Heavy Commercial Vehicle Market

Heavy Commercial Vehicle Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705548 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

Heavy Commercial Vehicle Market Size

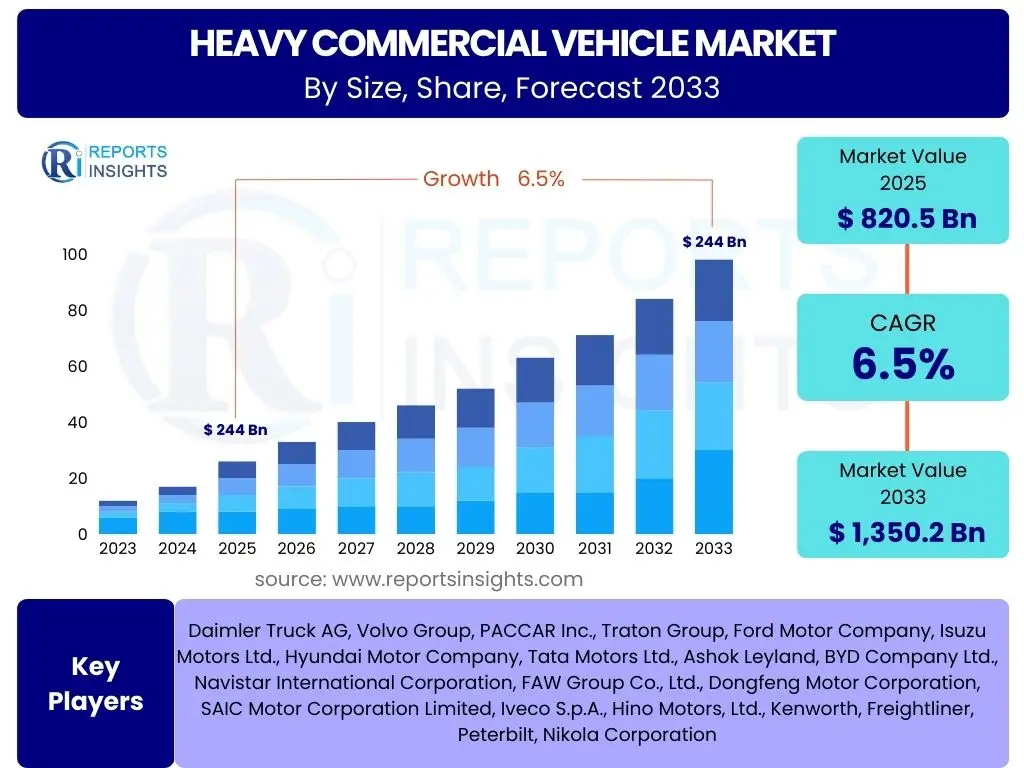

According to Reports Insights Consulting Pvt Ltd, The Heavy Commercial Vehicle Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 820.5 Billion in 2025 and is projected to reach USD 1,350.2 Billion by the end of the forecast period in 2033.

Key Heavy Commercial Vehicle Market Trends & Insights

The Heavy Commercial Vehicle (HCV) market is currently undergoing a significant transformation driven by advancements in technology, evolving logistics demands, and stringent environmental regulations. A primary trend observed is the accelerating shift towards electric and alternative fuel vehicles, fueled by global decarbonization initiatives and rising fuel costs. This transition is influencing vehicle design, charging infrastructure development, and operational models for fleet owners. Simultaneously, the integration of advanced telematics and connectivity solutions is becoming standard, offering enhanced fleet management capabilities, predictive maintenance, and optimized route planning, thereby improving operational efficiency and reducing downtime.

Another prominent insight is the growing emphasis on vehicle autonomy and driver assistance systems. While fully autonomous heavy commercial vehicles are still in developmental stages, increasing levels of automation are being incorporated to enhance safety, reduce driver fatigue, and improve fuel efficiency. The expansion of e-commerce and the increasing complexity of supply chains are also profoundly shaping the market, driving demand for specialized HCVs for last-mile delivery, refrigerated transport, and high-capacity long-haul logistics. Furthermore, the market is seeing a surge in demand for lightweight materials and aerodynamic designs, aimed at improving fuel economy and reducing operational costs for fleet operators.

The regulatory landscape continues to play a pivotal role, with governments worldwide implementing stricter emission norms (e.g., Euro VI, Bharat Stage VI) and safety standards. These regulations compel manufacturers to invest heavily in research and development to produce more efficient and environmentally friendly vehicles. The convergence of these trends suggests a market moving towards more sustainable, intelligent, and efficient transport solutions, fundamentally redefining the capabilities and applications of heavy commercial vehicles.

- Electrification and adoption of alternative fuels (hydrogen, natural gas).

- Integration of advanced telematics and connectivity for fleet management.

- Development and deployment of autonomous driving features and ADAS.

- Increased demand driven by the expansion of e-commerce and logistics.

- Focus on lightweight materials and aerodynamic designs for fuel efficiency.

- Stricter global emission standards driving innovation.

- Growth of integrated logistics solutions and smart transportation.

AI Impact Analysis on Heavy Commercial Vehicle

Artificial Intelligence (AI) is set to revolutionize the Heavy Commercial Vehicle (HCV) market by enhancing operational efficiency, improving safety, and enabling new service models. One of the most significant impacts is in predictive maintenance, where AI algorithms analyze vast amounts of data from vehicle sensors to anticipate component failures before they occur. This allows for proactive maintenance scheduling, minimizing costly unplanned downtime and extending the lifespan of vehicles. Furthermore, AI is crucial for optimizing logistics and route planning, processing real-time traffic, weather, and delivery data to determine the most efficient routes, thereby reducing fuel consumption, travel time, and operational costs.

In the realm of autonomous driving, AI serves as the core intelligence, enabling HCVs to perceive their environment, make decisions, and navigate complex road conditions without human intervention. While full Level 5 autonomy is still distant, AI-powered advanced driver-assistance systems (ADAS) are already widely implemented, enhancing safety through features like adaptive cruise control, lane-keeping assist, and automatic emergency braking. These systems reduce the probability of accidents, protect valuable cargo, and improve driver well-being. The integration of AI also extends to driver monitoring systems, which use AI to detect fatigue or distraction, issuing alerts to prevent accidents and ensure compliance with safety regulations.

Beyond vehicle operation, AI influences supply chain management, demand forecasting, and inventory optimization for components and parts. AI-driven analytics provide insights into market trends, customer behavior, and operational bottlenecks, allowing manufacturers and fleet operators to make more informed strategic decisions. This comprehensive integration of AI across various facets of the HCV ecosystem promises a future where heavy commercial transport is safer, more efficient, and significantly more intelligent, ultimately contributing to a more sustainable and productive global logistics network.

- Predictive maintenance using AI for proactive vehicle servicing.

- Enhanced route optimization and logistics planning through AI algorithms.

- Foundation for advanced driver-assistance systems (ADAS) and autonomous driving.

- Real-time driver monitoring for safety and fatigue detection.

- AI-powered demand forecasting and supply chain optimization.

- Development of smart charging solutions for electric HCVs.

- Improved safety and accident reduction through AI-driven insights.

Key Takeaways Heavy Commercial Vehicle Market Size & Forecast

The Heavy Commercial Vehicle (HCV) market is poised for robust and sustained growth through 2033, driven by a confluence of factors including expanding global trade, the booming e-commerce sector, and significant advancements in vehicle technology. The projected Compound Annual Growth Rate (CAGR) indicates a healthy expansion, signaling strong investment opportunities and an evolving landscape where efficiency, sustainability, and connectivity are paramount. This growth is not merely volumetric but also qualitative, reflecting a shift towards more sophisticated, technologically integrated, and environmentally conscious vehicles. Market participants must align their strategies with these foundational shifts to capitalize on emerging opportunities.

A significant takeaway is the increasing importance of regulatory frameworks and environmental considerations. Governments worldwide are imposing stricter emission standards and promoting cleaner transportation solutions, compelling manufacturers to innovate and introduce vehicles powered by electricity, hydrogen, and other alternative fuels. This regulatory push, combined with rising consumer and corporate demand for sustainable logistics, is a key driver for market transformation. The forecast also underscores the critical role of developing economies, particularly in Asia Pacific, where infrastructure development and urbanization are rapidly increasing the demand for HCVs across various applications, from construction to last-mile delivery.

Finally, the market's future will be heavily influenced by technological adoption, including autonomous features, advanced telematics, and AI-driven solutions. These technologies are not just add-ons but integral components that enhance vehicle performance, optimize operational costs, and improve safety. Companies that prioritize research and development in these areas and adapt their business models to leverage these innovations will gain a significant competitive advantage. The market is not just growing in size but also in its complexity and technological sophistication, requiring continuous adaptation from all stakeholders.

- Strong projected CAGR indicating sustained market expansion.

- Accelerated shift towards electric and alternative fuel HCVs.

- Significant impact of e-commerce growth on logistics and vehicle demand.

- Increasing integration of AI, telematics, and autonomous technologies.

- Stricter global emission regulations driving innovation.

- Emerging economies as key growth centers for HCV demand.

- Focus on operational efficiency and total cost of ownership reduction.

Heavy Commercial Vehicle Market Drivers Analysis

The Heavy Commercial Vehicle (HCV) market is propelled by a multitude of interconnected factors that stimulate demand across various industries. A primary driver is the burgeoning global logistics and transportation sector, fueled by an expanding international trade landscape and the rapid growth of e-commerce. As goods increasingly move across borders and directly to consumers, the need for efficient and reliable heavy-duty trucks and specialized vehicles for last-mile delivery and long-haul transport intensifies. This fundamental demand underpins much of the market’s current and future growth trajectory. Coupled with this, significant investments in infrastructure development, particularly in emerging economies, create substantial demand for construction equipment and dump trucks, directly boosting the HCV segment.

Furthermore, evolving regulatory landscapes and a global push towards sustainability are paradoxically driving innovation and market growth. Stricter emission standards, such as Euro VI and Bharat Stage VI, compel manufacturers to invest heavily in developing cleaner, more fuel-efficient vehicles, including electric and hydrogen-powered trucks. This regulatory pressure, while posing initial challenges, ultimately fosters technological advancement and expands the market for new, compliant vehicles. Additionally, the increasing adoption of fleet management solutions, telematics, and digital logistics platforms contributes to greater operational efficiency and cost savings for operators, making HCV investments more attractive and driving demand for technologically advanced vehicles.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in E-commerce & Logistics | +1.8% | Global, particularly North America, APAC, Europe | Short to Long-term (2025-2033) |

| Infrastructure Development & Construction Boom | +1.5% | Asia Pacific, Latin America, Middle East & Africa | Mid to Long-term (2025-2033) |

| Rising Demand for Fuel-Efficient & Electric Vehicles | +1.2% | Europe, North America, China | Short to Long-term (2025-2033) |

| Technological Advancements in Telematics & IoT | +0.8% | Global | Short to Mid-term (2025-2029) |

| Favorable Government Regulations & Initiatives for Clean Transport | +0.7% | Europe, China, India, North America | Mid to Long-term (2026-2033) |

Heavy Commercial Vehicle Market Restraints Analysis

Despite robust growth prospects, the Heavy Commercial Vehicle (HCV) market faces several significant restraints that could impede its expansion. One major challenge is the high initial acquisition cost of new, technologically advanced HCVs, especially electric and autonomous models. This elevated upfront investment can be a deterrent for small and medium-sized fleet operators, who may struggle with financing, leading them to delay fleet upgrades or opt for older, less efficient vehicles. Coupled with this, the volatility of fuel prices and the rising costs of raw materials, such as steel and aluminum, continue to exert pressure on operational expenses and manufacturing costs, impacting profitability margins for both manufacturers and end-users.

Another critical restraint stems from the inadequate charging and refueling infrastructure for alternative fuel vehicles. While the push towards electrification is strong, the sparse availability of charging stations for heavy-duty electric trucks over long distances, particularly in remote areas, presents a significant logistical hurdle. This infrastructure gap creates range anxiety and operational limitations, slowing down the widespread adoption of electric HCVs. Furthermore, the persistent shortage of skilled drivers and technicians capable of operating and maintaining modern, complex HCVs, including those with advanced electronics and alternative powertrains, poses a significant operational challenge for fleet owners globally.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Acquisition Cost of Advanced HCVs | -1.1% | Global, particularly developing economies | Short to Mid-term (2025-2029) |

| Inadequate Charging/Refueling Infrastructure for EVs/AFVs | -0.9% | Global, especially long-haul routes | Mid-term (2026-2030) |

| Volatility of Fuel Prices and Raw Material Costs | -0.7% | Global | Short-term (2025-2027) |

| Shortage of Skilled Drivers and Technicians | -0.6% | North America, Europe, parts of Asia | Short to Long-term (2025-2033) |

| Stringent Emission Regulations & Compliance Costs | -0.5% | Europe, North America, China, India | Short to Mid-term (2025-2029) |

Heavy Commercial Vehicle Market Opportunities Analysis

The Heavy Commercial Vehicle (HCV) market presents substantial opportunities driven by evolving technological landscapes and global shifts in consumer behavior and industrial practices. One of the most significant avenues for growth lies in the accelerating adoption of electric and hydrogen fuel cell HCVs. As governments worldwide intensify their efforts to decarbonize the transportation sector and advancements in battery technology reduce costs and improve range, the market for zero-emission commercial vehicles is set for exponential growth. This presents opportunities for vehicle manufacturers, battery suppliers, charging infrastructure providers, and related technology companies to innovate and capture market share in this burgeoning segment.

Furthermore, the continuous expansion of the e-commerce sector globally and the increasing demand for expedited and specialized logistics services create immense opportunities for tailored HCV solutions. This includes the development of lighter, more agile vehicles for urban last-mile delivery, as well as specialized refrigerated and temperature-controlled trucks for perishable goods. The integration of advanced telematics, IoT, and AI-driven fleet management systems also represents a significant growth area, enabling operators to optimize routes, monitor driver behavior, conduct predictive maintenance, and enhance overall operational efficiency, offering value-added services beyond mere vehicle sales.

Emerging markets, particularly in Asia Pacific, Latin America, and Africa, offer vast untapped potential. Rapid urbanization, industrialization, and infrastructure development projects in these regions are driving a surge in demand for HCVs for construction, mining, and freight transport. As these economies mature and disposable incomes rise, the demand for sophisticated and efficient transport solutions will only grow, providing a fertile ground for market expansion. Collaborative ventures, strategic partnerships, and focused R&D investments in these areas will be crucial for capitalizing on these diverse and dynamic opportunities within the HCV market.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Electric and Fuel Cell HCVs | +1.5% | Europe, North America, China, Japan | Mid to Long-term (2026-2033) |

| Increasing Demand for Autonomous & Connected HCVs | +1.0% | North America, Europe, select Asian countries | Long-term (2028-2033) |

| Growth in Specialized Logistics and Last-Mile Delivery | +0.8% | Global, especially urban areas | Short to Mid-term (2025-2029) |

| Untapped Potential in Emerging Economies | +0.7% | Asia Pacific (India, Southeast Asia), Latin America, Africa | Mid to Long-term (2026-2033) |

| Development of Advanced Telematics & Fleet Management Solutions | +0.6% | Global | Short to Mid-term (2025-2029) |

Heavy Commercial Vehicle Market Challenges Impact Analysis

The Heavy Commercial Vehicle (HCV) market faces a series of multifaceted challenges that can hinder its growth and transformation. One prominent challenge is the complexity and cost associated with developing and integrating new technologies, particularly in the realm of electrification and autonomous driving. This includes not only the research and development expenses but also the retooling of manufacturing facilities and the need for new supply chains for components like high-capacity batteries and advanced sensors. Ensuring the reliability, safety, and performance of these cutting-edge systems in diverse operating conditions presents significant engineering and validation hurdles.

Another critical challenge is the establishment of comprehensive and robust infrastructure to support the transition to electric and alternative fuel HCVs. The existing fueling infrastructure is largely built around fossil fuels, and significant investment is required to deploy a widespread network of charging stations and hydrogen refueling points that can cater to the specific needs of heavy-duty vehicles, including fast charging capabilities and grid stability. Furthermore, regulatory fragmentation and varied emission standards across different regions can create compliance complexities for global manufacturers, necessitating localized adaptations and increasing production costs.

The shortage of skilled labor, including professional truck drivers and technicians trained in emerging vehicle technologies, continues to be a systemic challenge. This scarcity impacts operational efficiency for fleet owners and also affects the ability to maintain and repair advanced HCVs, thereby influencing vehicle uptime and total cost of ownership. Addressing these challenges requires collaborative efforts among governments, industry stakeholders, and technology providers to foster innovation, build supportive infrastructure, and develop a skilled workforce to navigate the evolving landscape of the heavy commercial vehicle market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High R&D and Production Costs for New Technologies | -0.8% | Global | Short to Mid-term (2025-2029) |

| Lack of Adequate Charging/Refueling Infrastructure | -0.7% | Global, particularly long-haul routes | Mid-term (2026-2030) |

| Skilled Labor Shortages (Drivers & Technicians) | -0.6% | North America, Europe, parts of Asia | Short to Long-term (2025-2033) |

| Regulatory Complexity and Fragmentation | -0.5% | Europe, North America, Asia Pacific | Short to Mid-term (2025-2029) |

| Cybersecurity Risks for Connected Vehicles | -0.4% | Global | Mid to Long-term (2026-2033) |

Heavy Commercial Vehicle Market - Updated Report Scope

This comprehensive market research report offers an in-depth analysis of the Heavy Commercial Vehicle market, providing a detailed understanding of its current dynamics, historical performance, and future growth trajectories. The report meticulously covers market size estimations, growth forecasts, key market trends, and a thorough analysis of drivers, restraints, opportunities, and challenges influencing the industry. It also includes an exhaustive segmentation breakdown and regional insights, aimed at providing a holistic view for stakeholders and enabling informed strategic decision-making within the global Heavy Commercial Vehicle sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 820.5 Billion |

| Market Forecast in 2033 | USD 1,350.2 Billion |

| Growth Rate | 6.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Daimler Truck AG, Volvo Group, PACCAR Inc., Traton Group, Ford Motor Company, Isuzu Motors Ltd., Hyundai Motor Company, Tata Motors Ltd., Ashok Leyland, BYD Company Ltd., Navistar International Corporation, FAW Group Co., Ltd., Dongfeng Motor Corporation, SAIC Motor Corporation Limited, Iveco S.p.A., Hino Motors, Ltd., Kenworth, Freightliner, Peterbilt, Nikola Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Heavy Commercial Vehicle (HCV) market is broadly segmented to provide a granular understanding of its diverse components and applications. This segmentation allows for precise analysis of market dynamics across different vehicle types, fuel types, applications, and regional demands, reflecting the complex interplay of various factors driving industry growth. Understanding these segments is crucial for manufacturers to tailor their product offerings, for logistics companies to optimize fleet composition, and for policymakers to implement effective regulations and support infrastructure development. Each segment and sub-segment contributes uniquely to the overall market valuation and future growth trajectory, influenced by specific economic, technological, and regulatory conditions.

- By Vehicle Type:

- Trucks (Light Duty, Medium Duty, Heavy Duty)

- Buses (City Bus, Coach Bus, School Bus)

- Construction Equipment (Excavators, Loaders, Dozers, Dump Trucks)

- Special Purpose Vehicles

- By Application:

- Logistics & Transportation

- Construction & Mining

- Passenger Transport

- Waste Management

- Agriculture

- Others

- By Fuel Type:

- Diesel

- Gasoline

- Electric

- Hybrid

- Natural Gas

- By Emission Standard:

- Bharat Stage VI/Euro VI

- Euro V

- Euro IV

- Others

- By Tonnage Capacity:

- Below 5 Ton

- 5-10 Ton

- 10-15 Ton

- 15-20 Ton

- Above 20 Ton

- By Component:

- Engine

- Transmission

- Axle

- Suspension

- Braking System

- Chassis

- Others

Regional Highlights

The Heavy Commercial Vehicle market exhibits distinct regional dynamics, each influenced by unique economic, regulatory, and infrastructural factors. Asia Pacific stands as the largest and fastest-growing region, primarily driven by rapid industrialization, extensive infrastructure development projects, booming e-commerce, and increasing freight movement in countries like China, India, and Southeast Asian nations. The demand for construction equipment and heavy-duty trucks for logistics is particularly high here, coupled with a growing emphasis on adopting cleaner vehicle technologies due to escalating pollution concerns.

North America and Europe represent mature markets with significant advancements in technology and a strong focus on sustainable transportation. These regions are leading the charge in the adoption of electric and autonomous HCVs, supported by substantial government incentives and stringent emission regulations. While volume growth may be slower compared to Asia Pacific, the focus on high-value, technologically advanced vehicles and integrated fleet solutions is prominent. Investments in charging infrastructure and smart logistics are key trends shaping these markets. Latin America, the Middle East, and Africa (MEA) are emerging regions, where market growth is spurred by expanding trade routes, investments in oil & gas, mining, and urban development projects. Though adoption of advanced technologies is slower, the fundamental demand for reliable heavy commercial transport is steadily increasing as these economies develop, presenting long-term opportunities for market players.

- Asia Pacific: Dominant market due to rapid industrialization, infrastructure development, and thriving e-commerce. China and India are key contributors.

- North America: Significant market share driven by advanced logistics networks, technological adoption (telematics, EV), and renewed infrastructure spending.

- Europe: High adoption of sustainable and high-tech HCVs, influenced by stringent emission norms (Euro VI) and strong focus on green logistics.

- Latin America: Growing demand propelled by increasing trade activities, agricultural expansion, and investments in mining and infrastructure.

- Middle East & Africa (MEA): Emerging market with increasing demand linked to oil & gas sector, construction projects, and developing regional trade corridors.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Heavy Commercial Vehicle Market.- Daimler Truck AG

- Volvo Group

- PACCAR Inc.

- Traton Group

- Ford Motor Company

- Isuzu Motors Ltd.

- Hyundai Motor Company

- Tata Motors Ltd.

- Ashok Leyland

- BYD Company Ltd.

- Navistar International Corporation

- FAW Group Co., Ltd.

- Dongfeng Motor Corporation

- SAIC Motor Corporation Limited

- Iveco S.p.A.

- Hino Motors, Ltd.

- Kenworth

- Freightliner

- Peterbilt

- Nikola Corporation

Frequently Asked Questions

What is a Heavy Commercial Vehicle?

A Heavy Commercial Vehicle (HCV) refers to any vehicle designed and used for transporting heavy loads or large numbers of passengers. This category typically includes large trucks, lorries, buses, coaches, and specialized construction or mining vehicles. They are characterized by their significant gross vehicle weight, robust construction, and high carrying capacity, serving critical roles in logistics, public transport, and various industrial applications.

What are the key trends shaping the Heavy Commercial Vehicle market?

Key trends in the Heavy Commercial Vehicle market include a rapid shift towards electrification and alternative fuel vehicles (such as hydrogen fuel cell trucks), increasing integration of advanced telematics and connectivity for fleet management, and the development of autonomous driving technologies. Additionally, the growing e-commerce sector is driving demand for specialized logistics solutions, while stricter global emission regulations are accelerating innovation in vehicle design and powertrain efficiency.

How is electrification impacting the Heavy Commercial Vehicle industry?

Electrification is profoundly impacting the Heavy Commercial Vehicle industry by driving the development of zero-emission trucks and buses, aiming to reduce carbon footprint and operational costs. While it presents challenges like range limitations and the need for extensive charging infrastructure, it also offers opportunities for quieter operation, lower running costs, and compliance with increasingly stringent environmental regulations, prompting significant R&D investment and new market entrants.

What role does Artificial Intelligence (AI) play in Heavy Commercial Vehicles?

Artificial Intelligence (AI) plays a transformative role in Heavy Commercial Vehicles by enabling predictive maintenance, optimizing logistics and route planning, and enhancing safety through advanced driver-assistance systems (ADAS) and autonomous driving capabilities. AI analyzes vast datasets to improve fuel efficiency, reduce downtime, and manage complex operational scenarios, leading to more efficient, safer, and intelligent transportation solutions.

What are the primary challenges for the Heavy Commercial Vehicle market?

The primary challenges for the Heavy Commercial Vehicle market include the high initial acquisition costs of advanced and electric vehicles, the underdeveloped charging and refueling infrastructure for alternative fuels, and a persistent shortage of skilled drivers and technicians. Furthermore, stringent and varied emission regulations across regions, along with the complexities and costs associated with new technology integration, pose significant hurdles for market growth and operational efficiency.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted