Steel Cord Conveyor Belt Market

Steel Cord Conveyor Belt Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705331 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

Steel Cord Conveyor Belt Market Size

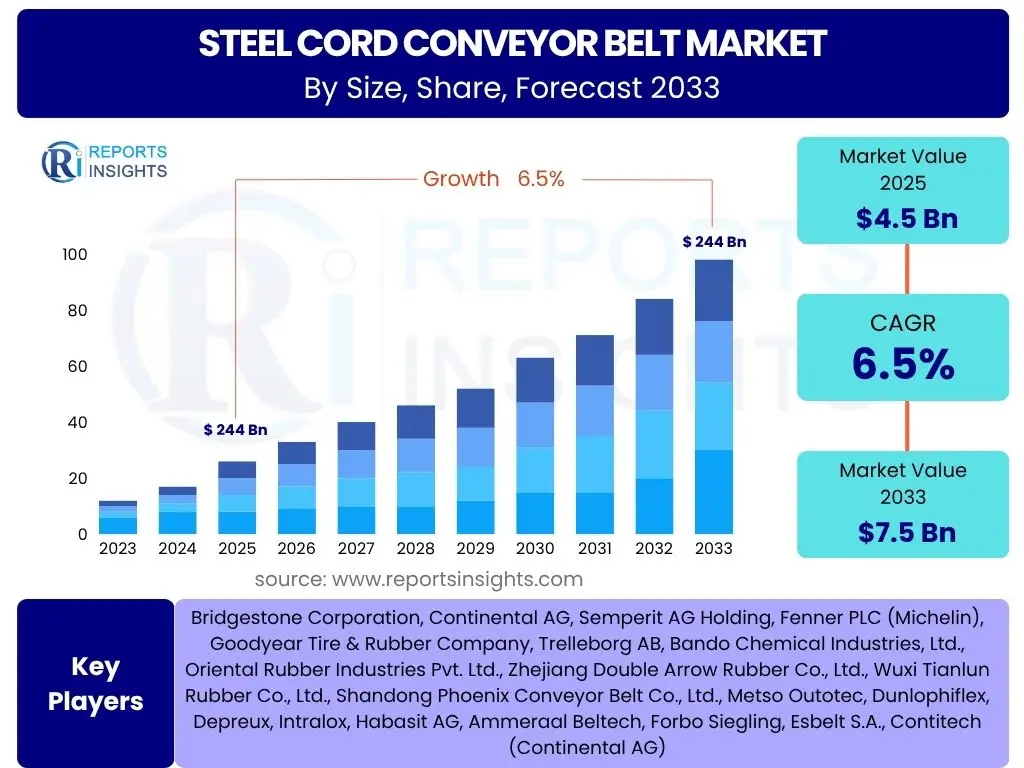

According to Reports Insights Consulting Pvt Ltd, The Steel Cord Conveyor Belt Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 4.5 billion in 2025 and is projected to reach USD 7.5 billion by the end of the forecast period in 2033.

Key Steel Cord Conveyor Belt Market Trends & Insights

The steel cord conveyor belt market is experiencing significant transformation driven by evolving industrial needs and technological advancements. User inquiries frequently highlight the shift towards higher performance and durability, particularly in harsh operating environments such as heavy mining and ports. There is a growing emphasis on intelligent monitoring systems and digital integration, reflecting the broader industry trend towards smart manufacturing and predictive maintenance. Furthermore, sustainability initiatives and the demand for energy-efficient solutions are increasingly influencing material selection and design innovations within the sector.

These trends underscore a market that is not only expanding in volume but also maturing in terms of technological sophistication and operational efficiency. The integration of advanced sensor technologies and data analytics is becoming paramount for optimizing belt performance, extending lifespan, and reducing operational costs. Simultaneously, manufacturers are focusing on developing belts that offer superior resistance to abrasion, heat, and impact, addressing critical pain points for end-users and ensuring uninterrupted material flow in demanding applications.

- Increased adoption of smart conveyor systems with integrated sensors for real-time monitoring and predictive maintenance.

- Development of high-performance steel cord belts offering enhanced resistance to heat, abrasion, and impact for extreme operating conditions.

- Growing focus on sustainable manufacturing practices and the development of energy-efficient belt designs.

- Expansion into new application areas requiring robust and reliable material handling solutions, beyond traditional mining and quarrying.

- Demand for customized belt solutions tailored to specific industry requirements and challenging environmental factors.

AI Impact Analysis on Steel Cord Conveyor Belt

Common user questions regarding AI's influence on the steel cord conveyor belt industry revolve around predictive maintenance, operational efficiency, and quality control. Users are keen to understand how AI can prevent costly downtimes, optimize material flow, and improve overall safety. The primary expectation is that AI will enable more intelligent and autonomous conveyor systems, moving beyond traditional reactive maintenance to a proactive, data-driven approach that significantly extends asset lifespan and reduces operational expenditures.

AI's impact is anticipated across several operational facets. In manufacturing, AI algorithms can optimize curing processes and detect defects during production, ensuring higher quality standards. For operational use, machine learning models can analyze data from embedded sensors to predict potential failures, schedule maintenance, and even suggest optimal belt speeds and loads for energy efficiency. This integration of artificial intelligence is expected to transform the steel cord conveyor belt from a passive component into an active, intelligent asset within industrial material handling systems, delivering substantial long-term value.

- Enhanced predictive maintenance capabilities through AI-powered sensor data analysis, reducing unscheduled downtime.

- Optimization of conveyor system performance, including speed and load management, to improve energy efficiency and throughput.

- Automated defect detection during manufacturing and operational monitoring, ensuring higher quality and early fault identification.

- Improved safety protocols through real-time anomaly detection and operational risk assessment.

- Development of self-optimizing conveyor systems that adapt to changing operational conditions and material properties.

Key Takeaways Steel Cord Conveyor Belt Market Size & Forecast

The analysis of common user questions regarding the steel cord conveyor belt market size and forecast reveals a strong interest in growth drivers, regional market dynamics, and the overarching investment landscape. Users are particularly interested in understanding which industrial sectors will fuel future demand and how technological advancements will shape market expansion. The key insight is that while traditional industries like mining remain foundational, the market's future growth will increasingly depend on diversification into new applications and the adoption of high-tech solutions.

Forecasting indicates robust growth driven by significant infrastructure projects globally, particularly in emerging economies, alongside a consistent demand from heavy industries. The shift towards higher capacity, longer-distance material transport, and the emphasis on operational efficiency are pivotal factors influencing market trajectory. Investors and industry stakeholders should recognize the increasing importance of advanced materials and integrated digital solutions as key differentiators in a competitive landscape.

- The market is poised for steady growth, primarily propelled by continued investments in mining, infrastructure development, and industrial expansion, especially in emerging economies.

- Technological advancements, including smart monitoring systems and enhanced material compositions, will be crucial in meeting the escalating demands for performance and durability.

- Asia Pacific is expected to remain the dominant market, with significant opportunities emerging in other regions driven by urbanization and industrialization.

- Operational efficiency, energy savings, and extended product lifespan are increasingly critical factors influencing purchasing decisions and market competitiveness.

- The aftermarket segment for replacement and maintenance services is anticipated to constitute a substantial portion of the market, driven by the long operational life of conveyor systems.

Steel Cord Conveyor Belt Market Drivers Analysis

The global steel cord conveyor belt market is propelled by a confluence of macroeconomic factors and industrial demands. A primary driver is the robust growth in mining activities worldwide, especially for commodities like iron ore, coal, and various minerals, which necessitate efficient and reliable material handling over long distances and often in challenging environments. Concurrently, large-scale infrastructure development projects, including port expansions, power plant construction, and highway development, are creating significant demand for heavy-duty conveying systems. The push for greater operational efficiency and automation across heavy industries also mandates the adoption of advanced conveyor solutions capable of continuous and high-volume material transport.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Mining Activities | +1.8% | APAC (China, Australia), Latin America (Brazil, Chile), Africa | Long-term (2025-2033) |

| Increased Infrastructure Development | +1.5% | Asia Pacific (India, Southeast Asia), North America, Europe | Mid-term to Long-term (2025-2030) |

| Rising Demand for Bulk Material Handling | +1.2% | Global, particularly Ports, Cement, Power Generation | Ongoing (2025-2033) |

| Focus on Operational Efficiency and Automation | +1.0% | Developed Economies (North America, Europe), Asia Pacific | Mid-term (2025-2029) |

| Expansion of Power Generation (Coal-fired, Thermal) | +0.8% | Asia Pacific (India, Southeast Asia), Africa | Short to Mid-term (2025-2028) |

Steel Cord Conveyor Belt Market Restraints Analysis

Despite significant growth drivers, the steel cord conveyor belt market faces certain restraints that could temper its expansion. One notable challenge is the high initial capital investment required for installing these robust systems, which can be prohibitive for smaller operations or in regions with limited financial resources. Furthermore, the volatility in raw material prices, particularly for steel and rubber, can directly impact manufacturing costs and, consequently, the final product pricing, leading to fluctuations in market demand. Stringent environmental regulations, especially concerning dust emissions and energy consumption, also pose limitations, requiring manufacturers to invest more in compliance and sustainable practices, which can increase production expenses.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment | -0.9% | Emerging Economies, SMEs Globally | Ongoing (2025-2033) |

| Volatility in Raw Material Prices | -0.7% | Global Supply Chains | Short to Mid-term (2025-2028) |

| Stringent Environmental Regulations | -0.6% | Europe, North America, specific Asian regions | Long-term (2025-2033) |

| Competition from Alternative Transport Methods | -0.4% | Specific Niche Applications, Urban Areas | Ongoing (2025-2033) |

Steel Cord Conveyor Belt Market Opportunities Analysis

The steel cord conveyor belt market is rich with opportunities stemming from technological advancements and evolving industrial landscapes. A significant opportunity lies in the development and adoption of smart conveyor systems, integrating IoT sensors, AI, and data analytics for predictive maintenance and optimized operational performance. This shift towards intelligent solutions offers enhanced efficiency and reduced downtime, appealing to a broader range of industrial clients. Moreover, the expanding focus on sustainable practices globally opens avenues for manufacturers to innovate in eco-friendly materials and energy-efficient designs, meeting the growing demand for greener industrial solutions. The emergence of new mining projects and infrastructure developments in previously untapped regions also presents substantial growth prospects.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration of Smart Technologies (IoT, AI) | +1.1% | Global, particularly Developed Markets | Mid-term to Long-term (2026-2033) |

| Development of Sustainable and Eco-Friendly Belts | +0.9% | Europe, North America, Environmentally Conscious Industries | Mid-term (2027-2031) |

| Expansion into Niche & Specialized Applications | +0.8% | Chemical, Recycling, Tunneling | Short to Mid-term (2025-2029) |

| Untapped Market Potential in Emerging Regions | +0.7% | Africa, parts of Southeast Asia, Central Asia | Long-term (2028-2033) |

Steel Cord Conveyor Belt Market Challenges Impact Analysis

The steel cord conveyor belt market faces several critical challenges that demand strategic responses from manufacturers and stakeholders. One significant hurdle is the persistent shortage of skilled labor required for the installation, maintenance, and complex repairs of these advanced systems, impacting operational efficiency and project timelines. Rapid technological advancements, while presenting opportunities, also bring the challenge of potential technological obsolescence for existing equipment, necessitating continuous investment in research and development. Furthermore, global supply chain disruptions, ranging from geopolitical tensions to logistical bottlenecks, can severely affect the timely availability of raw materials and components, leading to production delays and increased costs. Addressing these challenges requires agile business models, robust talent development programs, and diversified supply chain strategies to mitigate risks and sustain growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Shortage of Skilled Labor | -0.8% | Developed Economies, Specific Industrial Hubs | Ongoing (2025-2033) |

| Technological Obsolescence & High R&D Costs | -0.6% | Global | Mid-term (2026-2030) |

| Global Supply Chain Disruptions | -0.5% | Global, particularly reliant on specific raw material sources | Short-term to Mid-term (2025-2027) |

| Intensifying Price Competition | -0.4% | Global, especially from low-cost manufacturers | Ongoing (2025-2033) |

Steel Cord Conveyor Belt Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global steel cord conveyor belt market, covering historical data, current market dynamics, and future projections from 2025 to 2033. It offers critical insights into market size, growth drivers, restraints, opportunities, and challenges, along with detailed segmentation and regional analysis. The report aims to equip stakeholders with actionable intelligence to make informed strategic decisions within this evolving industrial sector, highlighting key trends and competitive landscapes.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 7.5 Billion |

| Growth Rate | 6.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Bridgestone Corporation, Continental AG, Semperit AG Holding, Fenner PLC (Michelin), Goodyear Tire & Rubber Company, Trelleborg AB, Bando Chemical Industries, Ltd., Oriental Rubber Industries Pvt. Ltd., Zhejiang Double Arrow Rubber Co., Ltd., Wuxi Tianlun Rubber Co., Ltd., Shandong Phoenix Conveyor Belt Co., Ltd., Metso Outotec, Dunlophiflex, Depreux, Intralox, Habasit AG, Ammeraal Beltech, Forbo Siegling, Esbelt S.A., Contitech (Continental AG) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The global steel cord conveyor belt market is extensively segmented to provide a granular view of its diverse landscape and to identify specific areas of growth and opportunity. This segmentation allows for a detailed understanding of market dynamics based on the product characteristics, the industries that utilize these belts, and the channels through which they are distributed. Analyzing these segments is crucial for stakeholders to tailor their strategies, optimize product development, and target specific customer needs effectively. The intricate interplay between these segments defines the market’s current structure and future potential, driven by technological evolution and demand from various end-use sectors.

Each segment holds distinct implications for market players. For instance, the demand for specialized types like ultra-heavy duty or heat-resistant belts is directly tied to the expansion of specific mining or industrial operations. Similarly, the dominance of the aftermarket segment reflects the long operational lifespan of conveyor systems and the ongoing need for maintenance and replacement. Geographical segmentation highlights regional disparities in industrial growth and infrastructure development, guiding investment decisions and market entry strategies. By understanding these divisions, businesses can better navigate the complexities of the global steel cord conveyor belt industry and capitalize on emerging trends.

- By Type: Standard Duty, Heavy Duty, Ultra-Heavy Duty, Heat Resistant, Fire Resistant, Oil Resistant, Rip Resistant, Impact Resistant.

- By Application/End-Use Industry: Mining (Coal, Metal Ore, Others), Ports & Terminals, Power Plants, Cement Industry, Steel & Metallurgy, Chemical Industry, Construction, Others.

- By Sales Channel: OEM (Original Equipment Manufacturer), Aftermarket.

- By Region: North America (U.S., Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC), Latin America (Brazil, Argentina, Rest of LATAM), Middle East & Africa (South Africa, Saudi Arabia, UAE, Rest of MEA).

Regional Highlights

- Asia Pacific: Expected to dominate the market due to robust industrial growth, extensive mining activities in countries like China, India, and Australia, and significant investments in infrastructure and port development. Rapid urbanization and industrialization continue to fuel demand for efficient bulk material handling systems across diverse sectors.

- North America: Demonstrates steady growth driven by modernization of existing infrastructure, increasing demand from the mining sector, and adoption of advanced conveying technologies for efficiency and safety. Emphasis on automation and smart systems is also a key regional driver.

- Europe: Characterized by a strong focus on high-performance and specialized steel cord conveyor belts, driven by stringent environmental regulations and a preference for energy-efficient, durable solutions. Renovation and upgrades of industrial facilities contribute significantly to market demand.

- Latin America: Presents significant opportunities, especially in the mining and port sectors, with countries like Brazil and Chile being major players in metal ore extraction. Investment in new projects and expansion of existing operations will drive regional market growth.

- Middle East & Africa (MEA): Emerging as a promising market due to ongoing infrastructure development projects, expansion of mining operations in Africa, and increased investment in industrial sectors across the Middle East. Demand for heavy-duty and robust conveyor belts is on the rise to support these large-scale endeavors.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Steel Cord Conveyor Belt Market.- Bridgestone Corporation

- Continental AG

- Semperit AG Holding

- Fenner PLC (Michelin)

- Goodyear Tire & Rubber Company

- Trelleborg AB

- Bando Chemical Industries, Ltd.

- Oriental Rubber Industries Pvt. Ltd.

- Zhejiang Double Arrow Rubber Co., Ltd.

- Wuxi Tianlun Rubber Co., Ltd.

- Shandong Phoenix Conveyor Belt Co., Ltd.

- Metso Outotec

- Dunlophiflex

- Depreux

- Intralox

- Habasit AG

- Ammeraal Beltech

- Forbo Siegling

- Esbelt S.A.

- Contitech (Continental AG)

Frequently Asked Questions

What are steel cord conveyor belts primarily used for?

Steel cord conveyor belts are primarily used for heavy-duty, long-distance, and high-volume material transport in industries such as mining (coal, metal ore), ports and terminals, power plants, cement manufacturing, and steel mills, where durability and strength are paramount.

What are the main advantages of using steel cord conveyor belts?

The main advantages include exceptional strength and impact resistance, minimal elongation and consistent tension, superior rip and tear resistance, longer service life, and the ability to operate effectively in harsh environments with high loads and long conveying distances.

How does AI impact the performance and maintenance of steel cord conveyor belts?

AI impacts performance and maintenance by enabling predictive analytics for early fault detection, optimizing operational parameters for energy efficiency, automating quality control during manufacturing, and enhancing safety through real-time monitoring and anomaly detection, leading to reduced downtime and extended belt lifespan.

Which regions are leading the demand for steel cord conveyor belts?

The Asia Pacific region, particularly countries like China, India, and Australia, currently leads the demand for steel cord conveyor belts due to extensive mining operations, rapid infrastructure development, and industrial expansion. North America and Europe also maintain significant market shares.

What are the key factors driving the growth of the steel cord conveyor belt market?

Key growth drivers include increasing global mining activities, significant investments in infrastructure development (ports, power plants, construction), rising demand for efficient bulk material handling solutions, and the ongoing push for automation and operational efficiency across various heavy industries worldwide.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted