Submarine Telecom Cable Market

Submarine Telecom Cable Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706334 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

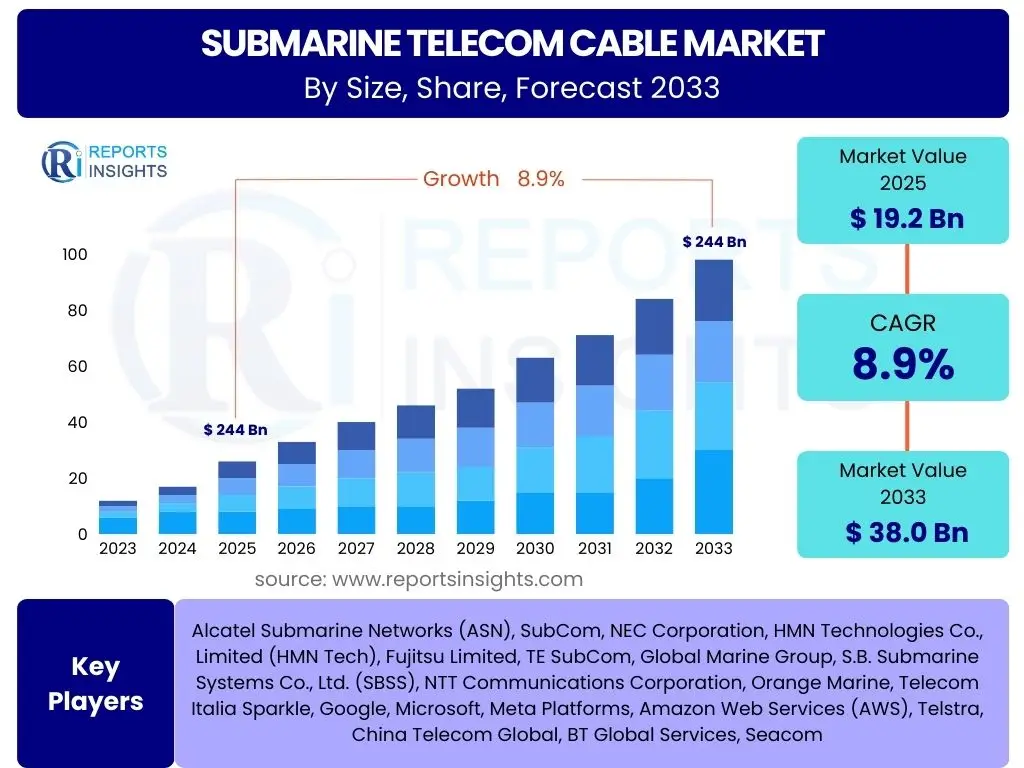

Submarine Telecom Cable Market Size

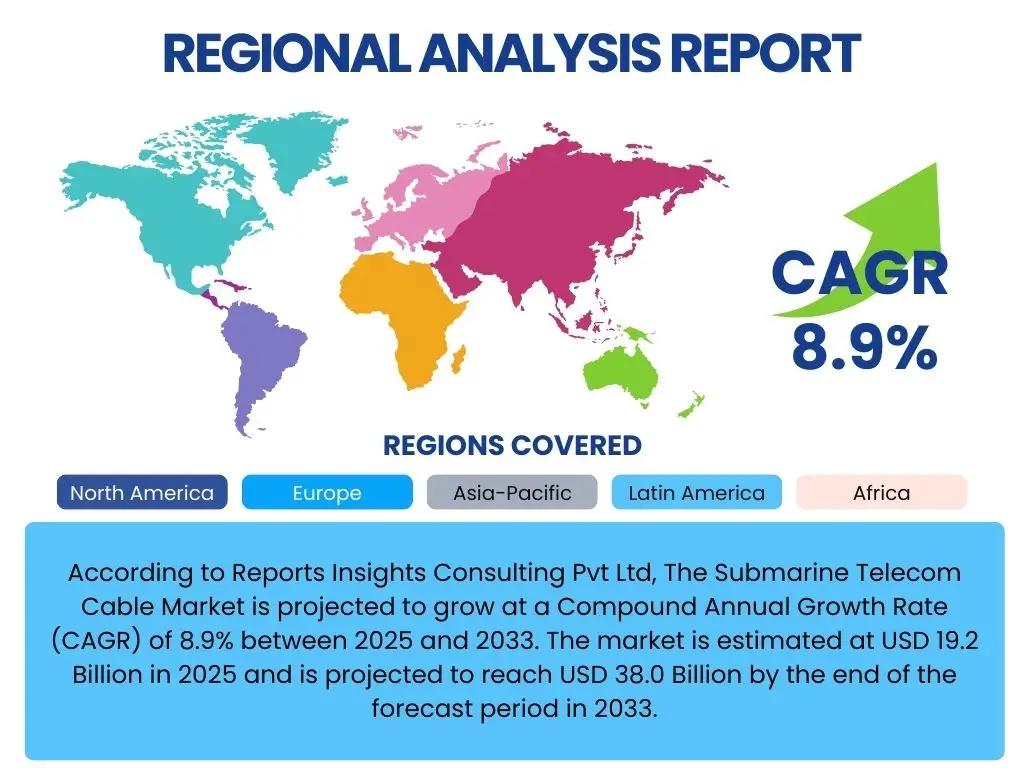

According to Reports Insights Consulting Pvt Ltd, The Submarine Telecom Cable Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2025 and 2033. The market is estimated at USD 19.2 Billion in 2025 and is projected to reach USD 38.0 Billion by the end of the forecast period in 2033.

Key Submarine Telecom Cable Market Trends & Insights

The submarine telecom cable market is currently experiencing dynamic shifts driven by an unprecedented surge in global data traffic and the strategic investments of hyperscale content providers. User inquiries frequently highlight concerns about network capacity, resilience against geopolitical events, and the technological evolution of undersea infrastructure. The market is witnessing a profound transformation from traditional carrier-centric models to one heavily influenced by the "Google-Microsoft-Meta-Amazon" (GMMA) consortium, which now finances and owns a substantial portion of new cable deployments to connect their global data centers. This shift underscores a critical trend towards private ownership and direct control over critical internet backbone infrastructure.

Technological advancements are paramount in meeting escalating demand, with innovations focusing on increasing fiber pair counts within single cables, improving optical amplification, and developing more robust and resilient cable designs. The push for higher bandwidth, lower latency, and greater network diversity is fueling investments in new routes, particularly those avoiding traditional choke points or opening up previously underserved regions. Environmental considerations and the complexities of permitting processes are also emerging as significant factors shaping deployment strategies, driving demand for more efficient and sustainable installation techniques.

- Explosive growth in global internet traffic and demand for cloud services.

- Dominance of hyperscale content providers (e.g., GMMA) in cable financing and ownership.

- Increased focus on network diversity and resilience to mitigate risks from outages or geopolitical events.

- Advancements in fiber optic technology, including higher fiber pair counts and improved optical amplifiers.

- Emergence of new, geographically diverse cable routes, including potential Arctic pathways.

- Growing emphasis on sustainability and environmental impact assessments in cable deployment.

- Demand for integrated cable systems combining telecom and power transmission capabilities for offshore energy.

AI Impact Analysis on Submarine Telecom Cable

The impact of Artificial Intelligence (AI) on the submarine telecom cable market is multifaceted, primarily manifesting through two key avenues: a massive surge in data traffic and the optimization of network operations. Users are increasingly curious about how AI-driven applications, such as large language models, advanced analytics, and autonomous systems, will strain existing network capacities and necessitate new cable deployments. This exponential growth in data generation and processing, often requiring ultra-low latency connections between data centers, directly translates into increased demand for high-capacity, resilient submarine cable infrastructure. AI algorithms themselves require vast amounts of data to be transferred and processed, making robust global connectivity indispensable.

Beyond driving demand, AI is also poised to revolutionize the operational aspects of submarine cable networks. AI and machine learning (ML) can be leveraged for predictive maintenance, analyzing sensor data from cables to anticipate potential faults, optimize repair schedules, and extend asset lifespan. This proactive approach can significantly reduce downtime and operational costs. Furthermore, AI can enhance network security by detecting anomalies and potential cyber threats in real-time, safeguarding critical infrastructure against malicious attacks. The integration of AI tools for traffic management and network optimization will ensure more efficient utilization of existing cable capacity and provide insights for future network expansion.

- Drives exponential growth in data traffic, necessitating higher capacity cable deployments.

- Enhances network efficiency through AI-driven traffic management and routing optimization.

- Enables predictive maintenance and fault detection, reducing downtime and operational costs.

- Improves cybersecurity posture for submarine cable infrastructure through AI-powered threat detection.

- Facilitates the development of new data-intensive applications (e.g., generative AI, IoT, AR/VR) that rely on global connectivity.

- Influences cable design and planning by optimizing routes and capacity based on predicted AI workload distribution.

Key Takeaways Submarine Telecom Cable Market Size & Forecast

The submarine telecom cable market is on a robust growth trajectory, fundamentally driven by the relentless global demand for data and the strategic imperatives of major internet content providers. User questions frequently revolve around the sustainability of this growth, the dominant investment trends, and the technological evolution that will underpin future expansion. The market's future is intricately linked to continued investment in high-capacity, low-latency connectivity, with a significant shift towards direct ownership and investment by large technology companies seeking to control their global data flows and ensure network performance for their cloud services and applications. This strategic imperative is a primary determinant of market expansion and technological innovation.

Key insights reveal that while traditional telecommunication carriers remain active, the landscape is increasingly shaped by hyperscalers, who are not only investing in new systems but also influencing design specifications to meet their specific, massive bandwidth requirements. Resilience, diversity, and the ability to serve emerging digital economies are paramount, leading to a proliferation of new routes and system upgrades. The market will also see continued innovation in cable technology, operational efficiencies driven by AI, and a heightened focus on environmental and geopolitical risk mitigation, all contributing to a complex yet highly critical global infrastructure sector.

- Sustained high demand for bandwidth due to cloud adoption, streaming, and AI.

- Increased private investment from content providers reshaping market dynamics.

- Focus on network resilience, diversity, and ultra-low latency connections.

- Technological advancements in fiber capacity and operational efficiency.

- Growth driven by both new deployments and upgrades of existing infrastructure.

- Emerging markets and remote regions present significant future opportunities for connectivity.

- Geopolitical and environmental factors increasingly influence route planning and project feasibility.

Submarine Telecom Cable Market Drivers Analysis

The burgeoning global demand for data transmission forms the primary impetus for the submarine telecom cable market's growth. The proliferation of digital services, from high-definition video streaming and online gaming to cloud computing and the Internet of Things (IoT), generates an ever-increasing volume of data that necessitates robust and high-capacity intercontinental connections. This data surge is compounded by the rapid adoption of AI and machine learning technologies, which require immense computational power and seamless data exchange between globally distributed data centers. Consequently, there is an insatiable need for new and upgraded submarine cable systems to keep pace with this demand, ensuring low latency and high reliability for users worldwide.

Another significant driver is the strategic imperative of hyperscale content providers, such as major technology companies, to build and own their global network infrastructure. These entities, with their vast cloud services and digital platforms, require unparalleled control over network performance, cost efficiencies, and resilience to support their global operations and user bases. By investing directly in submarine cables, they reduce reliance on third-party capacity, gain competitive advantages through optimized network paths, and ensure the scalability needed for future growth. This shift towards private ownership models has significantly accelerated cable deployment cycles and increased overall market investment.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Explosive Growth in Global Data Traffic | +2.5% | Global, particularly Asia Pacific & North America | 2025-2033 |

| Rise of Hyperscale Content Providers & Cloud Adoption | +2.0% | North America, Europe, Asia Pacific (Tier 1 cities) | 2025-2033 |

| Increased Demand for Network Diversity & Resilience | +1.5% | Global, especially vulnerable chokepoints & conflict zones | 2025-2033 |

| Technological Advancements in Fiber Optics | +1.0% | Global | 2025-2033 |

Submarine Telecom Cable Market Restraints Analysis

Despite the strong growth drivers, the submarine telecom cable market faces notable restraints, primarily centered around the extraordinarily high capital expenditure required for project development. Laying thousands of kilometers of fiber optic cable across ocean beds, installing repeaters, and establishing landing stations involves massive upfront investments, often running into hundreds of millions or even billions of dollars for a single major system. This financial barrier can limit the number of new projects, particularly for smaller consortiums or regions with limited access to capital. The long return-on-investment cycles and the inherent risks associated with such large-scale infrastructure projects also deter potential investors, creating a cautious investment climate in certain segments.

Another significant restraint involves the complex and lengthy permitting and regulatory processes. Deploying submarine cables requires approvals from numerous national and international bodies, including environmental agencies, maritime authorities, and telecommunications regulators across multiple jurisdictions. These processes can be protracted, highly bureaucratic, and subject to changing regulations, leading to significant delays and increased project costs. Furthermore, environmental concerns related to seabed disruption, marine life impact, and coastal zone management can introduce additional hurdles, requiring extensive environmental impact assessments and potentially leading to project modifications or cancellations. These regulatory complexities add layers of uncertainty and risk to cable development, impeding faster market expansion.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure & Long ROI Cycles | -1.8% | Global, particularly emerging markets | 2025-2033 |

| Complex & Lengthy Permitting and Regulatory Processes | -1.5% | Global, especially coastal zones & protected areas | 2025-2033 |

| Environmental Concerns & Impact Assessments | -1.0% | Globally sensitive marine ecosystems | 2025-2033 |

| Geopolitical Risks & Cable Damage Vulnerabilities | -0.8% | Regions with geopolitical instability, chokepoints | 2025-2033 |

Submarine Telecom Cable Market Opportunities Analysis

Significant opportunities in the submarine telecom cable market stem from the vast potential for connectivity expansion in emerging markets. Many regions in Africa, Latin America, and parts of Asia still lack robust, high-capacity internet access, leading to lower internet penetration rates and higher data costs. These underserved areas represent substantial untapped demand for reliable digital infrastructure, driven by growing populations, increasing smartphone adoption, and rising digital literacy. New cable deployments to these regions can unlock significant economic growth, foster innovation, and bridge the digital divide, presenting attractive long-term investment prospects for cable operators and content providers looking to expand their global reach.

The strategic development of new cable routes, particularly those designed to enhance network diversity and resilience, also offers substantial opportunities. With increasing geopolitical tensions and growing concerns over the vulnerability of existing chokepoints, there is a strong incentive to build alternative paths that bypass traditional high-risk areas. This includes potential Arctic routes, which could offer shorter latency paths between Asia and Europe/North America, as well as new intra-regional connections to create meshed networks. Furthermore, the integration of submarine cables with emerging technologies like edge computing and 5G networks presents a synergistic opportunity, enabling data processing closer to the source and enhancing the overall efficiency and responsiveness of global digital infrastructure. These trends promise to drive continued investment and innovation in the sector.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Underserved & Emerging Markets | +1.8% | Africa, Latin America, Southeast Asia, Pacific Islands | 2025-2033 |

| Development of New & Diverse Cable Routes (e.g., Arctic) | +1.5% | Arctic region, alternative Pacific/Atlantic paths | 2028-2033 |

| Integration with 5G Networks & Edge Computing Infrastructure | +1.2% | Global coastal areas, major internet exchange points | 2025-2030 |

| Demand for Upgrade & Capacity Expansion of Existing Systems | +1.0% | Global major routes (Trans-Atlantic, Trans-Pacific) | 2025-2033 |

Submarine Telecom Cable Market Challenges Impact Analysis

The operational challenges associated with submarine cable maintenance and repair present a significant hurdle for the market. Cables laid on the seabed are vulnerable to damage from various sources, including fishing activities (trawling), ship anchors, underwater landslides, and seismic events. Repairing a damaged cable is a complex and time-consuming operation, requiring specialized cable-laying vessels, skilled crews, and favorable weather conditions. These repairs can be incredibly costly, often running into millions of dollars per incident, and lead to significant service disruptions and revenue losses for operators. The geographical remoteness of some cable breaks further complicates logistics, extending downtime and increasing the financial burden on consortiums.

Another growing challenge is the escalating threat of cybersecurity attacks and intentional sabotage. As submarine cables form the backbone of global internet connectivity, they represent critical national infrastructure and are attractive targets for state-sponsored actors, terrorists, or malicious groups. Cyberattacks could aim to disrupt traffic, compromise data integrity, or even physically damage cable landing stations. Furthermore, geopolitical tensions can lead to concerns about deliberate physical interference or surveillance of cable systems, posing significant security risks. Ensuring the physical and cyber resilience of these vital assets against sophisticated threats requires continuous investment in advanced security measures, redundant pathways, and international cooperation, adding to the complexity and cost of network management in an increasingly volatile global landscape.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Cable Damage, Maintenance & Repair Logistics | -1.2% | Global, particularly high-traffic maritime routes | 2025-2033 |

| Geopolitical Tensions & Cybersecurity Threats | -1.0% | Global, especially sensitive geopolitical areas | 2025-2033 |

| Environmental Regulations & Climate Change Impacts | -0.7% | Coastal zones, vulnerable marine ecosystems | 2025-2033 |

| High Entry Barriers & Intense Competition | -0.5% | Global | 2025-2033 |

Submarine Telecom Cable Market - Updated Report Scope

This comprehensive market report delves into the intricate dynamics of the global Submarine Telecom Cable Market, providing an in-depth analysis of its current size, historical performance, and future growth projections. It offers a detailed examination of market trends, key drivers, restraints, opportunities, and challenges that shape the industry landscape. The report also incorporates an AI impact analysis, assessing how artificial intelligence influences both demand for and operations within the submarine cable sector. Furthermore, it presents a granular segmentation analysis across various types, components, applications, and end-users, complemented by a thorough regional outlook, offering insights into market distribution and growth potential across major geographical areas.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 19.2 Billion |

| Market Forecast in 2033 | USD 38.0 Billion |

| Growth Rate | 8.9% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Alcatel Submarine Networks (ASN), SubCom, NEC Corporation, HMN Technologies Co., Limited (HMN Tech), Fujitsu Limited, TE SubCom, Global Marine Group, S.B. Submarine Systems Co., Ltd. (SBSS), NTT Communications Corporation, Orange Marine, Telecom Italia Sparkle, Google, Microsoft, Meta Platforms, Amazon Web Services (AWS), Telstra, China Telecom Global, BT Global Services, Seacom |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The submarine telecom cable market is segmented to provide a granular view of its various facets, enabling a deeper understanding of demand drivers and growth opportunities across different categories. This segmentation helps stakeholders identify specific niches, technological preferences, and end-user requirements that influence market dynamics. By analyzing each segment independently and in relation to the whole, a comprehensive picture of the market's structure and future potential emerges, highlighting areas of robust growth and those facing particular challenges. This detailed breakdown supports strategic decision-making for investment, product development, and market entry strategies within the complex ecosystem of global connectivity.

Understanding these segments is crucial for accurate market forecasting and competitive analysis. For instance, the distinction between Wet Plant and Dry Plant components highlights the different technological and operational considerations in cable system deployment. Similarly, the diverse applications, ranging from traditional telecommunication to specialized needs of offshore oil & gas, showcase the versatility and critical importance of submarine cables across various industries. The evolving landscape of end-users, particularly the increasing dominance of content providers, signifies a fundamental shift in market power and investment patterns, necessitating tailored strategies from equipment manufacturers and service providers alike. This detailed segmentation offers a roadmap for navigating the complexities of the submarine telecom cable industry.

- By Type: This segment categorizes the market based on the major components of a submarine cable system.

- Wet Plant: Refers to the undersea components, including the cable itself and active equipment deployed on the seabed.

- Optical Fiber: The core medium for data transmission.

- Repeaters: Devices that amplify optical signals over long distances to overcome attenuation.

- Branching Units: Enable a single cable to split into multiple branches, connecting to different landing points.

- Cable Protection Systems: Structures and materials (e.g., armor, trenching) designed to protect the cable from external damage.

- Dry Plant: Encompasses the onshore equipment and infrastructure at the cable landing stations.

- Network Management Systems: Software and hardware for monitoring, controlling, and managing the cable network.

- Power Feeding Equipment: Provides the necessary electrical power to repeaters and other active components in the wet plant.

- Submarine Line Terminating Equipment (SLTE): Converts optical signals to electrical signals for terrestrial network integration and vice versa.

- Wet Plant: Refers to the undersea components, including the cable itself and active equipment deployed on the seabed.

- By Component: This segment drills down into the individual technological elements that constitute a submarine cable system.

- Optical Fiber: The fundamental medium for transmitting data as light pulses.

- Repeaters: Essential for signal amplification and regeneration along the cable length.

- Branching Units: Allow for flexible network configurations and connectivity to multiple points.

- Cable Protection Systems: Critical for ensuring the longevity and reliability of the undersea cable.

- Power Feeding Equipment: Supplies the electrical energy required for the wet plant's active components.

- Submarine Line Terminating Equipment (SLTE): The interface between the submarine and terrestrial networks.

- Network Management Systems: Tools for comprehensive oversight and control of the entire cable system.

- By Application: This segment highlights the diverse uses and end-industries benefiting from submarine cable infrastructure.

- Telecommunication: Traditional voice and data services provided by telecommunication carriers.

- Data Center Connectivity: High-capacity links between geographically dispersed data centers, crucial for cloud services.

- Internet Content Providers: Direct connections used by large technology companies to deliver content and services globally.

- Offshore Oil & Gas: Specialized communication links for offshore platforms, supporting exploration and production.

- Government & Defense: Secure and dedicated communication networks for national security and strategic operations.

- By End-user: This segment identifies the primary beneficiaries and investors in submarine cable systems.

- Wholesale Carriers: Companies that buy and sell bandwidth capacity to other service providers.

- Content Providers (Hyperscalers): Large internet companies that own and operate their own global networks.

- Enterprises: Businesses requiring dedicated international connectivity for their operations.

- Governments: National and local governmental bodies utilizing cables for various public services and defense.

- Research & Education Institutions: Networks supporting academic research, inter-university collaboration, and scientific data exchange.

Regional Highlights

- North America: A mature market characterized by significant investment from hyperscale content providers (e.g., Google, Microsoft, Meta, Amazon Web Services) driving demand for trans-Atlantic and trans-Pacific systems. Focus on high-capacity, low-latency connections to serve cloud computing and data center growth. The region serves as a major hub for internet traffic.

- Europe: A highly interconnected region with numerous intra-European and intercontinental cable systems. Strong emphasis on network diversity, resilience, and connectivity to Africa and Asia. Growing demand for digital services and data center expansion fuels continued investment, particularly in areas like Ireland and the Nordics due to favorable data center environments.

- Asia Pacific (APAC): The fastest-growing market, driven by massive population density, increasing internet penetration, and the explosion of digital economies. Dominated by new cable deployments connecting major economic hubs like Japan, South Korea, Singapore, Hong Kong, and Australia, as well as providing critical links to emerging markets in Southeast Asia and the Pacific Islands. Investments from both local carriers and global content providers are substantial.

- Latin America: An emerging market with significant potential, characterized by growing internet penetration and demand for improved connectivity to North America and Europe. Investments are focused on enhancing regional connectivity and reducing latency, with key landing points in Brazil, Chile, and Mexico. The region still presents opportunities for expanding digital inclusion.

- Middle East and Africa (MEA): A high-growth region for submarine cables, essential for bridging the digital divide and connecting vast, underserved populations to the global internet. The Middle East serves as a critical transit hub between Europe/Africa and Asia, while Africa is witnessing substantial investment in new cables along its coasts to bring reliable internet access to more countries. Development is often driven by international development goals and private investment.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Submarine Telecom Cable Market.- Alcatel Submarine Networks (ASN)

- SubCom

- NEC Corporation

- HMN Technologies Co., Limited (HMN Tech)

- Fujitsu Limited

- TE SubCom

- Global Marine Group

- S.B. Submarine Systems Co., Ltd. (SBSS)

- NTT Communications Corporation

- Orange Marine

- Telecom Italia Sparkle

- Microsoft

- Meta Platforms

- Amazon Web Services (AWS)

- Telstra

- China Telecom Global

- BT Global Services

- Seacom

Frequently Asked Questions

Analyze common user questions about the Submarine Telecom Cable market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the current growth rate of the Submarine Telecom Cable Market?

The Submarine Telecom Cable Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2025 and 2033, driven by increasing global data traffic and strategic investments.

Who are the primary investors driving new submarine cable deployments?

While traditional telecom carriers remain active, hyperscale content providers like Google, Microsoft, Meta, and Amazon Web Services are increasingly dominant, directly investing in and owning a significant portion of new submarine cable systems to support their global data center networks.

How does AI impact the demand for submarine telecom cables?

AI significantly boosts demand for submarine cables by generating vast amounts of data that require high-capacity, low-latency transmission between globally distributed data centers. It also drives the need for enhanced network resilience and efficiency for AI-driven applications.

What are the main challenges faced by the submarine cable industry?

Key challenges include high capital expenditure, complex and lengthy permitting processes, the risk and cost of cable damage (e.g., from fishing or anchors), and growing concerns over cybersecurity threats and geopolitical vulnerabilities.

Which regions are seeing the most significant growth in submarine cable investment?

Asia Pacific (APAC) is currently the fastest-growing market due to exploding data demand and rising internet penetration. North America and Europe also continue to see substantial investment, primarily from hyperscale content providers aiming to enhance intercontinental connectivity.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted