Silicon Carbide Power Semiconductor Market

Silicon Carbide Power Semiconductor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708524 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Silicon Carbide Power Semiconductor Market Size

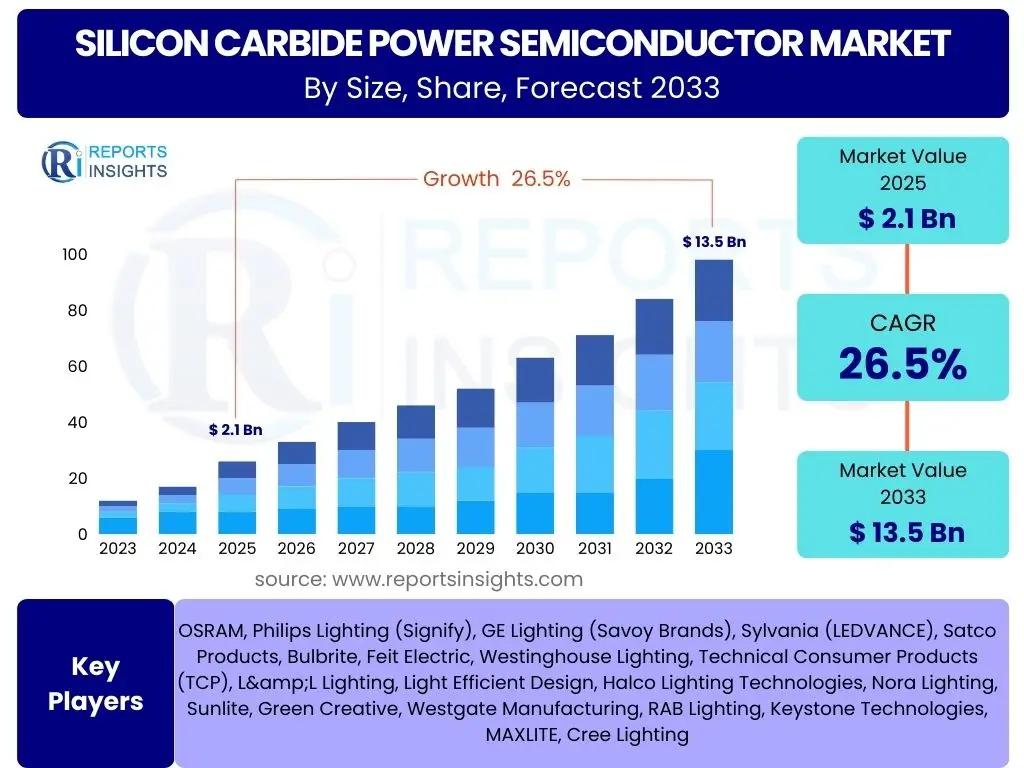

According to Reports Insights Consulting Pvt Ltd, The Silicon Carbide Power Semiconductor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 26.5% between 2025 and 2033. The market is estimated at USD 2.1 Billion in 2025 and is projected to reach USD 13.5 Billion by the end of the forecast period in 2033. This robust growth is primarily driven by the increasing demand for high-efficiency power electronics across various industries, particularly in electric vehicles, renewable energy systems, and industrial power management. The inherent advantages of silicon carbide, such as higher breakdown voltage, faster switching speeds, and lower energy losses compared to traditional silicon-based devices, are accelerating its adoption.

The expansion is further supported by significant investments in research and development, aiming to overcome existing manufacturing challenges and reduce production costs. As technological advancements continue to mature, the scalability and performance benefits of SiC power semiconductors are becoming more accessible, prompting a broader range of applications. This trajectory indicates a fundamental shift in the power electronics landscape, with SiC poised to become a cornerstone technology for energy-efficient solutions in the next decade.

Key Silicon Carbide Power Semiconductor Market Trends & Insights

Common inquiries about Silicon Carbide Power Semiconductor market trends reveal a strong interest in its role in emerging technologies, sustainability efforts, and industrial efficiency. Users are particularly keen on understanding how SiC is integrating into electric vehicles, renewable energy infrastructure, and advanced industrial applications. There is also significant curiosity regarding the evolution of manufacturing processes, material availability, and the impact of these developments on market pricing and accessibility. The drive towards higher power density, improved thermal performance, and miniaturization of electronic systems is a recurring theme in user questions, highlighting the critical performance attributes that SiC offers compared to conventional silicon.

Furthermore, questions frequently touch upon the competitive landscape, asking about the key players driving innovation and the regional dynamics shaping market growth. The ongoing transition from 6-inch to 8-inch SiC wafers is another area of interest, signifying the industry's push for greater production efficiency and cost reduction. These inquiries collectively underscore a market that is not only expanding rapidly but also undergoing significant technological and operational transformations, attracting attention from various stakeholders seeking to capitalize on its potential for energy-efficient power solutions.

- Exponential growth in Electric Vehicle (EV) adoption, particularly in on-board chargers, inverters, and DC-DC converters, driving SiC demand.

- Increasing integration of SiC devices in renewable energy systems, including solar inverters and wind turbine converters, for enhanced efficiency and reliability.

- Transition towards larger wafer sizes (e.g., 8-inch SiC wafers) to achieve economies of scale and reduce manufacturing costs.

- Development of advanced packaging technologies to improve thermal management and power density of SiC modules.

- Expansion of SiC applications into new industrial sectors, data centers, and 5G infrastructure for high-power, high-frequency operations.

- Focus on supply chain diversification and vertical integration among key players to ensure material availability and control costs.

- Growing investment in research and development to enhance SiC material quality, device performance, and reliability under extreme conditions.

AI Impact Analysis on Silicon Carbide Power Semiconductor

User queries regarding AI's influence on Silicon Carbide Power Semiconductors primarily focus on how artificial intelligence can optimize the design, manufacturing, and application of these advanced devices. There is keen interest in AI's potential to accelerate material discovery and characterization, improve fault detection in production, and enhance the predictive maintenance of SiC-based systems. Users anticipate AI playing a crucial role in managing complex power grids that integrate SiC components, and in developing more efficient control algorithms for electric vehicle powertrains. The overarching expectation is that AI will unlock new levels of performance and reliability, while simultaneously reducing the time and cost associated with product development and deployment.

Another significant area of user concern revolves around the practical implementation challenges and the necessary data infrastructure to support AI integration within the SiC ecosystem. Questions arise about the availability of high-quality training data for AI models, the computational resources required, and the specialized expertise needed to effectively apply AI techniques. These discussions highlight a recognized need for cross-disciplinary collaboration between AI specialists, material scientists, and power electronics engineers to fully realize the transformative potential of AI in shaping the future of silicon carbide technology.

- Design Optimization: AI-driven simulations and generative design can accelerate the development of SiC device structures, optimizing performance parameters like breakdown voltage, on-resistance, and switching speed.

- Material Characterization: Machine learning algorithms can analyze vast datasets from material synthesis to identify optimal growth conditions for high-quality SiC wafers, improving purity and crystal defect reduction.

- Manufacturing Efficiency: AI-powered predictive analytics can monitor production lines, anticipate equipment failures, and optimize process parameters, leading to higher yields and reduced waste in SiC fabrication.

- Quality Control and Inspection: Automated optical inspection (AOI) systems combined with AI can swiftly detect microscopic defects in SiC wafers and devices, ensuring stringent quality standards are met.

- System Integration and Control: AI algorithms can optimize the control strategies for SiC-based power converters in applications like EVs and renewable energy grids, enhancing efficiency and reliability under varying operating conditions.

- Predictive Maintenance: AI can enable real-time monitoring and predictive maintenance for SiC power modules in critical applications, reducing downtime and extending the lifespan of systems.

Key Takeaways Silicon Carbide Power Semiconductor Market Size & Forecast

An analysis of common user questions concerning the Silicon Carbide Power Semiconductor market size and forecast reveals a strong emphasis on understanding the primary growth catalysts and the long-term viability of this technology. Users are particularly interested in identifying which applications will drive the most significant demand, with electric vehicles and renewable energy consistently appearing as focal points. There is also a notable desire for insights into the competitive landscape, asking about the market dominance of key players and the potential for new entrants to disrupt established supply chains. The overarching sentiment indicates a market poised for substantial expansion, driven by its intrinsic value proposition of superior efficiency and performance.

Furthermore, inquiries frequently touch upon the critical success factors for market penetration, including cost reduction strategies, manufacturing scalability, and the development of robust, reliable devices. Stakeholders are keen to grasp the trajectory of market valuation and the underlying technological advancements that will sustain this growth over the forecast period. The summary of these insights underscores a consensus that Silicon Carbide power semiconductors represent a transformative technology with significant economic potential, prompting strategic planning and investment across various industrial sectors.

- The Silicon Carbide Power Semiconductor market is set for exceptional growth, projected to exceed USD 13 billion by 2033, driven by a high CAGR of 26.5%.

- Electric Vehicles and renewable energy systems are the primary growth engines, representing the largest and fastest-growing application segments.

- Technological advancements, including the shift to larger wafer sizes and improved manufacturing processes, are crucial for cost reduction and market accessibility.

- Key market players are heavily investing in research, development, and capacity expansion to meet escalating demand and solidify their competitive positions.

- Supply chain robustness and material sourcing remain critical factors influencing market stability and growth trajectory.

- The performance advantages of SiC over traditional silicon are leading to its widespread adoption across high-power, high-frequency, and high-temperature applications.

Silicon Carbide Power Semiconductor Market Drivers Analysis

The Silicon Carbide Power Semiconductor market is significantly influenced by a confluence of powerful drivers, each contributing to its accelerating adoption across various industries. The global imperative for energy efficiency and reduced carbon emissions stands as a foundational driver, pushing industries to seek superior power management solutions. SiC devices, with their inherently lower switching losses and higher operational temperatures, directly address these demands, enabling more compact, lighter, and ultimately more efficient electronic systems. This technological superiority is becoming increasingly critical in sectors where performance and energy savings are paramount.

Beyond the inherent material advantages, strategic governmental initiatives and corporate sustainability goals are further catalyzing market expansion. Subsidies for electric vehicles, mandates for renewable energy integration, and increasing investments in advanced manufacturing are creating a fertile ground for SiC technology. As the cost-performance ratio of SiC devices continues to improve through manufacturing innovations and economies of scale, their appeal broadens, attracting a wider array of applications from high-end industrial equipment to mainstream consumer electronics. These combined forces ensure a sustained and robust demand for Silicon Carbide power semiconductors.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Electric Vehicle (EV) Adoption | +8.0% | Global, particularly China, Europe, North America | Short to Long Term (2025-2033) |

| Renewable Energy Grid Integration | +5.5% | Global, particularly Europe, Asia Pacific | Medium to Long Term (2026-2033) |

| Industrial Power Supplies & Motor Drives | +4.0% | North America, Europe, Asia Pacific | Short to Medium Term (2025-2030) |

| Data Centers and 5G Infrastructure Expansion | +3.5% | North America, Asia Pacific, Europe | Medium Term (2026-2031) |

| Enhanced Energy Efficiency Requirements | +5.0% | Global | Long Term (2027-2033) |

Silicon Carbide Power Semiconductor Market Restraints Analysis

Despite its significant advantages, the Silicon Carbide Power Semiconductor market faces several notable restraints that could temper its growth trajectory. One of the primary challenges is the relatively high manufacturing cost associated with SiC wafers and devices compared to mature silicon-based counterparts. The complex and energy-intensive processes required for crystal growth and subsequent wafer fabrication contribute to a higher per-unit cost, which can deter adoption in price-sensitive applications. While costs are gradually decreasing with economies of scale and technological advancements, they remain a significant barrier for broader market penetration.

Another critical restraint is the ongoing challenge of supply chain robustness and material availability. The specialized nature of SiC material production means that the supply chain is less diversified and more susceptible to disruptions than that of silicon. Issues related to raw material purity, wafer quality, and consistent yield can impact production volumes and lead times. Furthermore, the limited availability of experienced engineers and technicians skilled in SiC device design and manufacturing also poses a challenge, impacting the pace of innovation and market expansion. Addressing these restraints will be crucial for the sustained, rapid growth of the Silicon Carbide Power Semiconductor market.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs of SiC Wafers & Devices | -3.0% | Global | Short to Medium Term (2025-2029) |

| Supply Chain Vulnerabilities and Material Availability | -2.0% | Global | Short to Medium Term (2025-2030) |

| Lack of Standardization Across the Industry | -1.5% | Global | Medium Term (2026-2031) |

| Technical Challenges in High-Volume Production | -1.0% | Global | Short Term (2025-2028) |

Silicon Carbide Power Semiconductor Market Opportunities Analysis

The Silicon Carbide Power Semiconductor market is rich with significant opportunities for innovation and expansion, driven by its superior performance characteristics and the evolving needs of various industries. One major opportunity lies in the continuous development of advanced packaging technologies. As SiC devices operate at higher temperatures and power densities, innovative thermal management and compact packaging solutions are essential to fully harness their potential, opening avenues for specialized component manufacturers and system integrators. This focus on optimized packaging can unlock further performance gains and enable new form factors for SiC-based modules.

Moreover, the burgeoning market for electric vehicle fast-charging infrastructure presents a lucrative opportunity. SiC devices are critical for efficient and high-power charging stations, both at home and publicly, significantly reducing charging times and enhancing user experience. Beyond automotive, the aerospace and defense sectors are increasingly exploring SiC for mission-critical applications requiring extreme reliability and weight reduction, offering a high-value, albeit specialized, market segment. Additionally, the global push towards smart grids and grid modernization initiatives creates demand for SiC in power conversion and management, promising enhanced grid stability and efficiency. These diverse applications underscore the vast untapped potential for Silicon Carbide technology across high-growth sectors.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Packaging Solutions | +4.0% | Global | Medium to Long Term (2026-2033) |

| Automotive Fast Charging Infrastructure | +3.5% | Global, particularly China, Europe, North America | Short to Long Term (2025-2033) |

| Aerospace & Defense Applications | +2.5% | North America, Europe | Medium to Long Term (2027-2033) |

| Smart Grid and Energy Storage Systems | +3.0% | Europe, Asia Pacific, North America | Medium to Long Term (2026-2033) |

Silicon Carbide Power Semiconductor Market Challenges Impact Analysis

The Silicon Carbide Power Semiconductor market, while promising, is not without its significant challenges that could impede its rapid expansion. Scaling production capacity to meet the exponentially growing demand, particularly from the automotive sector, is a formidable hurdle. The current manufacturing infrastructure, while expanding, still lags behind the anticipated future requirements, potentially leading to supply shortages and escalating costs. Achieving consistent high yield rates for large-diameter SiC wafers also remains a complex technical challenge, impacting overall production efficiency and profitability. These scalability issues are critical to address for the market to fully realize its potential.

Furthermore, the long technology development timelines and substantial capital investments required for new fabrication facilities present significant barriers to entry and expansion for many companies. The intricate intellectual property landscape surrounding SiC technology, with numerous patents held by established players, can also lead to complex legal disputes and hinder innovation or market access for newcomers. Lastly, the specialized nature of SiC manufacturing and design demands a highly skilled workforce, and the shortage of such talent globally poses a challenge for talent acquisition and retention, further complicating market growth and technological advancement. Overcoming these challenges will necessitate concerted efforts in R&D, infrastructure investment, and workforce development.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Scaling Production Capacity and Yield Rates | -3.5% | Global | Short to Medium Term (2025-2030) |

| High Capital Investment for New Fabs | -2.0% | Global | Medium Term (2026-2031) |

| Complex Intellectual Property Landscape | -1.5% | Global | Medium to Long Term (2027-2033) |

| Shortage of Skilled Workforce and Expertise | -1.0% | Global | Long Term (2028-2033) |

Silicon Carbide Power Semiconductor Market - Updated Report Scope

This updated report provides a comprehensive analysis of the Silicon Carbide Power Semiconductor market, encompassing critical insights into its current size, historical growth, and future projections. It delves into the key market trends, drivers, restraints, opportunities, and challenges that are shaping the industry landscape. The scope includes a detailed segmentation analysis across various product types, applications, and regional markets, offering a granular view of market dynamics. Furthermore, the report identifies and profiles leading market players, providing an overview of their strategic initiatives and competitive positioning. This document serves as an indispensable resource for stakeholders seeking to understand the evolving dynamics and future potential of SiC technology.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.1 Billion |

| Market Forecast in 2033 | USD 13.5 Billion |

| Growth Rate | 26.5% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Wolfspeed, Inc., STMicroelectronics N.V., ROHM Co., Ltd., Infineon Technologies AG, ON Semiconductor Corporation, Mitsubishi Electric Corporation, Littelfuse, Inc., WeEn Semiconductors, Fuji Electric Co., Ltd., Nexperia, Toshiba Corporation, Microsemi Corporation, Renesas Electronics Corporation, SEMIKRON Danfoss, Sanan Optoelectronics Co., Ltd., Basler AG, GeneSiC Semiconductor (MACOM Technology Solutions Inc.), UnitedSiC (Qorvo), Shindengen Electric Mfg. Co., Ltd., X-FAB Silicon Foundries SE |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Silicon Carbide Power Semiconductor market is extensively segmented to provide a granular understanding of its diverse applications and technological nuances. This segmentation allows for a detailed analysis of market dynamics across various product types, application areas, wafer sizes, and voltage ranges. Understanding these segments is crucial for identifying specific growth pockets, tailoring product development, and devising targeted market strategies. The market's complexity necessitates such a comprehensive breakdown to capture the full spectrum of opportunities and challenges inherent in this rapidly evolving industry, guiding stakeholders in their strategic decision-making and investment allocations.

Each segment exhibits unique growth patterns influenced by distinct end-user requirements, regulatory landscapes, and technological maturity. For instance, the Electric Vehicle segment demands specific voltage ranges and packaging solutions, while renewable energy applications prioritize efficiency and reliability under varying environmental conditions. Analyzing these individual segments helps in projecting future demand accurately and in understanding the competitive forces at play within each niche, ensuring that market participants can effectively position themselves to capitalize on emerging trends.

- By Product Type:

- SiC Diodes

- SiC MOSFETs

- SiC Modules

- Others (e.g., SiC Thyristors, BJTs)

- By Wafer Size:

- 4-inch

- 6-inch

- 8-inch

- Others (e.g., 2-inch)

- By Application:

- Electric Vehicles

- On-Board Chargers

- Traction Inverters

- DC-DC Converters

- Renewable Energy

- Solar Inverters

- Wind Turbine Converters

- Industrial

- Motor Drives

- Power Supplies (e.g., UPS)

- Welding Equipment

- Data Centers

- Aerospace & Defense

- Consumer Electronics

- Medical

- Others

- Electric Vehicles

- By Voltage Range:

- Low Voltage (<600V)

- Medium Voltage (600V-1200V)

- High Voltage (>1200V)

Regional Highlights

- Asia Pacific (APAC): Dominates the Silicon Carbide Power Semiconductor market, driven by robust growth in electric vehicle manufacturing, extensive renewable energy projects, and rapid industrialization in countries like China, Japan, South Korea, and Taiwan. The region benefits from significant government support for EV adoption and a strong electronics manufacturing base, making it a key hub for both production and consumption.

- Europe: Exhibits substantial growth, primarily fueled by stringent environmental regulations, ambitious decarbonization targets, and the presence of leading automotive manufacturers. The region is a pioneer in renewable energy integration and continues to invest heavily in advanced industrial applications, driving demand for high-efficiency SiC devices in countries such as Germany, France, and the Nordics.

- North America: A significant market characterized by strong R&D investments, increasing adoption of electric vehicles, and expansion in data center infrastructure. The presence of major technology innovators and a focus on upgrading aging power grids contribute to the region's steady demand for SiC power semiconductors, particularly in the United States.

- Latin America: An emerging market with growing interest in electric mobility and renewable energy projects. While currently smaller in scale, increasing foreign investments and improving economic conditions are expected to boost the adoption of SiC technology in countries like Brazil and Mexico over the forecast period.

- Middle East and Africa (MEA): Shows potential with rising investments in renewable energy infrastructure, particularly solar power, and efforts to diversify economies away from fossil fuels. Countries like Saudi Arabia and the UAE are exploring smart city initiatives and electric vehicle adoption, which will gradually drive demand for SiC power semiconductors in the long term.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Silicon Carbide Power Semiconductor Market.- Wolfspeed, Inc.

- STMicroelectronics N.V.

- ROHM Co., Ltd.

- Infineon Technologies AG

- ON Semiconductor Corporation

- Mitsubishi Electric Corporation

- Littelfuse, Inc.

- WeEn Semiconductors

- Fuji Electric Co., Ltd.

- Nexperia

- Toshiba Corporation

- Microsemi Corporation

- Renesas Electronics Corporation

- SEMIKRON Danfoss

- Sanan Optoelectronics Co., Ltd.

- Basler AG

- GeneSiC Semiconductor (MACOM Technology Solutions Inc.)

- UnitedSiC (Qorvo)

- Shindengen Electric Mfg. Co., Ltd.

- X-FAB Silicon Foundries SE

Frequently Asked Questions

Analyze common user questions about the Silicon Carbide Power Semiconductor market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a Silicon Carbide Power Semiconductor?

A Silicon Carbide (SiC) power semiconductor is an electronic device made from silicon carbide material, which offers superior performance characteristics like higher voltage resistance, faster switching speeds, and lower energy losses compared to traditional silicon-based semiconductors. These devices are crucial for high-power, high-frequency, and high-temperature applications.

Why is Silicon Carbide preferred over Silicon for power electronics?

SiC is preferred over silicon due to its wider bandgap, higher thermal conductivity, and higher breakdown electric field. These properties enable SiC devices to operate at higher voltages, temperatures, and frequencies with significantly reduced energy losses, leading to more compact, efficient, and reliable power electronic systems.

What are the primary applications driving the growth of the SiC market?

The primary applications driving market growth are Electric Vehicles (EVs), including on-board chargers and traction inverters, and Renewable Energy systems such as solar inverters and wind turbine converters. Industrial power supplies, data centers, and 5G infrastructure are also significant growth sectors.

What are the main challenges facing the Silicon Carbide Power Semiconductor market?

Key challenges include the high manufacturing costs of SiC wafers and devices, complexities in scaling up production capacity while maintaining high yield rates, vulnerabilities in the supply chain for raw materials, and a shortage of skilled labor with specialized SiC expertise.

How is the market expected to evolve in terms of wafer size?

The market is rapidly transitioning from 4-inch and 6-inch SiC wafers to larger 8-inch wafers. This shift aims to achieve greater economies of scale, reduce the per-device cost, and significantly increase production output to meet the surging demand from various industries, particularly the automotive sector.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted