Static Synchronou Compensator Market

Static Synchronou Compensator Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705212 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

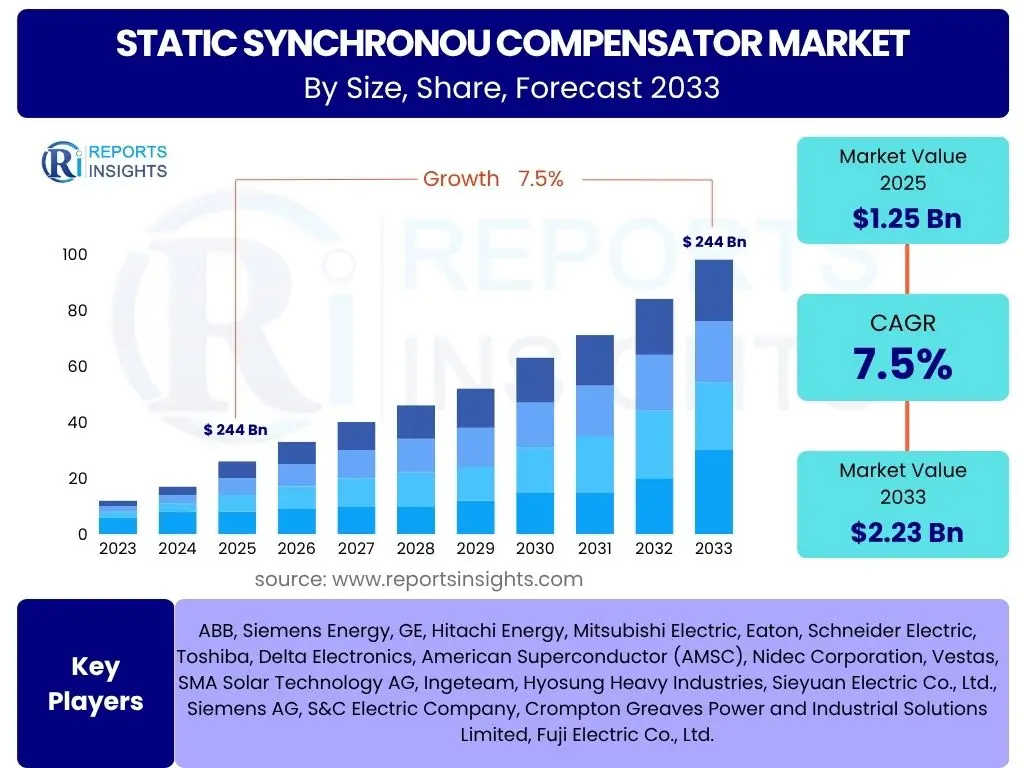

Static Synchronous Compensator Market Size

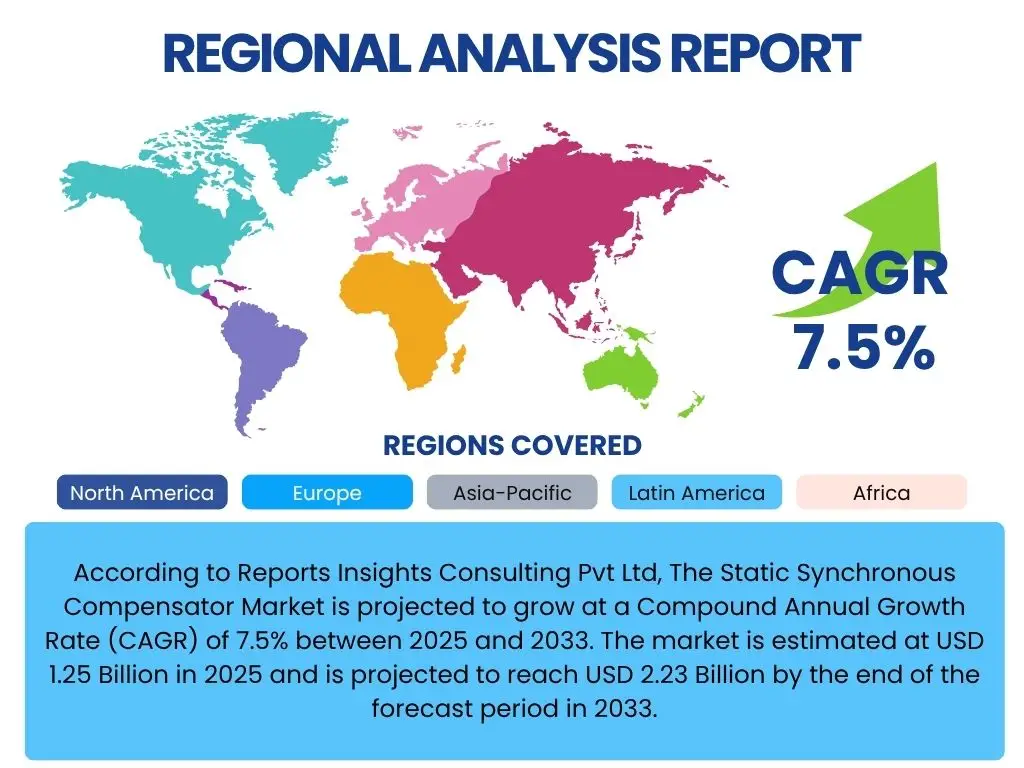

According to Reports Insights Consulting Pvt Ltd, The Static Synchronous Compensator Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2025 and 2033. The market is estimated at USD 1.25 Billion in 2025 and is projected to reach USD 2.23 Billion by the end of the forecast period in 2033.

Key Static Synchronous Compensator Market Trends & Insights

The Static Synchronous Compensator (STATCOM) market is undergoing significant transformation, driven by global energy transitions and the imperative for robust grid infrastructure. Key trends revolve around the increasing integration of intermittent renewable energy sources, which necessitate advanced reactive power compensation solutions to maintain grid stability and power quality. The modernization of aging electrical grids across developed nations and the rapid expansion of industrial and urban infrastructure in emerging economies are also pivotal, increasing the demand for efficient and flexible voltage support systems.

Furthermore, advancements in power electronics, particularly in insulated-gate bipolar transistor (IGBT) technology, are enabling more compact, efficient, and faster-responding STATCOM units. There is a discernible shift towards intelligent grid solutions, where STATCOMs are integrated into broader smart grid architectures to facilitate real-time monitoring, control, and optimization of power flow. The emphasis on energy efficiency and reduced carbon footprints also positions STATCOMs as critical components for sustainable energy ecosystems.

- Increasing adoption in renewable energy integration, especially for solar and wind farms.

- Growing demand for enhanced grid stability and power quality in utility and industrial sectors.

- Advancements in high-power semiconductor technology leading to more efficient and compact designs.

- Expansion of smart grid infrastructure and digital substations integrating advanced control capabilities.

- Decentralization of power generation necessitating localized reactive power support.

- Rising focus on energy efficiency and reduction of transmission losses.

AI Impact Analysis on Static Synchronous Compensator

Artificial intelligence (AI) is set to profoundly influence the design, operation, and maintenance of Static Synchronous Compensators (STATCOMs), transforming them into more intelligent and adaptive grid assets. Users frequently inquire about how AI can optimize STATCOM performance, enhance grid resilience, and facilitate predictive maintenance strategies. The integration of AI algorithms enables STATCOMs to move beyond traditional reactive power compensation to proactive grid management, anticipating grid disturbances and dynamically adjusting their output for optimal stability.

AI-driven analytics can process vast amounts of real-time grid data, identifying patterns and anomalies that might lead to system instability, thereby enabling STATCOMs to respond with unprecedented speed and precision. This intelligence extends to predictive maintenance, where AI algorithms forecast potential equipment failures, allowing for timely interventions that reduce downtime and operational costs. Moreover, AI can optimize energy management across the grid, ensuring that STATCOMs operate at peak efficiency, contributing to overall grid reliability and sustainability.

- Predictive maintenance and fault detection enabled by AI for reduced downtime and operational costs.

- Optimized real-time control and response for dynamic grid conditions, enhancing stability and power quality.

- Enhanced grid resilience through intelligent algorithms that anticipate and mitigate disturbances.

- Data-driven performance analysis and efficiency improvements, leading to optimized energy management.

- Seamless integration with wider energy management systems and smart grid platforms for holistic control.

- Automated diagnostics and self-healing capabilities reducing human intervention.

Key Takeaways Static Synchronous Compensator Market Size & Forecast

The Static Synchronous Compensator market is poised for robust expansion, reflecting critical global trends in energy infrastructure development and sustainability. A key insight is the significant role STATCOMs play in supporting the transition to renewable energy by mitigating grid instability caused by intermittent generation sources. The projected substantial growth indicates a strong market demand driven by the imperative to modernize existing grids and construct resilient new power transmission and distribution networks, especially in rapidly industrializing regions.

Furthermore, the market's trajectory is reinforced by ongoing technological innovations in power electronics and the increasing integration of digital solutions, making STATCOMs more efficient, adaptable, and cost-effective. Stakeholders across utilities, industrial sectors, and renewable energy developers recognize STATCOMs as indispensable for ensuring power quality and grid reliability, leading to sustained investment. This positive outlook underscores a fertile ground for manufacturers, service providers, and technology developers in the power electronics and grid infrastructure domains.

- Robust market expansion projected, driven by global energy demand and grid modernization efforts.

- Critical role of STATCOMs in successful integration of intermittent renewable energy sources.

- Increasing investment in global grid infrastructure upgrades, particularly in developing economies.

- Technological advancements in power electronics significantly enhancing STATCOM capabilities and efficiency.

- Positive long-term outlook for market stakeholders due to growing demand for power quality and stability.

- Emerging opportunities in industrial applications and smart grid deployments.

Static Synchronous Compensator Market Drivers Analysis

The Static Synchronous Compensator market is significantly driven by the global energy transition, which necessitates the integration of a growing share of renewable energy sources into existing grids. As solar and wind power generation expands, the intermittent nature of these sources introduces voltage fluctuations and power quality issues, which STATCOMs effectively mitigate. This fundamental shift in energy generation paradigms creates a sustained demand for advanced reactive power compensation solutions to maintain grid stability and reliability.

Another major driver is the escalating demand for power quality and grid stability across various sectors, including utilities, heavy industries, and commercial establishments. Modern industrial processes and sensitive electronic equipment require stable and clean power, making STATCOMs crucial for preventing costly disruptions and equipment damage. Additionally, the ongoing efforts to modernize aging electrical infrastructure in developed countries and the rapid expansion of power grids in emerging economies further fuel the adoption of STATCOMs to enhance network resilience and efficiency.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Integration of Renewable Energy Sources | +2.5% | Global, particularly Europe, Asia Pacific, North America | Short to Medium-term |

| Growing Demand for Grid Stability and Power Quality | +2.0% | Global | Ongoing |

| Modernization of Aging Grid Infrastructure | +1.5% | North America, Europe, parts of Asia Pacific | Medium to Long-term |

| Industrialization and Urbanization in Developing Economies | +1.0% | Asia Pacific, Middle East & Africa, Latin America | Medium-term |

| Technological Advancements in Power Electronics | +0.5% | Global | Ongoing |

Static Synchronous Compensator Market Restraints Analysis

Despite the strong growth drivers, the Static Synchronous Compensator market faces certain restraints that could impede its full potential. A primary challenge is the high initial capital investment required for the procurement and installation of STATCOM units. These systems involve sophisticated power electronics and complex control mechanisms, making them significantly more expensive than traditional reactive power compensation devices. This high upfront cost can be a deterrent for smaller utilities or industrial players with limited budgets, potentially slowing adoption in cost-sensitive markets or projects.

Another restraint is the complexity associated with the design, integration, and maintenance of STATCOM systems. Their optimal operation requires specialized expertise in power electronics, control systems, and grid dynamics, which may not be readily available in all regions. This complexity can lead to longer project implementation times and higher operational expenditures due to the need for highly skilled personnel. Furthermore, the lack of standardized regulations or incentive programs in some emerging markets can create uncertainty and hinder widespread deployment, delaying market penetration despite evident technical benefits.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment | -1.0% | Global, particularly developing economies | Short to Medium-term |

| Complex Design and Integration Challenges | -0.5% | Global | Short-term |

| Lack of Standardized Regulations and Incentives in Some Regions | -0.3% | Developing economies | Medium-term |

| Competition from Conventional SVC and Other Compensation Technologies | -0.2% | Global | Ongoing |

Static Synchronous Compensator Market Opportunities Analysis

Significant opportunities exist within the Static Synchronous Compensator market, particularly in the ongoing global expansion of smart grid initiatives. As power grids evolve into more interconnected, intelligent, and resilient systems, STATCOMs will play a pivotal role in providing dynamic and precise reactive power compensation, enabling advanced functionalities like demand-side management and microgrid integration. This technological evolution opens new avenues for STATCOM deployment beyond traditional utility applications, extending into sophisticated industrial and commercial power management solutions.

The increasing focus on grid hardening and resilience against extreme weather events and cyber threats also presents a strong opportunity. STATCOMs can contribute to system stability during disturbances and aid in faster recovery, making them integral to future grid security strategies. Furthermore, the development of smaller, modular, and more flexible STATCOM units, driven by continuous innovation in power electronics, will broaden their applicability to distributed generation sites and localized power quality issues, unlocking market potential in diverse geographical and application segments, especially in emerging economies with rapidly growing industrial and urban loads.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Smart Grid Initiatives and Digitalization | +1.5% | Global, particularly developed regions | Medium to Long-term |

| Growing Industrial and Commercial Demand for Power Quality | +1.0% | Asia Pacific, North America, Europe | Short to Medium-term |

| Development of Advanced Power Electronics and Modular Solutions | +0.8% | Global | Medium to Long-term |

| Investments in Grid Hardening and Resiliency Against Disruptions | +0.7% | North America, Europe | Medium-term |

Static Synchronous Compensator Market Challenges Impact Analysis

The Static Synchronous Compensator market faces several challenges that require strategic navigation by industry players. One significant challenge is the rapid pace of technological advancements, which can lead to rapid obsolescence of existing systems if manufacturers do not continuously innovate. Keeping up with evolving power electronics, control algorithms, and software integration demands substantial research and development investment, posing a hurdle for smaller companies or those with limited R&D budgets. This constant need for upgrades influences capital expenditure and product lifecycle management.

Another crucial challenge pertains to cybersecurity risks associated with integrating STATCOMs into increasingly digitized grid infrastructures. As these devices become more interconnected and controlled remotely, they become potential targets for cyberattacks, which could compromise grid stability and national security. Ensuring robust cybersecurity measures and developing resilient systems is paramount but adds to the complexity and cost of deployment. Furthermore, the global shortage of skilled personnel proficient in power electronics, smart grid technologies, and STATCOM operations presents a significant talent gap, impacting deployment efficiency and long-term maintenance capabilities across various regions.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Advancements and Potential Obsolescence | -0.6% | Global | Ongoing |

| Cybersecurity Risks to Grid Infrastructure | -0.5% | Global | Ongoing |

| Skilled Workforce Shortage in Power Electronics and Smart Grid Technologies | -0.4% | Global | Short to Medium-term |

| Intense Price Competition from Established and Emerging Players | -0.3% | Global | Ongoing |

Static Synchronous Compensator Market - Updated Report Scope

This report provides a comprehensive analysis of the Static Synchronous Compensator market, detailing its current size, historical performance, and future growth projections through 2033. It meticulously examines key market trends, drivers, restraints, opportunities, and challenges influencing market dynamics. The scope extends to an in-depth segmentation analysis across various parameters, offering detailed insights into market sub-segments. Furthermore, the report presents a thorough regional analysis and profiles leading companies, offering a holistic view of the competitive landscape and strategic insights for stakeholders. The aim is to equip decision-makers with actionable intelligence for strategic planning and investment in this rapidly evolving sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.25 Billion |

| Market Forecast in 2033 | USD 2.23 Billion |

| Growth Rate | 7.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ABB, Siemens Energy, GE, Hitachi Energy, Mitsubishi Electric, Eaton, Schneider Electric, Toshiba, Delta Electronics, American Superconductor (AMSC), Nidec Corporation, Vestas, SMA Solar Technology AG, Ingeteam, Hyosung Heavy Industries, Sieyuan Electric Co., Ltd., Siemens AG, S&C Electric Company, Crompton Greaves Power and Industrial Solutions Limited, Fuji Electric Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Static Synchronous Compensator market is extensively segmented to provide granular insights into its diverse applications and technological manifestations. This segmentation allows for a precise understanding of market dynamics across different product types, key components, operational voltage levels, and end-use industries. Analyzing these segments is crucial for identifying specific growth pockets, emerging technological preferences, and regional adoption patterns, enabling stakeholders to tailor their strategies and investments effectively.

The market is primarily segmented by type, differentiating between Voltage Source Converter (VSC) based and Current Source Converter (CSC) based STATCOMs, with VSC-based systems generally dominating due to their superior performance characteristics. Further segmentation by component highlights the critical elements such as power modules, control systems, and cooling systems, essential for the functionality and efficiency of STATCOM units. Voltage level segmentation, ranging from low to high voltage, reflects the varied applications from localized industrial power quality to large-scale grid stability. Application and end-use segmentations delineate the demand from renewable energy integration, heavy industries, and utility transmission and distribution networks, offering a comprehensive view of the market's breadth.

- By Type: Voltage Source Converter (VSC) Based, Current Source Converter (CSC) Based.

- By Component: Power Module (IGBT, GTO), Control System, Capacitor Bank, Cooling System, Harmonic Filter, Transformer.

- By Voltage Level: Low Voltage STATCOM (Below 11kV), Medium Voltage STATCOM (11kV-132kV), High Voltage STATCOM (Above 132kV).

- By Application: Renewable Energy Integration (Wind Farms, Solar Farms), Industrial Applications (Electric Arc Furnaces, Rolling Mills), Utility Applications (Transmission and Distribution Grids), Oil & Gas, Mining, Pulp & Paper.

- By End Use: Power Generation, Transmission & Distribution, Industrial, Commercial.

Regional Highlights

- North America: This region is characterized by significant investments in grid modernization and the integration of renewable energy sources. The aging infrastructure in countries like the United States and Canada necessitates advanced power quality solutions, driving the adoption of STATCOMs for grid stability and reliability. Government initiatives and incentives for renewable energy projects further bolster market growth.

- Europe: Europe stands as a frontrunner in renewable energy adoption, with stringent regulations supporting grid stability and carbon reduction. Countries such as Germany, the UK, and Spain are heavily investing in offshore wind and solar projects, creating a robust demand for STATCOMs to manage grid fluctuations. The emphasis on smart grid development and cross-border energy trading also contributes to the market's expansion.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing market, propelled by rapid industrialization, urbanization, and burgeoning energy demand in countries like China, India, and Southeast Asian nations. Massive infrastructure development, coupled with ambitious renewable energy targets and the expansion of heavy industries, drives significant STATCOM deployments for grid reinforcement and power quality improvement.

- Latin America: This region is experiencing a surge in renewable energy investments, particularly in Brazil, Chile, and Mexico. The development of new transmission lines and the need to stabilize power grids in the face of increasing industrial loads are key factors driving the adoption of STATCOMs. The market is also supported by efforts to improve energy access and reliability.

- Middle East & Africa (MEA): MEA is witnessing substantial investments in power generation and transmission infrastructure, driven by economic diversification and growing populations. Countries in the Gulf Cooperation Council (GCC) are investing heavily in utility-scale renewable energy projects and industrial complexes, creating a strong demand for STATCOMs to ensure grid stability and efficient power delivery.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Static Synchronous Compensator Market.- ABB

- Siemens Energy

- GE

- Hitachi Energy

- Mitsubishi Electric

- Eaton

- Schneider Electric

- Toshiba

- Delta Electronics

- American Superconductor (AMSC)

- Nidec Corporation

- Vestas

- SMA Solar Technology AG

- Ingeteam

- Hyosung Heavy Industries

- Sieyuan Electric Co., Ltd.

- Siemens AG

- S&C Electric Company

- Crompton Greaves Power and Industrial Solutions Limited

- Fuji Electric Co., Ltd.

Frequently Asked Questions

What is a Static Synchronous Compensator (STATCOM)?

A Static Synchronous Compensator (STATCOM) is a shunt-connected flexible alternating current transmission system (FACTS) device that rapidly generates or absorbs reactive power to regulate bus voltage, improve power factor, and enhance grid stability. It is particularly vital in modern power systems integrating intermittent renewable energy sources.

Why is STATCOM important for renewable energy integration?

STATCOMs are crucial for renewable energy integration as they rapidly compensate for voltage fluctuations and power quality issues caused by intermittent sources like solar and wind power. By providing dynamic reactive power support, STATCOMs ensure stable and reliable grid operation, preventing blackouts and enhancing the overall efficiency of renewable energy assets.

What are the primary applications of STATCOMs?

Primary applications of STATCOMs include voltage stability enhancement in transmission and distribution networks, power factor correction and harmonic mitigation in industrial loads (such as electric arc furnaces and rolling mills), seamless integration of renewable energy sources, and support for critical grid infrastructure to improve overall power quality and reliability.

How does AI impact STATCOM technology?

Artificial intelligence significantly enhances STATCOM technology through predictive maintenance, enabling anticipation of equipment failures; real-time optimal control for dynamic grid conditions; advanced anomaly detection; and data-driven performance analytics. These AI applications lead to improved efficiency, reliability, and more adaptive grid responses for STATCOM systems.

What are the key growth drivers for the STATCOM market?

Key growth drivers for the STATCOM market include the increasing global adoption of renewable energy sources requiring grid stabilization, the urgent need for modernization and upgrades of aging power grid infrastructure, and rising industrial demand for superior power quality and stable voltage to protect sensitive equipment and processes.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted