State In Vehicle Networking Market

State In Vehicle Networking Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705429 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

State In Vehicle Networking Market Size

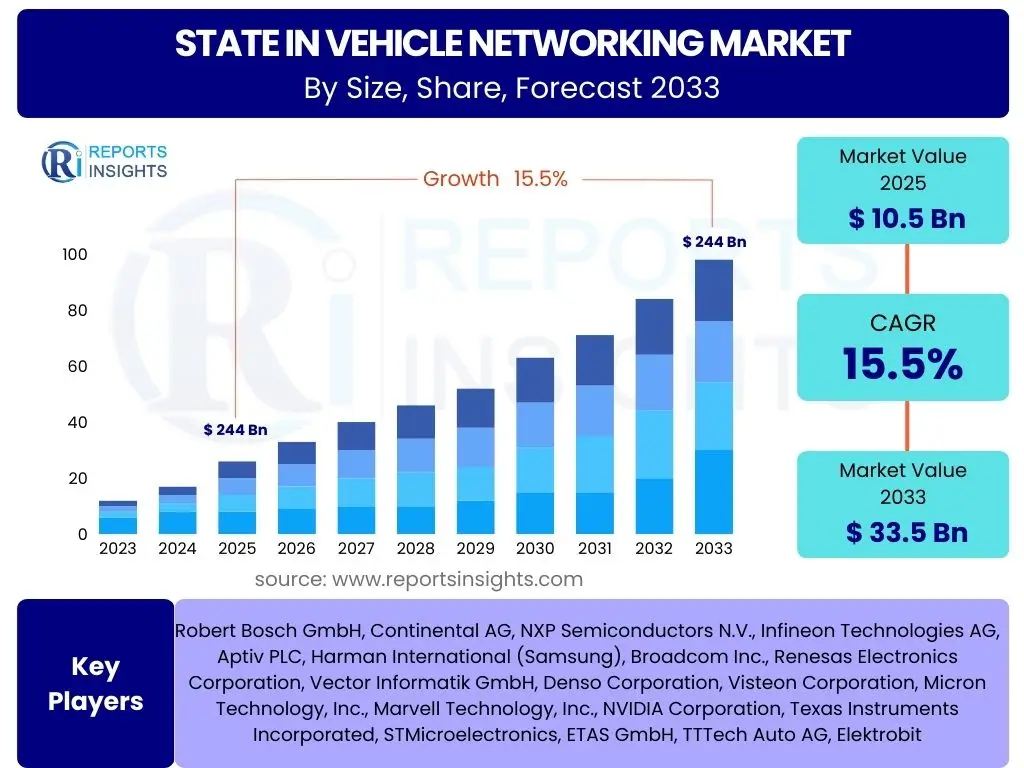

According to Reports Insights Consulting Pvt Ltd, The State In Vehicle Networking Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.5% between 2025 and 2033. The market is estimated at USD 10.5 Billion in 2025 and is projected to reach USD 33.5 Billion by the end of the forecast period in 2033.

Key State In Vehicle Networking Market Trends & Insights

The State In Vehicle Networking market is undergoing significant transformation driven by the escalating demand for advanced vehicle functionalities and enhanced user experiences. A primary trend involves the shift towards high-bandwidth communication networks, such as Automotive Ethernet, to support the immense data transfer requirements of advanced driver-assistance systems (ADAS) and autonomous driving. This evolution is also fostering the integration of software-defined vehicle architectures, enabling over-the-air (OTA) updates and flexible feature deployment, which is critical for future vehicle development and monetization strategies.

Another prominent insight is the increasing convergence of in-vehicle networks with external cloud services and vehicle-to-everything (V2X) communication. This integration facilitates real-time data exchange for traffic optimization, predictive maintenance, and enhanced safety features. Furthermore, the market is witnessing a growing emphasis on robust cybersecurity measures within the network infrastructure to protect sensitive data and ensure vehicle integrity against potential threats. This focus is paramount as vehicles become more connected and susceptible to remote vulnerabilities.

- Transition to Automotive Ethernet for high-bandwidth applications.

- Proliferation of software-defined vehicle architectures and OTA updates.

- Increased integration of cloud connectivity and V2X communication.

- Heightened focus on cybersecurity within in-vehicle network designs.

- Adoption of zonal and domain-controller architectures for simplified wiring.

AI Impact Analysis on State In Vehicle Networking

Artificial intelligence is profoundly reshaping the State In Vehicle Networking landscape by enabling smarter, more adaptive, and highly efficient communication within vehicles. AI algorithms are increasingly being embedded into network controllers and gateways to manage complex data flows, prioritize critical information for safety-critical applications, and optimize network performance in real-time. This includes predictive analytics for network health monitoring, dynamic bandwidth allocation, and intelligent fault detection, significantly enhancing the reliability and responsiveness of in-vehicle systems.

Moreover, AI plays a crucial role in empowering advanced functionalities such as autonomous driving and sophisticated infotainment systems. AI-powered perception systems generate vast amounts of data from sensors, which must be processed and communicated efficiently across the network for timely decision-making. Similarly, AI enhances the personalized user experience by optimizing content delivery, voice command processing, and adaptive cabin controls, all of which rely on robust and intelligent in-vehicle networking capabilities. The ongoing development of AI at the edge, within the vehicle itself, is pushing the boundaries of what in-vehicle networks can achieve.

- Enables intelligent data routing and network traffic management.

- Facilitates real-time processing for ADAS and autonomous driving decisions.

- Powers predictive maintenance and anomaly detection in network components.

- Enhances personalized in-car experiences and infotainment systems.

- Optimizes power consumption and resource allocation within the network.

Key Takeaways State In Vehicle Networking Market Size & Forecast

The State In Vehicle Networking market is poised for substantial expansion, primarily driven by the accelerated adoption of advanced driver-assistance systems (ADAS) and the progression towards fully autonomous vehicles. This growth trajectory indicates a fundamental shift in automotive architecture, moving away from traditional, isolated electronic control units (ECUs) towards integrated, high-performance network solutions. The increasing complexity of vehicle functionalities necessitates robust, high-speed, and secure communication backbones, presenting significant opportunities for innovation and market penetration in networking technologies.

A critical insight from the market forecast is the growing importance of software in defining vehicle capabilities and enabling new revenue streams. As vehicles transform into connected, intelligent platforms, the value proposition shifts from hardware-centric designs to software-defined functionalities, requiring adaptable and upgradeable in-vehicle networks. Furthermore, the forecast highlights the imperative for industry stakeholders to invest heavily in cybersecurity solutions and standardized protocols to ensure data integrity and system reliability across increasingly interconnected vehicle ecosystems.

- Significant market growth fueled by ADAS and autonomous driving advancements.

- Transition from traditional ECUs to integrated, high-performance network architectures.

- Increasing strategic importance of software-defined vehicle functionalities.

- Critical need for robust cybersecurity and standardized communication protocols.

- Opportunities arising from new business models based on connected services.

State In Vehicle Networking Market Drivers Analysis

The State In Vehicle Networking market is significantly propelled by several key drivers that are fundamentally transforming the automotive industry. The escalating consumer demand for connected car features, ranging from advanced infotainment systems to sophisticated navigation and telematics services, necessitates high-bandwidth and reliable in-vehicle communication infrastructures. Simultaneously, the rapid advancements in Advanced Driver Assistance Systems (ADAS) and the ongoing development of autonomous driving technologies are creating an urgent need for ultra-low latency, high-throughput networks capable of handling vast amounts of real-time sensor data.

Furthermore, stringent automotive safety regulations worldwide are compelling manufacturers to integrate more electronic systems that rely on robust networking for their operation. The proliferation of electric vehicles (EVs) also contributes to market growth, as EVs typically incorporate more sophisticated electronic architectures and connectivity features compared to traditional internal combustion engine vehicles. These combined factors are driving the adoption of advanced network technologies like Automotive Ethernet and pushing the boundaries of network efficiency and reliability within the automotive domain.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Connected Cars | +3.2% | Global, particularly North America, Europe, Asia Pacific | Short to Medium-term (2025-2030) |

| Growth in ADAS and Autonomous Driving | +4.5% | Global, with strong focus in North America, Europe, China | Medium to Long-term (2025-2033) |

| Proliferation of In-Car Infotainment Systems | +2.8% | Global, high penetration in developed markets | Short to Medium-term (2025-2030) |

| Regulatory Mandates for Vehicle Safety | +2.0% | Europe, North America, Japan, China | Ongoing (2025-2033) |

| Adoption of Automotive Ethernet | +3.0% | Global, driven by high-end vehicle segments initially | Medium to Long-term (2026-2033) |

State In Vehicle Networking Market Restraints Analysis

Despite the robust growth prospects, the State In Vehicle Networking market faces several restraints that could potentially impede its full expansion. One significant challenge is the high cost associated with implementing advanced networking solutions, particularly for legacy vehicle platforms or in cost-sensitive market segments. The transition from established, lower-cost technologies like CAN and LIN to newer, high-bandwidth solutions such as Automotive Ethernet requires substantial investment in hardware, software, and skilled labor, which can be a barrier for some manufacturers.

Another critical restraint is the inherent complexity of integrating diverse networking technologies and protocols within a single vehicle architecture. As the number of connected devices and functionalities increases, managing compatibility, ensuring seamless data flow, and maintaining real-time performance across various network domains become increasingly challenging. Furthermore, the rising concerns around cybersecurity threats and data privacy present a formidable hurdle, as any vulnerability in the in-vehicle network can have severe consequences, requiring continuous investment in robust security measures and compliance with evolving regulations.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Implementation | -1.8% | Global, particularly in emerging markets | Medium-term (2025-2030) |

| Cybersecurity Threats and Data Privacy Concerns | -2.5% | Global, prominent in developed economies with strict regulations | Ongoing (2025-2033) |

| Lack of Standardization and Interoperability Issues | -1.5% | Global, affecting multi-vendor integrations | Medium-term (2025-2030) |

| Technical Complexity of Network Integration | -1.2% | Global, impacting development cycles | Short to Medium-term (2025-2028) |

| Legacy System Compatibility Challenges | -1.0% | Global, particularly for established automotive manufacturers | Short to Medium-term (2025-2029) |

State In Vehicle Networking Market Opportunities Analysis

The State In Vehicle Networking market presents significant growth opportunities stemming from several transformative trends in the automotive industry. The advent of software-defined vehicles (SDVs) is opening vast avenues for innovation, allowing vehicle functionalities to be updated and enhanced through software, independent of hardware cycles. This paradigm shift necessitates highly flexible, scalable, and secure in-vehicle networks that can support dynamic software deployments and over-the-air (OTA) updates, creating a demand for advanced networking solutions and related services.

Furthermore, the ongoing global rollout of 5G technology and the increasing adoption of vehicle-to-everything (V2X) communication promise to revolutionize automotive connectivity. These technologies offer ultra-low latency and high bandwidth, enabling real-time data exchange between vehicles, infrastructure, and other road users, which is crucial for autonomous driving and smart city initiatives. This creates new opportunities for networking component providers and software developers. Additionally, the expansion into emerging markets, where vehicle ownership and demand for connected features are rapidly growing, represents a fertile ground for market expansion, particularly in regions like Asia Pacific and Latin America, which are witnessing significant automotive sector investments.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rise of Software-Defined Vehicles (SDVs) | +3.5% | Global, particularly developed automotive markets | Medium to Long-term (2026-2033) |

| Emergence of 5G and V2X Communication | +4.0% | Global, driven by smart city initiatives and regulatory push | Medium to Long-term (2027-2033) |

| Expansion into Emerging Markets | +2.8% | Asia Pacific, Latin America, Middle East & Africa | Short to Long-term (2025-2033) |

| Development of New Business Models (e.g., subscription services) | +2.5% | Global, appealing to OEMs and Tier-1 suppliers | Medium-term (2025-2030) |

| Advancements in Zonal and Domain Architectures | +3.0% | Global, for simplified wiring and optimized processing | Medium to Long-term (2026-2033) |

State In Vehicle Networking Market Challenges Impact Analysis

The State In Vehicle Networking market faces several significant challenges that require strategic attention from industry participants. One primary challenge is the successful integration of increasingly disparate and complex electronic control units (ECUs) and sensors from various suppliers into a cohesive and efficient network architecture. This integration complexity is compounded by the need to manage massive volumes of data generated by advanced systems like ADAS and autonomous driving, while ensuring real-time performance and low latency for safety-critical functions.

Furthermore, maintaining stringent cybersecurity standards amidst a rapidly evolving threat landscape remains a persistent challenge. As vehicles become more connected and susceptible to remote attacks, securing the in-vehicle network from unauthorized access and data breaches is paramount, requiring continuous updates and robust encryption protocols. Another substantial challenge is the shortage of highly skilled professionals proficient in both automotive engineering and advanced networking technologies, which can hinder innovation and slow down product development cycles across the industry. Addressing these challenges effectively will be crucial for the sustained growth and maturity of the State In Vehicle Networking market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration of Disparate Systems and Protocols | -2.0% | Global, impacting OEMs and Tier-1 suppliers | Short to Medium-term (2025-2030) |

| Managing Escalating Data Volumes and Bandwidth Demands | -1.5% | Global, particularly for high-end and autonomous vehicles | Ongoing (2025-2033) |

| Ensuring Real-Time Reliability and Functional Safety | -1.8% | Global, critical for safety-related applications | Ongoing (2025-2033) |

| Shortage of Skilled Workforce | -1.0% | Global, impacting R&D and implementation | Long-term (2025-2033) |

| Regulatory Compliance and Certification | -0.8% | Global, varying by region and application | Ongoing (2025-2033) |

State In Vehicle Networking Market - Updated Report Scope

This market research report provides an in-depth analysis of the State In Vehicle Networking market, encompassing historical data from 2019 to 2023, a base year of 2024, and a comprehensive forecast extending from 2025 to 2033. The scope includes a detailed examination of market size, growth drivers, restraints, opportunities, and challenges, along with a comprehensive segmentation analysis by network technology, application, vehicle type, component, bandwidth, and topology. The report offers regional insights across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, complemented by profiles of key market players to provide a holistic view of the industry landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 10.5 Billion |

| Market Forecast in 2033 | USD 33.5 Billion |

| Growth Rate | 15.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Robert Bosch GmbH, Continental AG, NXP Semiconductors N.V., Infineon Technologies AG, Aptiv PLC, Harman International (Samsung), Broadcom Inc., Renesas Electronics Corporation, Vector Informatik GmbH, Denso Corporation, Visteon Corporation, Micron Technology, Inc., Marvell Technology, Inc., NVIDIA Corporation, Texas Instruments Incorporated, STMicroelectronics, ETAS GmbH, TTTech Auto AG, Elektrobit |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The State In Vehicle Networking market is intricately segmented across various dimensions to provide a granular understanding of its dynamics and growth trajectories. These segmentations allow for a detailed analysis of how different technologies, applications, vehicle types, components, bandwidth requirements, and network topologies contribute to the overall market landscape. Understanding these segments is crucial for identifying specific growth pockets, emerging trends, and strategic opportunities for stakeholders across the automotive value chain, from semiconductor manufacturers to software developers and automotive OEMs.

- By Network Technology: This segment analyzes the adoption and evolution of various communication protocols within vehicles.

Controller Area Network (CAN) remains a foundational technology for many automotive applications, known for its robustness and cost-effectiveness in low-speed communication. However, the increasing data demands of modern vehicles are pushing the adoption of higher-bandwidth solutions. Local Interconnect Network (LIN) complements CAN for simpler, cost-sensitive applications within vehicle subsystems. FlexRay offers higher bandwidth and deterministic communication for safety-critical applications, while Media Oriented Systems Transport (MOST) has traditionally served high-bandwidth multimedia and infotainment systems.

Automotive Ethernet is rapidly emerging as the backbone for next-generation in-vehicle networks due to its high bandwidth, scalability, and ability to handle IP-based communication, which is essential for ADAS, autonomous driving, and software-defined architectures. Wireless technologies such as Wi-Fi, Bluetooth, 5G/LTE, and Ultra-Wideband (UWB) are also gaining prominence for external connectivity, vehicle-to-cloud communication, and specific in-cabin applications, facilitating seamless data exchange and enhancing user experience.

- Controller Area Network (CAN)

- Local Interconnect Network (LIN)

- FlexRay

- Media Oriented Systems Transport (MOST)

- Automotive Ethernet

- Wireless Technologies (Wi-Fi, Bluetooth, 5G/LTE, UWB)

- By Application: This segmentation highlights the diverse functional areas where in-vehicle networking is critical.

Advanced Driver Assistance Systems (ADAS) represent a significant driver, requiring ultra-low latency and high-bandwidth communication for sensors, cameras, and processing units to enable features like adaptive cruise control, lane-keeping assist, and automatic emergency braking. Infotainment and Telematics systems demand robust networking for navigation, media streaming, smartphone integration, and connectivity services, enhancing the driver and passenger experience.

Powertrain applications rely on networking for engine control, transmission management, and battery management in electric vehicles, ensuring optimal performance and efficiency. Body Electronics encompass systems like lighting, HVAC, and power windows, where networking provides efficient control and diagnostics. Chassis and Safety systems, including braking, steering, and airbag deployment, require highly reliable and redundant networks for critical safety functions. Autonomous Driving Systems, the pinnacle of automotive technology, necessitate the most advanced in-vehicle networks to process vast amounts of sensor data and facilitate real-time decision-making for safe and reliable self-driving capabilities.

- Advanced Driver Assistance Systems (ADAS)

- Infotainment and Telematics

- Powertrain

- Body Electronics

- Chassis and Safety

- Autonomous Driving Systems

- By Vehicle Type: This segment differentiates market penetration across various vehicle categories.

Passenger Vehicles constitute the largest segment, driven by the mass adoption of connected features, ADAS, and luxury options that demand sophisticated in-vehicle networks. The increasing integration of advanced safety features and infotainment systems in everyday cars directly fuels the growth in this segment. The competitive landscape in the passenger vehicle market pushes manufacturers to continuously innovate and differentiate their offerings through enhanced connectivity and automation, all reliant on robust networking.

Commercial Vehicles, including trucks, buses, and vans, are increasingly adopting in-vehicle networking for fleet management, telematics, predictive maintenance, and enhanced safety features. The focus here is often on operational efficiency, uptime, and regulatory compliance. Electric Vehicles (EVs) represent a rapidly expanding segment, inherently featuring more complex electronic architectures and a greater reliance on advanced networking for battery management systems, charging infrastructure communication, and integration with smart grids, driving the demand for high-performance and secure networks.

- Passenger Vehicles

- Commercial Vehicles

- Electric Vehicles (EVs)

- By Component: This segmentation dissects the market into hardware, software, and services essential for in-vehicle networking.

The Hardware segment includes the physical components such as transceivers, microcontrollers, gateways, switches, connectors, and wiring harnesses that form the backbone of the network. These components are critical for data transmission, processing, and system integration. Advancements in semiconductor technology and materials are continuously improving the performance and efficiency of these hardware elements, enabling higher bandwidths and lower power consumption.

The Software segment encompasses operating systems, middleware, communication protocols, and diagnostic tools that manage and control the in-vehicle network. This segment is growing significantly as vehicles become more software-defined, requiring complex software stacks for network management, data processing, and application integration. Services include integration, maintenance, and consulting, which are vital for designing, deploying, and supporting sophisticated in-vehicle networking solutions. These services ensure optimal performance, reliability, and security throughout the vehicle's lifecycle, supporting OEMs and Tier-1 suppliers in navigating the complexities of advanced network architectures.

- Hardware (Transceivers, Microcontrollers, Gateways, Switches, Connectors, Wiring Harnesses)

- Software (Operating Systems, Middleware, Communication Protocols, Diagnostic Tools)

- Services (Integration, Maintenance, Consulting)

- By Bandwidth: This segment categorizes networks based on their data transfer capacity.

Low Bandwidth networks, primarily utilizing technologies like LIN and basic CAN, are suitable for less data-intensive applications such as comfort functions (e.g., power windows, seat adjustments) and simple sensor data transmission. They are cost-effective and sufficient for isolated, lower-speed communications within specific vehicle domains.

Medium Bandwidth networks, often leveraging advanced CAN or FlexRay, cater to applications requiring moderate data transfer rates and enhanced reliability, such as powertrain control, some ADAS features, and chassis systems. These networks strike a balance between performance and cost. High Bandwidth networks, predominantly Automotive Ethernet, are essential for data-heavy applications including complex ADAS, autonomous driving, high-definition infotainment, and camera systems, where real-time processing of massive data volumes is critical. The trend is clearly moving towards higher bandwidth solutions to support future vehicle architectures.

- Low Bandwidth

- Medium Bandwidth

- High Bandwidth

- By Topology: This segmentation describes the physical and logical layout of the network.

Bus Topology, like in CAN, connects all devices to a single shared communication line, offering simplicity and cost-effectiveness for lower data rates. Star Topology, increasingly seen with Automotive Ethernet, connects each device to a central hub or switch, providing dedicated bandwidth and improved fault isolation, which is crucial for high-speed and critical applications.

Ring Topology connects devices in a closed loop, offering inherent redundancy as data can travel in both directions, making it suitable for applications where high availability is paramount. Hybrid Topology combines elements of different topologies to optimize network design for various functional domains within a vehicle, leveraging the strengths of each to meet specific performance, cost, and reliability requirements across the complex in-vehicle network architecture.

- Bus Topology

- Star Topology

- Ring Topology

- Hybrid Topology

Regional Highlights

- North America: North America is a prominent market for State In Vehicle Networking, driven by early adoption of advanced automotive technologies and a strong focus on autonomous driving research and development. The region benefits from significant investments in connected infrastructure and a consumer base that highly values in-car connectivity, premium infotainment, and cutting-edge safety features. Regulatory initiatives, particularly concerning vehicle safety and emissions, also push the integration of more sophisticated electronic systems that rely on robust in-vehicle networks. The presence of leading automotive OEMs and technology innovators further propels market growth, with a growing emphasis on software-defined vehicles and over-the-air update capabilities.

- Europe: Europe stands as a mature and highly innovative market for State In Vehicle Networking, characterized by stringent safety regulations, a strong emphasis on premium vehicle segments, and a well-established automotive manufacturing base. European OEMs are at the forefront of adopting advanced networking solutions, including FlexRay and Automotive Ethernet, to meet complex functional safety requirements and support sophisticated ADAS features. The region's focus on sustainable mobility also drives the integration of advanced electronics in electric and hybrid vehicles, further necessitating robust and efficient in-vehicle networks.

Germany, with its robust automotive industry, particularly in luxury and performance vehicles, leads the European market. The country's strong engineering capabilities and extensive research into autonomous driving contribute significantly to the adoption of cutting-edge networking technologies. Other key countries like France, the UK, and Italy are also investing heavily in connected car technologies and smart mobility solutions, fostering a competitive environment for in-vehicle networking advancements. The emphasis on standardization and interoperability across the European Union further shapes the market, promoting widespread adoption and seamless integration of various components.

The European market is also witnessing a strong push towards zonal architectures and centralized computing platforms to simplify wiring harnesses and optimize network performance. This trend supports the development of software-defined vehicles, enabling greater flexibility and faster deployment of new features. Furthermore, the region is highly attuned to data privacy regulations, which directly influence the design and implementation of secure in-vehicle communication systems.

- Asia Pacific (APAC): The Asia Pacific region is the fastest-growing market for State In Vehicle Networking, propelled by rapid urbanization, increasing vehicle production, and a burgeoning middle class demanding advanced automotive features. Countries like China, Japan, South Korea, and India are key drivers of this growth, with significant investments in smart city infrastructure, electric vehicles, and autonomous driving research. The sheer volume of vehicle sales and the push towards domestic innovation in automotive technology contribute substantially to the market's expansion.

China dominates the APAC market, driven by its massive automotive production capacity, aggressive adoption of electric vehicles, and supportive government policies for connected and intelligent cars. The country is a hotspot for both domestic and international automotive players, leading to rapid technological advancements in in-vehicle networking. Japan and South Korea, renowned for their technological prowess, are leaders in developing and implementing advanced driver assistance systems and integrated infotainment solutions that rely heavily on high-performance networks.

India and Southeast Asian countries are emerging as significant markets due to increasing disposable incomes, rising vehicle penetration, and growing consumer awareness of connected car benefits. The region is characterized by a strong focus on cost-effective solutions alongside high-end offerings, leading to a diverse demand for various networking technologies. The rapid deployment of 5G infrastructure also presents immense opportunities for V2X communication and enhanced in-vehicle connectivity across the Asia Pacific landscape.

- Latin America: The Latin American market for State In Vehicle Networking is in a nascent but growing phase, primarily driven by increasing vehicle sales, improving economic conditions, and the gradual adoption of connected car technologies. While the market is smaller compared to developed regions, there is a rising awareness and demand for vehicle safety features and basic connectivity solutions. Government initiatives to modernize infrastructure and improve road safety are gradually fostering an environment conducive to the adoption of advanced in-vehicle electronics.

Brazil and Mexico are the leading countries in Latin America, owing to their significant automotive manufacturing bases and larger domestic markets. These countries are witnessing increased integration of basic and mid-range in-vehicle networking technologies in new vehicle models. The focus is often on infotainment systems, basic telematics, and entry-level ADAS features that enhance driver convenience and safety.

Challenges such as economic volatility and infrastructure limitations can impact the pace of adoption of high-end networking solutions. However, as disposable incomes rise and consumer preferences shift towards more technologically advanced vehicles, the region is expected to experience steady growth. Opportunities lie in providing scalable and cost-effective networking solutions that cater to the evolving needs of the growing automotive sector in the region.

- Middle East and Africa (MEA): The Middle East and Africa region presents a developing market for State In Vehicle Networking, influenced by investments in smart city projects, economic diversification efforts, and a growing luxury automotive segment in certain countries. The demand for connected cars is primarily driven by affluent consumers in the GCC countries (e.g., UAE, Saudi Arabia) who seek premium features, advanced infotainment, and robust safety systems in their vehicles. Government visions for smart cities, such as Neom in Saudi Arabia, are also spurring interest in autonomous and connected mobility solutions.

In the Middle East, high disposable incomes and a preference for luxury vehicles are driving the adoption of sophisticated in-vehicle networking technologies that support advanced features. The region is also increasingly focused on improving road safety and traffic management through connected vehicle initiatives. In Africa, while the market is still emerging, there is a growing demand for telematics and fleet management solutions in commercial vehicles, alongside increasing interest in affordable connected car options for passenger vehicles.

Challenges in the region include varying levels of technological infrastructure, economic disparities, and regulatory frameworks that are still under development. However, as connectivity penetration increases and automotive production expands, particularly in countries like South Africa and Egypt, the MEA market is anticipated to show consistent growth. Opportunities exist in providing tailored solutions that address the specific needs and infrastructure capabilities of diverse sub-regions within MEA.

The United States leads the regional market due to substantial R&D spending, a large fleet of connected cars, and a conducive ecosystem for technological innovation in the automotive sector. Canada also contributes significantly, particularly in the development and testing of autonomous vehicle technologies. The demand for high-bandwidth networks like Automotive Ethernet is surging to support complex ADAS features and advanced infotainment systems, ensuring seamless data flow and enhanced user experiences across various vehicle segments.

Key developments in North America include collaborations between tech giants and automotive manufacturers to integrate AI-powered solutions and cloud connectivity directly into vehicle architectures. The region is also at the forefront of cybersecurity advancements for in-vehicle networks, addressing the growing concerns around data privacy and system integrity in increasingly connected automobiles. This proactive approach ensures that the market evolves with a strong emphasis on security and reliability.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the State In Vehicle Networking Market.- Robert Bosch GmbH

- Continental AG

- NXP Semiconductors N.V.

- Infineon Technologies AG

- Aptiv PLC

- Harman International (Samsung)

- Broadcom Inc.

- Renesas Electronics Corporation

- Vector Informatik GmbH

- Denso Corporation

- Visteon Corporation

- Micron Technology, Inc.

- Marvell Technology, Inc.

- NVIDIA Corporation

- Texas Instruments Incorporated

- STMicroelectronics

- ETAS GmbH

- TTTech Auto AG

- Elektrobit

Frequently Asked Questions

What is the projected growth rate of the State In Vehicle Networking Market?

The State In Vehicle Networking Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.5% between 2025 and 2033.

What are the primary drivers of growth in the In Vehicle Networking market?

Key drivers include the escalating demand for connected cars, the rapid growth in Advanced Driver Assistance Systems (ADAS) and autonomous driving technologies, and the increasing proliferation of in-car infotainment systems.

How is AI impacting In Vehicle Networking?

AI is significantly impacting In Vehicle Networking by enabling intelligent data routing, real-time processing for ADAS and autonomous decisions, predictive maintenance, and enhancing personalized in-car experiences through optimized network management.

What are the main challenges facing the State In Vehicle Networking Market?

Primary challenges include the complex integration of disparate systems and protocols, managing escalating data volumes and bandwidth demands, ensuring real-time reliability and functional safety, and addressing the shortage of skilled workforce.

Which network technologies are gaining prominence in the automotive sector?

Automotive Ethernet is rapidly gaining prominence due to its high bandwidth and scalability, while traditional technologies like CAN and LIN continue to be used for specific applications. Wireless technologies like 5G/LTE and UWB are also becoming crucial for external and internal connectivity.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted