Smart Water Management Market

Smart Water Management Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702915 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Smart Water Management Market Size

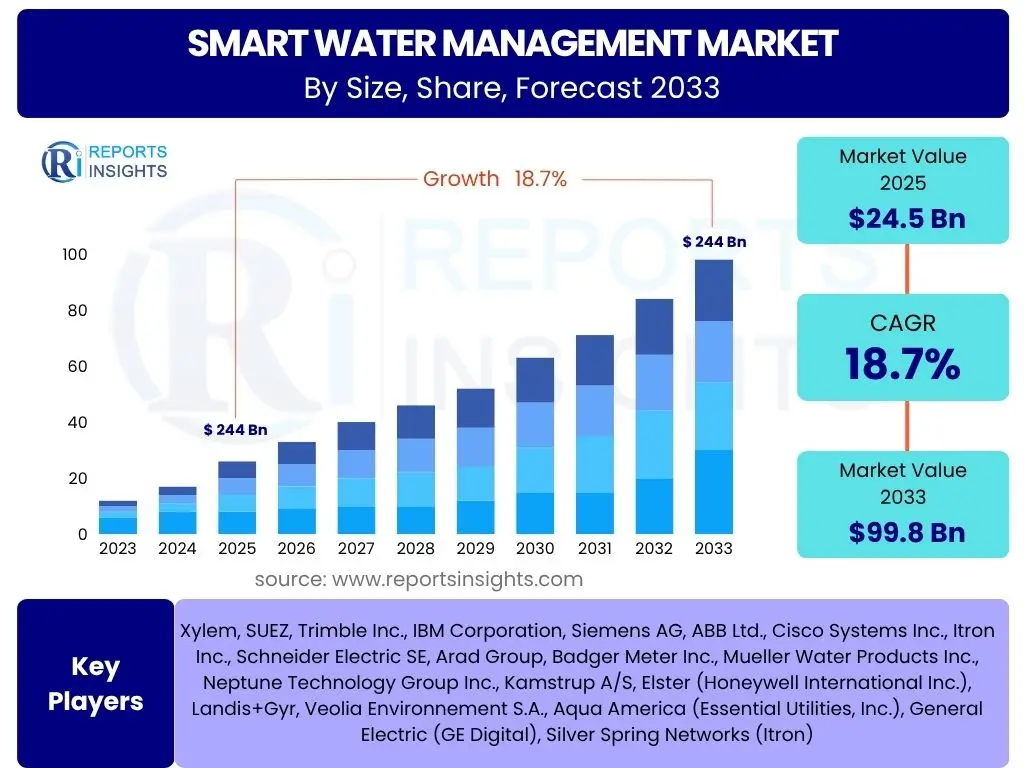

According to Reports Insights Consulting Pvt Ltd, The Smart Water Management Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.7% between 2025 and 2033. The market is estimated at USD 24.5 billion in 2025 and is projected to reach USD 99.8 billion by the end of the forecast period in 2033.

Key Smart Water Management Market Trends & Insights

The Smart Water Management market is currently experiencing a transformative phase, driven by a convergence of technological advancements and increasing global emphasis on resource optimization. A primary trend involves the widespread adoption of Internet of Things (IoT) sensors and advanced metering infrastructure (AMI), enabling real-time data collection and remote monitoring of water networks. This digitalization is paramount for identifying inefficiencies, preventing leaks, and optimizing distribution, thereby addressing critical challenges such as water scarcity and aging infrastructure. Stakeholders are increasingly recognizing the value of proactive management over traditional reactive approaches, leading to greater investments in smart solutions.

Another significant trend is the growing integration of artificial intelligence (AI) and machine learning (ML) capabilities into smart water systems. These technologies are being leveraged for predictive analytics, demand forecasting, anomaly detection, and automated decision-making, which enhance operational efficiency and resource allocation. Furthermore, there is a pronounced shift towards comprehensive, integrated platforms that connect various components of the water management ecosystem, from source to tap, including wastewater treatment. This holistic approach facilitates better data synergy and enables utilities and municipalities to make informed strategic decisions, fostering resilience and sustainability in water resource management.

- Accelerated adoption of IoT sensors and advanced metering infrastructure (AMI) for real-time monitoring and data collection.

- Increased integration of Artificial Intelligence (AI) and Machine Learning (ML) for predictive analytics, demand forecasting, and anomaly detection.

- Growing focus on smart irrigation systems and water quality monitoring to enhance agricultural and environmental sustainability.

- Development and deployment of digital twins and hydraulic modeling for comprehensive network visualization and simulation.

- Emphasis on cybersecurity measures to protect critical water infrastructure from digital threats.

- Expansion of public-private partnerships to fund and implement large-scale smart water initiatives.

- Leveraging big data analytics for improved decision-making and operational efficiency across the water lifecycle.

AI Impact Analysis on Smart Water Management

User queries regarding AI's influence in smart water management frequently center on its practical applications, potential benefits, and implementation challenges. Users are keen to understand how AI can improve efficiency, reduce costs, and enhance sustainability. The core expectation revolves around AI's capacity for intelligent automation and data-driven insights that surpass traditional analytical methods. Specific areas of interest include AI's role in predictive maintenance, leak detection, demand forecasting, and optimizing water distribution networks. There is also a notable concern about the complexity of integrating AI with existing legacy infrastructure and the need for specialized skills.

Artificial intelligence is profoundly transforming the smart water management landscape by enabling unprecedented levels of operational intelligence and predictive capabilities. AI algorithms can analyze vast datasets from sensors, meters, and environmental sources to identify patterns, predict anomalies, and optimize resource allocation in real-time. This allows water utilities to move from reactive maintenance to predictive intervention, significantly reducing water loss from leaks and bursts, minimizing energy consumption, and ensuring higher service reliability. Furthermore, AI contributes to more accurate demand forecasting, helping manage supply and demand fluctuations more effectively and preventing resource depletion during peak periods or drought conditions. The technology also plays a crucial role in water quality monitoring by detecting contaminants and unusual parameters, facilitating rapid response to potential public health risks.

- Predictive maintenance for infrastructure, minimizing downtime and repair costs.

- Enhanced leak detection and localization through pattern recognition in flow data.

- Optimized water distribution and pressure management, reducing energy consumption.

- Accurate demand forecasting for efficient resource allocation and supply management.

- Real-time water quality monitoring and anomaly detection.

- Automated decision-making for network adjustments and incident response.

- Improved customer service through personalized consumption insights and alerts.

- Development of digital twins for simulating network behavior and testing interventions.

Key Takeaways Smart Water Management Market Size & Forecast

Analysis of common user questions regarding the Smart Water Management market size and forecast reveals a strong interest in the underlying drivers of growth, the segments offering the most potential, and the overall trajectory of market expansion. Users seek clarity on how technological advancements, environmental pressures, and regulatory frameworks are shaping the market's future. There is a clear emphasis on understanding the investment opportunities and the long-term sustainability implications of adopting smart water solutions, alongside concerns about the pace of adoption and regional disparities in implementation.

The Smart Water Management market is poised for substantial growth, reflecting a global imperative to address water scarcity, deteriorating infrastructure, and the escalating demands of urbanization and climate change. The projected exponential increase in market valuation underscores the increasing adoption of digital solutions, including IoT, AI, and big data analytics, to enhance efficiency, reduce water loss, and improve water quality. This growth is not merely driven by technological push but also by regulatory pull and the economic benefits associated with optimized water resource management. The market is transitioning from niche applications to mainstream adoption, indicating a widespread recognition of smart technologies as essential tools for future-proof water systems.

- Significant market expansion anticipated, driven by urgent global water challenges.

- Technology integration, particularly IoT and AI, is a primary catalyst for growth.

- Increasing government initiatives and private investments are fueling market adoption.

- Focus shifts towards proactive and predictive water management strategies.

- Efficiency gains and sustainability benefits are key economic motivators for stakeholders.

- Market growth indicates a widespread shift towards digital transformation in water utilities.

Smart Water Management Market Drivers Analysis

The smart water management market is experiencing robust growth propelled by several critical factors. The most prominent driver is the escalating global issue of water scarcity and the increasing strain on existing water resources due to population growth, urbanization, and climate change. This necessitates more efficient and sustainable water management practices. Concurrently, the aging and deteriorating water infrastructure in many developed and developing regions leads to significant water losses, pushing utilities to invest in smart technologies for leak detection, predictive maintenance, and overall network optimization. Furthermore, stringent government regulations and supportive policies aimed at promoting water conservation, efficiency, and quality compliance are incentivizing the adoption of smart solutions, often coupled with substantial public funding.

Technological advancements, particularly in IoT, data analytics, and artificial intelligence, serve as foundational drivers, providing the tools necessary for real-time monitoring, intelligent automation, and data-driven decision-making. The increasing awareness among consumers and industries about the importance of water conservation also contributes to the demand for smart solutions. Finally, the growing demand for accurate billing, improved operational efficiency, and enhanced customer service among water utilities further accelerates the adoption of smart water management systems. These interconnected drivers collectively create a compelling environment for the market's sustained expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Water Scarcity and Stress | +2.1% | Global, particularly arid and semi-arid regions (e.g., Middle East, Africa, parts of Asia) | Ongoing, Long-term |

| Aging and Deteriorating Water Infrastructure | +1.8% | North America, Europe, parts of developed Asia Pacific | Short-term to Long-term |

| Stringent Government Regulations and Policies | +1.5% | Europe, North America, Australia, rapidly developing Asian economies | Medium-term to Long-term |

| Advancements in IoT, AI, and Data Analytics Technologies | +2.3% | Global, especially technologically advanced regions | Ongoing, Short-term to Medium-term |

| Growing Urbanization and Industrialization | +1.6% | Asia Pacific, Latin America, Africa | Long-term |

Smart Water Management Market Restraints Analysis

Despite significant growth drivers, the smart water management market faces several notable restraints that could impede its full potential. A primary challenge is the high initial investment costs associated with deploying smart water infrastructure, including sensors, advanced meters, communication networks, and software platforms. Many municipalities and smaller utilities, particularly in developing regions, face budget constraints that make such large-scale capital expenditures difficult to justify, leading to slower adoption rates. Furthermore, the complexity of integrating new smart systems with existing legacy infrastructure poses a significant hurdle. Older systems may lack the necessary compatibility or digital readiness, requiring substantial upgrades or complete overhauls, which adds to both cost and implementation time.

Another significant restraint involves data security and privacy concerns. As smart water systems collect vast amounts of sensitive operational and consumption data, protecting this information from cyber threats and ensuring compliance with data privacy regulations becomes paramount. Stakeholders may hesitate to adopt solutions if they perceive vulnerabilities in data handling. Additionally, a lack of skilled personnel capable of managing, analyzing, and maintaining complex smart water technologies is a limiting factor in many regions. Without adequate expertise, utilities may struggle to maximize the benefits of these advanced systems. Finally, the fragmented regulatory landscape across different regions and countries can create inconsistencies in standards and policies, complicating the widespread deployment and interoperability of smart water solutions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment Costs and Budget Constraints | -1.9% | Developing economies, municipalities with limited funding globally | Short-term to Medium-term |

| Integration Complexities with Legacy Infrastructure | -1.5% | Mature markets (North America, Europe) with established older systems | Medium-term |

| Data Security and Privacy Concerns | -1.2% | Global, particularly in regions with strict data protection laws (e.g., EU) | Ongoing |

| Lack of Skilled Personnel and Expertise | -1.0% | Global, more pronounced in developing regions | Short-term to Medium-term |

| Regulatory and Policy Fragmentation | -0.8% | Global, impacting international solution deployment | Long-term |

Smart Water Management Market Opportunities Analysis

The smart water management market presents significant opportunities for growth and innovation, particularly through the expansion of smart city initiatives worldwide. As urban areas increasingly prioritize sustainable living and efficient resource management, the integration of smart water solutions becomes a foundational component of broader smart city frameworks. This creates a synergistic effect, enabling comprehensive resource optimization across various urban services. Another major opportunity lies in the untapped potential of emerging markets, especially in Asia Pacific, Latin America, and Africa. These regions face acute water challenges, rapid urbanization, and are often developing new infrastructure, providing a fertile ground for the direct adoption of advanced smart water technologies without the burden of extensive legacy systems.

The continuous evolution of AI and machine learning offers substantial opportunities for developing more sophisticated predictive maintenance, anomaly detection, and demand forecasting models, leading to even greater efficiencies and resilience in water networks. Furthermore, the increasing emphasis on public-private partnerships (PPPs) provides a viable pathway for accelerating the deployment of smart water infrastructure. PPPs can mitigate financial risks for municipalities and leverage private sector expertise and innovation. Finally, the demand for advanced analytics and digital twin technology, which allows for virtual simulation and optimization of water systems, represents a high-growth area for specialized solution providers, offering deeper insights and strategic planning capabilities for water utilities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with Smart City Initiatives | +1.7% | Urban centers globally, particularly Asia Pacific, Europe, North America | Medium-term to Long-term |

| Expansion into Emerging Markets | +2.0% | Asia Pacific, Latin America, Middle East & Africa | Long-term |

| Advancements in AI, ML, and Predictive Analytics | +1.8% | Global, especially technologically advanced regions | Ongoing, Short-term to Medium-term |

| Increasing Adoption of Public-Private Partnerships (PPPs) | +1.3% | Global, particularly for large-scale infrastructure projects | Medium-term to Long-term |

| Demand for Digital Twin and Advanced Modeling | +1.5% | Global, primarily advanced utilities and industrial sectors | Medium-term |

Smart Water Management Market Challenges Impact Analysis

The smart water management market faces distinct challenges that require strategic navigation to ensure widespread adoption and effective implementation. Cybersecurity threats represent a significant concern, as digitalizing critical water infrastructure creates new vulnerabilities for malicious attacks, potentially disrupting service or compromising sensitive data. Ensuring robust security protocols is paramount but also complex and costly. Another key challenge is the interoperability and standardization of diverse smart water technologies. The lack of universal standards can hinder seamless integration between different vendor solutions and existing legacy systems, leading to fragmented data and operational inefficiencies. This often complicates system deployments and limits scalability for utilities.

Regulatory complexities and fragmented governance structures across different jurisdictions can also pose substantial hurdles. Varied regulations concerning data privacy, technology adoption, and infrastructure investment can create inconsistencies and delays in project approvals and deployments. Furthermore, stakeholder resistance, including reluctance from utility personnel to adopt new technologies due to perceived job security threats or a lack of training, can impede successful implementation. Overcoming these challenges requires collaborative efforts between technology providers, utilities, governments, and regulatory bodies to establish clear guidelines, promote skill development, and build trust in smart water solutions.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Cybersecurity Risks and Data Vulnerabilities | -1.3% | Global, particularly for interconnected critical infrastructure | Ongoing |

| Interoperability and Standardization Issues | -1.1% | Global, affecting multi-vendor deployments | Short-term to Medium-term |

| Regulatory and Governance Complexities | -0.9% | Global, varying by country and region | Long-term |

| Resistance to Change and Lack of Public Acceptance | -0.7% | Global, varying by community and stakeholder group | Short-term to Medium-term |

| High Cost of Data Management and Analysis | -0.6% | Global, particularly for smaller utilities | Ongoing |

Smart Water Management Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Smart Water Management market, offering detailed insights into its current size, historical performance, and future growth projections from 2025 to 2033. It meticulously examines key market trends, drivers, restraints, opportunities, and challenges that influence market dynamics. The report also includes a thorough segmentation analysis by component, application, and end-user, complemented by a detailed regional breakdown to highlight unique market characteristics across different geographies. Additionally, it features profiles of leading market players, offering a holistic view of the competitive landscape and strategic initiatives shaping the industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 24.5 Billion |

| Market Forecast in 2033 | USD 99.8 Billion |

| Growth Rate | 18.7% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Xylem, SUEZ, Trimble Inc., IBM Corporation, Siemens AG, ABB Ltd., Cisco Systems Inc., Itron Inc., Schneider Electric SE, Arad Group, Badger Meter Inc., Mueller Water Products Inc., Neptune Technology Group Inc., Kamstrup A/S, Elster (Honeywell International Inc.), Landis+Gyr, Veolia Environnement S.A., Aqua America (Essential Utilities, Inc.), General Electric (GE Digital), Silver Spring Networks (Itron) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Smart Water Management market is meticulously segmented to provide a granular understanding of its diverse components and applications. This segmentation allows for precise market sizing and forecasting, highlighting areas of high growth and specific technological adoption patterns. Analyzing the market across various segments helps stakeholders identify niche opportunities, understand consumer and industry needs, and tailor solutions effectively. The structure spans hardware, software, and services, offering a comprehensive view of the technological ecosystem involved, from physical sensors and smart meters to advanced analytics platforms and consulting services. This detailed breakdown facilitates strategic planning and investment decisions for market participants.

Furthermore, the segmentation by application elucidates how smart water management technologies are being deployed across critical areas such as water distribution, leakage detection, quality monitoring, and smart metering. Understanding these application-specific dynamics is crucial for solution providers to develop targeted offerings that address pressing challenges in each domain. The end-user segmentation, encompassing utilities, industrial, commercial, residential, and agricultural sectors, reveals the varying demands and adoption drivers across different consumer groups. This multi-dimensional segmentation provides a robust framework for assessing market maturity, identifying key growth areas, and understanding the competitive landscape within the Smart Water Management industry.

- By Component:

- Hardware (Sensors, Smart Meters, Pipes & Fittings, Valves, Pumps, Controllers, Communication Infrastructure)

- Software (Analytics & Data Management, Network Management, Billing & Customer Information, SCADA, GIS, Cloud-based Platforms)

- Services (Professional Services, Managed Services, Support & Maintenance)

- By Application:

- Water Distribution Network Monitoring

- Leakage Detection & Management

- Pressure Management

- Water Quality Monitoring

- Smart Metering & Billing

- Wastewater Management

- Irrigation Management

- Residential Water Management

- Commercial & Industrial Water Management

- Drainage Management

- By End-User:

- Utilities & Municipalities

- Industrial

- Commercial

- Residential

- Agriculture

Regional Highlights

- North America: A mature market with high adoption rates of smart water technologies due to aging infrastructure, increasing awareness about water conservation, and significant investments in smart city initiatives. The U.S. and Canada are leading in deploying AMI, leak detection systems, and advanced analytics, driven by regulatory support and the presence of key technology providers.

- Europe: Characterized by strong government mandates for water efficiency, stringent environmental regulations, and a proactive approach to adopting sustainable practices. Countries like the UK, Germany, France, and the Netherlands are at the forefront of implementing smart metering, wastewater management solutions, and digital twin technologies.

- Asia Pacific (APAC): The fastest-growing region driven by rapid urbanization, industrial growth, increasing population, and escalating water scarcity issues, particularly in countries like China, India, and Australia. Significant investments in new smart infrastructure and the adoption of IoT-based solutions are prevalent.

- Latin America: An emerging market with growing recognition of smart water management benefits, primarily driven by the need to address water losses, improve service delivery, and manage increasing water demand in expanding urban areas. Brazil and Mexico are key markets showing promising growth.

- Middle East & Africa (MEA): Experiencing significant growth due to extreme water scarcity, particularly in the Middle East, necessitating advanced solutions for water conservation, desalination, and efficient distribution. Government initiatives and large-scale infrastructure projects are driving market adoption in this region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Smart Water Management Market.- Xylem

- SUEZ

- Trimble Inc.

- IBM Corporation

- Siemens AG

- ABB Ltd.

- Cisco Systems Inc.

- Itron Inc.

- Schneider Electric SE

- Arad Group

- Badger Meter Inc.

- Mueller Water Products Inc.

- Neptune Technology Group Inc.

- Kamstrup A/S

- Elster (Honeywell International Inc.)

- Landis+Gyr

- Veolia Environnement S.A.

- Aqua America (Essential Utilities, Inc.)

- General Electric (GE Digital)

- Silver Spring Networks (Itron)

Frequently Asked Questions

Analyze common user questions about the Smart Water Management market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Smart Water Management?

Smart Water Management (SWM) involves using advanced technologies like IoT sensors, data analytics, and artificial intelligence to monitor, control, and optimize water networks in real-time. It aims to improve water efficiency, reduce losses, enhance quality, and ensure sustainable resource utilization from source to consumption.

What are the primary benefits of implementing Smart Water Management solutions?

Key benefits include significant reduction in water loss through proactive leak detection, optimized pressure management, lower operational costs due to increased efficiency, improved water quality and public health, enhanced customer service, and better planning for future water demands.

How does IoT specifically impact Smart Water Management?

IoT enables SWM by providing real-time data from connected devices such as smart meters, sensors, and actuators embedded throughout the water infrastructure. This data allows for continuous monitoring of flow, pressure, quality, and consumption, facilitating immediate insights and automated responses for improved network performance.

What are the key technologies used in Smart Water Management systems?

Core technologies include Advanced Metering Infrastructure (AMI), various types of sensors (pressure, flow, water quality), Geographic Information Systems (GIS), Supervisory Control and Data Acquisition (SCADA) systems, cloud computing, big data analytics platforms, and Artificial Intelligence (AI) and Machine Learning (ML) algorithms.

What are the main challenges in adopting Smart Water Management?

Major challenges include high upfront investment costs, complexities in integrating new smart systems with existing legacy infrastructure, concerns regarding data security and privacy, a shortage of skilled professionals to manage these advanced systems, and navigating fragmented regulatory landscapes.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted