Smart Glass in Automotive Market

Smart Glass in Automotive Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703119 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Smart Glass in Automotive Market Size

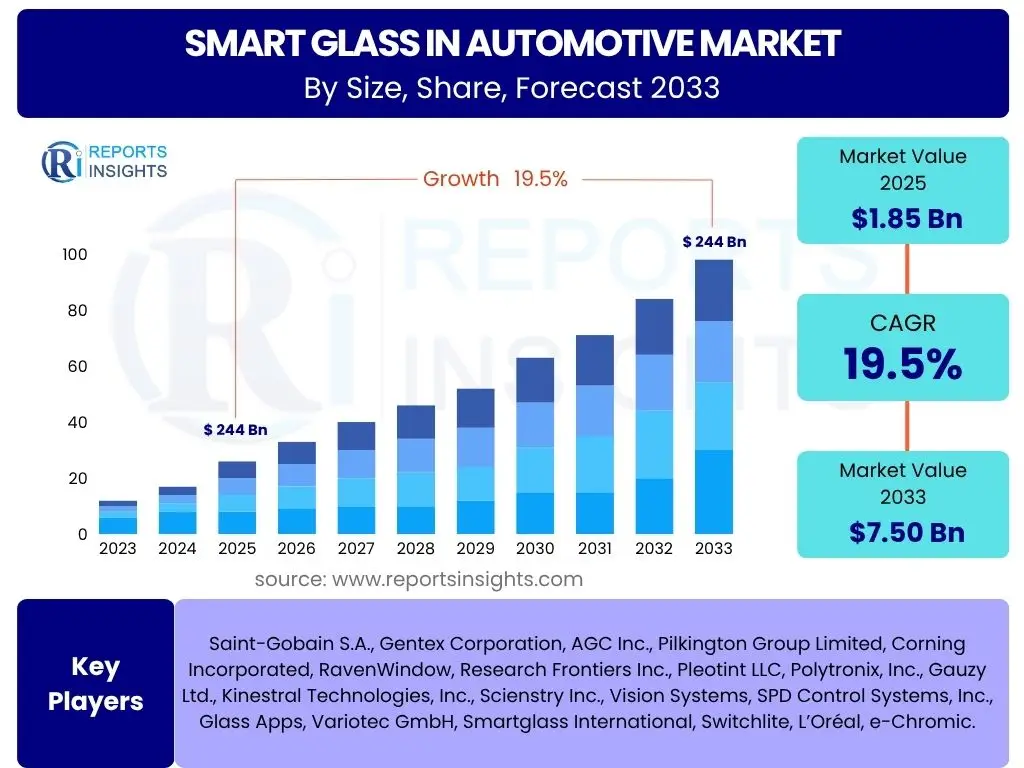

According to Reports Insights Consulting Pvt Ltd, The Smart Glass in Automotive Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 19.5% between 2025 and 2033. The market is estimated at USD 1.85 billion in 2025 and is projected to reach USD 7.50 billion by the end of the forecast period in 2033.

Key Smart Glass in Automotive Market Trends & Insights

The Smart Glass in Automotive market is undergoing significant transformation, driven by advancements in material science, electronics integration, and evolving consumer expectations for vehicle comfort, safety, and personalization. A prominent trend involves the increasing adoption of electrochromic and suspended particle device (SPD) technologies, which offer dynamic light control and instant privacy, catering to the luxury and premium vehicle segments. These technologies are increasingly integrated into panoramic roofs, side windows, and rearview mirrors, enhancing the in-cabin experience and reducing glare.

Another key trend is the growing emphasis on energy efficiency and thermal management within vehicles. Smart glass solutions help regulate interior temperatures by controlling solar heat gain, thereby reducing the reliance on air conditioning systems and improving fuel efficiency or extending electric vehicle range. Furthermore, the convergence of smart glass with advanced driver-assistance systems (ADAS) and augmented reality (AR) functionalities is emerging, transforming windshields into interactive displays that can project navigation, speed, and other crucial information directly into the driver's line of sight, promising a more intuitive and safer driving experience.

The market also observes a shift towards greater customization and connectivity. Consumers are seeking vehicles that offer a more personalized environment, allowing them to adjust transparency, color, and even display content on glass surfaces. This trend is bolstered by the integration of smart glass systems with vehicle infotainment and connectivity platforms, enabling seamless control via voice commands, touchscreens, or smartphone applications. The development of lighter, more durable, and cost-effective smart glass materials is also a continuous trend, aiming to expand their application beyond premium segments to mass-market vehicles.

- Enhanced integration of electrochromic and SPD technologies in premium and luxury vehicles.

- Increased focus on energy efficiency and thermal regulation through dynamic solar control.

- Convergence of smart glass with ADAS and augmented reality for interactive windshields.

- Growing demand for personalized in-cabin experiences and connectivity features.

- Development of cost-effective and lightweight smart glass materials for broader market adoption.

- Emphasis on privacy and security features through instant opaqueness.

- Regulatory push for improved occupant comfort and safety standards.

AI Impact Analysis on Smart Glass in Automotive

Artificial Intelligence is poised to revolutionize the Smart Glass in Automotive market by enabling more intelligent, adaptive, and predictive functionalities. Users are keen to understand how AI can elevate the performance and user experience of smart glass beyond simple tinting. One primary area of impact is through environmental sensing and adaptive control. AI algorithms, processing data from external light sensors, GPS, and weather forecasts, can autonomously adjust glass transparency to optimize cabin comfort, reduce glare, and maximize energy efficiency without manual intervention. This predictive capability moves smart glass from a reactive to a proactive system, anticipating changes in driving conditions.

Furthermore, AI will significantly enhance personalization and user interaction. By learning individual driver preferences, AI can create customized profiles for tint levels, privacy settings, and even projected display content. Gesture recognition and voice control, powered by AI, could allow intuitive interaction with smart glass, making adjustments seamless and hands-free. This integration is crucial for creating a truly intelligent cabin environment where the vehicle adapts to the occupant's needs, improving both convenience and safety by minimizing driver distraction.

The advent of autonomous vehicles presents another profound impact area for AI in smart glass. As vehicles become self-driving, the cabin transforms into a multi-functional space for work, relaxation, or entertainment. AI can manage dynamic privacy settings, transforming windows into interactive displays for meetings or entertainment, or instantly switching to opaque for passenger privacy. Predictive analytics, driven by AI, can also monitor the integrity and performance of the smart glass itself, predicting maintenance needs or optimizing material properties for longevity, ensuring reliability and safety in future mobility solutions.

- Adaptive tinting: AI-driven adjustment of glass transparency based on external conditions (light, weather) and occupant preferences.

- Personalized cabin environment: AI learning and applying individual user preferences for privacy, comfort, and display settings.

- Enhanced user interaction: Integration of AI-powered voice commands and gesture controls for seamless smart glass operation.

- Autonomous vehicle integration: Dynamic privacy management and interactive display functionalities for self-driving cars.

- Predictive maintenance: AI analyzing smart glass performance to anticipate maintenance requirements and optimize durability.

- Real-time glare reduction: AI instantly adjusting glass opaqueness to mitigate sudden glare from headlights or sun.

Key Takeaways Smart Glass in Automotive Market Size & Forecast

The Smart Glass in Automotive market is poised for robust expansion, driven primarily by an escalating demand for enhanced occupant comfort, safety, and personalized driving experiences. The significant projected CAGR reflects a strong industry commitment to integrating advanced technologies into vehicle design, extending beyond luxury segments into mainstream models. This growth is underpinned by continuous innovations in material science, leading to more versatile and cost-effective smart glass solutions, making them increasingly accessible and appealing to a broader consumer base.

A crucial takeaway is the transformative potential of smart glass in reshaping the automotive interior. Beyond basic light control, these intelligent surfaces are evolving into dynamic interfaces capable of displaying information, providing real-time privacy, and contributing to vehicle energy efficiency. This multi-functional aspect positions smart glass as a pivotal component in the development of future-ready vehicles, including electric and autonomous models, where interior versatility and energy management are paramount considerations for manufacturers and consumers alike.

Furthermore, the market's trajectory indicates a strong correlation with the automotive industry's broader shift towards digitalization and connectivity. As vehicles become more integrated with digital ecosystems, smart glass will play a vital role in creating seamless user experiences, from intuitive controls to personalized content delivery. Investment in research and development, alongside strategic partnerships across the automotive, electronics, and material science sectors, will be instrumental in overcoming existing challenges and fully capitalizing on the immense opportunities within this evolving market.

- Strong projected CAGR signifies significant market growth and adoption over the forecast period.

- Primary drivers include increasing demand for occupant comfort, safety, and personalized in-cabin experiences.

- Technological advancements in material science are expanding the application and affordability of smart glass.

- Smart glass is evolving into a multi-functional component for information display, privacy, and energy efficiency.

- Critical for future vehicle design, especially in electric and autonomous vehicles, due to interior versatility and energy management.

- Market growth is closely tied to the automotive industry's broader digitalization and connectivity trends.

- Continued R&D and strategic collaborations are essential for unlocking full market potential.

Smart Glass in Automotive Market Drivers Analysis

The expansion of the Smart Glass in Automotive market is significantly propelled by several key factors. One major driver is the escalating consumer demand for enhanced vehicle comfort and luxury features. As consumers seek more sophisticated and personalized automotive experiences, the ability to control light, glare, and privacy with a touch of a button or automatically appeals strongly to the premium and luxury segments, subsequently trickling down to mid-range vehicles as the technology matures and becomes more accessible. This desire for superior in-cabin environments directly fuels the adoption of smart glass solutions that offer dynamic control over light and thermal comfort.

Another significant driver is the increasing integration of advanced driver-assistance systems (ADAS) and the progression towards autonomous vehicles. Smart glass, particularly in windshields, offers a unique platform for projecting augmented reality information, navigation details, and safety alerts directly into the driver's field of vision, thereby reducing distraction and enhancing safety. In autonomous vehicles, smart glass will be critical for dynamic privacy management, transforming windows into interactive displays for passengers, and adapting to various scenarios whether for entertainment, work, or rest.

Furthermore, stringent automotive regulations concerning energy efficiency and CO2 emissions, especially in regions like Europe and North America, are driving manufacturers to adopt innovative solutions for thermal management. Smart glass effectively reduces solar heat gain, lessening the reliance on air conditioning and thereby contributing to fuel efficiency in internal combustion engine vehicles and extended range in electric vehicles. This regulatory push, combined with a growing environmental consciousness among consumers, provides a strong impetus for the adoption of energy-saving smart glass technologies across the automotive industry.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Vehicle Comfort & Luxury | +4.2% | Global, particularly North America, Europe, Asia Pacific (China) | Short to Medium Term (2025-2029) |

| Integration with ADAS & Autonomous Driving | +3.8% | North America, Europe, Asia Pacific (Japan, South Korea, China) | Medium to Long Term (2027-2033) |

| Emphasis on Vehicle Energy Efficiency & Sustainability | +3.5% | Europe, North America, Asia Pacific (China, India) | Short to Medium Term (2025-2030) |

| Advancements in Smart Glass Technology & Materials | +2.9% | Global | Short to Medium Term (2025-2030) |

| Rising Disposable Income & Vehicle Sales in Emerging Economies | +2.5% | Asia Pacific (India, Southeast Asia), Latin America | Medium to Long Term (2028-2033) |

Smart Glass in Automotive Market Restraints Analysis

Despite the promising growth trajectory, the Smart Glass in Automotive market faces several significant restraints that could impede its widespread adoption. The primary restraint is the relatively high manufacturing cost associated with smart glass technologies, such as electrochromic, suspended particle device (SPD), and polymer dispersed liquid crystal (PDLC) films. These complex multi-layered structures, coupled with specialized fabrication processes, result in a significantly higher price point compared to traditional automotive glass. This cost premium limits their application primarily to high-end and luxury vehicle segments, hindering mass-market penetration and slowing the overall market's expansion.

Another critical restraint is the technical complexity involved in integrating smart glass systems into the existing automotive manufacturing infrastructure. Integrating these electronic components requires precise wiring, control units, and software interfaces that must seamlessly communicate with other vehicle systems. This complexity can lead to higher development costs for automakers, potential challenges in assembly line modifications, and concerns regarding long-term reliability and durability in harsh automotive environments, including exposure to extreme temperatures, vibrations, and continuous usage cycles. Ensuring robust performance and longevity remains a key challenge for manufacturers.

Furthermore, limited consumer awareness and initial skepticism about the practical benefits and durability of smart glass present another hurdle. While early adopters in the luxury segment may be keen, the broader consumer base often prioritizes cost-effectiveness and proven reliability. Educating consumers about the benefits of improved thermal comfort, privacy, and aesthetic appeal, while assuring them of the long-term performance and safety of these advanced glass systems, is crucial for overcoming this restraint. Without a clear value proposition that justifies the increased cost, mainstream adoption will remain slow, impacting market growth forecasts.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs of Smart Glass | -3.5% | Global | Short to Medium Term (2025-2029) |

| Complexity of Integration & Durability Concerns | -3.0% | Global | Short to Medium Term (2025-2030) |

| Limited Consumer Awareness & Market Acceptance | -2.2% | Emerging Markets, Mass Market Segments | Short Term (2025-2027) |

| Power Consumption Requirements | -1.8% | Global, particularly for Electric Vehicles | Short to Medium Term (2025-2028) |

Smart Glass in Automotive Market Opportunities Analysis

The Smart Glass in Automotive market presents significant opportunities for growth, primarily fueled by the accelerating shift towards electric vehicles (EVs) and autonomous driving. As EVs become more prevalent, the emphasis on maximizing battery range and energy efficiency intensifies. Smart glass, by intelligently managing solar heat gain, can significantly reduce the energy consumption of climate control systems, thereby extending EV range. This inherent energy-saving capability positions smart glass as a highly attractive feature for EV manufacturers and consumers, opening up a vast new market segment that prioritizes efficiency and sustainability.

Another burgeoning opportunity lies in the development of augmented reality (AR) windshields and interactive cabin displays. As vehicle interiors evolve into multi-functional living or working spaces, smart glass can serve as dynamic surfaces for projecting navigation, entertainment, or connectivity features, transforming the driving experience. This capability extends beyond the windshield to side windows and panoramic roofs, offering personalized content and interactive interfaces for all occupants. The continuous advancements in display technology and sensor integration present a fertile ground for innovating new applications and enhancing user engagement within the vehicle cabin.

Furthermore, emerging markets, particularly in Asia Pacific and Latin America, offer substantial untapped potential for smart glass adoption. As disposable incomes rise and consumer preferences for advanced vehicle features grow in these regions, the demand for luxury and technology-rich vehicles is expected to surge. Manufacturers who can scale production and develop more cost-effective smart glass solutions tailored for these markets will find immense opportunities for expansion. Strategic partnerships with local automotive players and investments in regional manufacturing capabilities will be key to capitalizing on these evolving market dynamics and driving widespread adoption beyond established markets.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion in Electric Vehicle (EV) Segment | +4.5% | Global, especially Europe, China, North America | Medium to Long Term (2027-2033) |

| Augmented Reality Windshields & Interactive Displays | +4.0% | North America, Europe, Asia Pacific (Japan, South Korea) | Long Term (2029-2033) |

| Untapped Potential in Emerging Automotive Markets | +3.5% | Asia Pacific (India, Southeast Asia), Latin America, MEA | Medium Term (2026-2032) |

| Development of Cost-Effective and Scalable Solutions | +3.0% | Global | Short to Medium Term (2025-2030) |

Smart Glass in Automotive Market Challenges Impact Analysis

The Smart Glass in Automotive market faces several pertinent challenges that could influence its growth trajectory. One significant challenge revolves around the durability and long-term reliability of smart glass components in the harsh automotive environment. Unlike static glass, smart glass contains sensitive electronic layers and materials that must withstand extreme temperature fluctuations, constant vibrations, UV radiation, and mechanical stresses over the vehicle's lifespan. Ensuring the longevity and consistent performance of these dynamic properties without degradation is a complex engineering task that requires rigorous testing and material advancements, presenting a hurdle for widespread adoption and customer confidence.

Another notable challenge is the complexity of integrating smart glass into existing vehicle electrical systems and manufacturing processes. Smart glass requires dedicated power management, control units, and intricate wiring that must be seamlessly incorporated during vehicle assembly. This not only adds to the complexity of the vehicle's electrical architecture but also demands retooling and adaptation of manufacturing lines, leading to increased production costs and potential delays. Standardizing communication protocols and interfaces across different automotive platforms and smart glass technologies is crucial for streamlining this integration, but remains an ongoing industry effort.

Furthermore, competition from established and evolving traditional automotive glass solutions, coupled with the high research and development (R&D) costs for smart glass, poses a considerable challenge. While smart glass offers unique functionalities, its premium price point compared to conventional glass requires a compelling value proposition to justify the investment for both automakers and consumers. The continuous need for significant R&D expenditures to enhance performance, reduce costs, and develop new applications can strain manufacturers' resources, potentially slowing down innovation and market penetration, especially for mass-market vehicles where cost-sensitivity is high.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Durability & Reliability in Harsh Automotive Environments | -2.8% | Global | Short to Medium Term (2025-2029) |

| Complex Integration into Vehicle Systems & Manufacturing | -2.5% | Global | Short to Medium Term (2025-2030) |

| High R&D Costs & Competitive Landscape | -2.0% | Global | Short Term (2025-2027) |

| Regulatory Hurdles & Standardization Issues | -1.5% | Europe, North America, Asia Pacific | Medium Term (2026-2031) |

Smart Glass in Automotive Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Smart Glass in Automotive market, covering market size estimations, growth forecasts, key trends, drivers, restraints, opportunities, and challenges influencing its trajectory from 2025 to 2033. It offers a detailed segmentation analysis across various technologies, applications, and vehicle types, complemented by regional insights to provide a holistic view of the market landscape. The report also profiles leading market players, offering strategic insights into their competitive positioning and recent developments.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 billion |

| Market Forecast in 2033 | USD 7.50 billion |

| Growth Rate | 19.5% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Saint-Gobain S.A., Gentex Corporation, AGC Inc., Pilkington Group Limited, Corning Incorporated, RavenWindow, Research Frontiers Inc., Pleotint LLC, Polytronix, Inc., Gauzy Ltd., Kinestral Technologies, Inc., Scienstry Inc., Vision Systems, SPD Control Systems, Inc., Glass Apps, Variotec GmbH, Smartglass International, Switchlite, L’Oréal, e-Chromic. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Smart Glass in Automotive market is meticulously segmented to provide a granular understanding of its diverse landscape, reflecting the various technologies, applications, and vehicle types driving its evolution. This segmentation highlights the specific niches and growth areas within the broader market, allowing for targeted strategic planning and investment. The market's technological diversity, ranging from electrochromic to SPD and PDLC, caters to different performance requirements and cost points, influencing adoption rates across various automotive segments.

Application-wise, smart glass is expanding beyond luxury sunroofs to encompass critical areas like windows, windshields, and mirrors, each offering unique benefits such as enhanced privacy, improved visibility, and integrated display functionalities. The adoption of these solutions varies significantly by vehicle type, with passenger vehicles, particularly premium and electric models, being early adopters. However, commercial vehicles are also increasingly exploring smart glass for practical applications like driver comfort and efficiency, broadening the market's potential reach.

Understanding these segments is crucial for stakeholders to identify key market drivers and restraints pertinent to specific product types or vehicle categories. For instance, while cost remains a barrier for mass-market adoption of advanced smart glass in passenger vehicles, the long-term energy savings and enhanced safety features might justify the investment in fleet-based commercial vehicles or high-end electric models. This detailed segmentation analysis provides a roadmap for innovation and market penetration strategies, ensuring that products are tailored to meet the specific needs and expectations of each sub-market.

- By Technology:

- Electrochromic: Known for gradual tinting, widely used in rearview mirrors and sunroofs for glare reduction and privacy.

- Suspended Particle Device (SPD): Offers instant switching between clear and opaque states, ideal for privacy windows and dynamic sun control.

- Polymer Dispersed Liquid Crystal (PDLC): Provides privacy and projection capabilities, often used for interior partitions or specific window applications.

- Thermotropic: Responds to temperature changes, offering passive thermal control.

- Photochromic: Changes tint based on UV light intensity, typically used in eyewear but has niche automotive applications.

- Others: Includes emerging technologies like micro-shutter and active-light control systems.

- By Application:

- Sunroofs: Offers dynamic light and heat control, enhancing comfort and aesthetic appeal.

- Windows (Side & Rear): Provides instant privacy, glare reduction, and improved thermal insulation.

- Windshields: Potential for augmented reality displays, glare control, and advanced safety features.

- Rearview Mirrors: Automatic dimming for glare reduction from headlights.

- Others: Includes interior partitions for privacy in luxury or autonomous vehicles, and head-up display components.

- By Vehicle Type:

- Passenger Vehicles: Largest segment, driven by luxury, comfort, and technological advancements.

- Hatchback

- Sedan

- SUV

- Commercial Vehicles: Growing adoption for driver comfort, energy efficiency, and operational benefits.

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

- Electric Vehicles (EVs): Critical for extending range through energy-efficient climate control and enhancing the futuristic appeal.

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Fuel Cell Electric Vehicles (FCEV)

- Passenger Vehicles: Largest segment, driven by luxury, comfort, and technological advancements.

Regional Highlights

- North America: This region is a significant market for smart glass in automotive, characterized by a strong presence of luxury and performance vehicle manufacturers, coupled with high consumer disposable income and a penchant for advanced automotive technologies. The demand for enhanced comfort, privacy, and the early adoption of autonomous driving features drive market growth here. Regulatory support for energy-efficient solutions also contributes to the market's expansion.

- Europe: A leading region in automotive innovation, Europe demonstrates robust adoption of smart glass due to stringent environmental regulations promoting energy efficiency and the strong market for premium and electric vehicles. Consumers in this region prioritize vehicle safety, comfort, and sustainable technologies, making smart glass solutions highly appealing. Germany, France, and the UK are key contributors to market revenue.

- Asia Pacific (APAC): Expected to be the fastest-growing market, primarily driven by the expanding automotive manufacturing base in countries like China, Japan, South Korea, and India. Rapid urbanization, increasing disposable incomes, and the growing demand for technologically advanced and luxury vehicles are fueling the adoption of smart glass. Government initiatives supporting electric vehicles and smart city infrastructure also create favorable conditions for market expansion.

- Latin America: This region presents emerging opportunities for smart glass in automotive, albeit at a slower pace compared to developed regions. Growth is primarily driven by increasing vehicle production, a rising middle class, and growing awareness of advanced vehicle features. Economic stability and foreign investments in the automotive sector will further stimulate market penetration.

- Middle East and Africa (MEA): The MEA region is witnessing gradual adoption, particularly in countries with significant luxury vehicle imports and increasing investment in smart infrastructure projects. Extreme climatic conditions in parts of the MEA also create a strong demand for smart glass that can offer superior thermal control, improving passenger comfort and reducing the strain on air conditioning systems.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Smart Glass in Automotive Market.- Saint-Gobain S.A.

- Gentex Corporation

- AGC Inc.

- Pilkington Group Limited

- Corning Incorporated

- RavenWindow

- Research Frontiers Inc.

- Pleotint LLC

- Polytronix, Inc.

- Gauzy Ltd.

- Kinestral Technologies, Inc.

- Scienstry Inc.

- Vision Systems

- SPD Control Systems, Inc.

- Glass Apps

- Variotec GmbH

- Smartglass International

- Switchlite

- L’Oréal

- e-Chromic

Frequently Asked Questions

Analyze common user questions about the Smart Glass in Automotive market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is smart glass in automotive applications?

Smart glass in automotive refers to specialized glass that can dynamically change its properties, such as transparency, opacity, or tint, in response to external stimuli like electricity, light, or temperature. It's used in vehicles for sunroofs, windows, and windshields to enhance privacy, reduce glare, improve thermal comfort, and potentially display information, significantly upgrading the in-cabin experience.

How does smart glass benefit vehicle occupants?

Smart glass offers numerous benefits to vehicle occupants, including enhanced privacy on demand, instant glare reduction for improved visibility and safety, superior thermal regulation to maintain comfortable cabin temperatures, and potential integration with augmented reality for interactive displays. These features contribute to a more comfortable, secure, and technologically advanced driving and riding experience.

What are the primary technologies used in automotive smart glass?

The primary technologies employed in automotive smart glass include Electrochromic (EC), Suspended Particle Device (SPD), and Polymer Dispersed Liquid Crystal (PDLC). Electrochromic glass changes tint gradually with an electrical current; SPD offers instant switching between clear and opaque states by aligning microscopic particles; and PDLC glass allows for privacy or can be used as a projection screen when a voltage is applied, scattering or aligning liquid crystals.

Is smart glass energy efficient in cars?

Yes, smart glass can significantly contribute to vehicle energy efficiency. By dynamically controlling solar heat gain, it reduces the need for constant air conditioning, thereby decreasing fuel consumption in internal combustion engine vehicles and extending the battery range in electric vehicles. This thermal management capability makes smart glass an increasingly vital component for eco-friendly and sustainable automotive design.

What is the future outlook for smart glass in autonomous vehicles?

For autonomous vehicles, smart glass is expected to play a transformative role, converting the cabin into a versatile living or working space. It will facilitate dynamic privacy settings, transforming windows into interactive displays for entertainment or virtual meetings, and integrate with AI to adapt the environment to occupant preferences. The technology is crucial for enhancing comfort, entertainment, and functionality in the self-driving future.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted