Facility Management Market

Facility Management Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703423 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

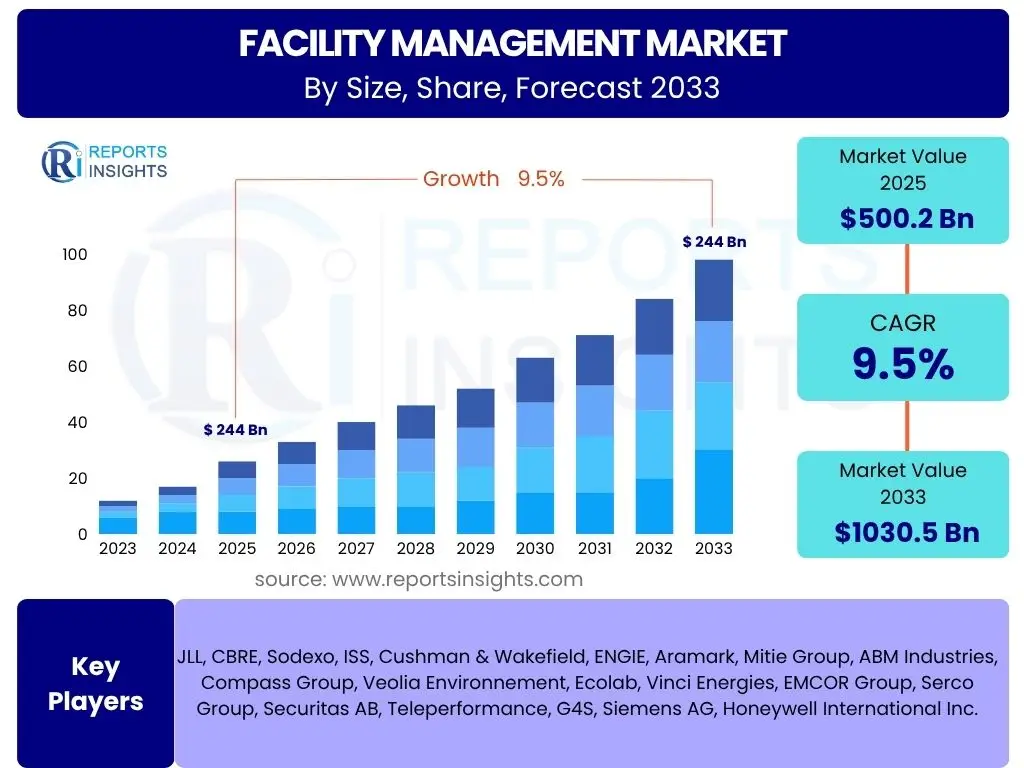

Facility Management Market Size

According to Reports Insights Consulting Pvt Ltd, The Facility Management Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. The market is estimated at USD 500.2 Billion in 2025 and is projected to reach USD 1030.5 Billion by the end of the forecast period in 2033.

Key Facility Management Market Trends & Insights

User inquiries frequently focus on the evolving landscape of facility management, particularly how technological advancements and changing business priorities are shaping service delivery. There is significant interest in understanding the shift towards integrated service models, the increasing demand for sustainable and energy-efficient building operations, and the emphasis on occupant experience within commercial and industrial spaces. Furthermore, the adoption of smart building technologies and data analytics for predictive maintenance and operational optimization is a recurrent theme in user questions about market trends.

The market is witnessing a profound transformation driven by digital integration and a heightened awareness of environmental responsibilities. Facility management is moving beyond traditional maintenance, evolving into a strategic function that directly impacts business continuity, employee well-being, and operational costs. This includes a shift from reactive to proactive and predictive maintenance, leveraging real-time data to anticipate failures and optimize resource allocation. The market is also increasingly influenced by the need for regulatory compliance regarding health, safety, and environmental standards, pushing providers to adopt more sophisticated and transparent operational practices.

- Digital transformation and smart building integration for enhanced operational efficiency.

- Rising adoption of Integrated Facility Management (IFM) services for streamlined operations.

- Increasing focus on sustainability, energy efficiency, and green building certifications.

- Emphasis on occupant well-being and productivity through improved indoor environments.

- Shift from traditional reactive maintenance to predictive and proactive strategies.

- Growth in demand for specialized services like cybersecurity for building systems.

AI Impact Analysis on Facility Management

Common user questions regarding AI's impact on Facility Management revolve around its practical applications, benefits in terms of efficiency and cost reduction, and potential challenges like job displacement or data security. Users are keen to understand how AI can automate routine tasks, optimize energy consumption, and enhance predictive maintenance capabilities. There is also curiosity about the role of AI in improving decision-making processes and creating smarter, more responsive building environments, alongside concerns about the initial investment and skill requirements for AI adoption.

Artificial Intelligence is set to revolutionize facility management by enabling unprecedented levels of automation, predictive analytics, and operational intelligence. AI-powered systems can analyze vast amounts of data from IoT sensors, building management systems, and historical records to predict equipment failures, optimize energy usage in real-time, and automate routine tasks like scheduling maintenance or adjusting climate controls. This leads to significant reductions in operational costs, minimized downtime, and improved resource allocation, transforming facility operations from reactive to highly proactive and intelligent.

The integration of AI also enhances the occupant experience by personalizing environmental controls and improving safety protocols through advanced surveillance and anomaly detection. While AI adoption presents challenges related to data privacy, cybersecurity, and the need for a skilled workforce, its long-term benefits in creating autonomous, energy-efficient, and secure facilities are undeniable. AI applications are moving beyond basic automation to provide actionable insights for strategic decision-making, ensuring buildings are not just maintained but actively optimized for performance and sustainability.

- Enhanced predictive maintenance: AI algorithms analyze equipment data to forecast potential failures, reducing downtime and maintenance costs.

- Optimized energy management: AI systems learn usage patterns to autonomously adjust HVAC, lighting, and other systems for maximum energy efficiency.

- Automated operational tasks: AI can automate scheduling, resource allocation, and routine monitoring, freeing up human staff for more complex tasks.

- Improved space utilization: AI-powered analytics provide insights into how spaces are used, informing optimal layouts and resource deployment.

- Enhanced security and surveillance: AI-driven video analytics can detect unusual activities, identify security breaches, and streamline access control.

- Data-driven decision making: AI processes large datasets to offer actionable insights for strategic planning, budgeting, and performance improvement.

Key Takeaways Facility Management Market Size & Forecast

User queries frequently seek a concise summary of the market's trajectory, identifying the most impactful growth drivers and the overarching investment prospects. They aim to understand where the market is headed, what factors will sustain its growth, and what are the most promising areas for future development and technological adoption within facility management. Insights into the long-term viability and resilience of the sector are also a common area of interest.

The Facility Management market is poised for robust expansion, driven by increasing outsourcing trends, technological advancements, and a growing emphasis on operational efficiency and sustainability across various industries. The substantial projected growth in market size signifies a critical shift in how organizations manage their physical assets and optimize their operational environments. This forecast indicates a sustained demand for integrated, data-driven, and specialized facility management services, reflecting the sector's evolving role from a support function to a strategic business enabler.

- Substantial growth trajectory: The market is set to more than double in size by 2033, indicating robust demand for services.

- Technological integration as a core driver: Smart building technologies, IoT, and AI are pivotal to future growth and service enhancement.

- Outsourcing remains a key strategy: Businesses increasingly prefer specialized third-party providers for efficiency and cost-effectiveness.

- Sustainability is not a trend, but a mandate: Green building practices and energy efficiency are central to new service offerings.

- Occupant experience is paramount: FM services are increasingly focused on creating productive, comfortable, and safe environments.

- Resilient market against economic shifts: Essential nature of FM services ensures continuous demand even amidst economic fluctuations.

Facility Management Market Drivers Analysis

The Facility Management market is significantly propelled by several key factors that reinforce its strategic importance to businesses globally. The increasing complexities of managing diverse facilities, coupled with a strong emphasis on operational efficiency and cost reduction, are leading organizations to outsource their facility management needs. Furthermore, rapid urbanization and the proliferation of smart buildings are creating new demands for advanced, integrated services. The continuous evolution of technology, particularly in IoT, AI, and data analytics, is enabling more sophisticated and proactive facility management solutions, further driving market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing demand for integrated services (IFM) | +2.5% | North America, Europe, Asia Pacific | Short-term to Mid-term (2025-2029) |

| Growing adoption of IoT, AI, and automation in buildings | +2.0% | Global, particularly developed economies | Mid-term to Long-term (2027-2033) |

| Focus on energy efficiency and sustainable practices | +1.8% | Europe, North America, emerging Asia Pacific | Short-term to Long-term (2025-2033) |

| Regulatory compliance and government mandates | +1.5% | Global, varies by region (e.g., EU Green Deal) | Short-term to Long-term (2025-2033) |

| Rising outsourcing of non-core business activities | +1.7% | Global, strong in North America and Europe | Short-term to Mid-term (2025-2030) |

Facility Management Market Restraints Analysis

Despite significant growth potential, the Facility Management market faces several inherent restraints that could temper its expansion. High initial capital expenditure required for adopting advanced smart building technologies and integrated platforms can be a barrier for smaller enterprises or those with limited budgets. Additionally, the shortage of skilled professionals equipped to manage complex digital facility systems poses a challenge in maintaining service quality and innovation. Concerns over data security and privacy, especially with the increasing integration of IoT devices and cloud-based solutions, also present a significant hurdle for widespread adoption and trust.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial investment for advanced technologies | -1.2% | Emerging markets, small to medium enterprises (SMEs) | Short-term to Mid-term (2025-2029) |

| Shortage of skilled workforce in smart FM | -1.0% | Global, particularly developing regions | Mid-term (2027-2031) |

| Data security and privacy concerns with IoT integration | -0.8% | Global, highly sensitive sectors (e.g., healthcare) | Short-term to Long-term (2025-2033) |

| Resistance to change from traditional FM practices | -0.7% | Traditional industries, public sector | Short-term (2025-2027) |

| Economic uncertainties and budget constraints | -0.9% | Global, highly volatile economic regions | Short-term (2025-2026) |

Facility Management Market Opportunities Analysis

Significant opportunities abound in the Facility Management market, driven by evolving client needs and technological breakthroughs. The expanding scope of smart cities initiatives worldwide presents a vast untapped potential for integrated urban infrastructure management. Moreover, the increasing demand for specialized and niche services, such as healthcare facility management or data center maintenance, allows for market diversification and value creation. The ongoing push for digital transformation in various industries opens doors for FM providers to offer comprehensive technology-driven solutions, including predictive maintenance and energy optimization through advanced analytics. Furthermore, emerging economies represent greenfield opportunities for market entry and expansion, offering vast potential for new contracts and partnerships as infrastructure develops.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with smart city infrastructure projects | +1.8% | Asia Pacific, Middle East, Europe | Mid-term to Long-term (2027-2033) |

| Expansion into niche and specialized service areas | +1.5% | Global, particularly healthcare, data centers | Short-term to Mid-term (2025-2030) |

| Leveraging Big Data and advanced analytics for insights | +1.7% | North America, Europe, technologically advanced APAC | Mid-term to Long-term (2027-2033) |

| Growth in emerging economies and infrastructure development | +1.6% | ASEAN, India, Latin America, Africa | Long-term (2029-2033) |

| Development of circular economy models and waste management | +1.0% | Europe, North America | Mid-term to Long-term (2027-2033) |

Facility Management Market Challenges Impact Analysis

The Facility Management market is contending with several notable challenges that necessitate strategic adaptation from service providers. Intense competition from a fragmented market, comprising both large multinational corporations and numerous local players, exerts downward pressure on pricing and profit margins. Moreover, the rapid pace of technological change requires continuous investment in new solutions and upskilling of the workforce, which can strain resources. Managing complex service level agreements (SLAs) across diverse client portfolios and ensuring consistent quality of service remains a significant operational challenge. Additionally, the increasing stringency of regulatory environments regarding safety, environment, and data protection demands meticulous compliance and constant vigilance, adding to operational complexities and costs for service providers.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense competition and price pressure | -1.5% | Global, highly fragmented markets | Short-term to Mid-term (2025-2030) |

| Rapid technological obsolescence and integration complexity | -1.1% | Global, particularly for less tech-savvy firms | Short-term to Long-term (2025-2033) |

| Managing complex Service Level Agreements (SLAs) | -0.9% | Global, especially for large, diversified contracts | Short-term to Long-term (2025-2033) |

| Cybersecurity threats to interconnected building systems | -0.8% | Global, critical infrastructure, smart buildings | Short-term to Long-term (2025-2033) |

| Compliance with evolving global and local regulations | -0.7% | Global, especially highly regulated industries | Short-term to Long-term (2025-2033) |

Facility Management Market - Updated Report Scope

This comprehensive market research report on the Facility Management market provides an in-depth analysis of current market dynamics, historical data, and future growth projections. It offers strategic insights into market size, key trends, drivers, restraints, and opportunities, segmented by various service types, deployment models, and end-user industries. The report also includes a thorough regional analysis, identifying high-growth markets and the competitive landscape, making it an essential tool for stakeholders seeking to understand and capitalize on the evolving Facility Management sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 500.2 Billion |

| Market Forecast in 2033 | USD 1030.5 Billion |

| Growth Rate | 9.5% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | JLL, CBRE, Sodexo, ISS, Cushman & Wakefield, ENGIE, Aramark, Mitie Group, ABM Industries, Compass Group, Veolia Environnement, Ecolab, Vinci Energies, EMCOR Group, Serco Group, Securitas AB, Teleperformance, G4S, Siemens AG, Honeywell International Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Facility Management market is comprehensively segmented to provide a granular view of its diverse components and their respective growth trajectories. These segments include breakdowns by service type, differentiating between hard and soft facility management, and increasingly, integrated facility management solutions which combine various services under a single contract. Further segmentation occurs by deployment model, distinguishing between on-premise solutions for in-house management and cloud-based platforms for outsourced or technologically advanced operations. The market is also analyzed across various end-user industries, recognizing the unique needs of sectors such as commercial, industrial, healthcare, and public administration. Lastly, the market is categorized by the type of management, differentiating between outsourced services provided by third-party experts and in-house management by an organization's internal team, reflecting the varied operational strategies adopted by businesses globally.

- By Service Type:

- Hard FM: Encompasses services related to the physical structure of a building and its systems, including HVAC maintenance, electrical systems, plumbing, civil works, and fire safety systems. These are typically fixed and permanent installations.

- Soft FM: Covers services that make a building habitable and operational, focusing on the people within it. This includes cleaning and janitorial services, landscaping, security services, waste management, catering, and mailroom services.

- Integrated FM: Represents a holistic approach where multiple facility management services, both hard and soft, are delivered through a single contract or provider, aiming for greater synergy, efficiency, and cost savings.

- By Deployment:

- On-premise: Facility management software and systems are installed and run on the organization's own servers and infrastructure. This offers greater control but requires significant upfront investment and IT resources.

- Cloud-based: Services and software are hosted on external servers and accessed via the internet. This model offers flexibility, scalability, reduced upfront costs, and ease of access from various locations, appealing to a wide range of businesses.

- By End-User Industry:

- Commercial: Includes corporate offices, retail spaces, shopping malls, and hospitality establishments (hotels, restaurants), focusing on optimizing client and employee experience.

- Industrial: Covers manufacturing plants, warehouses, logistics centers, and utility companies, emphasizing operational uptime, safety, and compliance with industrial standards.

- Government & Public Sector: Encompasses government buildings, public institutions, defense facilities, and infrastructure, with a strong focus on public safety, regulatory compliance, and budget efficiency.

- Healthcare: Includes hospitals, clinics, and medical facilities, demanding stringent hygiene, safety, and specialized equipment maintenance to ensure patient well-being.

- Education: Involves schools, colleges, and universities, focusing on providing a safe, conducive learning environment, maintenance of academic infrastructure, and resource management.

- By Type:

- Outsourced: Refers to organizations contracting third-party service providers for their facility management needs, leveraging specialized expertise, cost efficiencies, and scalability.

- In-house: Pertains to organizations managing their facility operations with their own dedicated staff and resources, maintaining direct control over processes and personnel.

Regional Highlights

- North America: This region dominates the Facility Management market due to early adoption of integrated services, advanced technological infrastructure, and the presence of numerous key market players. The strong emphasis on smart building technologies, energy efficiency mandates, and a mature outsourcing culture continue to drive growth. High corporate demand for optimizing operational costs and enhancing employee productivity also contributes significantly to market expansion.

- Europe: Europe represents a robust market, driven by stringent regulatory frameworks concerning environmental sustainability, energy performance of buildings, and workplace safety. Countries like the UK, Germany, and France are at the forefront of adopting advanced IFM solutions and sustainable practices. The region's focus on green buildings and circular economy principles is fostering innovation in facility management services.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, fueled by rapid urbanization, extensive infrastructure development projects, and increasing foreign direct investment in commercial and industrial sectors. Emerging economies such as China, India, and ASEAN countries are witnessing substantial growth in the construction of smart cities and corporate facilities, leading to a surge in demand for professional facility management services.

- Latin America: This region is experiencing steady growth, primarily driven by increasing awareness of the benefits of professional facility management services among local businesses and multinational corporations expanding their operations. Economic development and urbanization in countries like Brazil and Mexico are creating new opportunities, though market penetration of advanced FM solutions remains lower compared to developed regions.

- Middle East and Africa (MEA): The MEA region is characterized by significant investment in large-scale infrastructure projects, including mega-cities and commercial hubs, particularly in the GCC countries. This unprecedented construction boom is driving the demand for comprehensive facility management services, with a growing focus on integrating smart technologies and sustainable practices to manage these new developments.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Facility Management Market.- Jones Lang LaSalle (JLL)

- CBRE Group, Inc.

- Sodexo

- ISS A/S

- Cushman & Wakefield plc

- ENGIE SA

- Aramark

- Mitie Group PLC

- ABM Industries Inc.

- Compass Group PLC

- Veolia Environnement S.A.

- Ecolab Inc.

- Vinci Energies

- EMCOR Group, Inc.

- Serco Group plc

- Securitas AB

- Teleperformance SE

- G4S plc

- Siemens AG

- Honeywell International Inc.

Frequently Asked Questions

What is Facility Management and why is it important?

Facility Management (FM) is a professional discipline encompassing multiple disciplines to ensure functionality, comfort, safety, and efficiency of a built environment by integrating people, place, process, and technology. It is crucial because it optimizes operational costs, extends asset lifecycles, ensures regulatory compliance, enhances occupant well-being, and supports an organization's core business objectives, thereby directly impacting productivity and profitability. Effective FM enables a seamless and supportive environment for an organization's primary activities, allowing them to focus on their core competencies while the facility is expertly managed.

What are the primary types of services offered in Facility Management?

Facility Management services are broadly categorized into Hard FM and Soft FM, often integrated into a comprehensive solution. Hard FM services deal with the physical aspects of the building, such as HVAC systems maintenance, electrical systems, plumbing, and structural upkeep, ensuring the building's infrastructure functions efficiently. Soft FM services focus on human-centric aspects and general operations, including cleaning, security, landscaping, waste management, catering, and administrative support. Integrated Facility Management (IFM) combines both hard and soft services under a single provider or contract to achieve greater synergy, operational efficiency, and cost savings.

How is technology impacting the Facility Management market?

Technology is fundamentally transforming the Facility Management market by introducing smart building solutions, IoT devices, Artificial Intelligence (AI), and data analytics. These technologies enable real-time monitoring of building systems, predictive maintenance through data analysis, optimized energy consumption, and enhanced security. AI and automation are streamlining routine tasks, improving operational efficiency, and providing actionable insights for strategic decision-making. The integration of technology allows for more proactive, data-driven, and sustainable facility operations, creating intelligent environments that adapt to occupant needs and business objectives.

What are the key drivers for growth in the Facility Management market?

Key growth drivers for the Facility Management market include the increasing trend of outsourcing non-core business activities to specialized providers, the growing adoption of advanced technologies such as IoT, AI, and cloud-based solutions for enhanced efficiency, and a rising global emphasis on sustainable and energy-efficient building operations. Additionally, rapid urbanization and infrastructure development, coupled with stricter regulatory compliance requirements for health, safety, and environmental standards, are significantly contributing to the market's expansion by increasing the demand for professional and integrated facility management services.

What are the main challenges faced by the Facility Management industry?

The Facility Management industry faces several challenges, including intense market competition leading to price pressures, a shortage of skilled professionals capable of managing increasingly complex digital and smart building systems, and significant initial capital investment requirements for adopting advanced technologies. Concerns over data security and privacy, particularly with the proliferation of interconnected devices, also pose a considerable challenge. Additionally, managing intricate Service Level Agreements (SLAs) across diverse client portfolios and adapting to rapidly evolving regulatory landscapes demand constant vigilance and strategic flexibility from service providers.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted