condensers, primarily due to ambitious infrastructure development plans, diversification of energy sources, and growing electricity demand. Countries in the Middle East are investing in modernizing their grids and integrating renewable energy alongside conventional power, while African nations are focused on expanding their power access and improving grid stability to support economic growth. Investments in large-scale industrial projects and smart city initiatives also contribute to the demand for robust grid stabilization solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Synchronou Condenser Market.- GE

- Siemens Energy

- ABB

- Mitsubishi Electric

- Toshiba

- Eaton

- Hitachi Energy

- Hyundai Electric

- Fuji Electric

- WEG S.A.

- Ansaldo Energia

- Brush Electrical Machines

- Bharat Heavy Electricals Limited (BHEL)

- Shanghai Electric

- Xian Electric Engineering Co. Ltd.

- Shandong Power Equipment

- Ingeteam

- ZTT

- Crompton Greaves

Frequently Asked Questions

What is a synchronous condenser and why is it important?

A synchronous condenser is an electrical machine designed to provide or absorb reactive power to or from an alternating current power system. It operates without mechanical load, solely for grid stabilization. Its importance lies in maintaining voltage stability, providing inertia to the grid to counteract sudden frequency changes, enhancing short-circuit strength, and improving overall power quality, which is crucial for grids with high penetration of non-synchronous renewable energy sources.

How does the growth of renewable energy impact the synchronous condenser market?

The increasing growth of renewable energy, such as wind and solar, directly boosts the synchronous condenser market. Unlike traditional generators, renewables lack inherent inertia and reactive power capabilities. Synchronous condensers compensate for this, providing the essential grid inertia, voltage support, and fault current necessary to ensure the stability and reliability of power systems increasingly dominated by intermittent renewable sources.

What are the primary applications of synchronous condensers?

The primary applications of synchronous condensers include maintaining grid voltage stability, providing dynamic reactive power compensation, contributing to grid inertia for frequency stability, increasing short-circuit capacity, and enhancing grid resilience against disturbances. They are widely used in transmission networks, at renewable energy integration points, and in large industrial facilities to ensure reliable power quality.

What are the main alternatives to synchronous condensers?

Main alternatives to synchronous condensers for reactive power compensation and voltage control include Static Synchronous Compensators (STATCOMs), Static Var Compensators (SVCs), and other Flexible AC Transmission Systems (FACTS) devices. While these alternatives offer faster response times and typically have a smaller footprint, they generally do not provide the mechanical inertia or short-circuit contribution inherent to synchronous condensers, making the latter uniquely valuable for overall grid stability.

What are the future outlook and key trends for the synchronous condenser market?

The future outlook for the synchronous condenser market is positive, driven by continued renewable energy expansion, global grid modernization initiatives, and the decommissioning of traditional power plants. Key trends include the development of larger, more efficient units, hybrid solutions combining condensers with energy storage, and the integration of AI for predictive maintenance and optimized control. The market will see sustained demand for grid stability as energy transitions accelerate worldwide.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted