Steel Rebar Market

Steel Rebar Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704542 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

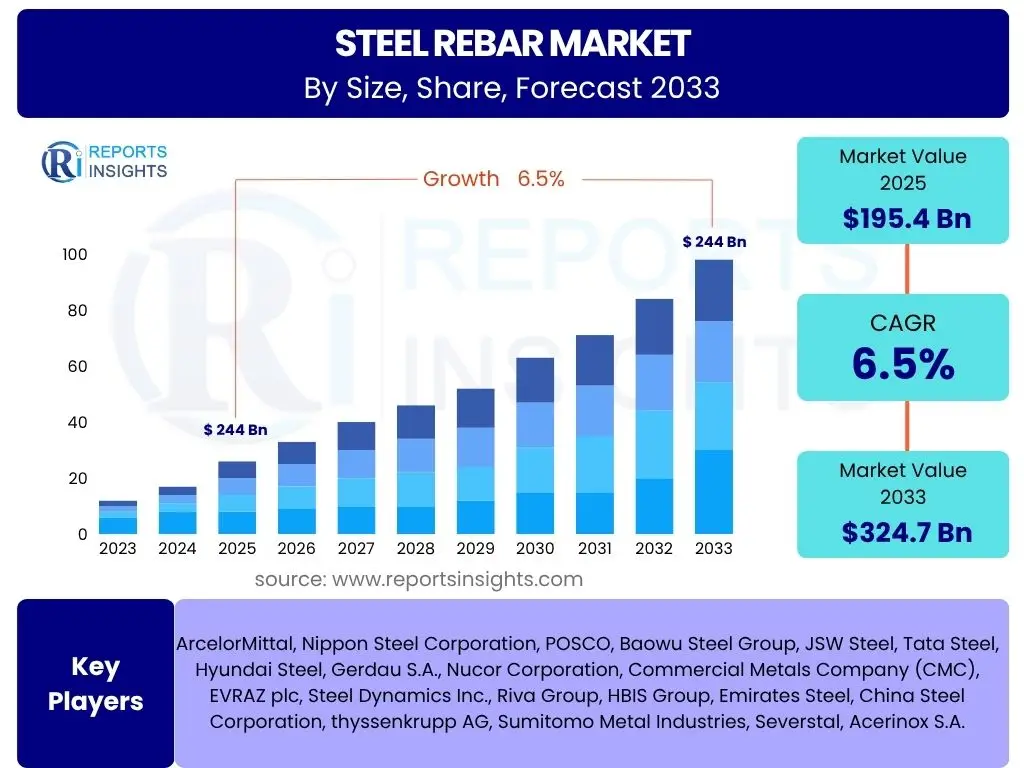

Steel Rebar Market Size

According to Reports Insights Consulting Pvt Ltd, The Steel Rebar Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 195.4 Billion in 2025 and is projected to reach USD 324.7 Billion by the end of the forecast period in 2033.

Key Steel Rebar Market Trends & Insights

User queries regarding the Steel Rebar market frequently center on evolving construction practices, material innovations, and the industry's response to environmental demands. Analysis reveals a prominent shift towards sustainable production methods, driven by increasing regulatory pressures and growing awareness of carbon footprints. Furthermore, technological advancements in manufacturing processes, such as improved rolling techniques and metallurgical enhancements, are leading to the development of higher-strength and more corrosion-resistant rebar, addressing critical durability concerns in infrastructure projects.

Another significant trend is the increasing adoption of prefabricated and modular construction, which demands precise, high-quality rebar components and reduces on-site labor and waste. Digitalization across the construction supply chain, including Building Information Modeling (BIM) and digital twin technologies, is streamlining rebar specification, procurement, and installation. The robust demand from developing economies, particularly for urban infrastructure and housing, continues to be a foundational driver, while developed markets focus on renovation, seismic retrofitting, and specialized high-performance applications.

- Growing demand for sustainable and green rebar solutions.

- Advancements in high-strength and corrosion-resistant rebar technologies.

- Increasing adoption of prefabricated and modular construction methods.

- Digitalization and integration of Building Information Modeling (BIM) in construction.

- Focus on circular economy principles in steel production and recycling.

- Expansion of infrastructure projects globally, particularly in emerging economies.

AI Impact Analysis on Steel Rebar

User inquiries concerning the impact of Artificial Intelligence (AI) on the Steel Rebar market highlight a strong interest in how AI can optimize manufacturing, improve supply chain efficiency, and enhance quality control. There is an expectation that AI will lead to more predictive and precise production processes, minimizing waste and energy consumption. Users are keen to understand how AI-driven analytics can forecast demand fluctuations, manage inventory more effectively, and identify potential bottlenecks in the raw material supply chain, thus mitigating risks and improving operational resilience.

Furthermore, AI is anticipated to play a crucial role in the design and engineering phases of construction, enabling advanced simulations for structural integrity and material performance. Predictive maintenance for manufacturing machinery, AI-powered quality inspection systems, and optimized logistics for rebar delivery are other areas of significant user curiosity. The overall sentiment suggests that AI will drive a transformation towards more intelligent, efficient, and sustainable steel rebar production and utilization, though concerns about data security, integration costs, and workforce retraining also emerge.

- Optimized production planning and scheduling through AI algorithms.

- Predictive maintenance for steel manufacturing equipment, reducing downtime.

- Enhanced supply chain visibility and efficiency, from raw materials to delivery.

- AI-driven quality control and defect detection in rebar production.

- Improved demand forecasting and inventory management using machine learning.

- Potential for AI-assisted structural design and material optimization.

Key Takeaways Steel Rebar Market Size & Forecast

User questions about key takeaways from the Steel Rebar market size and forecast often revolve around the drivers of long-term growth, the resilience of the market against economic fluctuations, and the primary regional contributors to its expansion. The analysis indicates that the market is poised for robust and sustained growth, primarily fueled by global urbanization trends and substantial investments in infrastructure development, particularly in Asian and African economies. The forecast reflects an underlying demand for foundational construction materials that is less susceptible to short-term economic volatilities compared to other sectors.

Another crucial insight is the increasing emphasis on sustainable and resilient construction, which will necessitate high-quality, durable rebar. The market's upward trajectory is also supported by government initiatives promoting smart cities and advanced transportation networks, which require significant quantities of steel rebar. Despite potential challenges such as raw material price volatility, the fundamental need for housing, commercial spaces, and critical infrastructure ensures a positive outlook, with technological advancements and innovative applications contributing significantly to future market expansion.

- Consistent and robust growth projected, driven by global infrastructure development.

- Urbanization and population growth are primary accelerators for rebar demand.

- Asia Pacific continues to be a dominant market, with significant growth in South Asia and Southeast Asia.

- Increased focus on resilient and sustainable construction methods supports demand for advanced rebar.

- Government investments in public infrastructure and smart city projects are key market stimulants.

- Technological advancements in rebar manufacturing contribute to market stability and innovation.

Steel Rebar Market Drivers Analysis

The Steel Rebar market is propelled by a confluence of macroeconomic and industry-specific factors that collectively stimulate demand. Foremost among these is the escalating pace of urbanization across developing nations, leading to a substantial need for residential and commercial infrastructure. Governments globally are also committing significant capital to public works projects, including roads, bridges, railways, and utilities, all of which are highly dependent on steel rebar for structural integrity. This consistent investment creates a stable and growing demand base.

Furthermore, the global population growth directly translates into increased demand for housing, necessitating more construction activity and, consequently, more rebar. Industrialization in emerging economies also drives the construction of manufacturing facilities, warehouses, and power plants, further boosting rebar consumption. The resilience and adaptability of steel rebar as a foundational construction material make it indispensable for modern building practices, ensuring its sustained market relevance amidst evolving architectural and engineering demands.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Urbanization and Population Growth | +1.8% | Asia Pacific, Africa, Latin America | Long-term (2025-2033) |

| Increased Government Infrastructure Spending | +1.5% | Global, particularly India, China, USA, Southeast Asia | Medium to Long-term (2025-2030) |

| Growth in Residential and Commercial Construction | +1.2% | Global, especially emerging economies | Long-term (2025-2033) |

| Reconstruction and Renovation Activities | +0.8% | Developed regions (Europe, North America) | Medium-term (2025-2029) |

| Technological Advancements in Steel Manufacturing | +0.5% | Global | Long-term (2025-2033) |

Steel Rebar Market Restraints Analysis

Despite its inherent demand, the Steel Rebar market faces several significant restraints that can impede its growth trajectory. The most prominent challenge is the high volatility in raw material prices, particularly for iron ore and steel scrap. Fluctuations in these commodity prices directly impact production costs for rebar manufacturers, leading to unstable pricing, reduced profit margins, and increased financial risk. This volatility makes long-term planning and fixed-price contracts difficult, creating uncertainty across the supply chain.

Environmental regulations and stringent carbon emission reduction targets also pose a substantial restraint, especially in regions with mature economies. Steel production is energy-intensive and has a significant carbon footprint, requiring substantial investments in cleaner technologies and sustainable practices. Compliance costs can increase the overall production expenditure, potentially affecting the competitiveness of rebar in the market. Furthermore, economic downturns or recessions can lead to a slowdown in construction activities, directly impacting rebar demand and market growth. Labor shortages in the construction and manufacturing sectors, coupled with high energy costs for production, further complicate the operational landscape for rebar manufacturers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices (Iron Ore, Scrap) | -1.2% | Global | Short to Medium-term (2025-2028) |

| Stringent Environmental Regulations and Carbon Emission Targets | -0.9% | Europe, North America, China | Long-term (2025-2033) |

| Economic Slowdowns and Recessionary Pressures | -0.7% | Global, variable by region | Short-term (2025-2026) |

| High Energy Costs for Steel Production | -0.6% | Europe, North America, Asia Pacific | Medium-term (2025-2029) |

| Labor Shortages and Skilled Workforce Availability | -0.4% | Developed economies | Medium to Long-term (2025-2033) |

Steel Rebar Market Opportunities Analysis

The Steel Rebar market is ripe with opportunities that can significantly accelerate its growth and evolution. A major area of opportunity lies in the burgeoning demand for sustainable and green building materials. As environmental consciousness grows and regulations tighten, there is increasing incentive for manufacturers to produce rebar with lower carbon footprints, utilizing recycled content, and employing energy-efficient production processes. This shift caters to the rising trend of green construction and offers a competitive edge to innovators.

Another substantial opportunity stems from the global push for smart city development and advanced infrastructure projects. These initiatives often require high-performance rebar with enhanced properties, such as superior corrosion resistance for coastal or seismic zones, or specialized applications in resilient structures. The development of advanced rebar technologies, including fiber-reinforced polymer (FRP) rebar or high-strength steel rebar, presents a niche but growing market segment. Furthermore, the expansion into untapped or under-penetrated markets, particularly in emerging African and Southeast Asian economies, offers significant avenues for market penetration and volume growth as these regions embark on massive urbanization and infrastructure build-outs. Strategic collaborations and technological licensing also offer avenues for market expansion and innovation adoption.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Green and Sustainable Rebar | +1.0% | Global, particularly Europe, North America, APAC | Long-term (2025-2033) |

| Investments in Smart City and Advanced Infrastructure Projects | +0.9% | Global, especially China, India, Middle East, USA | Long-term (2025-2033) |

| Development of Advanced Rebar Technologies (e.g., Corrosion-resistant, FRP) | +0.8% | Developed economies, specific niche markets | Medium to Long-term (2026-2033) |

| Expansion into Emerging Markets (Africa, Southeast Asia) | +0.7% | Africa, ASEAN countries, Latin America | Long-term (2025-2033) |

| Increased Adoption of Prefabricated Construction | +0.6% | Global | Medium-term (2025-2030) |

Steel Rebar Market Challenges Impact Analysis

The Steel Rebar market faces several inherent challenges that demand strategic responses from industry players. One significant challenge is the highly competitive landscape, characterized by numerous domestic and international manufacturers. This intense competition often leads to price wars, reduced profit margins, and a struggle for market share, making it difficult for new entrants or smaller players to establish a strong foothold. Maintaining product differentiation and competitive pricing in such an environment requires continuous innovation and operational efficiency.

Another major challenge involves navigating complex and dynamic regulatory frameworks across different regions and countries. Compliance with varying building codes, quality standards, and environmental regulations can be onerous and costly, particularly for companies operating globally. Supply chain disruptions, often triggered by geopolitical events, natural disasters, or pandemics, pose a persistent threat to timely raw material procurement and product delivery, impacting production schedules and profitability. Furthermore, the capital-intensive nature of steel manufacturing necessitates substantial initial investments and ongoing expenditures for maintenance and upgrades, which can be a barrier for new players and a financial strain for existing ones, especially during economic downturns. These challenges require robust risk management, agile supply chain strategies, and a strong commitment to regulatory adherence.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Market Competition and Price Pressures | -1.0% | Global | Long-term (2025-2033) |

| Complex and Evolving Regulatory Environment | -0.8% | Europe, North America, specific Asian countries | Long-term (2025-2033) |

| Supply Chain Disruptions and Logistics Challenges | -0.7% | Global | Short to Medium-term (2025-2027) |

| Capital-Intensive Nature of Manufacturing | -0.6% | Global | Long-term (2025-2033) |

| Fluctuations in Construction Sector Demand | -0.5% | Global, variable by regional economic cycles | Short-term (2025-2026) |

Steel Rebar Market - Updated Report Scope

This market research report offers a comprehensive analysis of the global Steel Rebar market, providing an in-depth understanding of market dynamics, segmentation, and regional landscapes. It encompasses historical data, current trends, and forward-looking projections to offer strategic insights for stakeholders. The report meticulously examines market size, growth drivers, restraints, opportunities, and challenges, along with the competitive scenario and profiles of key industry players.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 195.4 Billion |

| Market Forecast in 2033 | USD 324.7 Billion |

| Growth Rate | 6.5% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ArcelorMittal, Nippon Steel Corporation, POSCO, Baowu Steel Group, JSW Steel, Tata Steel, Hyundai Steel, Gerdau S.A., Nucor Corporation, Commercial Metals Company (CMC), EVRAZ plc, Steel Dynamics Inc., Riva Group, HBIS Group, Emirates Steel, China Steel Corporation, thyssenkrupp AG, Sumitomo Metal Industries, Severstal, Acerinox S.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The global Steel Rebar market is comprehensively segmented to provide a detailed understanding of its various facets and their respective contributions to the overall market dynamics. This segmentation facilitates a granular analysis, allowing stakeholders to identify high-growth areas, understand consumer preferences, and tailor strategies to specific market niches. The primary segmentation criteria include the type of rebar, the manufacturing process employed, the specific application areas, and the broader end-use industries.

Each segment exhibits unique characteristics and growth trajectories driven by distinct market forces. For instance, deformed rebar, due to its enhanced bonding properties, dominates residential and commercial construction, while mild rebar finds applications where less stringent structural requirements are present. The distinction between Basic Oxygen Furnace (BOF) and Electric Arc Furnace (EAF) processes highlights the industry's shift towards more environmentally sustainable production methods, with EAF gaining prominence for its ability to utilize recycled steel. Analyzing these segments helps in comprehending the multifaceted nature of the steel rebar industry and its varied demand patterns across different sectors.

- By Type:

- Deformed Rebar

- Mild Rebar

- Others (Epoxy-Coated Rebar, Galvanized Rebar, Stainless Steel Rebar)

- By Process:

- Basic Oxygen Furnace (BOF)

- Electric Arc Furnace (EAF)

- By Application:

- Residential Buildings

- Commercial Buildings (Offices, Retail, Hospitality)

- Infrastructure (Roads, Bridges, Railways, Airports, Dams, Utilities)

- Industrial Structures (Manufacturing Plants, Power Plants, Warehouses)

- By End-Use:

- Construction

- Manufacturing

Regional Highlights

- Asia Pacific (APAC): Dominates the global steel rebar market due to extensive infrastructure development, rapid urbanization, and significant investments in residential and commercial construction, particularly in countries like China, India, and Southeast Asian nations.

- North America: Exhibits stable growth, driven by investments in aging infrastructure upgrades, robust residential construction, and a strong focus on resilient building practices and advanced rebar solutions.

- Europe: A mature market characterized by stringent environmental regulations, a focus on sustainable construction, and renovation projects. Demand is primarily influenced by public infrastructure investments and a move towards green steel production.

- Latin America: An emerging market with increasing demand for rebar fueled by urbanization, housing deficits, and ongoing infrastructure projects, albeit susceptible to economic and political fluctuations.

- Middle East and Africa (MEA): Shows high growth potential, particularly in the GCC countries and parts of Africa, driven by mega-project developments (smart cities, tourism infrastructure) and rapid population growth requiring new housing and basic infrastructure.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Steel Rebar Market.- ArcelorMittal

- Nippon Steel Corporation

- POSCO

- Baowu Steel Group

- JSW Steel

- Tata Steel

- Hyundai Steel

- Gerdau S.A.

- Nucor Corporation

- Commercial Metals Company (CMC)

- EVRAZ plc

- Steel Dynamics Inc.

- Riva Group

- HBIS Group

- Emirates Steel

- China Steel Corporation

- thyssenkrupp AG

- Sumitomo Metal Industries

- Severstal

- Acerinox S.A.

Frequently Asked Questions

What is steel rebar primarily used for?

Steel rebar, or reinforcing bar, is primarily used as a tensioning device in reinforced concrete and masonry structures to strengthen and aid concrete under tension. It is crucial for enhancing the structural integrity and durability of buildings, bridges, roads, and other infrastructure projects.

What are the main factors driving the Steel Rebar market?

The key drivers for the Steel Rebar market include rapid urbanization, increasing global population, significant government investments in infrastructure development, and consistent growth in residential and commercial construction activities worldwide.

What are the different types of steel rebar available?

The main types of steel rebar include deformed rebar, which has ridges for better concrete bonding, and mild rebar, which is plain. Other specialized types include epoxy-coated rebar for corrosion resistance, galvanized rebar, and stainless steel rebar for extreme environments.

How is steel rebar manufactured?

Steel rebar is typically manufactured using two primary processes: the Basic Oxygen Furnace (BOF), which primarily uses virgin iron ore, and the Electric Arc Furnace (EAF), which predominantly uses recycled steel scrap. Both processes involve melting, refining, continuous casting, and hot rolling into the desired bar shape.

What is the future outlook for the Steel Rebar market?

The future outlook for the Steel Rebar market is positive, projected for robust growth driven by ongoing global infrastructure development, sustainable construction initiatives, technological advancements in rebar production, and sustained demand from emerging economies for urbanization and industrialization.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted