Specialized Threat Analysi and Protection Market

Specialized Threat Analysi and Protection Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709951 | Last Updated : December 24, 2025 |

Format : ![]()

![]()

![]()

![]()

Specialized Threat Analysi and Protection Market Size

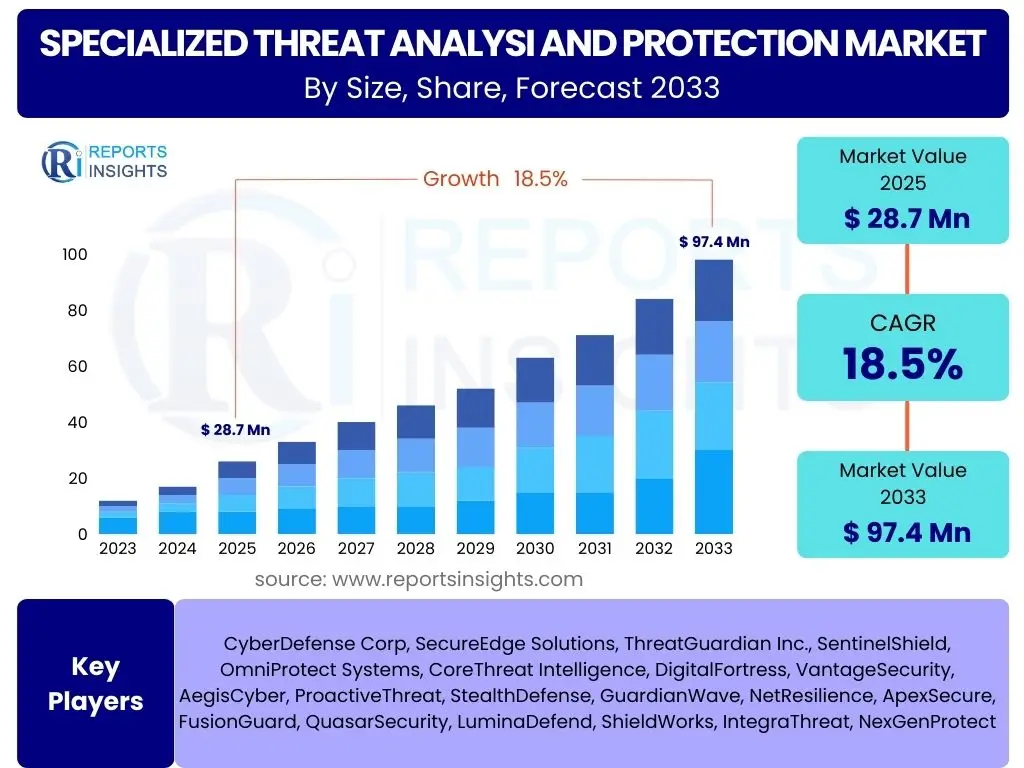

According to Reports Insights Consulting Pvt Ltd, The Specialized Threat Analysi and Protection Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 28.7 Billion in 2025 and is projected to reach USD 97.4 Billion by the end of the forecast period in 2033.

The consistent expansion of the specialized threat analysis and protection market is primarily driven by the escalating sophistication and volume of cyber threats globally. Enterprises across all sectors are facing advanced persistent threats (APTs), zero-day exploits, and highly targeted attacks that traditional security measures often fail to detect. This growing threat landscape necessitates the adoption of more advanced and specialized solutions capable of deep analysis, behavioral anomaly detection, and proactive threat hunting, thereby fueling market demand.

Furthermore, the rapid digital transformation initiatives undertaken by organizations, including the widespread adoption of cloud computing, IoT devices, and remote work models, have significantly expanded the attack surface. This expansion creates new vulnerabilities that specialized threat analysis and protection solutions are designed to address. The increasing regulatory pressure for data privacy and security compliance also compels businesses to invest in robust security frameworks, further contributing to the market's robust growth trajectory through the forecast period.

Key Specialized Threat Analysi and Protection Market Trends & Insights

The specialized threat analysis and protection market is undergoing significant evolution, driven by the dynamic nature of cyber threats and technological advancements. User inquiries frequently center on understanding the leading innovations, shifts in defensive strategies, and the integration of emerging technologies within this critical security domain. Key trends indicate a pronounced move towards predictive and proactive security measures, a greater emphasis on automation to combat alert fatigue, and the pervasive integration of artificial intelligence and machine learning to enhance detection and response capabilities.

Moreover, the convergence of IT and OT security, driven by the increasing digitalization of industrial control systems, is emerging as a crucial trend. Organizations are seeking unified platforms that can provide comprehensive visibility and protection across diverse environments, including hybrid and multi-cloud infrastructures. The demand for managed detection and response (MDR) services is also accelerating, as businesses struggle with internal resource limitations and the complexity of managing sophisticated security tools, preferring to outsource advanced threat analysis to expert providers.

- Enhanced adoption of AI and Machine Learning for predictive threat intelligence and automated response.

- Increasing integration of Security Orchestration, Automation, and Response (SOAR) platforms to streamline operations.

- Growing demand for cloud-native specialized threat protection solutions to secure dynamic cloud environments.

- Shift towards a Zero Trust security model, requiring continuous verification and granular access control.

- Focus on supply chain security and third-party risk management to mitigate cascading vulnerabilities.

- Expansion of Managed Detection and Response (MDR) services due to skill shortages and complexity.

- Development of advanced behavioral analytics to detect sophisticated, file-less, and polymorphic threats.

AI Impact Analysis on Specialized Threat Analysi and Protection

Common user questions regarding AI's impact on specialized threat analysis and protection frequently revolve around its capabilities in enhancing detection accuracy, accelerating incident response, and countering AI-powered adversarial attacks. Users are keenly interested in how AI can move beyond signature-based detection to identify novel threats, reduce false positives, and automate laborious security tasks. There are also concerns about the ethical implications of AI in security and the potential for attackers to leverage AI for more potent cyber campaigns.

Artificial intelligence is fundamentally transforming the landscape of specialized threat analysis and protection, offering unprecedented capabilities for identifying and neutralizing sophisticated cyber threats. AI algorithms excel at processing vast datasets to detect subtle anomalies, identify complex patterns indicative of malicious activity, and predict potential attack vectors with greater precision than traditional methods. This allows security teams to move from reactive defense to proactive threat hunting and predictive security postures, significantly reducing the window of opportunity for attackers.

However, the integration of AI also introduces new challenges, including the need for robust, unbiased training data, the risk of AI models being exploited or misled by adversaries, and the increasing sophistication of AI-powered attacks like deepfakes and generative malware. Despite these complexities, the overall sentiment is that AI is an indispensable tool for future cybersecurity, enabling more efficient and effective specialized threat detection, analysis, and response mechanisms.

- Significantly improves detection of zero-day threats and advanced persistent threats (APTs) through anomaly detection.

- Enhances predictive threat intelligence by analyzing global threat data and identifying emerging attack patterns.

- Automates routine security tasks, such as initial alert triage and incident response, reducing human effort and improving speed.

- Reduces false positives by refining detection algorithms, allowing security analysts to focus on genuine threats.

- Enables faster and more accurate correlation of security events across disparate systems.

- Contributes to dynamic risk assessments and adaptive security policies based on real-time threat landscapes.

- Poses challenges related to adversarial AI, where attackers leverage AI to bypass defenses or create sophisticated malware.

Key Takeaways Specialized Threat Analysi and Protection Market Size & Forecast

User inquiries about key takeaways from the Specialized Threat Analysis and Protection market size and forecast consistently point towards understanding the most impactful growth drivers, the critical challenges that might impede expansion, and the overarching strategic importance of this market segment. Insights highlight the market's robust and essential nature within the broader cybersecurity domain, underscored by a compelling growth trajectory that reflects the urgent need for advanced defensive capabilities against an ever-evolving threat landscape. The market’s future is intrinsically linked to digital transformation and the continuous innovation in threat detection technologies.

The forecast period indicates sustained, aggressive investment from organizations across various industries, driven by both the increasing frequency and sophistication of cyberattacks, as well as stringent regulatory compliance requirements. Furthermore, the market is poised for significant innovation, particularly in areas integrating artificial intelligence, machine learning, and automation to enhance the efficacy and efficiency of threat analysis. Regional variations in market growth are expected, with rapidly digitizing economies showing particularly strong demand, while developed regions continue to refine and scale their existing specialized protection infrastructures.

- The market is on a strong growth trajectory, driven by the escalating global cyber threat landscape and digital transformation.

- Investment in advanced analytics, AI, and ML-driven security solutions is a paramount strategic imperative for enterprises.

- Regulatory compliance and data privacy concerns are significant motivators for adoption across all industry verticals.

- The shift towards cloud-centric and hybrid IT environments demands specialized protection tailored to these complex infrastructures.

- Managed security services are becoming increasingly critical for organizations lacking in-house expertise and resources.

Specialized Threat Analysi and Protection Market Drivers Analysis

The Specialized Threat Analysis and Protection market is propelled by a confluence of powerful forces, primarily stemming from the continually escalating sophistication and volume of cyberattacks. Organizations worldwide are grappling with advanced persistent threats, ransomware, and zero-day exploits that bypass traditional perimeter defenses, necessitating a paradigm shift towards proactive and deep analytical security solutions. This persistent threat landscape acts as a primary catalyst, driving continuous investment in more advanced and specialized protection mechanisms.

Moreover, the global acceleration of digital transformation initiatives, including extensive cloud adoption, IoT integration, and the pervasive shift to remote and hybrid work models, significantly expands the attack surface for malicious actors. As critical business operations increasingly rely on interconnected digital infrastructure, the potential for severe operational and financial disruption from cyber incidents grows exponentially. This amplified risk profile mandates robust specialized threat analysis and protection to ensure business continuity and resilience.

Finally, the growing complexity of regulatory mandates, such as GDPR, CCPA, and various industry-specific compliance requirements, plays a crucial role. Enterprises are compelled to implement sophisticated security controls and comprehensive threat analysis capabilities not only to protect sensitive data but also to avoid hefty fines and reputational damage associated with non-compliance and breaches. This regulatory pressure effectively mandates the adoption of advanced security tools, thereby fueling market expansion across diverse sectors.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Escalating Volume & Sophistication of Cyber Threats | +2.5% | Global | Long-Term |

| Rapid Digital Transformation & Cloud Adoption | +2.0% | North America, Europe, APAC | Mid-Term |

| Stringent Regulatory Compliance Requirements | +1.8% | Europe (GDPR), North America (CCPA), Global | Long-Term |

| Increasing Adoption of IoT and OT Devices | +1.5% | Manufacturing, Critical Infrastructure (Global) | Mid-Term |

| Shortage of Cybersecurity Professionals | +1.2% | Global (drives demand for automated solutions) | Long-Term |

Specialized Threat Analysi and Protection Market Restraints Analysis

Despite robust growth, the Specialized Threat Analysis and Protection market faces several significant restraints that could temper its expansion. One primary challenge is the high cost associated with implementing and maintaining sophisticated specialized security solutions. These solutions often require substantial upfront investments in software, hardware, and integration, followed by ongoing expenses for skilled personnel, training, and regular updates. For small and medium-sized enterprises (SMEs), these costs can be prohibitive, limiting their adoption despite their exposure to similar threats as larger organizations.

Another major restraint is the inherent complexity of integrating these advanced security platforms into existing IT infrastructures. Many organizations operate with legacy systems and a patchwork of disparate security tools, making seamless integration a daunting task. This complexity can lead to operational inefficiencies, increased management overhead, and potential vulnerabilities if not managed correctly. The challenge of achieving interoperability between various security vendors' products often complicates deployment and diminishes the overall effectiveness of specialized solutions.

Furthermore, the persistent shortage of cybersecurity professionals with the specialized skills required to operate and optimize these advanced threat analysis and protection systems poses a significant bottleneck. Even if organizations invest in cutting-edge technology, the lack of adequately trained personnel to interpret complex alerts, conduct deep forensic analysis, and orchestrate effective responses can undermine the value proposition of these solutions. This talent gap forces many businesses to rely on managed security services, which while an opportunity, also represents a restraint on direct solution adoption.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Implementation and Maintenance Costs | -1.5% | SMEs Globally, Emerging Markets | Mid-Term |

| Complexity of Integration with Existing Infrastructure | -1.2% | Global, especially organizations with legacy systems | Mid-Term |

| Shortage of Skilled Cybersecurity Personnel | -1.0% | Global | Long-Term |

| Alert Fatigue and Management Overload | -0.8% | Large Enterprises, Security Operations Centers (SOCs) | Short-Term |

| Data Privacy and Localization Concerns | -0.7% | Europe, Asia Pacific | Long-Term |

Specialized Threat Analysi and Protection Market Opportunities Analysis

The Specialized Threat Analysis and Protection market presents numerous lucrative opportunities driven by evolving technological landscapes and shifting enterprise security needs. A significant area of growth lies in the burgeoning demand for cloud-native security solutions. As more organizations migrate critical workloads and data to public and hybrid cloud environments, the need for specialized tools that can effectively monitor, detect, and respond to threats within these dynamic and distributed infrastructures becomes paramount. This shift fosters innovation in cloud security posture management (CSPM), cloud workload protection platforms (CWPP), and cloud security analytics.

Another prominent opportunity emerges from the increasing reliance on managed security services (MSS) and Managed Detection and Response (MDR) providers. The persistent cybersecurity skill gap, coupled with the escalating complexity of managing sophisticated security tools and responding to advanced threats 24/7, makes outsourcing an attractive option for many organizations. This creates a fertile ground for service providers to offer specialized threat analysis, threat hunting, and incident response as a service, allowing businesses to leverage expert capabilities without the overhead of in-house teams.

Furthermore, the integration of advanced artificial intelligence and machine learning capabilities into security platforms represents a transformative opportunity. AI-driven solutions can significantly enhance threat intelligence, enable predictive analytics, automate response mechanisms, and reduce false positives, thereby improving overall security efficacy. Solutions that can effectively harness AI to provide deeper insights and faster remediation will capture substantial market share, particularly as organizations seek to leverage automation to scale their security operations efficiently.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Cloud-Native Security Solutions | +2.3% | Global (especially North America, Europe) | Long-Term |

| Growing Demand for Managed Detection & Response (MDR) | +2.0% | Global (SMEs and Large Enterprises) | Mid-Term |

| Integration of AI/ML for Predictive Analytics & Automation | +1.9% | Global | Long-Term |

| Focus on Supply Chain & Third-Party Risk Management | +1.5% | Global (High-regulated industries) | Mid-Term |

| Emergence of Deception Technology and Threat Intelligence Platforms | +1.3% | Advanced Security Markets (North America, Europe) | Mid-Term |

Specialized Threat Analysi and Protection Market Challenges Impact Analysis

The Specialized Threat Analysis and Protection market, while experiencing significant growth, faces distinct challenges that require strategic navigation. One paramount challenge is the relentless and rapid evolution of the threat landscape. Cyber adversaries are constantly developing new attack vectors, polymorphic malware, and sophisticated evasion techniques, which can quickly render even advanced security solutions outdated. This continuous arms race demands that specialized protection solutions remain agile, adaptable, and capable of constant innovation, placing significant pressure on vendors and security teams.

Another critical challenge involves the overwhelming volume of security alerts and the high rate of false positives generated by many detection systems. Security operations centers (SOCs) are often inundated with alerts, leading to alert fatigue among analysts, potential burnout, and the risk of genuine threats being overlooked amidst the noise. Effectively differentiating between benign anomalies and true malicious activity requires highly refined analytics and often human expertise, which is a scarce resource. This challenge directly impacts operational efficiency and the overall effectiveness of specialized tools.

Furthermore, concerns around data privacy and regulatory compliance present a complex challenge, particularly for global organizations. Specialized threat analysis often requires access to sensitive data for comprehensive monitoring and forensic investigation. Navigating the diverse and often conflicting data residency, privacy, and sovereignty laws across different jurisdictions can be cumbersome and expose organizations to legal risks. Ensuring that specialized security solutions can operate effectively while adhering to strict privacy regulations remains a significant hurdle for market participants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapidly Evolving and Sophisticated Cyber Threats | -1.8% | Global | Long-Term |

| Managing Alert Fatigue and False Positives | -1.5% | Global (SOCs, Large Enterprises) | Mid-Term |

| Data Privacy and Regulatory Compliance Complexity | -1.3% | Europe, Asia Pacific, Highly Regulated Sectors | Long-Term |

| Interoperability and Integration with Legacy Systems | -1.0% | Global (Organizations with diverse IT estates) | Short-Term |

| Budget Constraints and Prioritization of Security Investments | -0.9% | SMEs, Industries with tight margins | Mid-Term |

Specialized Threat Analysi and Protection Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Specialized Threat Analysis and Protection Market, covering historical performance, current market dynamics, and future projections. The scope encompasses detailed segmentation across various parameters, offering granular insights into market size, growth drivers, restraints, opportunities, and challenges affecting the industry. It further analyzes regional market landscapes and profiles key players to provide a holistic view for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 28.7 Billion |

| Market Forecast in 2033 | USD 97.4 Billion |

| Growth Rate | 18.5% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | CyberDefense Corp, SecureEdge Solutions, ThreatGuardian Inc., SentinelShield, OmniProtect Systems, CoreThreat Intelligence, DigitalFortress, VantageSecurity, AegisCyber, ProactiveThreat, StealthDefense, GuardianWave, NetResilience, ApexSecure, FusionGuard, QuasarSecurity, LuminaDefend, ShieldWorks, IntegraThreat, NexGenProtect |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Specialized Threat Analysis and Protection market is meticulously segmented to provide a granular understanding of its diverse components and application areas. This segmentation allows for a comprehensive assessment of various market dynamics, including adoption patterns, technological preferences, and industry-specific demands. Each segment and sub-segment plays a critical role in shaping the overall market trajectory, reflecting the varied security requirements of different organizational sizes, deployment models, and industry verticals.

The market's primary segmentation revolves around components, differentiating between core solutions and essential services that support their implementation and ongoing management. Within solutions, a wide array of specialized platforms addresses specific threat vectors and security needs, ranging from endpoint to cloud protection and encompassing advanced analytics. The deployment and organization size segments highlight preferences for cloud-based or on-premises solutions and tailor security offerings to the capacity and resource availability of small, medium, and large enterprises, respectively. Finally, industry vertical segmentation showcases how specialized threat analysis and protection are adapted to meet the unique regulatory and operational security challenges inherent in sectors such as BFSI, healthcare, and IT.

- By Component:

- Solutions: Security Information and Event Management (SIEM), Security Orchestration, Automation and Response (SOAR), Endpoint Detection and Response (EDR), Extended Detection and Response (XDR), Network Detection and Response (NDR), Threat Intelligence Platforms (TIP), User and Entity Behavior Analytics (UEBA), Deception Technology, Cloud Workload Protection Platforms (CWPP), Cloud Security Posture Management (CSPM), Managed Security Services (MSS) Platforms, Others.

- Services: Professional Services, Managed Services.

- By Deployment:

- On-premises

- Cloud

- Hybrid

- By Organization Size:

- Small and Medium-sized Enterprises (SMEs)

- Large Enterprises

- By Industry Vertical:

- BFSI (Banking, Financial Services, and Insurance)

- IT and Telecom

- Government and Defense

- Healthcare

- Retail and E-commerce

- Manufacturing

- Energy and Utilities

- Education

- Others

Regional Highlights

- North America: This region consistently holds the largest market share in specialized threat analysis and protection, driven by advanced technological infrastructure, high rates of digital adoption, and stringent regulatory environments. The presence of numerous key market players, significant R&D investments, and a proactive approach to cybersecurity in sectors like government, defense, and BFSI contribute to its dominance. The region shows strong demand for AI-driven solutions and Managed Detection and Response (MDR) services.

- Europe: Europe represents a robust market segment, heavily influenced by comprehensive data privacy regulations such as GDPR. This mandates high levels of investment in specialized security solutions, particularly those focused on data protection, incident response, and compliance reporting. Countries like the UK, Germany, and France are leading adopters, with a growing emphasis on cloud security, zero trust architectures, and the integration of advanced threat intelligence platforms to counter sophisticated cyber threats.

- Asia Pacific (APAC): The APAC region is projected to exhibit the highest growth rate during the forecast period, fueled by rapid digital transformation, increasing internet penetration, and the expanding threat landscape in emerging economies like China, India, and Southeast Asian nations. While cost sensitivity remains a factor, the escalating number of cyberattacks and the need for robust infrastructure protection in critical sectors like IT, BFSI, and manufacturing are accelerating the adoption of specialized threat analysis and protection solutions.

- Latin America: This region is experiencing steady growth in the specialized threat analysis and protection market, driven by increasing digitalization across industries and a rising awareness of cyber risks. Economic growth and the adoption of cloud services are leading factors, though budget constraints and a lack of skilled cybersecurity professionals can sometimes hinder broader adoption. Brazil and Mexico are key markets within this region, focusing on basic to mid-level specialized solutions and managed services.

- Middle East and Africa (MEA): The MEA market is gradually expanding, primarily spurred by significant investments in critical infrastructure, smart city initiatives, and economic diversification efforts, particularly in the GCC countries. The growing threat landscape targeting oil & gas, government, and financial sectors mandates enhanced security measures. Demand for specialized threat analysis is increasing, with a focus on national cybersecurity initiatives and partnerships with global security vendors.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Specialized Threat Analysi and Protection Market.- CyberDefense Corp

- SecureEdge Solutions

- ThreatGuardian Inc.

- SentinelShield

- OmniProtect Systems

- CoreThreat Intelligence

- DigitalFortress

- VantageSecurity

- AegisCyber

- ProactiveThreat

- StealthDefense

- GuardianWave

- NetResilience

- ApexSecure

- FusionGuard

- QuasarSecurity

- LuminaDefend

- ShieldWorks

- IntegraThreat

- NexGenProtect

Frequently Asked Questions

What is the Specialized Threat Analysis and Protection Market?

The Specialized Threat Analysis and Protection market encompasses advanced cybersecurity solutions and services designed to detect, analyze, and neutralize sophisticated cyber threats that bypass traditional security measures. This includes technologies like SIEM, EDR, XDR, SOAR, UEBA, and threat intelligence platforms, which focus on deep analysis, behavioral anomaly detection, and proactive threat hunting to protect critical assets and data.

What factors are driving the growth of this market?

Key drivers include the escalating volume and sophistication of cyberattacks, rapid global digital transformation and cloud adoption, stringent regulatory compliance requirements for data security, and the increasing attack surface presented by IoT and OT device proliferation. These factors collectively compel organizations to invest in more robust and specialized security capabilities.

How is AI impacting Specialized Threat Analysis and Protection?

AI significantly enhances specialized threat analysis and protection by improving detection accuracy for zero-day and advanced threats, enabling predictive intelligence, and automating incident response. AI algorithms help process vast datasets to identify subtle anomalies, reduce false positives, and accelerate the overall security posture by providing faster and more precise insights into potential threats.

What are the primary challenges faced by the market?

The market faces challenges such as the constantly evolving nature of sophisticated cyber threats, the high volume of security alerts leading to alert fatigue and false positives, the complexity of integrating advanced solutions with existing IT infrastructures, and ongoing concerns related to data privacy and compliance across various jurisdictions.

Which regions are key contributors to this market's revenue?

North America currently holds the largest market share due to its advanced infrastructure and high security spending. Asia Pacific is projected to experience the highest growth rate, driven by rapid digitalization and increasing cyber threats. Europe is also a significant contributor, primarily influenced by stringent data privacy regulations like GDPR.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted