Student And Worker Non residential Accommodation Market

Student And Worker Non residential Accommodation Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702225 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

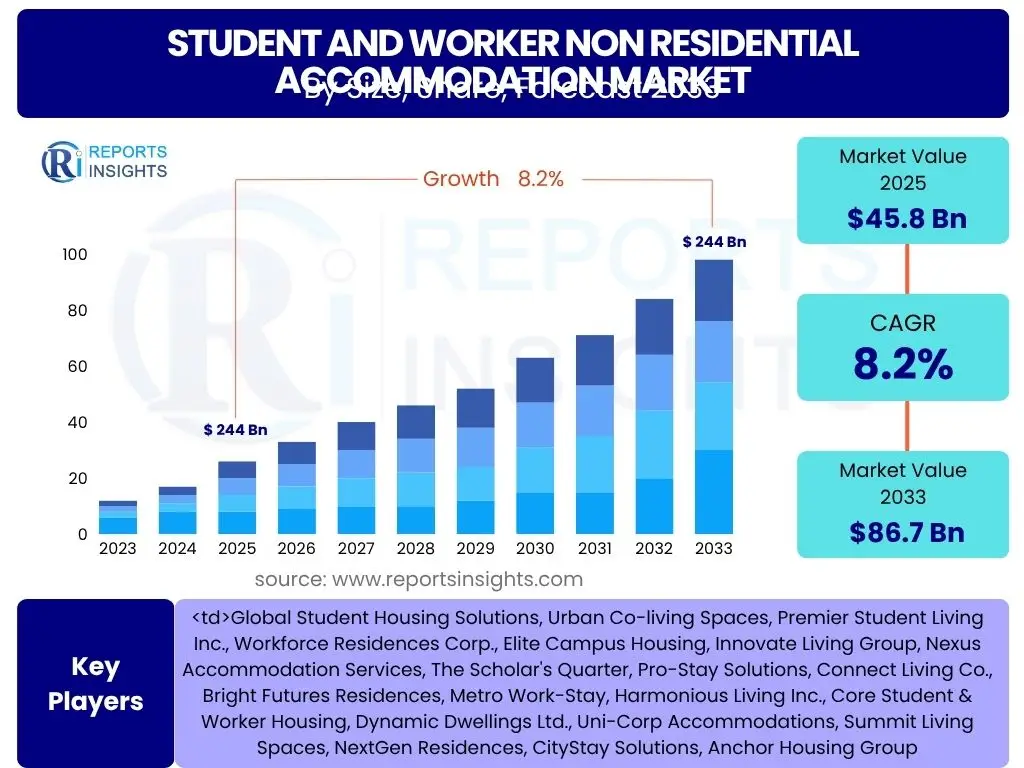

Student And Worker Non residential Accommodation Market Size

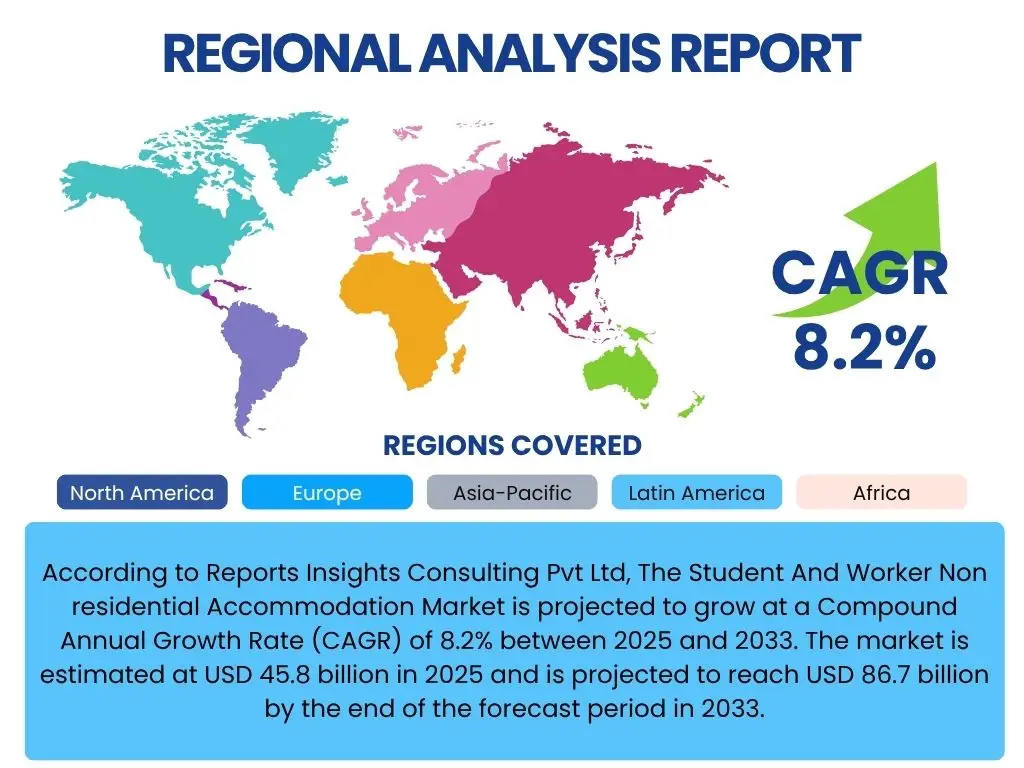

According to Reports Insights Consulting Pvt Ltd, The Student And Worker Non residential Accommodation Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.2% between 2025 and 2033. The market is estimated at USD 45.8 billion in 2025 and is projected to reach USD 86.7 billion by the end of the forecast period in 2033.

Key Student And Worker Non residential Accommodation Market Trends & Insights

The Student And Worker Non residential Accommodation market is undergoing significant transformations driven by evolving socio-economic patterns and technological advancements. Key insights reveal a persistent demand for flexible, amenity-rich, and community-oriented living solutions. Urbanization continues to be a primary driver, leading to increased pressure on housing markets in major cities globally, thereby enhancing the appeal of purpose-built accommodation for specific demographics. The rise of the gig economy and remote work has also blurred traditional lines between professional and personal living, fostering demand for spaces that integrate work, leisure, and social interaction.

Furthermore, there is a growing emphasis on sustainability and well-being within the sector. Developers and operators are increasingly incorporating eco-friendly designs, energy-efficient systems, and wellness programs to attract and retain tenants. The market also reflects a shift towards more digitalized operations, from online booking and virtual tours to smart living technologies within units. This focus on convenience, personalization, and a sense of belonging is shaping new service models and property types, moving beyond basic accommodation to comprehensive lifestyle offerings.

The market is also witnessing an increased interest from institutional investors, recognizing the stable and often counter-cyclical nature of demand for student and worker housing. This influx of capital supports larger-scale developments and the professionalization of property management. The ability to cater to diverse needs, from short-term project workers to long-term international students, necessitates agile business models and a deep understanding of tenant preferences, leading to highly customized and segmented market approaches.

- Growing demand for co-living and flexible lease models.

- Increased focus on sustainability and smart building technologies.

- Integration of health, wellness, and community-centric amenities.

- Digitization of booking, management, and tenant services.

- Rising institutional investment in purpose-built accommodation.

AI Impact Analysis on Student And Worker Non residential Accommodation

The integration of Artificial Intelligence (AI) is set to significantly reshape the Student And Worker Non residential Accommodation sector by enhancing operational efficiencies, improving tenant experiences, and optimizing asset management. AI-powered platforms can streamline various processes, from initial tenant screening and lease management to maintenance scheduling and personalized communication. Predictive analytics, driven by AI, can forecast occupancy rates, identify peak demand periods, and optimize pricing strategies, leading to higher revenue yields and reduced vacancies. This allows operators to make data-driven decisions that enhance profitability and service quality.

Beyond operational improvements, AI can profoundly impact the tenant experience. AI-driven chatbots and virtual assistants can provide instant support for inquiries, amenity bookings, and issue reporting, offering 24/7 responsiveness. Smart building systems, powered by AI, can personalize environmental controls, optimize energy consumption based on occupancy patterns, and enhance security through advanced surveillance and access control. This level of personalization and responsiveness contributes to greater tenant satisfaction and retention, creating a more attractive living environment.

The long-term impact of AI also extends to new service offerings and business models. AI can facilitate the creation of highly customized living packages, matching tenants with specific room types, amenities, and community activities based on their profiles and preferences. Furthermore, AI can aid in the design and development phases of new properties by analyzing vast datasets on urban planning, demographics, and real estate trends, ensuring that new accommodations are strategically located and optimally designed to meet future demand. The ethical considerations around data privacy and algorithmic bias, however, remain critical areas for careful management as AI adoption expands.

- Enhanced operational efficiency through AI-powered property management systems.

- Personalized tenant experiences via smart amenities and virtual assistants.

- Optimized pricing and occupancy management using predictive analytics.

- Streamlined maintenance and security with AI-driven monitoring.

- Data-driven insights for strategic development and investment decisions.

Key Takeaways Student And Worker Non residential Accommodation Market Size & Forecast

The Student And Worker Non residential Accommodation market is poised for robust expansion, driven by urbanization, demographic shifts, and the evolving nature of work and education. The projected growth to USD 86.7 billion by 2033 underscores a significant opportunity for investors and operators, reflecting sustained demand for purpose-built, professionally managed housing. This growth is not merely quantitative but also qualitative, emphasizing a shift towards more flexible, amenity-rich, and technologically integrated living solutions that cater to the modern tenant's needs for convenience, community, and well-being. The market's resilience, even amidst economic fluctuations, highlights its fundamental role in urban infrastructure and talent attraction.

A crucial takeaway is the increasing institutionalization of the sector, which is bringing greater professionalism, standardization, and scale to what was once a fragmented market. This trend is facilitating larger investments in new developments and the acquisition of existing portfolios, further professionalizing the management and operational standards across the industry. The focus on enhancing the living experience through advanced technology and community programs is becoming a differentiator, moving beyond mere accommodation to comprehensive lifestyle offerings that resonate with both students and temporary workers seeking more than just a place to stay.

Furthermore, the market's trajectory is heavily influenced by underlying global trends such as increased student mobility, the rise of the gig economy, and corporate relocations. These factors create a diverse tenant base requiring tailored solutions, from short-term stays for project-based workers to academic year leases for students. Operators who can successfully navigate these diverse demands by offering adaptable living arrangements, integrating smart technologies, and prioritizing tenant satisfaction will be best positioned to capitalize on the market's significant growth potential. The market outlook remains highly positive, signaling a continuous evolution in living solutions to meet dynamic global needs.

- Substantial market growth projected to USD 86.7 billion by 2033.

- Demand for purpose-built, professionally managed, and amenity-rich spaces is accelerating.

- Institutional investment is professionalizing and expanding the sector.

- Technological integration and personalization are key to tenant satisfaction.

- Market resilience driven by fundamental demographic and economic shifts.

Student And Worker Non residential Accommodation Market Drivers Analysis

The expansion of the Student And Worker Non residential Accommodation market is primarily propelled by several robust macroeconomic and demographic trends. Increased urbanization globally continues to concentrate populations in urban centers, leading to acute housing shortages and driving up rental costs, thereby making purpose-built, managed accommodations an attractive and often more affordable alternative for students and workers. This demographic shift, coupled with the rising mobility of students seeking higher education abroad and the flexible nature of modern employment, contributes significantly to sustained demand for temporary and semi-permanent housing solutions. The proliferation of corporate assignments and the gig economy further necessitate flexible, well-located accommodation options beyond traditional hotels.

Moreover, the growing preference for community-oriented living, especially among younger demographics, is a significant driver. Students and young professionals often seek environments that offer social interaction, shared amenities, and a sense of belonging, which is precisely what modern non-residential accommodations are designed to provide. This desire for convenience, safety, and a curated living experience, often bundled with utilities and services, removes many of the logistical challenges associated with traditional private rentals. The increasing number of international students and workers also fuels this demand, as they often require fully furnished and managed housing solutions upon arrival in a new country or city.

The professionalization of the sector, attracting significant institutional capital, also acts as a driver. Large-scale investments enable developers to build high-quality, amenity-rich properties at scale, meeting the demand more efficiently and offering competitive pricing. These professional operators bring expertise in management, marketing, and tenant services, enhancing the overall appeal and reliability of the accommodation. Furthermore, government policies in some regions, aimed at attracting skilled labor or supporting educational hubs, inadvertently boost the demand for such accommodations by creating a more conducive environment for foreign talent and students.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Urbanization and Population Density | +0.8% | Global, particularly Asia Pacific, North America | Long-term (5+ years) |

| Rising Student Mobility and International Enrollment | +0.6% | Europe, North America, Australia | Mid-term (3-5 years) |

| Growth of Gig Economy and Flexible Work Models | +0.7% | North America, Europe, Asia Pacific | Short-term (1-3 years) |

| Preference for Amenity-Rich, Community-Oriented Living | +0.5% | Globally, strong in developed markets | Mid-term (3-5 years) |

| Increased Corporate Relocations and Project-Based Work | +0.4% | Global business hubs | Short-term (1-3 years) |

Student And Worker Non residential Accommodation Market Restraints Analysis

Despite the positive growth trajectory, the Student And Worker Non residential Accommodation market faces several significant restraints that could impede its full potential. High capital expenditure is a primary barrier, as developing purpose-built student and worker accommodation requires substantial upfront investment in land acquisition, construction, and fitting out. This high entry barrier can deter smaller developers and restrict the pace of new supply, particularly in prime urban locations where land costs are exceptionally high. Financing such large-scale projects can also be challenging, requiring robust financial backing and favorable lending conditions.

Regulatory hurdles and complex planning permissions also present a notable restraint. Local zoning laws, building codes, and community resistance (NIMBYism – Not In My Backyard) can significantly delay or even halt development projects. Navigating diverse and often stringent regulations across different municipalities and countries adds complexity and cost to development, slowing down market expansion. Concerns about increased local traffic, noise, and changes to neighborhood character often lead to opposition from existing residents, making it difficult to secure approvals for new developments.

Economic downturns and fluctuations in disposable income can directly impact demand. During periods of economic instability, prospective students might opt for more affordable education options or defer enrollment, while companies might reduce temporary assignments or relocation budgets. This directly affects occupancy rates and rental yields for accommodation providers. Furthermore, intense competition from private landlords and traditional rental markets, especially during periods of high vacancy, can exert downward pressure on rental prices, impacting the profitability of purpose-built accommodation providers who often offer premium services at higher price points.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure and Development Costs | -0.7% | Global, especially prime urban areas | Long-term (5+ years) |

| Stringent Regulatory Frameworks and Planning Hurdles | -0.6% | Europe, North America | Mid-term (3-5 years) |

| Economic Downturns and Reduced Disposable Income | -0.5% | Global, particularly emerging markets | Short-term (1-3 years) |

| Competition from Traditional Rental Markets | -0.4% | Mature markets with abundant housing stock | Mid-term (3-5 years) |

| Public Opposition and NIMBYism | -0.3% | Developed countries, urban centers | Short-term (1-3 years) |

Student And Worker Non residential Accommodation Market Opportunities Analysis

Significant opportunities exist within the Student And Worker Non residential Accommodation market for strategic growth and innovation. The expansion into underserved niche markets represents a substantial avenue for development. This includes specialized accommodation for postgraduate students, medical residents, vocational trainees, or specific corporate sectors requiring extended stay options. Identifying and catering to these distinct segments with tailored amenities and services can unlock new revenue streams and establish market leadership in specific niches that are less saturated than general student housing. This diversification moves beyond a one-size-fits-all approach to highly specialized offerings.

Technological integration presents another major opportunity, particularly in leveraging smart building technologies, AI-driven management platforms, and personalized digital services. Implementing advanced booking systems, virtual tours, IoT-enabled amenities (e.g., smart locks, climate control), and predictive maintenance can significantly enhance operational efficiency, reduce costs, and improve the overall tenant experience. Furthermore, data analytics derived from these technologies can provide invaluable insights into tenant preferences and building performance, enabling continuous optimization and personalized service delivery, which are key differentiators in a competitive market.

The growing emphasis on sustainability and ESG (Environmental, Social, and Governance) principles offers a unique opportunity for market differentiation and attracting environmentally conscious tenants and investors. Developing green buildings, implementing renewable energy sources, waste reduction programs, and fostering strong community engagement can not only reduce operational costs but also enhance brand reputation and appeal. Exploring partnerships with educational institutions, corporations, and local governments to provide dedicated accommodation solutions can also secure long-term contracts and stable occupancy rates, creating mutually beneficial relationships and expanding market reach into previously untapped institutional demand. The potential for retrofitting older properties to meet modern standards and demands also presents a significant refurbishment and redevelopment opportunity.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Underserved Niche Markets | +0.9% | Global, particularly emerging cities | Mid-term (3-5 years) |

| Advanced Technology Integration (Smart Buildings, AI) | +0.8% | Developed markets, tech-forward regions | Long-term (5+ years) |

| Focus on Sustainability and ESG Practices | +0.7% | Europe, North America, APAC | Mid-term (3-5 years) |

| Partnerships with Educational Institutions and Corporations | +0.6% | Globally, urban and university towns | Short-term (1-3 years) |

| Redevelopment and Repurposing Existing Structures | +0.5% | Mature urban centers with older housing stock | Long-term (5+ years) |

Student And Worker Non residential Accommodation Market Challenges Impact Analysis

The Student And Worker Non residential Accommodation market is confronted by several significant challenges that require careful navigation from operators and investors. Fluctuating demand patterns pose a constant operational challenge. Student accommodation, for instance, typically experiences cyclical demand peaking during academic years and declining during holidays, leading to periods of lower occupancy. Similarly, demand for worker accommodation can be influenced by project cycles, economic conditions, and corporate hiring trends. Managing these ebbs and flows requires flexible operational strategies, diverse tenant acquisition approaches, and potentially variable pricing models to maintain profitability and occupancy rates year-round.

Maintaining high-quality facilities and managing rising operational costs are continuous concerns. Non-residential accommodations, particularly those offering extensive amenities, incur significant expenses related to maintenance, utilities, security, and staff salaries. The wear and tear associated with high tenant turnover, especially in student housing, necessitates ongoing refurbishment and upkeep, which can be capital-intensive. Balancing the provision of premium services with cost efficiencies is crucial for long-term financial viability, especially as inflation impacts material and labor costs.

Furthermore, evolving tenant expectations present a dynamic challenge. Today's students and workers are increasingly sophisticated, demanding not only basic accommodation but also high-speed internet, collaborative workspaces, wellness facilities, and vibrant community programs. Meeting these diverse and often evolving expectations requires continuous investment in amenities and services, as well as innovative approaches to community building. The rapid pace of technological change also necessitates ongoing investment in digital infrastructure to remain competitive. Geopolitical instabilities and global health crises, as evidenced by recent events, also pose unpredictable challenges, impacting international mobility and, consequently, demand for accommodation in specific regions, requiring quick adaptation and robust contingency planning.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Fluctuating Demand and Occupancy Rates | -0.8% | Global, seasonal markets | Short-term (1-3 years) |

| Rising Operational and Maintenance Costs | -0.7% | Global, particularly high-cost regions | Mid-term (3-5 years) |

| Evolving Tenant Expectations and Amenities Demands | -0.6% | Developed markets, competitive urban centers | Long-term (5+ years) |

| Talent Retention and Staffing Challenges | -0.5% | Global, particularly hospitality sector | Short-term (1-3 years) |

| Geopolitical Instability and Health Crises | -0.4% | Global, region-specific impact | Short-term (1-3 years) |

Student And Worker Non residential Accommodation Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Student And Worker Non residential Accommodation market, encompassing historical data, current market dynamics, and future projections. It delivers critical insights into market size, growth drivers, restraints, opportunities, and challenges affecting the industry landscape from 2019 to 2033. The scope includes detailed segmentation analysis by accommodation type, end-user, and service model, alongside a thorough regional and country-level examination. It also incorporates the impact of emerging technologies like AI and sustainability trends on market evolution, offering a holistic view for stakeholders to make informed strategic decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 45.8 billion |

| Market Forecast in 2033 | USD 86.7 billion |

| Growth Rate | 8.2% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Student Housing Solutions, Urban Co-living Spaces, Premier Student Living Inc., Workforce Residences Corp., Elite Campus Housing, Innovate Living Group, Nexus Accommodation Services, The Scholar's Quarter, Pro-Stay Solutions, Connect Living Co., Bright Futures Residences, Metro Work-Stay, Harmonious Living Inc., Core Student & Worker Housing, Dynamic Dwellings Ltd., Uni-Corp Accommodations, Summit Living Spaces, NextGen Residences, CityStay Solutions, Anchor Housing Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Student And Worker Non residential Accommodation market is highly diverse, and its segmentation reflects the varied needs of its distinct user bases. Understanding these segments is crucial for operators to tailor their offerings effectively and for investors to identify lucrative opportunities. The primary segmentation categories encompass the type of accommodation provided, the specific end-user demographic, and the operational service model, each influencing demand, pricing, and required amenities. This granular view allows for a more precise strategic approach to market penetration and service delivery, ensuring that offerings are aligned with specific tenant expectations and operational capabilities.

Within accommodation types, Purpose-Built Student Accommodation (PBSA) and Co-Living Spaces represent the most dynamic and rapidly expanding segments, catering to different but often overlapping preferences for community and amenities. Serviced Apartments and Corporate Housing cater more to the professional demographic seeking comfort, privacy, and flexible terms for longer stays. Each type offers a unique value proposition, from the academic-focused environment of PBSA to the social and flexible nature of co-living, impacting development decisions and market positioning. Operators must analyze the dominant characteristics of their target regions to determine the most viable accommodation type.

The end-user segmentation clearly distinguishes between students (university, vocational) and workers (corporate, gig economy, project-based), as their accommodation needs, budget constraints, and duration of stay can vary significantly. Service models, ranging from fully managed to self-catered or hybrid approaches, dictate the level of support and services provided, impacting operational costs and tenant satisfaction. This multi-layered segmentation allows stakeholders to identify specific underserved niches and develop highly targeted solutions, optimizing resource allocation and maximizing market relevance in a competitive landscape.

- By Accommodation Type:

- Purpose-Built Student Accommodation (PBSA): Dedicated facilities for students, often near educational institutions, offering a range of amenities.

- Co-Living Spaces: Shared living environments designed for community, often catering to young professionals or students, emphasizing shared communal areas and social events.

- Serviced Apartments: Fully furnished apartments with hotel-like services, popular among corporate travelers and those seeking short to medium-term stays with amenities.

- Corporate Housing: Furnished accommodation specifically for business travelers or relocating employees, often arranged by companies.

- Hostel-Style Accommodation: Budget-friendly options, often with shared rooms and facilities, catering to transient workers or students on a tight budget.

- By End-User:

- University Students: Including undergraduate, postgraduate, and international students.

- Vocational Students: Attending technical schools, apprenticeships, or specialized training.

- Corporate Employees: Individuals on business trips, training, or relocation assignments.

- Gig Economy Workers: Freelancers, contractors, and temporary staff seeking flexible housing.

- Project-Based Professionals: Individuals on short-term projects requiring temporary accommodation.

- By Service Model:

- Fully Managed: Comprehensive services including cleaning, security, maintenance, and community management.

- Self-Catered: Provides accommodation only, with tenants responsible for their own services.

- Hybrid Models: A combination of managed services and self-catered options, offering flexibility.

Regional Highlights

- North America: The market in North America is characterized by robust demand for both student housing and corporate extended-stay solutions, particularly in major university towns and economic hubs. The region benefits from a large student population, including a significant influx of international students, driving demand for PBSA. Concurrently, the dynamic corporate sector and the rise of remote work hubs fuel the need for flexible worker accommodations. Investment here is driven by institutional capital seeking stable returns, leading to the development of high-quality, amenity-rich properties. However, high land costs and stringent zoning regulations in key cities pose challenges.

- Europe: Europe presents a highly diversified market, influenced by differing national educational systems, labor mobility, and urban development policies. Western European countries, like the UK, Germany, and Spain, have mature student housing markets with strong institutional investment, while Eastern European nations are emerging, offering growth potential at lower development costs. Co-living is gaining significant traction across major European cities due to urbanization and affordability challenges. The region's extensive network of universities and multinational corporations ensures a steady demand, but regulatory fragmentation across countries requires localized strategies.

- Asia Pacific (APAC): The APAC region is experiencing the most rapid growth in the non-residential accommodation market, driven by massive urbanization, a burgeoning middle class, and increasing enrollment in higher education, particularly from China, India, and Southeast Asian countries. Demand for modern, secure, and well-managed student housing is surging. Economic growth also fuels corporate travel and project-based work, supporting the expansion of serviced apartments and co-living spaces. Government initiatives to attract foreign talent and promote education hubs further contribute to market expansion, though varied regulatory landscapes and infrastructure disparities exist.

- Latin America: The Latin American market for non-residential accommodation is still in its nascent stages compared to developed regions but shows significant potential. Growth is primarily driven by increasing urbanization, a growing youth population seeking higher education, and foreign direct investment in key industrial and commercial centers. Brazil, Mexico, and Colombia are emerging as significant markets for student and worker accommodation, particularly in their respective capitals and major economic cities. Challenges include economic volatility, less developed regulatory frameworks, and a reliance on local developers, but opportunities for first-mover advantage remain high.

- Middle East and Africa (MEA): The MEA region offers a mixed landscape. In the Middle East, particularly the GCC countries, demand is largely driven by expatriate workers, skilled professionals, and a burgeoning higher education sector aiming to become regional academic hubs. Luxury serviced apartments and corporate housing are prominent. African markets are less developed but exhibit long-term potential fueled by rapid urbanization, infrastructure development, and growing educational aspirations. Challenges include political instability in some areas, diverse economic conditions, and a need for significant investment in modern accommodation infrastructure.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Student And Worker Non residential Accommodation Market.- Global Student Housing Solutions

- Urban Co-living Spaces

- Premier Student Living Inc.

- Workforce Residences Corp.

- Elite Campus Housing

- Innovate Living Group

- Nexus Accommodation Services

- The Scholar's Quarter

- Pro-Stay Solutions

- Connect Living Co.

- Bright Futures Residences

- Metro Work-Stay

- Harmonious Living Inc.

- Core Student & Worker Housing

- Dynamic Dwellings Ltd.

- Uni-Corp Accommodations

- Summit Living Spaces

- NextGen Residences

- CityStay Solutions

- Anchor Housing Group

Frequently Asked Questions

What is the projected growth rate of the Student And Worker Non residential Accommodation Market?

The Student And Worker Non residential Accommodation Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.2% between 2025 and 2033, reaching an estimated USD 86.7 billion by 2033.

What key factors are driving the demand for non-residential accommodation?

Key drivers include increasing urbanization, rising student mobility for higher education, the expansion of the gig economy, growing corporate relocations, and a strong preference for amenity-rich, community-oriented living spaces among target demographics.

How is AI impacting the non-residential accommodation sector?

AI is transforming the sector by enhancing operational efficiency through smart property management, optimizing pricing and occupancy, personalizing tenant experiences via smart amenities and virtual assistants, and providing data-driven insights for strategic development and maintenance.

What are the main challenges faced by this market?

Significant challenges include fluctuating demand and occupancy rates due to seasonality or economic shifts, rising operational and maintenance costs, evolving tenant expectations for advanced amenities, and complex regulatory environments coupled with community opposition to new developments.

Which regions offer the most significant growth opportunities?

Asia Pacific is experiencing the most rapid growth due to urbanization and large student populations. Europe and North America remain mature markets with strong institutional investment, while Latin America and parts of the Middle East and Africa present emerging opportunities driven by infrastructure development and increasing mobility.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted