CPVC Pipe and Fitting Market

CPVC Pipe and Fitting Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707374 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

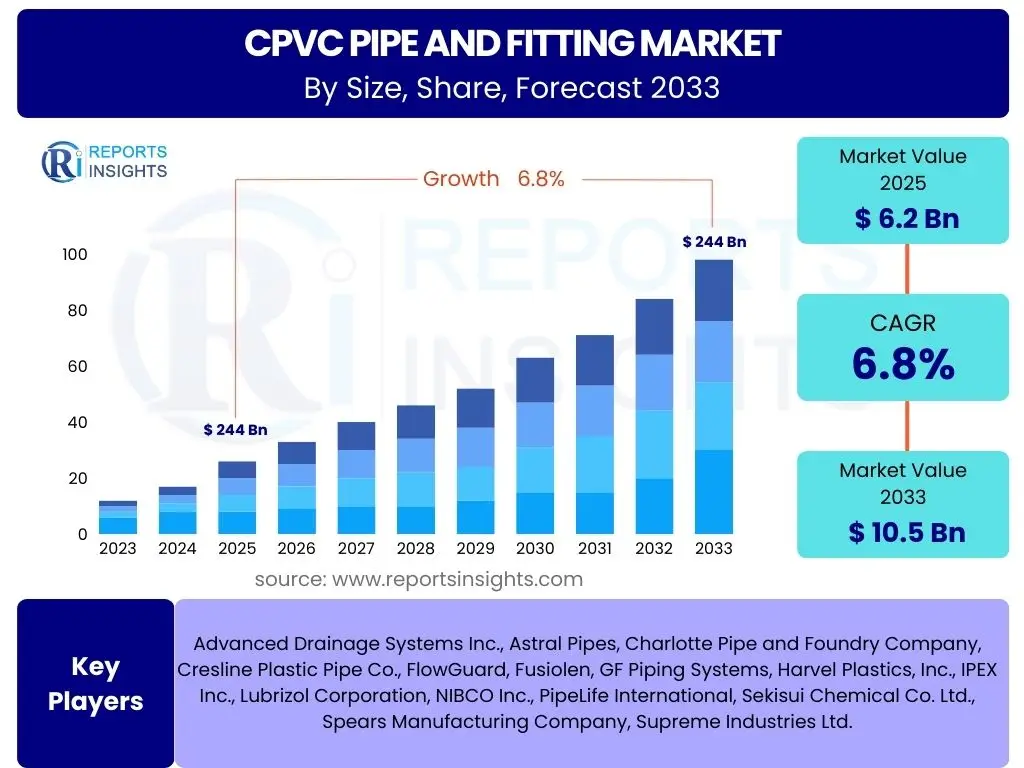

CPVC Pipe and Fitting Market Size

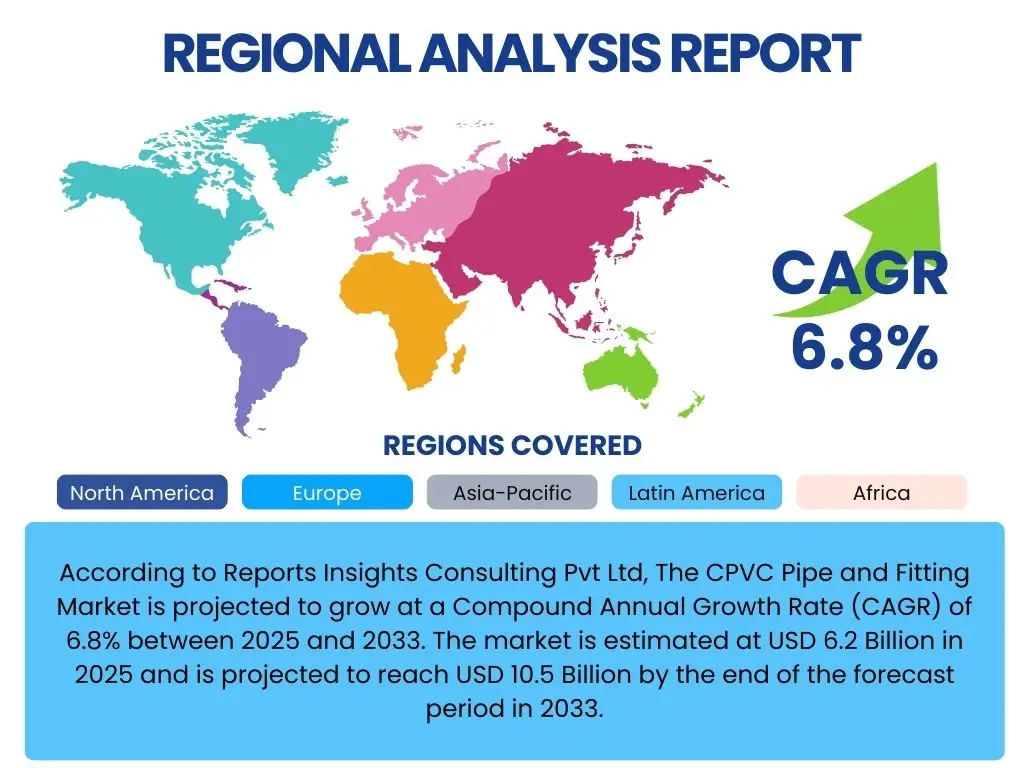

According to Reports Insights Consulting Pvt Ltd, The CPVC Pipe and Fitting Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 6.2 Billion in 2025 and is projected to reach USD 10.5 Billion by the end of the forecast period in 2033.

Key CPVC Pipe and Fitting Market Trends & Insights

Current market discourse indicates a strong user interest in understanding the evolving landscape of the CPVC pipe and fitting sector. Common inquiries revolve around the adoption of sustainable manufacturing practices, the integration of smart technologies for performance monitoring, and the shifting preferences in building and construction materials. Users are also keen to learn about the impact of stringent regulatory standards on product development and market entry, alongside the increasing demand for fire-resistant and corrosion-proof piping solutions across various industries.

The market is witnessing a notable trend towards customization and specialized solutions, driven by diverse application requirements in residential, commercial, and industrial settings. This includes the development of CPVC products with enhanced pressure ratings and temperature resistance for demanding environments. Furthermore, the global emphasis on improving water infrastructure and sanitation systems in developing economies is creating new avenues for market expansion, pushing manufacturers to innovate in terms of material efficiency and installation ease.

- Increasing adoption in residential and commercial plumbing due to durability and cost-effectiveness.

- Growing demand for hot and cold-water distribution systems in new construction and renovation projects.

- Emphasis on fire safety and chemical resistance driving usage in industrial applications.

- Development of sustainable and lead-free CPVC formulations in response to environmental regulations.

- Rise of pre-fabricated CPVC piping solutions for faster and more efficient installations.

- Technological advancements leading to improved performance characteristics and extended product lifespan.

AI Impact Analysis on CPVC Pipe and Fitting

User queries regarding the impact of Artificial Intelligence (AI) on the CPVC Pipe and Fitting market frequently explore its potential to optimize manufacturing processes, enhance quality control, and streamline supply chain logistics. Stakeholders are interested in how AI can contribute to predictive maintenance for piping systems, improve material science for new compound development, and automate design and engineering tasks, leading to faster project completion and reduced costs. There is a general expectation that AI will introduce efficiencies that were previously unattainable through traditional methods, ultimately transforming production and distribution methodologies.

AI's influence extends beyond just manufacturing efficiency. Users anticipate its role in demand forecasting, enabling manufacturers to better predict market needs and optimize inventory management, thereby reducing waste and improving responsiveness. Furthermore, AI-powered analytics can process vast amounts of performance data from installed CPVC systems, providing insights into durability, failure points, and optimal usage conditions, which can feed back into product design and material improvement. This analytical capability is expected to significantly enhance product reliability and customer satisfaction.

- AI-driven optimization of manufacturing processes for reduced waste and energy consumption.

- Enhanced quality control through AI-powered defect detection in production lines.

- Predictive maintenance analytics for installed CPVC piping systems to prevent failures.

- Supply chain optimization using AI for demand forecasting and inventory management.

- Automated design and simulation of CPVC pipe networks for improved efficiency and accuracy.

- Material innovation and formulation discovery accelerated by AI algorithms.

Key Takeaways CPVC Pipe and Fitting Market Size & Forecast

User inquiries about the key takeaways from the CPVC Pipe and Fitting market size and forecast consistently point towards a desire to understand the primary drivers of growth, the segments offering the most lucrative opportunities, and the overall trajectory of the market. There is a keen interest in identifying which regions are poised for significant expansion and how technological advancements are expected to influence market dynamics over the forecast period. The summary below addresses these core concerns, providing a concise overview of the market's current state and future outlook.

The market is characterized by robust growth, primarily fueled by extensive infrastructure development and increasing urbanization in emerging economies. The inherent advantages of CPVC, such as corrosion resistance, high-temperature tolerance, and ease of installation, continue to make it a preferred material across various applications, from residential plumbing to industrial fluid handling. The forecast indicates sustained expansion, with innovation in product formulations and manufacturing techniques playing a crucial role in maintaining market momentum and addressing evolving industry standards.

- Significant growth projected, driven by global construction and infrastructure spending.

- Asia Pacific anticipated to be a dominant and rapidly growing region due to urbanization.

- Residential and commercial plumbing remain primary application segments.

- Emphasis on product innovation for improved performance and environmental compliance.

- Market resilience despite raw material price fluctuations due to strong end-user demand.

CPVC Pipe and Fitting Market Drivers Analysis

The CPVC Pipe and Fitting market is propelled by a confluence of factors that underscore its increasing utility and preference across diverse sectors. A primary driver is the burgeoning construction industry globally, particularly in developing nations, where rapid urbanization and infrastructure development necessitate efficient and durable piping solutions for residential, commercial, and industrial buildings. The superior properties of CPVC, such as its resistance to corrosion, high-temperature tolerance, and longevity, make it an ideal choice over traditional materials like galvanized iron or copper, leading to higher adoption rates.

Furthermore, the growing demand for safe and reliable water distribution systems, alongside efficient waste management solutions, significantly contributes to market expansion. Governments and private entities worldwide are investing heavily in upgrading aging infrastructure and developing new networks, where CPVC's low maintenance requirements and ease of installation offer substantial long-term benefits. Regulatory support for lead-free and sustainable piping materials also acts as a catalyst, pushing industries towards CPVC alternatives that comply with stricter environmental and health standards.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Urbanization & Construction Growth | +1.5% | Asia Pacific, Middle East & Africa | Short to Medium Term (2025-2029) |

| Increasing Investment in Water Infrastructure | +1.2% | North America, Europe, South Asia | Medium to Long Term (2027-2033) |

| Superior Properties (Corrosion & Temp. Resistance) | +1.0% | Global | Long Term (2025-2033) |

| Replacement of Traditional Piping Materials | +0.8% | Developed Economies | Medium Term (2026-2030) |

| Strict Regulatory Standards for Potable Water | +0.7% | Europe, North America | Short Term (2025-2027) |

CPVC Pipe and Fitting Market Restraints Analysis

Despite its robust growth prospects, the CPVC Pipe and Fitting market faces several restraints that could temper its expansion. One significant challenge is the volatility and fluctuation in the prices of raw materials, particularly chlorine and vinyl chloride monomer (VCM), which are essential components in CPVC production. These price variations can directly impact manufacturing costs, leading to increased product prices and potentially affecting market demand, especially in price-sensitive regions or segments. Managing these raw material costs requires sophisticated procurement strategies and robust supply chain management.

Another notable restraint is the intense competition from alternative piping materials such as PVC, PEX, HDPE, and PPR. While CPVC offers distinct advantages in specific applications, these alternatives often present lower upfront costs or different performance characteristics that appeal to certain segments of the market. The pervasive use of these substitutes, coupled with established supply chains and consumer familiarity, can limit CPVC's market penetration. Furthermore, the complexities associated with recycling CPVC, compared to some other plastics, can also pose an environmental challenge and a perceived drawback in increasingly sustainability-conscious markets.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw Material Price Volatility | -0.9% | Global | Short to Medium Term (2025-2028) |

| Competition from Alternative Piping Materials | -0.7% | Global | Long Term (2025-2033) |

| Perceived High Initial Cost vs. Alternatives | -0.5% | Developing Economies | Medium Term (2026-2030) |

| Limited Awareness in Certain Regions | -0.4% | Africa, Parts of Asia | Short Term (2025-2027) |

CPVC Pipe and Fitting Market Opportunities Analysis

The CPVC Pipe and Fitting market is presented with significant opportunities, primarily stemming from the rapid industrialization and urbanization across emerging economies. These regions are undergoing massive infrastructure development, creating a substantial demand for modern, efficient, and durable piping systems for new residential complexes, commercial buildings, and industrial facilities. The shift towards multi-story buildings and integrated townships further fuels the need for CPVC due to its robust performance in high-pressure and high-temperature applications, making it a preferred choice over traditional materials.

Another major opportunity lies in the replacement and renovation of aging infrastructure in developed countries. Many existing water and waste management systems utilize outdated materials prone to corrosion and leakage, leading to significant water losses and maintenance costs. CPVC offers a cost-effective and long-lasting solution for these upgrades, complying with contemporary health and safety standards, particularly concerning potable water supply. Furthermore, the increasing focus on sustainable building practices and the demand for green construction materials provide an impetus for CPVC manufacturers to innovate and offer environmentally friendly solutions, expanding their market footprint in this growing niche.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Infrastructure Development in Emerging Economies | +1.8% | Asia Pacific, Latin America, MEA | Long Term (2025-2033) |

| Replacement of Aging Infrastructure | +1.4% | North America, Europe | Medium to Long Term (2027-2033) |

| Growing Demand for Sustainable Building Materials | +1.0% | Global | Long Term (2025-2033) |

| Diversification into Industrial Applications (Chemical, HVAC) | +0.8% | Global | Medium Term (2026-2030) |

| Expansion in Niche Markets (Marine, Agriculture) | +0.6% | Global | Short to Medium Term (2025-2029) |

CPVC Pipe and Fitting Market Challenges Impact Analysis

The CPVC Pipe and Fitting market encounters several significant challenges that necessitate strategic responses from industry participants. A primary challenge involves navigating the complex and evolving regulatory landscape. Different regions and countries have varying standards for material composition, manufacturing processes, and installation guidelines for piping systems. Adhering to these diverse and often stringent regulations, particularly those concerning environmental impact and potable water safety, can increase compliance costs and limit market entry or expansion for manufacturers, requiring continuous R&D and adaptation.

Another critical challenge is the intense competition from a wide array of alternative piping materials. While CPVC possesses distinct advantages, materials like cross-linked polyethylene (PEX), polypropylene random copolymer (PPR), and high-density polyethylene (HDPE) often compete on factors such as cost, ease of installation, or specific application suitability. This competitive pressure necessitates ongoing innovation in CPVC product development, marketing, and pricing strategies to maintain and expand market share. Additionally, the need for skilled labor for proper installation and maintenance of CPVC systems can pose a challenge in regions where such expertise is scarce, potentially affecting the quality and longevity of installations.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Regulatory Compliance | -0.8% | Europe, North America, India | Long Term (2025-2033) |

| Intense Competition from Substitute Materials | -0.6% | Global | Long Term (2025-2033) |

| Skilled Labor Availability for Installation | -0.4% | Developing Economies | Medium Term (2026-2030) |

| Managing Perceptions Around Plastic Piping | -0.3% | Developed Economies | Short to Medium Term (2025-2029) |

CPVC Pipe and Fitting Market - Updated Report Scope

This report provides a comprehensive analysis of the global CPVC Pipe and Fitting Market, segmenting the market by product type, application, and end-use industry. It offers detailed insights into market size, growth trends, key drivers, restraints, opportunities, and challenges affecting the industry's trajectory from 2025 to 2033. The scope includes an in-depth examination of regional market dynamics across major geographies and profiles of leading market players, offering a holistic view for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.2 Billion |

| Market Forecast in 2033 | USD 10.5 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Advanced Drainage Systems Inc., Astral Pipes, Charlotte Pipe and Foundry Company, Cresline Plastic Pipe Co., FlowGuard, Fusiolen, GF Piping Systems, Harvel Plastics, Inc., IPEX Inc., Lubrizol Corporation, NIBCO Inc., PipeLife International, Sekisui Chemical Co. Ltd., Spears Manufacturing Company, Supreme Industries Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The CPVC Pipe and Fitting Market is comprehensively segmented to provide granular insights into its diverse components, allowing for a detailed understanding of market dynamics across various categories. This segmentation helps identify key growth areas, consumer preferences, and technological shifts within specific sub-markets. The market is primarily categorized by type of pipe and fitting, various application areas, and the end-use industries that predominantly utilize CPVC products, offering a multi-dimensional view of market demand and supply.

Each segment reflects unique market drivers and challenges, from the technical specifications required for different pipe schedules to the varying demands of residential versus industrial applications. Analyzing these segments individually and in conjunction with each other reveals intricate patterns of adoption, competitive landscapes, and regional consumption trends. This detailed breakdown is essential for stakeholders seeking to formulate targeted strategies and capitalize on specific market niches, ensuring that product development and marketing efforts are aligned with the precise needs of each segment.

- By Type:

- Schedule 40: Commonly used for residential and light commercial plumbing, lower pressure applications.

- Schedule 80: Designed for industrial applications and higher pressure systems, offering increased wall thickness and durability.

- Others (e.g., SDR series): Includes pipes with different standard dimension ratios for specific pressure ratings and applications.

- By Application:

- Residential: Hot and cold-water distribution, drainage, and vent systems in homes.

- Commercial: Plumbing and HVAC systems in offices, hotels, hospitals, and educational institutions.

- Industrial: Chemical processing, water treatment, and specialized fluid handling in manufacturing plants.

- By End-Use Industry:

- Building & Construction: Encompasses general plumbing and piping in new constructions and renovations.

- Chemical Processing: Transportation of corrosive chemicals due to CPVC's chemical resistance.

- Water Treatment: Piping for water purification and distribution systems.

- Fire Sprinkler Systems: Due to high-temperature resistance and fire performance properties.

- HVAC: Heating, ventilation, and air conditioning systems for water circulation.

- Others: Includes applications in agriculture, marine, and mining.

Regional Highlights

- North America: A mature market with steady demand for CPVC in residential and commercial plumbing renovations. Stringent building codes and a focus on lead-free solutions drive adoption. Significant investment in upgrading existing water infrastructure contributes to stable growth.

- Europe: Characterized by strict environmental regulations and high standards for potable water systems. The demand is driven by sustainable construction practices and the replacement of older piping materials. Germany and the UK are key markets with strong R&D activities.

- Asia Pacific (APAC): The fastest-growing region, fueled by rapid urbanization, massive infrastructure development, and a booming construction sector, especially in China and India. Increasing disposable incomes and a shift towards modern plumbing solutions are key drivers.

- Latin America: Exhibiting promising growth due to expanding construction activities and improving access to clean water in several countries. Brazil and Mexico are leading the regional market, with increasing awareness of CPVC benefits.

- Middle East & Africa (MEA): Growth is primarily driven by mega-construction projects, especially in the UAE and Saudi Arabia, alongside ongoing efforts to improve water and sanitation infrastructure across Africa. The harsh climate conditions favor CPVC's durability.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the CPVC Pipe and Fitting Market.- Advanced Drainage Systems Inc.

- Astral Pipes

- Charlotte Pipe and Foundry Company

- Cresline Plastic Pipe Co.

- FlowGuard

- Fusiolen

- GF Piping Systems

- Harvel Plastics, Inc.

- IPEX Inc.

- Lubrizol Corporation

- NIBCO Inc.

- PipeLife International

- Sekisui Chemical Co. Ltd.

- Spears Manufacturing Company

- Supreme Industries Ltd.

Frequently Asked Questions

What is the projected growth rate of the CPVC Pipe and Fitting Market?

The CPVC Pipe and Fitting Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, driven by increasing demand from the construction and industrial sectors.

What are the primary applications of CPVC pipes and fittings?

CPVC pipes and fittings are primarily used in residential and commercial plumbing for hot and cold-water distribution, industrial fluid handling (especially corrosive chemicals), fire sprinkler systems, and various water treatment applications.

Which region is expected to lead the CPVC Pipe and Fitting Market growth?

The Asia Pacific region is anticipated to lead the market growth due to rapid urbanization, significant infrastructure development, and a booming construction industry in countries like China and India.

What are the key advantages of CPVC over traditional piping materials?

CPVC offers superior advantages such as excellent corrosion resistance, high-temperature tolerance, pressure durability, low thermal conductivity, and ease of installation, making it a preferred alternative to materials like copper or galvanized iron.

What are the main challenges faced by the CPVC Pipe and Fitting Market?

Key challenges include volatility in raw material prices, intense competition from alternative piping materials (e.g., PEX, PPR), and the need to comply with diverse and evolving regional regulatory standards for product quality and environmental impact.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted