Styrene Market

Styrene Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702654 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

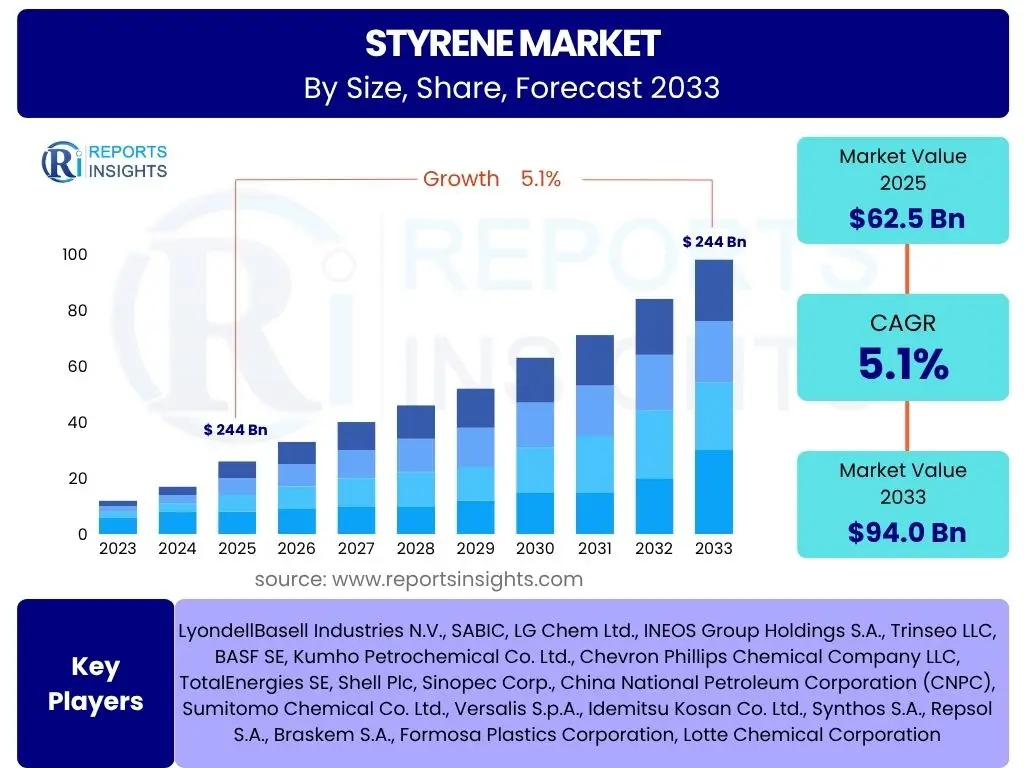

Styrene Market Size

According to Reports Insights Consulting Pvt Ltd, The Styrene Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.1% between 2025 and 2033. The market is estimated at USD 62.5 billion in 2025 and is projected to reach USD 94.0 billion by the end of the forecast period in 2033.

Key Styrene Market Trends & Insights

The global styrene market is currently experiencing significant shifts driven by evolving consumer demands, sustainability initiatives, and technological advancements. Key trends include the increasing adoption of sustainable and bio-based styrene alternatives, a growing emphasis on circular economy principles through advanced recycling technologies, and the expansion of its application in high-performance materials. Furthermore, the market is witnessing regional shifts in production and consumption, particularly with robust growth in emerging economies, alongside a continuous drive for operational efficiency and cost optimization across the value chain.

User inquiries frequently revolve around the impact of environmental regulations on production, the trajectory of demand in key end-use industries like packaging and automotive, and the potential for new market entrants or disruptive technologies. There is also considerable interest in how geopolitical factors and raw material price volatility influence market stability and future growth prospects. These trends collectively underscore a dynamic market environment where innovation, sustainability, and supply chain resilience are becoming increasingly critical for competitive advantage.

- Shift towards bio-based and recycled styrene derivatives.

- Increased demand from packaging and automotive lightweighting.

- Focus on energy-efficient production processes.

- Growing investment in advanced recycling technologies for polystyrene.

- Expansion of styrene applications in specialized composites and elastomers.

AI Impact Analysis on Styrene

The integration of Artificial Intelligence (AI) across the styrene value chain is emerging as a transformative force, with potential to significantly enhance operational efficiency, optimize production processes, and facilitate strategic decision-making. Common user questions concerning AI's impact often center on its ability to predict market fluctuations, manage supply chain complexities, and improve product quality control. AI-driven predictive analytics can forecast demand variations, enabling manufacturers to adjust production schedules proactively and minimize waste, thereby optimizing inventory management and reducing operational costs.

Moreover, AI algorithms can revolutionize research and development by accelerating the discovery of new catalysts or polymerization techniques, leading to more sustainable and cost-effective styrene derivatives. Users are also keen to understand how AI can be deployed for real-time monitoring of plant operations, enabling predictive maintenance, identifying anomalies, and ensuring safer working environments. While the adoption is still nascent for some applications, the overarching expectation is that AI will drive efficiency gains, foster innovation, and build more resilient supply chains within the styrene market.

- Optimized production processes through predictive analytics.

- Enhanced supply chain management and logistics.

- Accelerated R&D for new styrene derivatives and catalysts.

- Improved quality control and yield optimization.

- Predictive maintenance for manufacturing equipment, reducing downtime.

Key Takeaways Styrene Market Size & Forecast

The styrene market is poised for steady expansion through 2033, driven primarily by sustained demand from its diverse end-use applications, particularly in the packaging, automotive, and construction sectors. User inquiries frequently highlight the criticality of understanding the underlying growth drivers, such as increasing urbanization and industrialization in emerging economies, which underpin the market's positive outlook. Another significant takeaway is the ongoing evolution of the market towards more sustainable practices, including the development of bio-based styrene and advanced recycling technologies, which will be crucial in mitigating environmental concerns and ensuring long-term viability.

Furthermore, stakeholders should recognize the persistent influence of raw material price volatility and stringent environmental regulations as key factors shaping market dynamics. The forecast indicates that while traditional applications will continue to dominate, innovation in specialty applications and the adoption of circular economy principles will increasingly define competitive advantage. This necessitates a strategic focus on R&D for sustainable solutions and flexible supply chain management to navigate potential market disruptions effectively.

- Stable growth driven by end-use industries.

- Sustainability initiatives are key for future market direction.

- Emerging economies present significant growth opportunities.

- Raw material price volatility remains a critical market factor.

- Innovation in recycling and bio-based solutions is essential.

Styrene Market Drivers Analysis

The global styrene market is significantly propelled by the expanding demand across various key end-use industries. The packaging sector, particularly for food and consumer goods, continues to be a dominant consumer, benefiting from increasing urbanization and disposable incomes. Styrene derivatives, such as polystyrene (PS) and expanded polystyrene (EPS), are extensively used due to their lightweight, insulating, and protective properties. Similarly, the automotive industry's growing shift towards lightweighting vehicles to improve fuel efficiency and reduce emissions drives the demand for styrene-based composites and plastics like ABS (Acrylonitrile Butadiene Styrene) in interior and exterior components.

Furthermore, robust growth in the construction industry, particularly in developing regions, fuels the need for styrene-based insulation, pipes, and other building materials due to their durability and thermal performance. The burgeoning electronics industry also contributes substantially, utilizing styrene derivatives in casings, components, and insulators. The versatility and cost-effectiveness of styrene in these applications ensure its continued relevance and demand. The ongoing industrialization and infrastructural development in regions like Asia Pacific and Latin America further solidify these demand-side drivers, creating a positive feedback loop for market expansion.

Lastly, the increasing adoption of synthetic rubbers like Styrene-Butadiene Rubber (SBR) in tire manufacturing and other industrial applications provides another significant impetus. As global vehicle production and industrial activity rise, so does the demand for SBR, directly impacting styrene consumption. This broad spectrum of applications, coupled with continuous population growth and economic development, collectively acts as powerful drivers for the styrene market's sustained expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand from packaging industry | +1.5% | Asia Pacific, North America, Europe | Short to Medium Term (2025-2029) |

| Increasing use in automotive lightweighting | +1.2% | Europe, North America, China | Medium to Long Term (2027-2033) |

| Expansion of construction sector | +1.0% | Asia Pacific (India, China), Middle East | Short to Medium Term (2025-2030) |

| Rise in demand for synthetic rubbers (SBR) | +0.8% | Global, particularly Asia Pacific | Medium Term (2026-2031) |

Styrene Market Restraints Analysis

The styrene market faces several significant restraints that could impede its growth trajectory. One primary concern is the volatility of raw material prices, particularly benzene and ethylene, which are petrochemical derivatives. Fluctuations in crude oil prices directly impact the cost of these precursors, leading to unstable production costs for styrene manufacturers. This price unpredictability can squeeze profit margins and make long-term planning challenging, discouraging new investments in production capacity and potentially leading to a cautious approach from market participants.

Another major restraint involves stringent environmental regulations and health concerns associated with styrene. Styrene is classified as a hazardous air pollutant and a probable human carcinogen, leading to increasing regulatory scrutiny regarding emissions, worker exposure, and waste disposal. Regulations such as REACH in Europe and similar initiatives globally impose strict limits on production processes and end-use applications, necessitating significant investments in pollution control technologies and alternative, greener manufacturing methods. These compliance costs can be substantial, adding to the operational burden for producers.

Furthermore, the availability of substitute materials poses a competitive threat to styrene-based products. In various applications, alternative polymers or materials like polypropylene, polyethylene, or even bio-plastics can offer comparable performance, sometimes with lower environmental footprints or competitive pricing. While styrene's versatility is a strength, the continuous development and promotion of these substitutes can erode its market share in specific segments. Public perception regarding plastics and petrochemicals, often negative, also influences consumer preferences and regulatory pressure, indirectly acting as a restraint on market expansion.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile raw material prices | -1.3% | Global | Short to Medium Term (2025-2030) |

| Stringent environmental regulations & health concerns | -1.0% | Europe, North America, developed Asia Pacific | Medium to Long Term (2026-2033) |

| Competition from substitute materials | -0.7% | Global, especially in packaging & construction | Medium Term (2026-2031) |

Styrene Market Opportunities Analysis

The styrene market is presented with several promising opportunities that could unlock new growth avenues and foster sustainable development. A significant opportunity lies in the burgeoning field of bio-based styrene production. Research and development efforts are intensifying to produce styrene from renewable feedstocks such as biomass or agricultural waste, moving away from petrochemical reliance. This not only addresses environmental concerns but also offers a pathway to stable pricing less vulnerable to crude oil volatility, appealing to environmentally conscious consumers and industries.

Another substantial opportunity is the advancement and scaling of chemical recycling technologies for polystyrene waste. Traditional mechanical recycling of polystyrene has limitations, but innovative chemical processes can depolymerize polystyrene back into its monomer, styrene, which can then be used to produce virgin-quality plastic. This circular economy approach reduces waste, lowers the demand for virgin fossil resources, and aligns with global sustainability goals, opening up a massive new feedstock stream and improving the material's environmental profile.

Furthermore, the exploration of new and niche applications for styrene derivatives, particularly in high-performance materials like advanced composites for aerospace, wind energy, and specialized electronics, offers significant growth potential. As industries demand lighter, stronger, and more durable materials, the unique properties of styrene-based polymers can be tailored to meet these stringent requirements. Expanding market penetration in emerging economies, particularly those undergoing rapid industrialization and infrastructure development, also provides substantial opportunities for increased consumption across various end-use sectors, leveraging their growing demand for consumer goods, automotive components, and construction materials.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of bio-based styrene | +1.8% | Europe, North America, Japan | Medium to Long Term (2027-2033) |

| Advancements in polystyrene chemical recycling | +1.5% | Europe, North America, Developed Asia | Medium to Long Term (2027-2033) |

| Emerging applications in high-performance materials | +1.0% | Global, high-tech regions | Medium Term (2026-2031) |

| Untapped demand in developing economies | +0.9% | Africa, Southeast Asia, Latin America | Short to Medium Term (2025-2030) |

Styrene Market Challenges Impact Analysis

The styrene market faces several significant challenges that require strategic navigation to maintain growth and stability. One prominent challenge is the increasing scrutiny and negative public perception surrounding plastics and petrochemicals, particularly regarding their environmental impact and contribution to plastic pollution. This societal pressure often translates into heightened regulatory demands for sustainable practices, waste reduction, and the development of alternative materials, which can be costly and time-consuming for manufacturers to implement.

Another critical challenge involves the complex and often disrupted global supply chain. Events such as geopolitical tensions, natural disasters, and pandemics can lead to bottlenecks in raw material supply (benzene, ethylene), logistics disruptions, and capacity shortages. This unpredictability makes it difficult for producers to maintain consistent production levels, manage inventory efficiently, and meet global demand, leading to price volatility and potential revenue losses. The capital-intensive nature of styrene production facilities, coupled with long lead times for construction and expansion, exacerbates the challenge of rapidly adjusting to market shifts or unexpected demand surges.

Furthermore, managing the health and safety risks associated with styrene manufacturing and handling presents an ongoing challenge. Due to its classification as a hazardous chemical, adherence to strict occupational safety standards, continuous investment in safety equipment, and comprehensive employee training are essential to prevent accidents and ensure compliance. The costs associated with these measures, along with potential liabilities from non-compliance or incidents, add a significant operational burden. The industry also faces the challenge of developing economically viable and scalable sustainable alternatives or recycling solutions that can compete with the cost-effectiveness of conventional styrene production, which requires substantial R&D investment and collaborative efforts across the value chain.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Negative public perception & regulatory pressure on plastics | -1.2% | Global, particularly developed regions | Medium to Long Term (2026-2033) |

| Supply chain disruptions & logistical complexities | -1.0% | Global | Short to Medium Term (2025-2029) |

| High capital expenditure for sustainable transition | -0.8% | Global | Medium to Long Term (2027-2033) |

Styrene Market - Updated Report Scope

This report provides an in-depth analysis of the global styrene market, covering market dynamics, key trends, drivers, restraints, opportunities, and challenges. It includes detailed market sizing and forecasts segmented by various parameters to offer a holistic view of the industry. The scope encompasses a historical review, current market performance, and future projections, providing stakeholders with critical insights for strategic decision-making and investment planning across different geographies and end-use industries.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 62.5 billion |

| Market Forecast in 2033 | USD 94.0 billion |

| Growth Rate | 5.1% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | LyondellBasell Industries N.V., SABIC, LG Chem Ltd., INEOS Group Holdings S.A., Trinseo LLC, BASF SE, Kumho Petrochemical Co. Ltd., Chevron Phillips Chemical Company LLC, TotalEnergies SE, Shell Plc, Sinopec Corp., China National Petroleum Corporation (CNPC), Sumitomo Chemical Co. Ltd., Versalis S.p.A., Idemitsu Kosan Co. Ltd., Synthos S.A., Repsol S.A., Braskem S.A., Formosa Plastics Corporation, Lotte Chemical Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The styrene market is extensively segmented by application, end-use industry, technology, and grade to provide a granular understanding of its diverse components and drivers. This detailed segmentation allows for a precise analysis of demand patterns and growth prospects across various product forms and their specific uses. For instance, the market's reliance on traditional applications like polystyrene for packaging and ABS for automotive parts is juxtaposed with the emerging demand for advanced applications and sustainable derivatives.

Understanding these segments is crucial for identifying key growth areas and strategic investment opportunities. Each segment possesses unique market dynamics, competitive landscapes, and regulatory environments, necessitating a tailored approach for market entry or expansion. The report breaks down these segments to highlight their individual contributions to the overall market size and their projected growth trajectories, offering comprehensive insights for stakeholders.

- By Application:

- Polystyrene (PS)

- Acrylonitrile Butadiene Styrene (ABS)

- Styrene Butadiene Rubber (SBR)

- Unsaturated Polyester Resins (UPR)

- Styrene-Butadiene Latex (SBL)

- Expanded Polystyrene (EPS)

- Others (Styrene-Acrylonitrile (SAN), etc.)

- By End-Use Industry:

- Packaging

- Automotive

- Construction

- Electrical & Electronics

- Consumer Goods

- Marine

- Others

- By Technology:

- Ethylbenzene Dehydrogenation

- Styrene from Propylene Oxide (SM/PO)

- Others

- By Grade:

- General Purpose Polystyrene (GPPS)

- High Impact Polystyrene (HIPS)

- Expanded Polystyrene (EPS)

- Others

Regional Highlights

- Asia Pacific (APAC): This region is anticipated to be the largest and fastest-growing market for styrene, driven by rapid industrialization, increasing disposable incomes, and significant growth in end-use industries like packaging, construction, and automotive, particularly in countries such as China, India, and Southeast Asian nations. The expansion of manufacturing bases and robust infrastructure development initiatives contribute substantially to demand.

- North America: A mature yet significant market, North America maintains steady demand primarily from the packaging, automotive, and building & construction sectors. The region is characterized by technological advancements, increasing focus on lightweight materials, and growing investments in recycling technologies and bio-based alternatives, particularly in the United States and Canada.

- Europe: Europe is a key market with a strong emphasis on sustainability and circular economy principles. Strict environmental regulations drive innovation towards bio-based styrene and advanced recycling methods. Demand stems from the automotive, construction, and packaging industries, with a noticeable shift towards high-performance and specialty applications, particularly in Germany, France, and the UK.

- Latin America: This region presents emerging opportunities due to increasing industrial activity and urbanization. Countries like Brazil and Mexico are witnessing growing demand for styrene in packaging, construction, and consumer goods, although economic stability and infrastructure development remain influencing factors for market growth.

- Middle East & Africa (MEA): The MEA region is expected to show considerable growth, largely due to ongoing infrastructure projects, industrial expansion, and increasing domestic consumption. Investments in petrochemical production capacities, particularly in Saudi Arabia and UAE, support local demand and export potential for styrene and its derivatives.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Styrene Market.- LyondellBasell Industries N.V.

- SABIC

- LG Chem Ltd.

- INEOS Group Holdings S.A.

- Trinseo LLC

- BASF SE

- Kumho Petrochemical Co. Ltd.

- Chevron Phillips Chemical Company LLC

- TotalEnergies SE

- Shell Plc

- Sinopec Corp.

- China National Petroleum Corporation (CNPC)

- Sumitomo Chemical Co. Ltd.

- Versalis S.p.A.

- Idemitsu Kosan Co. Ltd.

- Synthos S.A.

- Repsol S.A.

- Braskem S.A.

- Formosa Plastics Corporation

- Lotte Chemical Corporation

Frequently Asked Questions

What is styrene primarily used for?

Styrene is primarily used as a chemical intermediate in the production of various polymers, most notably polystyrene (PS), acrylonitrile butadiene styrene (ABS), and styrene-butadiene rubber (SBR). These polymers find extensive applications in packaging, automotive components, construction materials, and consumer goods.

How is styrene produced?

Styrene is predominantly produced through the dehydrogenation of ethylbenzene, which is itself derived from benzene and ethylene. Another significant method involves the co-production of styrene and propylene oxide (SM/PO process).

What are the environmental concerns related to styrene?

Environmental concerns include the volatility of styrene monomer, which can lead to air emissions during production and use. Additionally, the end-of-life management of styrene-based plastics, particularly polystyrene, contributes to plastic waste, driving demand for recycling and bio-based alternatives.

What factors drive the growth of the styrene market?

The styrene market's growth is driven by increasing demand from end-use industries like packaging (e.g., food containers, protective packaging), automotive (e.g., lightweight parts, interiors), and construction (e.g., insulation, pipes). Urbanization, industrialization, and rising disposable incomes in emerging economies also contribute significantly.

What are the future trends for the styrene market?

Future trends in the styrene market include a strong focus on sustainability through the development of bio-based styrene and advanced chemical recycling technologies for polystyrene. Additionally, increased adoption of styrene in high-performance materials and the integration of AI for operational optimization are emerging trends.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted