Surfaced and Ground Water Monitoring Market

Surfaced and Ground Water Monitoring Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707894 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

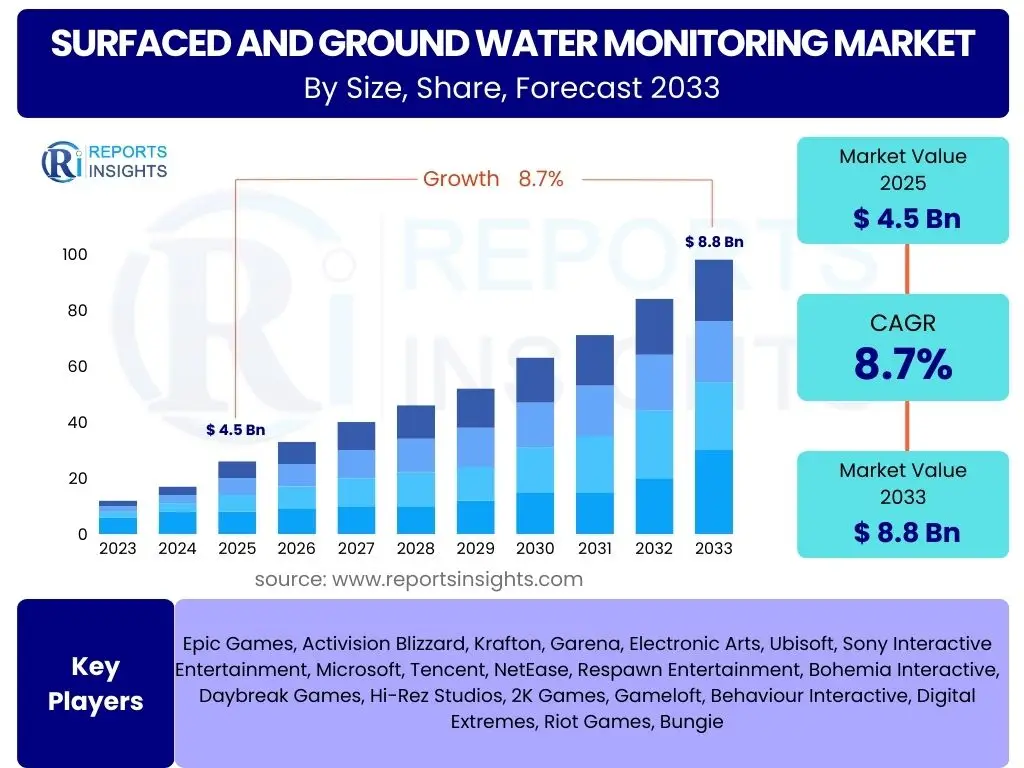

Surfaced and Ground Water Monitoring Market Size

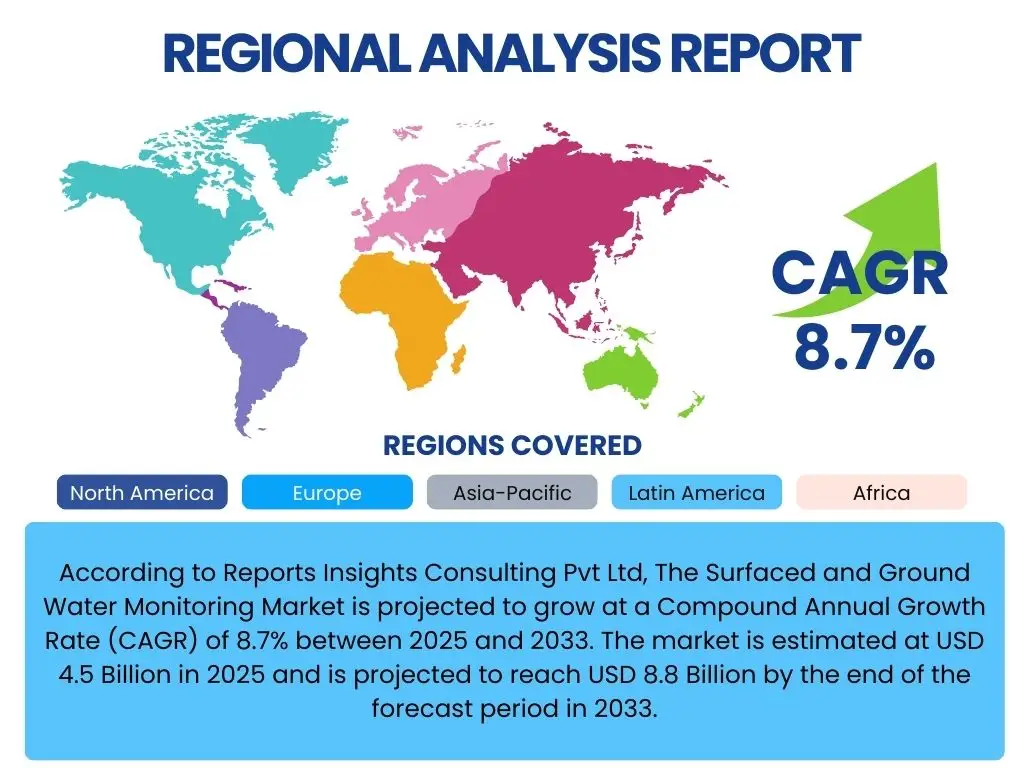

According to Reports Insights Consulting Pvt Ltd, The Surfaced and Ground Water Monitoring Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033. The market is estimated at USD 4.5 Billion in 2025 and is projected to reach USD 8.8 Billion by the end of the forecast period in 2033.

Key Surfaced and Ground Water Monitoring Market Trends & Insights

The Surfaced and Ground Water Monitoring market is experiencing significant evolution driven by escalating environmental concerns, stringent regulatory frameworks, and technological advancements. A primary trend involves the increasing adoption of real-time monitoring solutions, moving away from traditional manual sampling methods. This shift is critical for immediate detection of pollutants and rapid response to water quality degradation events, catering to the urgent need for proactive water resource management.

Furthermore, the integration of advanced sensor technologies, IoT devices, and data analytics platforms is revolutionizing how water data is collected, processed, and interpreted. These innovations enable more comprehensive and accurate data collection across vast and often remote geographical areas, providing a holistic view of water body health. The emphasis on data-driven decision-making is empowering governmental agencies, industrial operators, and environmental organizations to implement more effective conservation and pollution control strategies.

Another prominent insight is the growing demand for portable and autonomous monitoring systems. These systems are crucial for expanding monitoring capabilities into hard-to-reach locations and for applications requiring continuous, unattended operation. The miniaturization of sensors and improvements in battery life and communication technologies are key enablers of this trend, making comprehensive water quality assessment more accessible and cost-effective across various sectors.

- Shift towards real-time and continuous monitoring systems.

- Integration of IoT, AI, and advanced sensor technologies for data collection and analysis.

- Increased demand for autonomous and portable monitoring devices.

- Emphasis on data-driven decision-making for water resource management.

- Development of multi-parameter sensors for comprehensive water quality assessment.

AI Impact Analysis on Surfaced and Ground Water Monitoring

Artificial Intelligence (AI) is poised to profoundly transform the Surfaced and Ground Water Monitoring market by enhancing the efficiency, accuracy, and predictive capabilities of water quality assessment. Users are keenly interested in how AI can move beyond simple data aggregation to offer actionable insights. AI algorithms, particularly machine learning models, are being applied to analyze vast datasets from multiple sources, including sensor networks, satellite imagery, and historical records. This allows for the identification of complex patterns, anomalies, and correlations that would be imperceptible to traditional analytical methods, leading to more precise pollution source identification and early warning systems for water contamination.

A key expectation from AI integration is its capacity for predictive modeling. Instead of merely reporting current conditions, AI can forecast future water quality trends, predict pollution events, and model the impact of various environmental factors or human activities on water bodies. This predictive power is invaluable for proactive resource management, enabling authorities to implement preventative measures and optimize the allocation of treatment resources. Users also anticipate AI to automate routine monitoring tasks, thereby reducing human error and operational costs.

However, concerns exist regarding the implementation challenges of AI in this domain, including the need for high-quality, diverse training data, the complexity of model interpretation, and the ethical implications of data privacy and algorithmic bias. Despite these challenges, the overwhelming consensus is that AI will significantly improve the responsiveness and effectiveness of water monitoring programs, making them more adaptable to evolving environmental conditions and increasing demands for clean water.

- Enhanced data analysis and pattern recognition for pollution identification.

- Predictive modeling of water quality trends and contamination events.

- Automation of data collection, processing, and reporting tasks.

- Optimization of sensor placement and sampling strategies.

- Development of intelligent decision support systems for water resource managers.

Key Takeaways Surfaced and Ground Water Monitoring Market Size & Forecast

The Surfaced and Ground Water Monitoring market is set for robust growth, driven primarily by increasing global water scarcity, heightened awareness of water pollution, and the imperative for sustainable water management. A crucial takeaway is the fundamental shift towards integrated, smart monitoring systems that leverage advanced technologies to provide comprehensive and actionable data. This transition is essential for addressing the complex challenges associated with safeguarding water resources in an era of climate change and rapid industrialization.

Another significant insight is the escalating investment in infrastructure and technological innovation within the water monitoring sector. Governments, private entities, and research institutions are recognizing the long-term value of accurate water data for public health, economic stability, and ecological preservation. This investment is not only fueling market expansion but also fostering the development of more sophisticated and resilient monitoring solutions capable of operating in diverse and challenging environments.

Furthermore, the market forecast underscores the critical role of regulatory mandates and international cooperation in driving adoption. Stricter environmental protection laws and global initiatives aimed at achieving water security are compelling industries and municipalities to enhance their monitoring capabilities. The growing market size reflects a collective understanding that effective water monitoring is not merely a compliance requirement but a foundational element of sustainable development and environmental stewardship.

- Significant market growth driven by water scarcity and pollution concerns.

- Shift towards integrated, smart monitoring systems is a core growth catalyst.

- Increased investment in advanced water monitoring technologies and infrastructure.

- Regulatory frameworks and global sustainability goals are strong market drivers.

- Emphasis on real-time data for proactive management and informed decision-making.

Surfaced and Ground Water Monitoring Market Drivers Analysis

The demand for advanced surfaced and ground water monitoring solutions is fundamentally propelled by the intensifying global water crisis, characterized by increasing scarcity and degradation of water quality. Rapid population growth, industrial expansion, and agricultural intensification place immense pressure on existing water resources, necessitating continuous and accurate monitoring to ensure sustainable supply and safety. Public awareness regarding the detrimental effects of waterborne diseases and chemical contamination is also driving governmental and public efforts to improve water quality surveillance, making monitoring an indispensable tool for public health protection.

Furthermore, stringent environmental regulations and compliance standards enacted by international and national bodies are significant market drivers. These regulations often mandate regular monitoring of industrial discharges, agricultural runoffs, and urban wastewater to prevent pollution and protect aquatic ecosystems. Non-compliance can result in substantial penalties, compelling industries and municipalities to invest in robust monitoring technologies. The global push for achieving Sustainable Development Goals (SDGs), particularly SDG 6 (Clean Water and Sanitation), further reinforces the commitment to effective water resource management and, consequently, water monitoring.

Technological advancements in sensor capabilities, data analytics, and communication networks have also played a pivotal role in driving market expansion. Innovations such as multi-parameter sensors, autonomous underwater vehicles (AUVs), and remote sensing technologies offer enhanced accuracy, efficiency, and cost-effectiveness in data collection. The ability to integrate these technologies with IoT platforms and AI for real-time data processing and predictive analytics has transformed the scope and utility of water monitoring, making it more accessible and impactful across a wider range of applications.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Water Pollution and Scarcity | +2.5% | Global, particularly Asia Pacific, Africa | Long-term (2025-2033) |

| Stringent Environmental Regulations | +2.0% | North America, Europe, China, India | Medium to Long-term |

| Technological Advancements in Sensors and IoT | +1.8% | Global | Short to Medium-term |

| Growing Demand for Real-time Data | +1.5% | Developed Nations, Industrial Hubs | Medium-term |

| Public Health Concerns and Awareness | +1.2% | Global | Long-term |

Surfaced and Ground Water Monitoring Market Restraints Analysis

Despite the strong growth drivers, the Surfaced and Ground Water Monitoring market faces several significant restraints that could impede its full potential. A primary challenge is the high initial capital investment required for deploying sophisticated monitoring equipment, including advanced sensors, data loggers, communication infrastructure, and analytical software. This substantial upfront cost can be a barrier for smaller municipalities, developing countries, and resource-constrained organizations, limiting their ability to adopt comprehensive monitoring solutions despite the evident need.

Another key restraint is the complexity associated with data management and interpretation. Water monitoring systems often generate vast amounts of heterogeneous data, which requires specialized expertise to process, analyze, and translate into actionable insights. The shortage of skilled personnel capable of operating, maintaining, and effectively utilizing these advanced systems, coupled with the challenges of data integration from disparate sources, can hinder the efficient implementation and utilization of monitoring programs. This often leads to underutilization of collected data or delays in decision-making.

Furthermore, harsh environmental conditions and the remote nature of many monitoring sites present operational and maintenance challenges. Sensors can be prone to fouling, corrosion, and damage, requiring frequent calibration and replacement, which adds to operational expenditures. The reliability and longevity of equipment in extreme temperatures, high turbidity, or corrosive chemical environments remain ongoing concerns. Additionally, the fragmented nature of the water management sector, involving multiple stakeholders with varying priorities and funding mechanisms, can complicate the coordinated implementation of large-scale monitoring projects, thereby slowing market progression.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment | -1.5% | Developing Economies, Small Municipalities | Long-term |

| Complexity of Data Management and Analysis | -1.0% | Global | Medium-term |

| Lack of Skilled Personnel and Expertise | -0.8% | Global, particularly Emerging Markets | Medium to Long-term |

| Operational Challenges in Harsh Environments | -0.7% | Remote Areas, Industrial Sites | Short to Medium-term |

| Regulatory Gaps and Enforcement Weaknesses | -0.5% | Certain Developing Regions | Long-term |

Surfaced and Ground Water Monitoring Market Opportunities Analysis

The Surfaced and Ground Water Monitoring market presents significant opportunities for growth, particularly in the realm of advanced technological integration and expansion into underserved regions. The accelerating adoption of the Internet of Things (IoT) in environmental monitoring offers a substantial avenue for market players. By connecting a vast network of sensors, IoT platforms can facilitate real-time data transmission, remote monitoring, and automated alerts, thereby enhancing the efficiency and responsiveness of water quality management. The continued development of low-power, long-range communication technologies like LoRaWAN and NB-IoT further expands the possibilities for deploying monitoring solutions in remote and rural areas that traditionally lacked adequate infrastructure.

Moreover, the increasing focus on smart cities and sustainable infrastructure development globally creates a fertile ground for market expansion. As urban areas strive to optimize resource management and improve environmental quality, integrated smart water networks, which include comprehensive monitoring systems, become indispensable. This trend is particularly evident in rapidly urbanizing regions across Asia Pacific and Latin America, where new infrastructure is being designed with sustainability and smart capabilities in mind from the outset. Opportunities also lie in providing bundled solutions that combine hardware, software, and services, offering a holistic approach to water monitoring and management for end-users.

Another critical opportunity lies in the growing demand for predictive analytics and AI-driven insights. While raw data is valuable, the ability to transform this data into actionable intelligence through machine learning algorithms offers a competitive advantage. Companies that can provide advanced analytical tools for forecasting water quality changes, identifying pollution sources with greater precision, and optimizing water treatment processes will capture a larger market share. Furthermore, expanding into industrial process water monitoring and agricultural water management, beyond traditional environmental monitoring, represents a significant growth pathway, as these sectors face increasing pressure to optimize water usage and meet discharge quality standards.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration of IoT and Smart Sensor Networks | +1.8% | Global, especially Developed Countries | Short to Medium-term |

| Expansion in Smart Cities and Sustainable Infrastructure | +1.5% | Asia Pacific, North America, Europe | Medium to Long-term |

| Development of AI and Predictive Analytics Solutions | +1.2% | Global | Medium-term |

| Growth in Industrial and Agricultural Water Management | +1.0% | Emerging Economies, Industrialized Regions | Long-term |

| Public-Private Partnerships for Large Scale Projects | +0.9% | Global | Long-term |

Surfaced and Ground Water Monitoring Market Challenges Impact Analysis

The Surfaced and Ground Water Monitoring market confronts several formidable challenges that necessitate innovative solutions and strategic adaptations. A significant hurdle is the inherent difficulty in achieving comprehensive spatial and temporal coverage, particularly for groundwater resources which are often vast, deep, and difficult to access. Monitoring networks can be sparse, leading to data gaps and an incomplete understanding of water body dynamics. This challenge is compounded by the heterogeneity of water environments, requiring diverse sensor types and deployment strategies that are not always interoperable or cost-effective to implement on a broad scale.

Another critical challenge involves the management and standardization of data. With an increasing array of monitoring technologies generating data in different formats and resolutions, ensuring data quality, interoperability, and consistent reporting standards becomes complex. The absence of universally accepted protocols for data collection, storage, and exchange can hinder data sharing among stakeholders, impede comparative analysis, and complicate the development of integrated water management strategies. Furthermore, ensuring data security and privacy, especially when dealing with sensitive environmental or infrastructure data, adds another layer of complexity.

Moreover, the long-term sustainability of monitoring programs is often threatened by funding limitations and fluctuating political priorities. Establishing and maintaining a robust monitoring network requires continuous investment in equipment, personnel, and operational costs. Economic downturns or shifts in governmental focus can lead to budget cuts, compromising the effectiveness and continuity of monitoring efforts. The fragmented regulatory landscape in some regions, where responsibilities are distributed among multiple agencies with overlapping jurisdictions, can also create inefficiencies and hinder coordinated action against water pollution, thereby challenging the market's growth and impact.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Inadequate Spatial and Temporal Coverage | -1.2% | Global, especially Rural Areas | Long-term |

| Data Standardization and Interoperability Issues | -1.0% | Global | Medium-term |

| Funding Limitations and Political Instability | -0.9% | Developing Economies, Government-dependent Projects | Long-term |

| Maintenance and Calibration of Sensors in Field | -0.8% | Global | Short to Medium-term |

| Cybersecurity Risks for Connected Systems | -0.7% | Developed Nations, Critical Infrastructure | Medium-term |

Surfaced and Ground Water Monitoring Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Surfaced and Ground Water Monitoring Market, encompassing market dynamics, technological advancements, regulatory impacts, and future growth trajectories. It delivers detailed insights into market size, segmentation by technology, application, and end-use, alongside a thorough regional breakdown. The report also highlights key market trends, competitive landscape, and strategic recommendations for stakeholders navigating this evolving sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 8.8 Billion |

| Growth Rate | 8.7% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Xylem Inc., Danaher Corporation, SUEZ, Thermo Fisher Scientific Inc., Agilent Technologies, Inc., Shimadzu Corporation, Campbell Scientific, Inc., OTT Hydromet (A Xylem Brand), Aqua TROLL (A Xylem Brand), Eureka Water Probes, Horiba, Ltd., YSI, Inc. (A Xylem Brand), Teledyne Technologies Incorporated, Hach Company (A Danaher Company), Evoqua Water Technologies LLC, Seametrics, Inc., Fondriest Environmental, Inc., In-Situ Inc., RS Hydro, Solinst Canada Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Surfaced and Ground Water Monitoring market is comprehensively segmented to provide a detailed understanding of its diverse components and applications. This segmentation allows for precise analysis of market trends, drivers, and opportunities across various technological offerings, monitoring parameters, and end-user requirements. The market is broadly categorized by parameter type, product type, application, and end-use industry, reflecting the multifaceted nature of water quality assessment and management needs across global sectors.

The parameter-based segmentation highlights the different types of measurements critical for comprehensive water quality assessment, ranging from basic physical indicators to complex chemical and biological analyses. Product segmentation distinguishes between hardware components like sensors and monitoring stations, software for data processing, and associated services, illustrating the integrated solutions offered by market players. Furthermore, application and end-use industry segmentations reveal the varied demand landscape, from environmental consulting and drinking water utilities to industrial and agricultural sectors, each with unique monitoring challenges and requirements.

Understanding these segments is crucial for stakeholders to identify niche markets, develop targeted solutions, and formulate effective strategies for market penetration and growth. The granular detail provided by this segmentation assists in recognizing specific technological demands, regional preferences, and regulatory influences pertinent to each sub-market, thereby enabling more informed business decisions.

- By Parameter: Physical, Chemical, Biological

- By Type: Ground Water Monitoring, Surfaced Water Monitoring

- By Product: Portable Monitoring Devices, Fixed Monitoring Stations, Remotely Operated Vehicles (ROVs), Sensors (Multi-parameter, Single-parameter), Software and Data Management Platforms, Services (Installation, Maintenance, Calibration, Data Analytics)

- By Application: Environmental Consulting, Drinking Water Monitoring, Wastewater Monitoring, Industrial Effluent Monitoring, Agricultural Runoff Monitoring, Ecosystem Management, Research and Academia

- By End-Use Industry: Government and Utilities, Industrial (Oil and Gas, Mining, Chemical, Manufacturing), Agriculture, Environmental Organizations, Residential

Regional Highlights

- North America: A mature market with high adoption of advanced monitoring technologies driven by stringent EPA regulations, significant investment in wastewater treatment infrastructure, and a strong presence of key market players. The region focuses on smart water management and real-time data integration.

- Europe: Characterized by comprehensive environmental directives like the Water Framework Directive, fostering high demand for continuous monitoring and data reporting. Strong emphasis on R&D for innovative sensor technologies and robust water resource protection initiatives.

- Asia Pacific (APAC): Emerging as the fastest-growing region due to rapid industrialization, urbanization, increasing population, and escalating water pollution issues. Significant government investments in water infrastructure and environmental protection in countries like China and India are propelling market expansion.

- Latin America: Experiencing moderate growth with increasing awareness of water quality issues and growing investments in basic water infrastructure. Opportunities exist for affordable and robust monitoring solutions in urban and industrial areas.

- Middle East and Africa (MEA): Growing demand driven by severe water scarcity, particularly in the Middle East, leading to investments in advanced monitoring for desalination plants and agricultural efficiency. Africa faces challenges but has emerging opportunities in urban areas and for international aid projects focused on water quality.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Surfaced and Ground Water Monitoring Market.- Xylem Inc.

- Danaher Corporation

- SUEZ

- Thermo Fisher Scientific Inc.

- Agilent Technologies, Inc.

- Shimadzu Corporation

- Campbell Scientific, Inc.

- OTT Hydromet (A Xylem Brand)

- Aqua TROLL (A Xylem Brand)

- Eureka Water Probes

- Horiba, Ltd.

- YSI, Inc. (A Xylem Brand)

- Teledyne Technologies Incorporated

- Hach Company (A Danaher Company)

- Evoqua Water Technologies LLC

- Seametrics, Inc.

- Fondriest Environmental, Inc.

- In-Situ Inc.

- RS Hydro

- Solinst Canada Ltd.

Frequently Asked Questions

What is the current market size of the Surfaced and Ground Water Monitoring market?

The Surfaced and Ground Water Monitoring market is estimated at USD 4.5 Billion in 2025.

What is the projected growth rate for the Surfaced and Ground Water Monitoring market?

The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033, reaching USD 8.8 Billion by 2033.

What are the primary drivers for the Surfaced and Ground Water Monitoring market?

Key drivers include increasing water pollution and scarcity, stringent environmental regulations, and advancements in sensor and IoT technologies.

How is AI impacting water monitoring?

AI is transforming water monitoring through enhanced data analysis, predictive modeling of water quality, and automation of monitoring tasks, leading to more efficient and proactive water resource management.

Which regions are key contributors to the Surfaced and Ground Water Monitoring market?

North America and Europe are mature markets, while Asia Pacific is the fastest-growing region due to rapid industrialization and increasing environmental concerns.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted