Spoolable Pipe Market

Spoolable Pipe Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707391 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

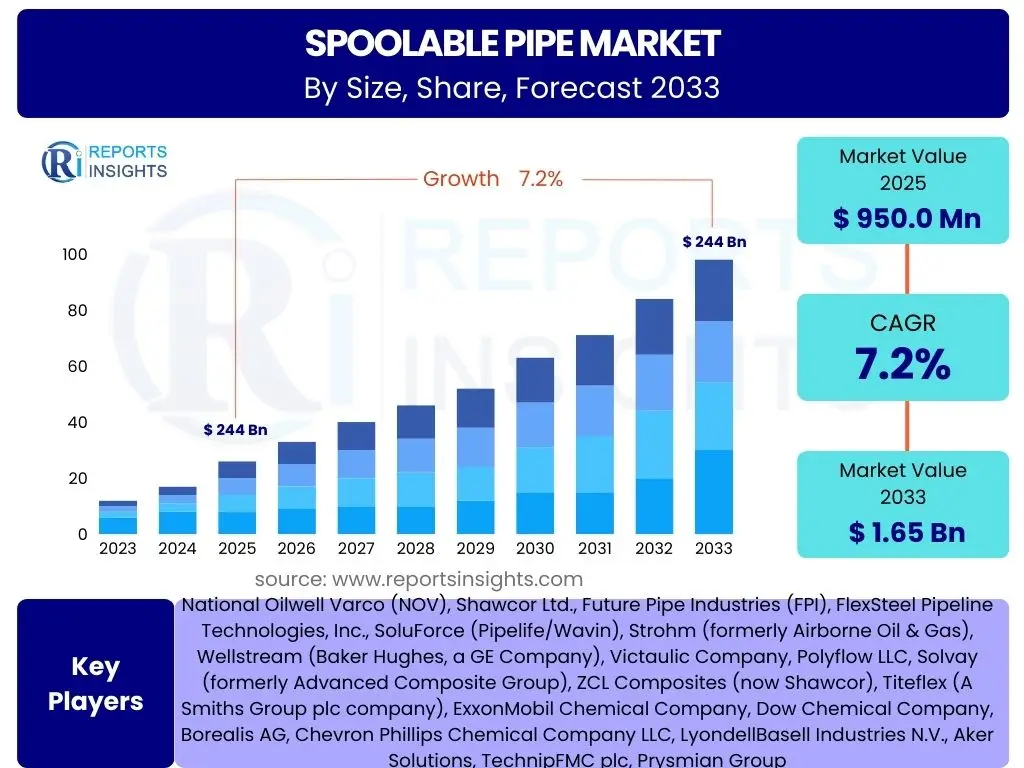

Spoolable Pipe Market Size

According to Reports Insights Consulting Pvt Ltd, The Spoolable Pipe Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.2% between 2025 and 2033. The market is estimated at USD 950.0 Million in 2025 and is projected to reach USD 1.65 Billion by the end of the forecast period in 2033.

Key Spoolable Pipe Market Trends & Insights

User inquiries frequently highlight the evolving landscape of the spoolable pipe market, focusing on how technological advancements, environmental regulations, and economic shifts are shaping its future. A predominant theme is the increasing demand for cost-effective and efficient pipeline solutions in both new and aging infrastructure projects. There is a strong interest in understanding the adoption rates of composite and thermoplastic materials over traditional steel, driven by their superior corrosion resistance, lighter weight, and easier installation. Furthermore, the market is witnessing a surge in applications beyond traditional oil and gas, extending into water, wastewater, and industrial sectors, reflecting a diversification of demand and a broader recognition of spoolable pipe benefits.

The market's trajectory is also heavily influenced by global energy transition efforts, prompting a closer look at the suitability of spoolable pipes for transporting new energy carriers like hydrogen or CO2. Users are keen to know about advancements in material science that enhance performance under extreme conditions, as well as the integration of smart technologies for monitoring and maintenance. The drive for operational expenditure reduction and improved safety profiles is consistently identified as a key factor steering market trends, with stakeholders exploring how these pipes can contribute to sustainable and resilient pipeline networks worldwide.

- Growing adoption of composite and thermoplastic materials due to corrosion resistance and ease of installation.

- Expansion of spoolable pipe applications beyond oil and gas to water, wastewater, and industrial sectors.

- Increasing focus on cost-efficiency and reduced operational expenditure in pipeline projects.

- Development of higher pressure and temperature rating pipes for demanding environments.

- Integration of smart monitoring and diagnostic technologies for enhanced pipeline integrity.

AI Impact Analysis on Spoolable Pipe

User queries regarding the impact of Artificial Intelligence (AI) on the spoolable pipe sector reveal a keen interest in how advanced analytics and machine learning can optimize various stages of the product lifecycle. Stakeholders are particularly curious about AI's potential in improving design precision, enhancing manufacturing efficiency, and revolutionizing predictive maintenance. The expectation is that AI algorithms will enable more accurate material selection, identify optimal pipe geometries, and streamline production processes by minimizing waste and defects, thereby leading to cost savings and improved product quality.

Furthermore, there is significant anticipation for AI's role in operational intelligence, including real-time pipeline monitoring, anomaly detection, and predicting potential failures before they occur. This predictive capability could drastically reduce downtime, enhance safety, and extend the lifespan of installed spoolable pipe systems. Users also foresee AI facilitating more efficient logistics and inventory management, as well as informing strategic decisions based on market demand forecasting and supply chain optimization, ultimately transforming the way spoolable pipes are manufactured, deployed, and maintained.

- Optimization of manufacturing processes through AI-driven quality control and defect detection.

- Enhanced predictive maintenance capabilities for installed pipes, reducing downtime and operational costs.

- AI-assisted material design and selection for improved performance characteristics.

- Streamlined logistics and supply chain management using AI for demand forecasting and route optimization.

- Development of smart monitoring systems for real-time pipeline integrity and anomaly detection.

Key Takeaways Spoolable Pipe Market Size & Forecast

Common user questions regarding key takeaways from the spoolable pipe market size and forecast consistently point towards an optimistic outlook for growth, driven by fundamental shifts in industry priorities. The primary insight is the market's robust expansion, fueled by the imperative for cost-effective, durable, and environmentally less impactful pipeline solutions across diverse sectors. Users are keen to understand that the anticipated growth is not merely incremental but represents a significant transition from traditional steel pipelines, particularly in scenarios where corrosion resistance, ease of installation, and operational longevity are paramount.

Another key takeaway is the increasing diversification of applications beyond oil and gas, with water management, mining, and industrial sectors emerging as significant growth catalysts. This diversification underscores the versatility and inherent advantages of spoolable pipe technologies. Furthermore, the forecast highlights the ongoing innovation in material science and manufacturing techniques, which continue to enhance the performance envelope of these pipes, making them suitable for more challenging environments and new energy transport mediums. The market is poised for sustained growth as industries increasingly prioritize efficiency, safety, and reduced environmental footprint in their infrastructure development.

- Significant market growth projected, driven by demand for cost-efficient and corrosion-resistant pipeline solutions.

- Broadening application base beyond conventional oil and gas to include water, wastewater, and industrial segments.

- Technological advancements in composite and thermoplastic materials are enhancing product performance and adoption.

- Emphasis on reducing installation time and operational expenditure continues to boost market appeal.

- Market expansion is global, with strong prospects in regions requiring rapid infrastructure development or maintenance.

Spoolable Pipe Market Drivers Analysis

The spoolable pipe market is propelled by a confluence of factors, primarily the increasing demand for pipeline infrastructure that offers enhanced efficiency, durability, and cost-effectiveness compared to traditional rigid pipes. The aging infrastructure across developed nations necessitates frequent repairs and replacements, where the rapid deployment and minimal disruption offered by spoolable pipes provide a significant advantage. Furthermore, the global shift towards unconventional oil and gas exploration, particularly in remote or challenging terrains, drives the need for lightweight, flexible, and corrosion-resistant piping solutions that can be installed quickly and economically.

Environmental regulations and the growing emphasis on reducing carbon footprints also play a crucial role, as composite and thermoplastic spoolable pipes offer superior leak integrity and often require less energy for manufacturing and transportation. The inherent resistance to corrosion eliminates the need for cathodic protection, leading to lower maintenance costs and a longer operational lifespan. Lastly, the diversification of applications beyond hydrocarbons, into industries such as water management, mining, and industrial fluid transfer, is expanding the market's reach and establishing new growth avenues for these innovative piping solutions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Aging Infrastructure & Replacement Needs | +1.1% | North America, Europe, APAC | Medium-to-Long Term |

| Growing Demand for Corrosion-Resistant Pipes | +1.3% | Global, especially Middle East, Latin America | Short-to-Medium Term |

| Cost-Efficiency & Reduced Installation Time | +1.0% | Global, particularly emerging economies | Short-to-Medium Term |

| Expansion of Unconventional Oil & Gas Exploration | +0.9% | North America, Middle East, Asia Pacific | Medium Term |

| Diversification of Applications (Water, Mining, Industrial) | +0.8% | Global | Long Term |

Spoolable Pipe Market Restraints Analysis

Despite its significant advantages, the spoolable pipe market faces several restraints that could impede its growth trajectory. One primary constraint is the volatility of crude oil and natural gas prices, which directly impacts investment in new pipeline projects within the dominant oil and gas sector. Periods of low commodity prices often lead to project deferrals or cancellations, consequently dampening demand for spoolable pipes. Additionally, the relatively higher initial capital expenditure for spoolable pipes compared to some traditional steel pipes can be a deterrent for budget-conscious operators, particularly for projects where long-term operational savings are not immediately prioritized or fully understood.

Another significant restraint is the limited awareness and conservative adoption rates in certain regions or specific industry segments. While spoolable pipes offer clear benefits, the entrenched preferences for conventional piping materials, combined with a lack of comprehensive understanding about their long-term performance and lifecycle costs, can slow market penetration. Furthermore, the specialized handling and installation procedures, though often faster, require specific training and equipment, which can present a barrier to entry for contractors unfamiliar with the technology. Regulatory hurdles and the need for new standards for emerging applications also pose challenges, potentially delaying widespread acceptance and deployment.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility of Crude Oil & Gas Prices | -0.8% | Global, especially Oil & Gas producing regions | Short-to-Medium Term |

| High Initial Capital Expenditure | -0.6% | Emerging Economies, Cost-Sensitive Markets | Short Term |

| Limited Awareness & Adoption in Traditional Markets | -0.5% | Global, particularly some APAC & MEA countries | Medium Term |

| Specialized Installation & Training Requirements | -0.4% | Global | Short Term |

Spoolable Pipe Market Opportunities Analysis

The spoolable pipe market is presented with significant opportunities, primarily driven by the expanding scope of its applications beyond conventional oil and gas. The growing global demand for clean water infrastructure, coupled with the need for efficient wastewater treatment and transportation, opens substantial new avenues for spoolable pipes due to their corrosion resistance and ease of installation in challenging environments. Furthermore, the push towards sustainable energy solutions, including hydrogen transport and carbon capture, utilization, and storage (CCUS) projects, represents a nascent but potentially transformative opportunity for these pipes, requiring materials that can safely handle novel media under varied conditions.

Technological advancements in composite materials, such as the development of pipes with higher pressure ratings, improved chemical resistance, and enhanced thermal properties, are continuously expanding the addressable market for spoolable solutions. This allows for their deployment in more demanding industrial processes and offshore applications. Moreover, the increasing focus on pipeline integrity management and the adoption of smart monitoring technologies present opportunities for manufacturers to offer integrated solutions, bundling advanced pipes with digital surveillance systems. Lastly, the ongoing efforts to reduce overall project timelines and costs, especially in remote or difficult-to-access locations, create a compelling business case for the inherent logistical and installation efficiencies offered by spoolable pipe technology.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Water & Wastewater Infrastructure | +1.2% | Global, particularly Asia Pacific & Latin America | Medium-to-Long Term |

| Emerging Applications in New Energy (Hydrogen, CCUS) | +0.9% | Europe, North America, Middle East | Long Term |

| Technological Advancements in Material Science | +0.8% | Global | Medium Term |

| Increased Focus on Pipeline Integrity & Smart Monitoring | +0.7% | North America, Europe | Medium Term |

Spoolable Pipe Market Challenges Impact Analysis

The spoolable pipe market faces several inherent challenges that require innovative solutions and strategic adaptation. One significant challenge is the ongoing competition from traditional steel pipes, which are well-established, widely understood, and often benefit from economies of scale, especially in large-diameter, high-pressure applications where steel still holds a strong market position. While spoolable pipes excel in many areas, overcoming the inertia of existing infrastructure and procurement practices remains a hurdle. Additionally, the complexity associated with material compatibility for diverse fluid compositions and extreme operating conditions presents a continuous technical challenge, as manufacturers must ensure their products meet rigorous industry standards and performance requirements.

Another challenge stems from the need for specialized equipment and trained personnel for the installation and repair of spoolable pipes. Although installation is often faster, the initial investment in this specialized equipment and the ongoing training requirements for crews can be a barrier for some operators, especially in regions with less developed infrastructure or a shortage of skilled labor. Furthermore, managing the entire supply chain, from raw material procurement to final installation, can be complex due to the global nature of projects and the need for just-in-time delivery of customized pipe lengths. Navigating evolving regulatory landscapes and obtaining approvals for new applications or materials also presents an ongoing challenge for market participants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Competition from Traditional Steel Pipes | -0.7% | Global | Short-to-Medium Term |

| Complexity of Material Compatibility & Standards | -0.5% | Global | Medium Term |

| Need for Specialized Installation Equipment & Training | -0.4% | Global, particularly developing regions | Short Term |

| Supply Chain & Logistics Management | -0.3% | Global | Short Term |

Spoolable Pipe Market - Updated Report Scope

This report provides a detailed analysis of the global spoolable pipe market, encompassing a comprehensive study of market size, trends, drivers, restraints, opportunities, and challenges. It offers an in-depth segmentation analysis by material, application, and end-use, providing granular insights into key growth segments. The report also highlights regional market dynamics, identifying prominent growth areas and country-specific influences. Furthermore, it profiles leading market players, offering an understanding of their strategies, product portfolios, and competitive positioning within the industry. The scope extends to a forward-looking forecast period, projecting market evolution and identifying key investment opportunities from 2025 to 2033.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 950.0 Million |

| Market Forecast in 2033 | USD 1.65 Billion |

| Growth Rate | 7.2% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | National Oilwell Varco (NOV), Shawcor Ltd., Future Pipe Industries (FPI), FlexSteel Pipeline Technologies, Inc., SoluForce (Pipelife/Wavin), Strohm (formerly Airborne Oil & Gas), Wellstream (Baker Hughes, a GE Company), Victaulic Company, Polyflow LLC, Solvay (formerly Advanced Composite Group), ZCL Composites (now Shawcor), Titeflex (A Smiths Group plc company), ExxonMobil Chemical Company, Dow Chemical Company, Borealis AG, Chevron Phillips Chemical Company LLC, LyondellBasell Industries N.V., Aker Solutions, TechnipFMC plc, Prysmian Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The spoolable pipe market is meticulously segmented to provide a granular understanding of its diverse components and growth drivers. This segmentation allows for targeted analysis of material preferences, application specific demands, and varying end-use requirements, revealing nuanced market dynamics. By categorizing the market based on the type of material used, the specific industry application, and the operational environment, stakeholders can identify niche opportunities, understand competitive landscapes within specific sub-segments, and tailor their strategies for maximum impact. This structured approach ensures a comprehensive view of the market's current state and future potential across its multifaceted dimensions.

- By Material:

- Composites: Fiber Reinforced Plastic (FRP), Glass Reinforced Epoxy (GRE), Reinforced Thermoplastic Pipe (RTP)

- Thermoplastics: High-Density Polyethylene (HDPE), Polyethylene of Raised Temperature (PE-RT), Polyamide (PA)

- Steel

- By Application:

- Oil & Gas: Onshore Gathering & Flowlines, Offshore Risers & Jumpers, Midstream Pipeline Rehabilitation, Downstream Facilities

- Chemical & Industrial: Chemical Processing Plants, Mining Operations, Power Generation Facilities, General Industrial Fluid Transfer

- Water & Wastewater: Potable Water Supply, Sewage and Drainage Systems, Irrigation

- By End-use:

- Onshore

- Offshore

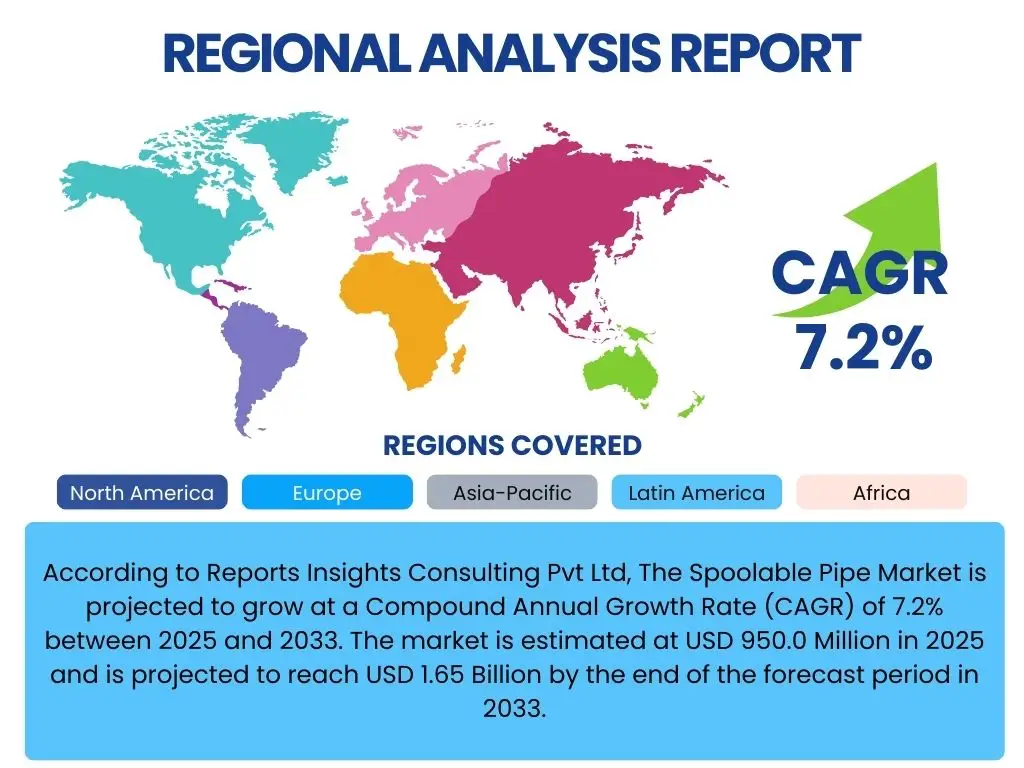

Regional Highlights

- North America: A dominant market driven by extensive oil and gas activities, particularly in unconventional resource extraction (shale gas, tight oil), aging pipeline infrastructure requiring rehabilitation, and a strong focus on enhancing operational efficiency and safety. The region benefits from early adoption of advanced piping solutions and significant R&D investments.

- Europe: Characterized by stringent environmental regulations, a strong emphasis on reducing carbon emissions, and increasing investment in renewable energy infrastructure. The market here is driven by pipeline replacement needs, offshore energy projects, and growing applications in water and wastewater management.

- Asia Pacific (APAC): Expected to be the fastest-growing region due to rapid industrialization, increasing energy demand, and significant investments in new infrastructure projects. Countries like China, India, and Southeast Asian nations are witnessing substantial growth in oil and gas, industrial, and water sectors, boosting the demand for cost-effective and durable piping solutions.

- Latin America: Holds considerable potential, especially in countries like Brazil, Mexico, and Argentina, driven by offshore oil and gas exploration, expanding midstream infrastructure, and the need for robust solutions in remote and challenging terrains. Economic development initiatives also fuel demand for water and industrial applications.

- Middle East and Africa (MEA): A crucial market, particularly due to large-scale oil and gas production and export activities. The region's hot and corrosive environments make spoolable pipes a preferred choice for their durability and corrosion resistance. Investments in new upstream and midstream projects, alongside diversification into industrial and water sectors, will drive growth.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Spoolable Pipe Market.- National Oilwell Varco (NOV)

- Shawcor Ltd.

- Future Pipe Industries (FPI)

- FlexSteel Pipeline Technologies, Inc.

- SoluForce (Pipelife/Wavin)

- Strohm (formerly Airborne Oil & Gas)

- Wellstream (Baker Hughes, a GE Company)

- Victaulic Company

- Polyflow LLC

- Solvay (formerly Advanced Composite Group)

- ZCL Composites (now Shawcor)

- Titeflex (A Smiths Group plc company)

- ExxonMobil Chemical Company

- Dow Chemical Company

- Borealis AG

- Chevron Phillips Chemical Company LLC

- LyondellBasell Industries N.V.

- Aker Solutions

- TechnipFMC plc

- Prysmian Group

Frequently Asked Questions

What are spoolable pipes?

Spoolable pipes are continuous, flexible piping systems manufactured from composite or thermoplastic materials, wound onto spools or reels for transportation and rapid installation. They offer significant advantages over traditional rigid pipes, including corrosion resistance, lighter weight, and reduced installation time and cost.

What are the primary applications of spoolable pipes?

Spoolable pipes are predominantly used in the oil and gas industry for onshore gathering lines, flowlines, and offshore risers. Their applications are expanding into water and wastewater management, chemical and industrial fluid transfer, and mining operations due to their durability and efficiency.

What are the main benefits of using spoolable pipes?

Key benefits include superior corrosion resistance, eliminating the need for cathodic protection; significant reduction in installation time and labor costs due to their continuous length; lighter weight, simplifying transport; and enhanced durability in challenging environments, leading to lower maintenance expenses and a longer service life.

How do spoolable pipes contribute to cost savings?

Cost savings are realized through reduced installation time, requiring fewer welds or connections; lower transportation costs due to lighter weight; minimized maintenance expenses from corrosion resistance; and an extended operational lifespan, contributing to a lower total cost of ownership compared to traditional piping solutions.

What is the future outlook for the spoolable pipe market?

The market is projected for robust growth, driven by increasing global demand for efficient and durable pipeline infrastructure, the expansion of applications into new sectors like water and new energy, and ongoing technological advancements enhancing pipe performance and versatility. Focus on sustainability and operational efficiency will further accelerate adoption.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted