Fiber based Packaging Market

Fiber based Packaging Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700205 | Last Updated : July 23, 2025 |

Format : ![]()

![]()

![]()

![]()

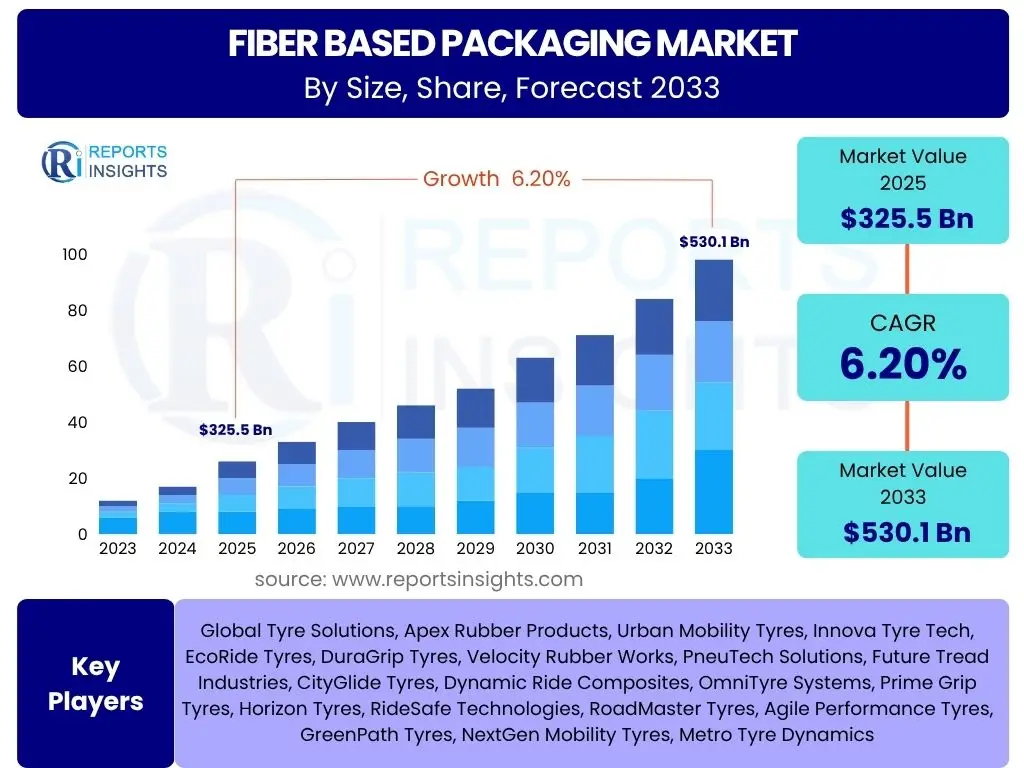

Fiber based Packaging Market is projected to grow at a Compound annual growth rate (CAGR) of 6.2% between 2025 and 2033, reaching USD 325.5 billion in 2025 and is projected to grow to USD 530.1 billion by 2033 the end of the forecast period.

Key Fiber based Packaging Market Trends & Insights

The fiber based packaging market is currently shaped by a confluence of powerful trends, primarily driven by an escalating global focus on sustainability and environmental stewardship. Consumers, businesses, and regulatory bodies are increasingly demanding alternatives to plastic, propelling innovation and adoption of paper and board solutions. This shift is not merely about material substitution but encompasses a holistic approach to packaging lifecycles, emphasizing recyclability, compostability, and the use of responsibly sourced materials. Technological advancements are playing a pivotal role, enabling the creation of fiber based packaging with enhanced barrier properties, improved strength, and novel designs, broadening its applicability across diverse sectors previously dominated by non-renewable materials. Furthermore, the burgeoning e-commerce sector significantly fuels demand for lightweight, protective, and brandable fiber based packaging, necessitating continuous evolution in packaging solutions to meet logistical and aesthetic requirements.

- Growing consumer and corporate demand for sustainable and eco-friendly packaging solutions.

- Increasing regulatory pressures and bans on single-use plastics globally.

- Technological innovations enhancing barrier properties, durability, and printability of fiber based materials.

- Rapid expansion of the e-commerce sector driving demand for protective and lightweight packaging.

- Shift towards circular economy principles, promoting recyclability and use of recycled content.

- Development of molded fiber solutions for intricate and protective applications.

- Integration of smart packaging features for enhanced consumer engagement and supply chain efficiency.

AI Impact Analysis on Fiber based Packaging

Artificial Intelligence (AI) is poised to revolutionize the fiber based packaging market by optimizing various stages of the value chain, from raw material sourcing to end-of-life management. In manufacturing, AI-powered systems can enhance production efficiency through predictive maintenance, real-time quality control, and intelligent process automation, leading to reduced waste and improved material utilization. Design and innovation stand to benefit immensely, with AI enabling rapid prototyping of complex structures, optimizing material usage for strength and lightweighting, and personalizing packaging designs to meet specific brand and consumer demands. Furthermore, AI can contribute to a more sustainable supply chain by optimizing logistics, predicting demand fluctuations, and facilitating advanced sorting and recycling processes, ultimately bolstering the circularity of fiber based materials and reducing environmental impact across the industry.

- Optimization of production processes and machinery through predictive analytics and automation.

- Enhanced quality control and defect detection using computer vision and machine learning.

- AI-driven design for optimal material usage, structural integrity, and customizability.

- Supply chain efficiency improvements, including demand forecasting, inventory management, and logistics optimization.

- Advancements in waste sorting and recycling technologies through AI-powered recognition systems.

- Personalized packaging solutions and marketing insights derived from consumer data analysis.

Key Takeaways Fiber based Packaging Market Size & Forecast

- The global fiber based packaging market is set for robust expansion, reflecting a fundamental shift in consumer and industry preferences towards sustainable alternatives.

- Projected to grow at a Compound Annual Growth Rate (CAGR) of 6.2% from 2025 to 2033, indicating sustained market momentum.

- The market size is estimated at USD 325.5 billion in 2025, underscoring its significant current valuation.

- Forecasts suggest a substantial increase to USD 530.1 billion by 2033, demonstrating considerable growth potential and investment opportunities.

- This growth is largely attributed to increasing environmental awareness, stringent regulatory frameworks, and rapid innovation in fiber based materials.

- Key segments such as food and beverage, e-commerce, and personal care are expected to drive the highest demand.

Fiber based Packaging Market Drivers Analysis

The fiber based packaging market is significantly propelled by several fundamental drivers that align with global sustainability imperatives and evolving consumer behaviors. A primary catalyst is the escalating environmental consciousness among consumers and industries, leading to a strong preference for eco-friendly packaging solutions over conventional plastic. This is further amplified by stringent regulatory frameworks and governmental initiatives worldwide, which are actively promoting the reduction of plastic waste and encouraging the adoption of recyclable and biodegradable materials. The rapid expansion of e-commerce also plays a crucial role, as it necessitates lightweight, protective, and customizable packaging solutions that fiber based materials readily provide. Additionally, continuous innovations in material science and manufacturing processes are enhancing the performance characteristics of fiber based packaging, making it viable for a broader range of applications and strengthening its competitive edge against other materials.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Sustainable Packaging | +2.5% | Global, particularly Europe and North America | Long-term, Continuous |

| Stringent Environmental Regulations and Plastic Bans | +1.8% | Europe, Asia Pacific (China, India), North America | Medium to Long-term |

| Expansion of the E-commerce Sector | +1.5% | Global, high growth in Asia Pacific and North America | Short to Medium-term, Ongoing |

| Innovation in Barrier Coatings and Material Science | +1.2% | Global, driven by R&D in developed economies | Medium to Long-term |

| Increasing Consumer Awareness and Preference | +1.0% | Developed economies, rapidly emerging in developing regions | Long-term, Sustained |

Fiber based Packaging Market Restraints Analysis

Despite robust growth, the fiber based packaging market faces certain restraints that could temper its expansion. One significant challenge is the volatility of raw material prices, particularly for pulp and paper, which can fluctuate due to supply chain disruptions, energy costs, and environmental factors impacting forest resources. Another restraint lies in the performance limitations of fiber based materials compared to plastics, especially concerning moisture, grease, and oxygen barriers, which can restrict their application in certain sensitive products like liquids or perishable foods without specialized coatings. The complexity and cost associated with developing advanced barrier solutions and establishing widespread recycling infrastructure for specific fiber based packaging formats (e.g., those with multi-material laminates) also present considerable hurdles. Furthermore, competition from alternative sustainable materials or evolving packaging technologies could pose a threat to market share, requiring continuous innovation to maintain competitiveness.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices | -0.8% | Global, impacting manufacturing hubs | Short to Medium-term, Cyclical |

| Performance Limitations (Moisture, Grease Barriers) | -0.7% | Global, prominent in food & beverage sectors | Medium-term, Until Innovation Catches Up |

| High Initial Investment for New Technologies | -0.5% | Developing regions, smaller manufacturers globally | Medium-term |

| Challenges in Recycling Complex Fiber Formats | -0.4% | Global, particularly for multi-material packaging | Long-term, Infrastructure Dependent |

Fiber based Packaging Market Opportunities Analysis

Significant opportunities abound in the fiber based packaging market, driven by a global push towards circularity and innovative material applications. The development of advanced barrier coatings and biodegradable laminations presents a vast opportunity to penetrate markets traditionally dominated by plastics, particularly in the food and beverage sector for liquid and perishable goods. Expanding the application of molded fiber technology beyond traditional uses into high-value consumer electronics and medical devices offers substantial growth avenues. Furthermore, the increasing adoption of smart packaging features, such as QR codes, NFC tags, and sensors embedded within fiber based structures, provides avenues for enhanced consumer engagement, brand protection, and supply chain traceability. Strategic partnerships and collaborations between pulp and paper manufacturers, technology providers, and brand owners can accelerate innovation and market penetration. Lastly, untapped potential exists in emerging economies where increasing disposable incomes and growing environmental awareness are fueling demand for sustainable packaging solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Barrier Coatings | +1.5% | Global, especially for food & beverage applications | Medium to Long-term |

| Expansion into New End-use Applications (e.g., molded fiber for electronics) | +1.3% | Global, strong potential in high-value goods sectors | Medium to Long-term |

| Integration of Smart Packaging Technologies | +1.0% | Developed economies, early adopters globally | Long-term, Emerging |

| Growth in Emerging Economies with Sustainability Focus | +0.9% | Asia Pacific, Latin America, Middle East & Africa | Long-term |

Fiber based Packaging Market Challenges Impact Analysis

The fiber based packaging market, while promising, navigates several significant challenges that can impede its optimal growth and adoption. One major challenge is ensuring the consistent quality and performance of fiber materials, particularly when incorporating recycled content, which can sometimes compromise strength or barrier properties. The complexity of designing and implementing truly circular systems, including widespread collection, sorting, and recycling infrastructure for diverse fiber based packaging formats (especially those with composite elements), remains a formidable hurdle. Competition from established plastic packaging, which often benefits from lower production costs and superior barrier properties for certain applications, continues to pose a challenge despite increasing environmental pressures. Furthermore, scaling up innovative fiber based solutions to meet industrial demand at competitive prices requires substantial investment in research and development and manufacturing capabilities, presenting financial and logistical obstacles for market participants, especially smaller entities.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining Performance with Increased Recycled Content | -0.6% | Global, critical for circular economy goals | Medium to Long-term |

| Development of Robust Recycling Infrastructure | -0.5% | Global, policy and investment dependent | Long-term |

| Cost Competitiveness Against Traditional Plastics | -0.4% | Global, particularly in price-sensitive markets | Short to Medium-term |

| Technological Scalability and Investment Requirements | -0.3% | Global, impacting SMEs and innovators | Medium-term |

Fiber based Packaging Market - Updated Report Scope

This comprehensive market research report delves into the intricate dynamics of the global fiber based packaging market, offering a robust analysis of its current landscape and future trajectory. It provides an in-depth understanding of market size, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. The report leverages extensive primary and secondary research to deliver actionable insights, enabling stakeholders to make informed strategic decisions. Furthermore, it incorporates the latest industry trends, the impact of technological advancements like AI, and a detailed profiling of key market players, presenting a holistic view of the market's competitive environment and potential growth avenues.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 325.5 Billion |

| Market Forecast in 2033 | USD 530.1 Billion |

| Growth Rate | 6.2% from 2025 to 2033 |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Smurfit Kappa Group, International Paper Company, WestRock Company, Packaging Corporation of America, DS Smith Plc, Mondi Group, Sappi Ltd., Stora Enso Oyj, BillerudKorsnäs AB, Nine Dragons Paper (Holdings) Limited, Oji Holdings Corporation, Georgia-Pacific LLC, Sylvamo Corporation, Sealed Air Corporation, Huhtamäki Oyj, Amcor Plc, Sonoco Products Company, Graphic Packaging International LLC, Evergreen Packaging LLC, Walki Group. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The fiber based packaging market is extensively segmented to provide a granular view of its diverse applications and material types, enabling a comprehensive understanding of market dynamics. Each segment represents a distinct facet of the industry, driven by specific consumer needs, industry standards, and technological advancements. Understanding these segments is crucial for identifying key growth areas, assessing competitive landscapes, and formulating targeted market strategies, allowing stakeholders to capitalize on emerging trends and mitigate potential risks across the value chain. This detailed segmentation reflects the versatility and expanding scope of fiber based packaging solutions in various sectors worldwide.

- By Material Type: This segment categorizes fiber based packaging based on the primary raw material used and its processing.

- Corrugated Board: Characterized by its fluted layer sandwiched between two flat linerboards, offering excellent strength-to-weight ratio.

- Recycled Corrugated: Made predominantly from post-consumer or post-industrial waste, emphasizing circularity and resource efficiency.

- Virgin Corrugated: Produced from freshly cut wood fibers, known for superior strength, purity, and aesthetic appeal, often used for demanding applications.

- Paperboard: A thicker, stiffer paper material, widely used for folding cartons and rigid boxes due to its printability and formability.

- Folding Boxboard (FBB): Composed of multiple layers of mechanical and chemical pulp, providing high stiffness, excellent bending properties, and smooth printing surface.

- Solid Bleached Sulfate (SBS): Made from bleached chemical pulp, known for its high brightness, purity, and strength, ideal for food and pharmaceutical packaging.

- Unbleached Kraft Board (UKB): Produced from unbleached chemical pulp, offering high tear and burst strength, often used for heavy-duty packaging and beverage carriers.

- White Lined Chipboard (WLC): Made primarily from recycled fibers with a white coating on one side for printability, a cost-effective option for various consumer goods.

- Flexible Paper: Lightweight and pliable paper materials used for wraps, bags, and pouches, emphasizing convenience and barrier properties.

- Kraft Paper: Strong and durable, made from chemical pulp, widely used for bags, wraps, and protective packaging.

- Greaseproof Paper: Treated to resist oil and grease, suitable for food wrapping and baking applications.

- Glassine Paper: Highly dense and smooth, offering limited barrier properties, often used for inner wraps or window patches.

- Parchment Paper: Treated for heat and moisture resistance, commonly used in baking and food preparation.

- Molded Fiber: Formed by pressing wet pulp into a desired shape, offering protective cushioning and unique designs, often seen as a sustainable alternative to plastics.

- Transfer Molded: A simpler process for less demanding shapes, often used for egg cartons and produce trays.

- Thermoformed: A more advanced process yielding smoother surfaces and more intricate, precise shapes, suitable for high-value protective packaging.

- Corrugated Board: Characterized by its fluted layer sandwiched between two flat linerboards, offering excellent strength-to-weight ratio.

- By Packaging Type: This segment delineates the market based on the structural form and primary function of the packaging.

- Boxes & Cartons: Encompasses a wide range of enclosed packaging solutions.

- Folding Cartons: Pre-creased and cut sheets that fold into boxes, common for consumer goods.

- Liquid Packaging Cartons: Designed with specialized barriers for liquids like milk and juice.

- Aseptic Cartons: Sterile packaging for extended shelf life without refrigeration, typically for beverages.

- Corrugated Boxes: Durable boxes for shipping and storage, made from corrugated board.

- Bags & Sacks: Flexible packaging solutions primarily for carrying or containing goods.

- Paper Bags: Retail and grocery bags, often recyclable and biodegradable.

- Multiwall Sacks: Heavy-duty bags with multiple layers, used for bulk materials like cement or grains.

- Trays & Clamshells: Open or hinged containers providing protective support and visibility for products.

- Cups & Plates: Single-use or reusable tableware, gaining traction as plastic alternatives.

- Wraps & Pouches: Flexible packaging for various products, often with barrier properties.

- Others: Includes specialized forms like fiber drums for industrial goods and fiber cans for food and beverage items.

- Boxes & Cartons: Encompasses a wide range of enclosed packaging solutions.

- By End-Use Industry: This segment analyzes the market based on the primary sector where the packaging is utilized, reflecting specific industry requirements and consumption patterns.

- Food & Beverages: The largest end-use segment, driven by consumer goods packaging needs.

- Dairy: Milk, yogurt, and cheese packaging.

- Baked Goods: Bread, pastries, and cookie packaging.

- Confectionery: Candy, chocolate, and sweets packaging.

- Fresh Produce: Fruits and vegetables, emphasizing breathability and protection.

- Frozen Food: Packaging designed to withstand freezing temperatures.

- Ready Meals: Packaging for convenience foods.

- Beverages: Cartons for juices, milk, and other drinks.

- Healthcare & Pharmaceuticals: Requires high purity, protection, and often tamper-evident features for medicines and medical devices.

- Personal Care & Cosmetics: Driven by branding, aesthetics, and product protection for beauty and hygiene products.

- Homecare: Packaging for household cleaning products and detergents.

- E-commerce: Specialized protective and lightweight packaging for online retail shipments.

- Industrial: Bulk packaging for chemicals, building materials, and automotive parts.

- Others: Includes segments like tobacco, textiles, and other general consumer goods.

- Food & Beverages: The largest end-use segment, driven by consumer goods packaging needs.

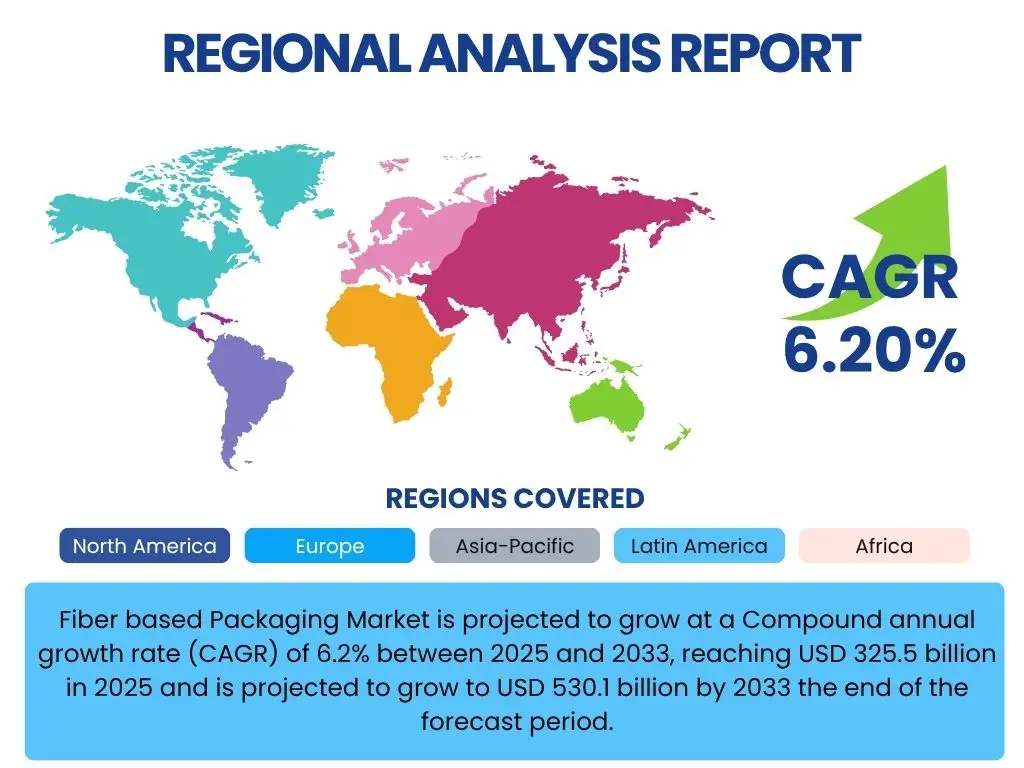

Regional Highlights

The global fiber based packaging market exhibits diverse growth patterns and regional dominance, influenced by varying regulatory landscapes, consumer awareness, and economic development. Key regions play pivotal roles in shaping the market's trajectory, driven by specific factors that make them critical to the industry's overall performance. Understanding these regional dynamics is essential for market participants seeking to optimize their supply chains, expand their market reach, and align with local sustainability agendas, thus enabling targeted strategies for maximum impact.

- North America: This region is a significant market for fiber based packaging, primarily driven by strong consumer demand for sustainable products and increasing corporate sustainability commitments. Regulations and initiatives to reduce plastic waste, especially in states like California and New York, are accelerating the shift. The thriving e-commerce sector further boosts demand for corrugated and paperboard solutions for shipping and protective packaging. Innovation in molded fiber and barrier coatings is also prominent, with a focus on advanced food packaging applications.

- Europe: Leading the global charge in sustainability, Europe is a cornerstone of the fiber based packaging market. Stringent regulations such as the European Green Deal and various national plastic taxes and bans are compelling industries to adopt fiber alternatives. High consumer environmental awareness and robust recycling infrastructures foster a strong circular economy model. Countries like Germany, the UK, and France are at the forefront of adopting innovative fiber based solutions for food and beverage, personal care, and industrial applications.

- Asia Pacific (APAC): This region is projected to be the fastest-growing market, propelled by rapid industrialization, urbanization, and a burgeoning middle class leading to increased consumption. While sustainability awareness is growing, the sheer volume of manufacturing and rising disposable incomes are the primary drivers. Countries like China and India are implementing plastic reduction policies, creating immense opportunities for fiber based packaging, particularly in the food and beverage, e-commerce, and personal care sectors. Investment in new pulp and paper mills and advanced packaging technologies is also on the rise.

- Latin America: The market in Latin America is witnessing steady growth, influenced by increasing environmental concerns and growing regulatory pressure in countries like Brazil and Mexico. The expansion of organized retail and e-commerce, coupled with a growing consumer preference for eco-friendly options, supports the adoption of fiber based packaging. While infrastructure for recycling is still developing in some areas, the potential for growth remains significant as regional economies mature and environmental policies become more widespread.

- Middle East and Africa (MEA): This region is an emerging market for fiber based packaging, driven by a rising awareness of environmental issues, increasing population, and diversification of economies away from oil dependency. Government initiatives to promote sustainable practices and attract foreign investment are creating new opportunities. While adoption rates vary across countries, there is a clear trend towards more sustainable packaging solutions, especially in the food packaging and retail sectors, as the region aligns with global sustainability goals.

Top Key Players:

The market research report covers the analysis of key stake holders of the Fiber based Packaging Market. Some of the leading players profiled in the report include -- Smurfit Kappa Group

- International Paper Company

- WestRock Company

- Packaging Corporation of America

- DS Smith Plc

- Mondi Group

- Sappi Ltd.

- Stora Enso Oyj

- BillerudKorsnäs AB

- Nine Dragons Paper (Holdings) Limited

- Oji Holdings Corporation

- Georgia-Pacific LLC

- Sylvamo Corporation

- Sealed Air Corporation

- Huhtamäki Oyj

- Amcor Plc

- Sonoco Products Company

- Graphic Packaging International LLC

- Evergreen Packaging LLC

- Walki Group

Frequently Asked Questions:

What is fiber based packaging?

Fiber based packaging refers to packaging materials primarily made from cellulose fibers derived from wood pulp, recycled paper, or other plant-based sources. This includes a wide range of products such as corrugated boxes, paperboard cartons, molded fiber trays, and paper bags, known for their recyclability, biodegradability, and renewable nature.

Why is fiber based packaging gaining popularity?

Fiber based packaging is gaining popularity due to increasing global environmental consciousness, stringent regulations targeting plastic pollution, and growing consumer demand for sustainable alternatives. Its renewable raw material base, recyclability, and biodegradability offer significant environmental advantages over traditional fossil-fuel-derived plastics.

What are the key end-use industries for fiber based packaging?

The key end-use industries for fiber based packaging include Food & Beverages (e.g., dairy, fresh produce, ready meals, beverages), E-commerce for shipping and protective packaging, Healthcare & Pharmaceuticals, Personal Care & Cosmetics, and Homecare, among others. Its versatility allows for adoption across a broad spectrum of consumer and industrial applications.

What innovations are driving the fiber based packaging market?

Innovations driving the fiber based packaging market include the development of advanced barrier coatings to enhance moisture and grease resistance, lightweighting technologies for reduced material use, advancements in molded fiber for complex shapes, and the integration of smart packaging features like QR codes for enhanced traceability and consumer engagement.

What are the environmental benefits of using fiber based packaging?

The primary environmental benefits of fiber based packaging include its renewability, as it originates from sustainably managed forests, and its high recyclability, contributing to a circular economy. Additionally, many fiber based packaging types are biodegradable or compostable, reducing landfill waste and minimizing environmental impact at the end of their life cycle.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted