Solder Paste Market

Solder Paste Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707352 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

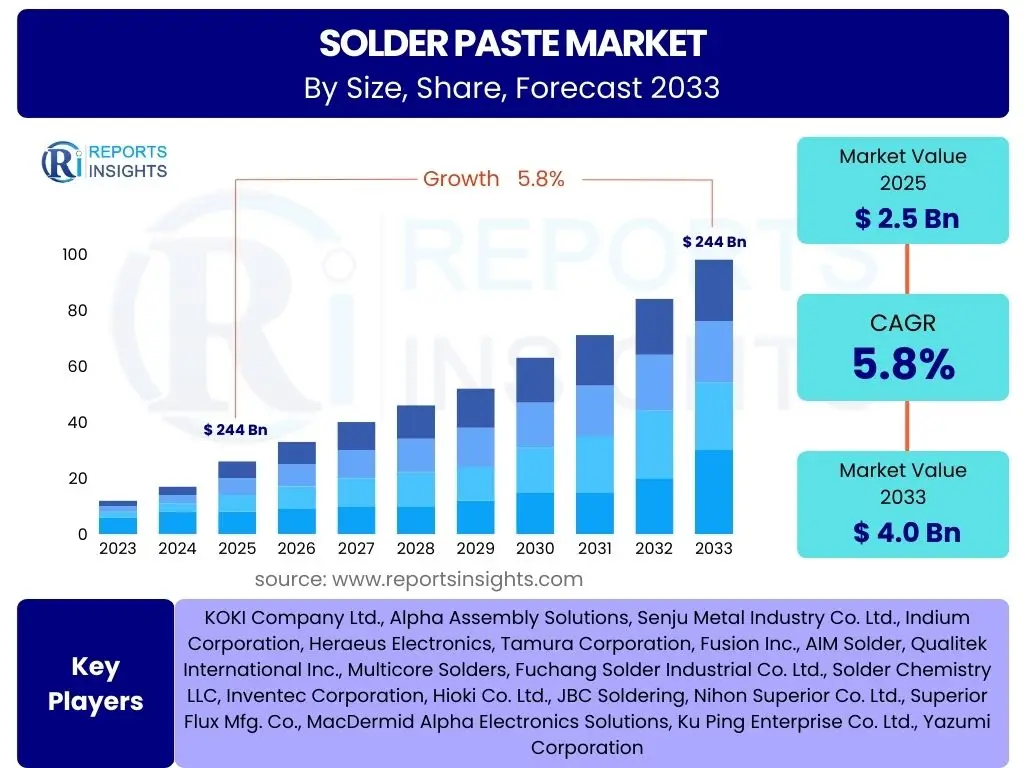

Solder Paste Market Size

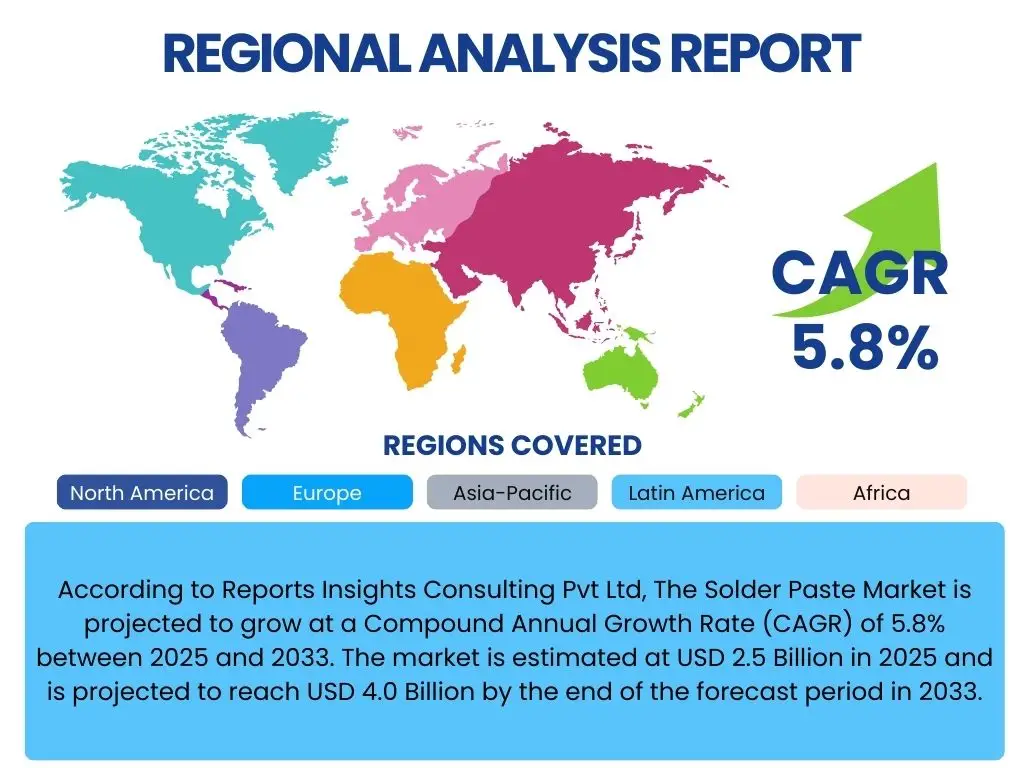

According to Reports Insights Consulting Pvt Ltd, The Solder Paste Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 2.5 Billion in 2025 and is projected to reach USD 4.0 Billion by the end of the forecast period in 2033.

Key Solder Paste Market Trends & Insights

User inquiries frequently focus on the evolving landscape of electronics manufacturing and its direct implications for solder paste formulations and applications. A prominent theme revolves around the global shift towards miniaturization, which demands finer pitch solutions and enhanced reliability. Another significant area of interest is the increasing adoption of lead-free solder pastes due to stringent environmental regulations, particularly in regions like Europe and North America, alongside growing awareness of health impacts. Furthermore, the rapid advancements in automotive electronics and 5G infrastructure are driving demand for high-performance and high-reliability solder paste materials capable of operating under extreme conditions.

The market is also witnessing a surge in demand for advanced packaging technologies, such as system-in-package (SiP) and chip-on-board (COB), which necessitate specialized solder paste properties for precise deposition and robust interconnections. Innovations in solder paste formulations, including low-temperature solder pastes for heat-sensitive components and halogen-free options for environmental compliance, are consistently highlighted in market discussions. These trends collectively underscore a market moving towards greater technological sophistication, environmental responsibility, and application-specific customization to meet the diverse needs of modern electronic devices.

- Miniaturization of electronic components driving demand for fine-pitch and ultra-fine pitch solder paste.

- Rising adoption of lead-free solder paste driven by environmental regulations and health concerns.

- Increasing integration of electronics in automotive systems, including EVs and autonomous vehicles, requiring high-reliability solder paste.

- Expansion of 5G infrastructure and IoT devices boosting demand for advanced solder paste solutions.

- Growth in advanced packaging technologies such as SiP, PoP, and BGA necessitating specialized solder paste formulations.

- Development and commercialization of low-temperature solder pastes for temperature-sensitive applications.

- Emphasis on halogen-free and eco-friendly solder paste formulations for sustainable manufacturing.

- Automation and precision in solder paste deposition processes in surface mount technology (SMT) lines.

AI Impact Analysis on Solder Paste

User queries regarding artificial intelligence (AI) in the solder paste domain often center on its potential to revolutionize manufacturing processes, enhance product quality, and optimize material usage. Key themes include the application of AI in predictive quality control, where algorithms can analyze real-time data from solder paste printing and reflow processes to identify potential defects before they occur. There is also significant interest in how AI can facilitate process optimization, enabling manufacturers to fine-tune deposition parameters and reflow profiles for improved yield and efficiency, reducing material waste and energy consumption.

Expectations are high for AI's role in advancing material science, particularly in the development of new solder paste formulations with enhanced properties. AI and machine learning could accelerate the discovery and testing of novel alloys and flux chemistries, leading to pastes with superior reliability, thermal performance, or environmental profiles. Furthermore, users anticipate AI-driven automation in dispensing and inspection systems, leading to higher precision, consistency, and reduced human error in electronics assembly. The overarching concern is how AI integration can lead to more robust, reliable, and cost-effective solder paste applications across various industries.

- AI-powered predictive analytics for defect detection and prevention in solder paste printing and reflow processes.

- Optimization of solder paste deposition parameters and reflow profiles using machine learning algorithms.

- Enhanced quality control and inspection through AI-driven vision systems for solder joint analysis.

- Acceleration of new solder paste material development and formulation testing via AI-driven material science.

- Automation and robotics integrated with AI for precise and consistent solder paste application.

- Supply chain optimization for solder paste materials using AI for demand forecasting and inventory management.

Key Takeaways Solder Paste Market Size & Forecast

Common user questions regarding the solder paste market size and forecast frequently highlight the underlying factors driving its expansion and the technological shifts shaping its future. A primary insight is the sustained growth propelled by the burgeoning global electronics industry, encompassing consumer electronics, automotive, telecommunications, and industrial applications. The transition towards compact and high-performance electronic devices inherently drives the need for advanced solder paste solutions, contributing significantly to market valuation. Furthermore, regulatory mandates, particularly concerning lead-free materials, are not only influencing formulation shifts but also creating new market segments and driving innovation.

Another crucial takeaway revolves around the regional disparities in market growth, with Asia Pacific emerging as a dominant force due to its robust manufacturing base and rapidly expanding electronics production. The forecast period anticipates continued innovation in material science and process technologies, aiming for enhanced reliability, reduced environmental impact, and suitability for next-generation electronic components. Stakeholders are keen to understand the balance between technological advancements and cost-effectiveness, as well as the resilience of the supply chain in supporting this projected growth. The market's future trajectory is strongly linked to advancements in miniaturization, high-speed data transmission, and the broader digitalization trend across industries.

- The solder paste market is set for consistent growth, driven by expanding electronics manufacturing and diverse application areas.

- Miniaturization and increasing complexity of electronic devices are primary growth catalysts for advanced solder paste solutions.

- Regulatory shifts towards lead-free and environmentally friendly materials are fundamentally reshaping product development and market dynamics.

- Asia Pacific is projected to remain the largest and fastest-growing regional market due to significant electronics production capacities.

- Innovation in solder paste formulations, including low-temperature and high-reliability options, will be critical for future market expansion.

Solder Paste Market Drivers Analysis

The global solder paste market is significantly propelled by the continuous expansion of the consumer electronics sector. Devices such as smartphones, laptops, wearables, and smart home appliances are undergoing relentless innovation, becoming more compact, powerful, and interconnected. This miniaturization and enhanced functionality necessitate advanced solder paste formulations capable of precise deposition, fine-pitch applications, and reliable connections for high-density interconnections, thereby fueling demand. The high volume production of these devices globally ensures a steady and increasing consumption of solder paste materials.

Another powerful driver is the burgeoning automotive electronics industry. The proliferation of electric vehicles (EVs), autonomous driving systems, advanced driver-assistance systems (ADAS), and in-car infotainment systems has led to a dramatic increase in electronic content per vehicle. These automotive applications demand extremely robust and reliable solder joints that can withstand harsh environmental conditions, including wide temperature fluctuations, vibrations, and humidity, over extended lifespans. This stringent requirement for high-reliability solder paste drives significant research and development, as well as market demand for specialized automotive-grade products.

Furthermore, the rapid global rollout of 5G infrastructure and the proliferation of Internet of Things (IoT) devices are creating substantial demand for high-performance solder paste. 5G technology requires high-frequency components and dense circuit boards, while IoT devices are often miniaturized and need robust, long-lasting connections in various environments. Both sectors push the boundaries for solder paste performance, requiring excellent electrical conductivity, thermal management, and long-term reliability. The accelerating pace of digitalization across industries, including industrial automation and healthcare, further underpins the consistent growth in demand for high-quality solder paste materials.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Consumer Electronics | +1.5% | Global, particularly Asia Pacific (China, South Korea) | Short to Mid-term (2025-2030) |

| Rising Demand for Automotive Electronics | +1.2% | North America, Europe, Asia Pacific (Japan, Germany, USA) | Mid to Long-term (2027-2033) |

| Expansion of 5G & IoT Infrastructure | +1.0% | Global, particularly North America, Asia Pacific (China, India) | Mid-term (2026-2031) |

| Advancements in Advanced Packaging Technologies | +0.8% | Global, especially North America, Asia Pacific (Taiwan, South Korea) | Mid to Long-term (2027-2033) |

| Increasing Adoption of Industrial Automation | +0.5% | Europe, North America, Asia Pacific (Germany, Japan, China) | Mid-term (2026-2032) |

Solder Paste Market Restraints Analysis

The solder paste market faces significant headwinds from the volatility of raw material prices, particularly for metals like tin, silver, and copper. These primary components constitute a substantial portion of the production cost, and their prices are subject to global supply-demand dynamics, geopolitical events, and speculative trading. Fluctuations can directly impact manufacturing costs, leading to unpredictable pricing for solder paste products. This uncertainty can erode profit margins for manufacturers and make long-term planning challenging, potentially hindering investment in research and development for new formulations.

Another notable restraint is the increasingly stringent environmental regulations, especially concerning hazardous substances like lead and halogen. While the shift to lead-free and halogen-free solder pastes presents opportunities for innovation, it also imposes significant research and development costs on manufacturers to reformulate products and ensure compliance. Adhering to directives such as RoHS (Restriction of Hazardous Substances) and REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) requires substantial investment in testing, certification, and process adjustments. These regulatory pressures can increase operational complexities and production costs, particularly for smaller manufacturers lacking extensive R&D resources.

Furthermore, intense competition within the solder paste market, coupled with the capital-intensive nature of advanced manufacturing processes, presents a significant challenge. The market is characterized by the presence of a few dominant players alongside numerous smaller regional manufacturers. This competitive landscape often leads to price wars, reducing profitability for market participants. The high capital expenditure required for advanced machinery, quality control systems, and ongoing R&D to meet evolving technological demands acts as a barrier to entry for new players and can strain the financial resources of existing ones, particularly during economic downturns.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices | -0.8% | Global | Short to Mid-term (2025-2030) |

| Stringent Environmental Regulations (Lead-free, Halogen-free) | -0.7% | Europe, North America, parts of Asia Pacific | Mid to Long-term (2026-2033) |

| High Research & Development Costs | -0.5% | Global | Long-term (2028-2033) |

| Intense Market Competition | -0.4% | Global | Ongoing |

| Technological Obsolescence | -0.3% | Global | Mid-term (2026-2031) |

Solder Paste Market Opportunities Analysis

The expansion of advanced packaging technologies presents a significant growth opportunity for the solder paste market. As electronic devices become more compact and functionally integrated, there is an increasing reliance on sophisticated packaging solutions like System-in-Package (SiP), Package-on-Package (PoP), and chip-scale packages (CSPs). These technologies demand solder pastes with superior properties, including finer particle sizes, enhanced printability, and robust performance in extreme environments. Manufacturers capable of developing and supplying specialized solder pastes for these high-precision applications stand to gain a competitive advantage and capture a larger market share.

Emerging economies, particularly in Asia Pacific and Latin America, offer substantial untapped potential for solder paste manufacturers. Rapid industrialization, increasing disposable incomes, and growing adoption of electronic devices in these regions are driving the establishment and expansion of electronics manufacturing facilities. This demographic and economic shift creates a burgeoning demand for solder paste, as local production scales up to meet both domestic consumption and export needs. Companies that establish strong distribution networks and localized production capabilities in these regions can capitalize on the burgeoning market opportunities.

Furthermore, the ongoing trend towards flexible and stretchable electronics opens up new avenues for innovation in solder paste formulations. These novel electronic applications, found in wearables, medical implants, and smart textiles, require solder materials that can withstand mechanical stress, bending, and stretching without compromising electrical integrity. Developing solder pastes with superior elasticity, adhesion, and reliability for these unique substrates represents a niche but highly promising growth area. Manufacturers investing in research and development for such specialized applications can differentiate their offerings and cater to a high-value segment of the market.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Advanced Packaging Technologies | +1.3% | Global, particularly Asia Pacific (Taiwan, South Korea, China) | Mid to Long-term (2026-2033) |

| Growth in Emerging Economies | +1.0% | Asia Pacific (India, Vietnam), Latin America (Mexico, Brazil) | Long-term (2028-2033) |

| Development of Low-Temperature Solder Pastes | +0.9% | Global | Mid-term (2026-2031) |

| Increasing Demand for Flexible Electronics | +0.7% | North America, Europe, Asia Pacific (Japan, South Korea) | Long-term (2029-2033) |

| Focus on Eco-Friendly & Halogen-Free Solutions | +0.6% | Europe, North America, Global | Short to Mid-term (2025-2030) |

Solder Paste Market Challenges Impact Analysis

The solder paste market grapples with the pervasive challenge of supply chain disruptions, a vulnerability significantly exposed by recent global events. Disruptions can arise from various factors, including geopolitical tensions, natural disasters, trade disputes, and public health crises. These events can severely impact the availability of critical raw materials such as tin, silver, copper, and various chemicals essential for flux formulation, leading to material shortages and increased procurement costs. Furthermore, logistics and transportation bottlenecks can delay delivery of both raw materials and finished products, disrupting manufacturing schedules and potentially resulting in significant financial losses for both producers and end-users.

Another substantial challenge is the constant pressure to innovate and adapt to rapid technological advancements in the electronics industry. The relentless pursuit of miniaturization, higher performance, and enhanced reliability in electronic devices necessitates continuous evolution in solder paste formulations. Manufacturers must invest heavily in research and development to create new pastes that can meet stringent requirements for fine-pitch printing, low-temperature processing, lead-free compatibility, and superior thermal management. Failure to keep pace with these technological shifts can lead to product obsolescence and a loss of market competitiveness, making innovation an ongoing and resource-intensive imperative.

Moreover, the market faces significant challenges related to the need for highly skilled labor and the complexities of quality control. The precise application and performance of solder paste are critical to the functionality and reliability of electronic assemblies. This requires operators with specialized knowledge of surface mount technology (SMT) processes, equipment calibration, and material handling. A shortage of such skilled professionals can hinder manufacturing efficiency and product quality. Concurrently, maintaining stringent quality control standards for solder paste consistency, rheology, and reliability across different batches and production sites is a complex task, with any deviation potentially leading to significant manufacturing defects and product recalls, impacting both reputation and profitability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Disruptions | -0.9% | Global | Short to Mid-term (2025-2028) |

| Rapid Technological Advancements & Obsolescence | -0.7% | Global | Ongoing |

| Need for Highly Skilled Labor | -0.6% | Global, particularly developed economies | Long-term (2027-2033) |

| Adherence to Evolving Quality Standards | -0.5% | Global | Ongoing |

| Disposal and Recycling of Electronic Waste | -0.4% | Europe, North America, Asia Pacific | Long-term (2029-2033) |

Solder Paste Market - Updated Report Scope

This report provides a comprehensive analysis of the global solder paste market, offering in-depth insights into its size, growth trajectory, key trends, and influencing factors from 2019 to 2033. It meticulously examines market drivers, restraints, opportunities, and challenges shaping the industry landscape. The scope encompasses detailed segmentation by product type, alloy composition, application, and end-use industry, providing a granular view of market dynamics across various categories. Furthermore, the report features extensive regional analysis, highlighting prominent growth opportunities and market specifics across major geographical areas, along with a competitive landscape assessment of leading market players and their strategic initiatives.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.5 Billion |

| Market Forecast in 2033 | USD 4.0 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | KOKI Company Ltd., Alpha Assembly Solutions, Senju Metal Industry Co. Ltd., Indium Corporation, Heraeus Electronics, Tamura Corporation, Fusion Inc., AIM Solder, Qualitek International Inc., Multicore Solders, Fuchang Solder Industrial Co. Ltd., Solder Chemistry LLC, Inventec Corporation, Hioki Co. Ltd., JBC Soldering, Nihon Superior Co. Ltd., Superior Flux Mfg. Co., MacDermid Alpha Electronics Solutions, Ku Ping Enterprise Co. Ltd., Yazumi Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The solder paste market is intricately segmented to provide a detailed understanding of its diverse applications and formulations. This segmentation includes analysis by type, distinguishing between lead-free and leaded solder pastes, reflecting the ongoing global transition driven by environmental regulations. Further categorization by alloy type, such as Tin-Silver-Copper (SnAgCu) and Tin-Bismuth (SnBi), provides insights into the material science aspect and performance characteristics. The market is also segmented by form, including cream, powder, and liquid, highlighting different physical states optimized for specific manufacturing processes.

Application-based segmentation is crucial, covering major areas like Surface Mount Technology (SMT), semiconductor packaging, and LED packaging, each demanding unique solder paste properties. End-use industries, including consumer electronics, automotive, telecommunications, industrial, and medical, are analyzed to illustrate the varying demands and growth patterns across key sectors. This multi-dimensional segmentation allows for a comprehensive assessment of market dynamics, identifies high-growth areas, and enables strategic decision-making for manufacturers and stakeholders by highlighting specific opportunities and challenges within each segment.

- By Type:

- Lead-free Solder Paste

- Leaded Solder Paste

- By Alloy Type:

- Tin-Silver-Copper (SnAgCu)

- Tin-Bismuth (SnBi)

- Tin-Lead (SnPb)

- Others (e.g., Tin-Antimony, Tin-Zinc)

- By Form:

- Cream

- Powder

- Liquid

- By Application:

- Surface Mount Technology (SMT)

- Semiconductor Packaging

- LED Packaging

- Medical Devices

- Industrial Electronics

- Consumer Electronics

- Automotive Electronics

- Telecommunications

- Others

- By End-Use Industry:

- Consumer Electronics

- Automotive

- Telecommunications

- Industrial

- Medical

- Aerospace & Defense

- Others

Regional Highlights

- Asia Pacific (APAC): Expected to dominate the solder paste market, primarily driven by its position as a global manufacturing hub for consumer electronics, automotive components, and telecommunication equipment. Countries like China, South Korea, Japan, Taiwan, and India are leading the production and consumption of electronic devices, necessitating high volumes of solder paste. Rapid industrialization, increasing disposable incomes, and the expansion of 5G infrastructure further bolster market growth in this region.

- North America: Exhibits significant growth, fueled by strong demand from the automotive electronics, medical devices, and aerospace and defense sectors. The region is characterized by advanced technological adoption and a focus on high-reliability applications, leading to the demand for specialized and high-performance solder paste formulations. Investment in R&D and stringent quality standards also play a crucial role.

- Europe: A key market driven by stringent environmental regulations promoting lead-free solder paste adoption and a strong automotive industry base, particularly in Germany and Eastern Europe. The region's emphasis on industrial automation, smart manufacturing, and the development of advanced electronic systems contributes significantly to market demand, with a focus on sustainable and efficient soldering solutions.

- Latin America: Showing nascent but steady growth in the solder paste market, largely attributed to increasing foreign investments in electronics manufacturing, particularly in countries like Mexico and Brazil. The region's growing consumer base and improving economic conditions are fostering local electronics production and assembly, creating new opportunities for solder paste suppliers.

- Middle East and Africa (MEA): Represents an emerging market with potential, driven by developing telecommunication infrastructure projects, increasing industrialization, and a growing consumer electronics market. While smaller in market share compared to other regions, ongoing economic diversification efforts and technological advancements are expected to contribute to future demand for solder paste.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Solder Paste Market.- KOKI Company Ltd.

- Alpha Assembly Solutions

- Senju Metal Industry Co. Ltd.

- Indium Corporation

- Heraeus Electronics

- Tamura Corporation

- Fusion Inc.

- AIM Solder

- Qualitek International Inc.

- Multicore Solders

- Fuchang Solder Industrial Co. Ltd.

- Solder Chemistry LLC

- Inventec Corporation

- Hioki Co. Ltd.

- JBC Soldering

- Nihon Superior Co. Ltd.

- Superior Flux Mfg. Co.

- MacDermid Alpha Electronics Solutions

- Ku Ping Enterprise Co. Ltd.

- Yazumi Corporation

Frequently Asked Questions

What is solder paste primarily used for in electronics manufacturing?

Solder paste is a crucial material in surface mount technology (SMT) for creating electrical and mechanical connections between electronic components and circuit boards. It is applied to pads on the PCB, components are placed on top, and then heated to form permanent solder joints.

What are the main types of solder paste available in the market?

The market primarily offers two main types: lead-free solder paste, which is increasingly favored due to environmental regulations and health concerns, and traditional leaded solder paste, still used in certain applications where lead-free alternatives are not yet optimal or mandated.

How do environmental regulations impact the solder paste market?

Environmental regulations, such as RoHS and REACH, significantly impact the market by driving the widespread adoption and development of lead-free and halogen-free solder paste formulations. This necessitates continuous innovation and reformulation efforts from manufacturers to ensure compliance and sustainability.

Which industries are the primary consumers of solder paste?

The primary consumers of solder paste include the consumer electronics industry (smartphones, laptops), automotive electronics (EVs, ADAS), telecommunications (5G infrastructure), industrial electronics, and medical device manufacturing. These sectors demand diverse solder paste properties for their specific applications.

What are the key technological trends influencing solder paste development?

Key technological trends include miniaturization of electronic components, increasing demand for fine-pitch applications, advancements in advanced packaging technologies (SiP, PoP), and the need for high-reliability solder joints in harsh environments. These trends drive innovation towards finer particle sizes, low-temperature soldering, and enhanced performance.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted