Small lift Launch Vehicle Market

Small lift Launch Vehicle Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705716 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

Small lift Launch Vehicle Market Size

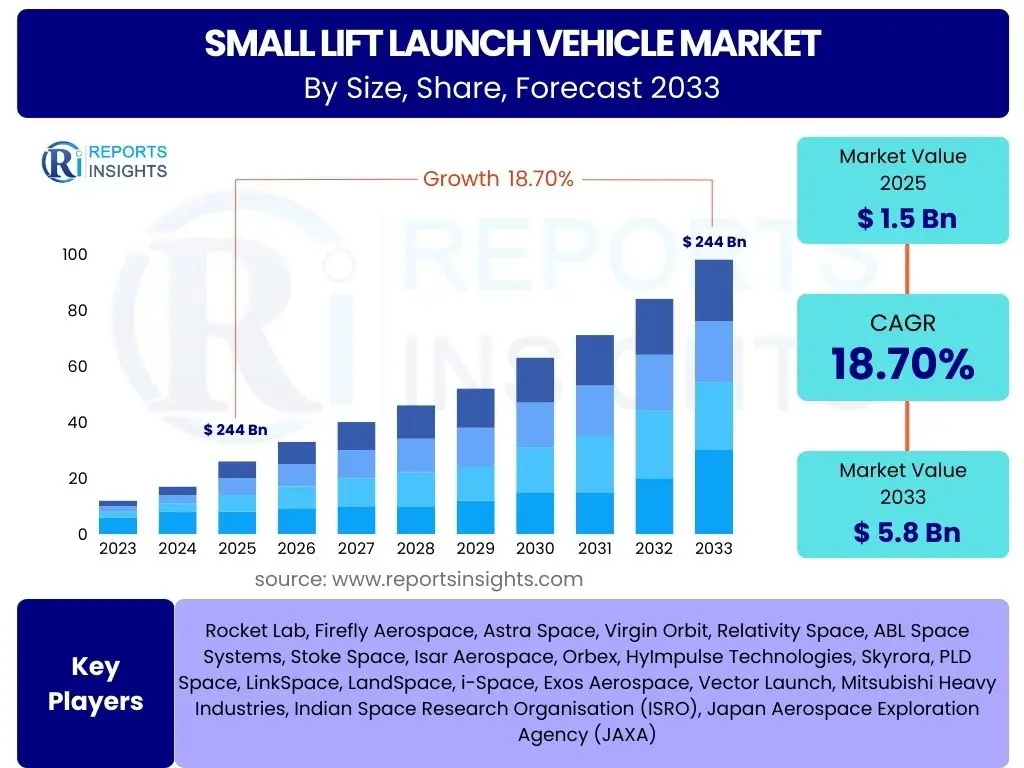

According to Reports Insights Consulting Pvt Ltd, The Small lift Launch Vehicle Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.7% between 2025 and 2033. The market is estimated at USD 1.5 billion in 2025 and is projected to reach USD 5.8 billion by the end of the forecast period in 2033.

Key Small lift Launch Vehicle Market Trends & Insights

The Small lift Launch Vehicle market is undergoing significant transformation, driven by a convergence of technological advancements, evolving commercial demands, and strategic governmental initiatives. User inquiries frequently center on the innovative approaches companies are adopting to enhance launch efficiency, reduce costs, and expand access to space for smaller payloads. Key areas of interest include the proliferation of dedicated smallsat launchers, the increasing adoption of reusability concepts, and the integration of advanced manufacturing techniques like 3D printing, all of which are fundamentally reshaping market dynamics and competitive landscapes.

A notable trend is the shift from rideshare opportunities on larger vehicles to dedicated small-lift launches. This provides small satellite operators with greater flexibility in terms of launch timing, orbital parameters, and mission specific requirements, which is crucial for the rapid deployment of burgeoning satellite constellations. Furthermore, the market is seeing a diversification of launch platforms, including air-launch and sea-launch systems, aimed at improving launch responsiveness and geographical reach, thereby mitigating dependency on traditional fixed launch sites. These innovations directly address the user need for more agile and adaptable space access solutions.

- Proliferation of dedicated small satellite launch services for enhanced mission flexibility.

- Increasing adoption of reusable rocket technologies to reduce per-launch costs and accelerate turnaround times.

- Development and integration of additive manufacturing (3D printing) for rapid prototyping and cost-effective production of rocket components.

- Emergence of diverse launch platforms, including air-launch, sea-launch, and mobile ground systems, to improve launch responsiveness.

- Growing demand for rapidly deployable satellite constellations for global connectivity and Earth observation.

- Emphasis on green propulsion technologies and sustainable launch practices to address environmental concerns.

- Standardization of payload interfaces and integration processes to streamline satellite deployment.

AI Impact Analysis on Small lift Launch Vehicle

Artificial Intelligence (AI) is set to profoundly impact the Small lift Launch Vehicle sector, addressing common user questions regarding efficiency, safety, and operational complexity. AI-driven solutions are being integrated across the entire launch lifecycle, from mission planning and trajectory optimization to autonomous pre-launch checks and in-flight anomaly detection. Users are keenly interested in how AI can minimize human error, automate routine processes, and significantly reduce operational costs, thereby making space access more affordable and reliable. This technological infusion promises to revolutionize how small launch missions are conceived, executed, and managed.

One primary area where AI offers transformative potential is in real-time decision-making during ascent. AI algorithms can analyze vast amounts of telemetry data instantaneously, identifying potential issues or deviations from nominal parameters and suggesting corrective actions with unprecedented speed. This capability is critical for ensuring mission success and improving safety margins. Furthermore, AI is instrumental in predictive maintenance for launch vehicle components, analyzing sensor data to anticipate failures before they occur, thus reducing downtime and enhancing reliability. The integration of machine learning into design and manufacturing processes also accelerates iteration cycles, optimizing performance and reducing development timelines for next-generation small lift vehicles.

- Optimized mission planning and trajectory calculations using AI algorithms for enhanced fuel efficiency and payload delivery accuracy.

- Autonomous pre-launch checks and intelligent diagnostics, reducing human error and accelerating launch preparations.

- Real-time anomaly detection and adaptive flight control during ascent, improving mission safety and responsiveness to unforeseen events.

- Predictive maintenance for propulsion systems and critical components, minimizing downtime and extending operational lifespans.

- AI-driven design and simulation tools accelerating the development of new, more efficient small lift vehicle architectures.

- Enhanced data analysis from post-flight telemetry for rapid identification of performance improvements and operational insights.

Key Takeaways Small lift Launch Vehicle Market Size & Forecast

The Small lift Launch Vehicle market is poised for robust expansion, reflecting a pivotal shift in the global space economy. Key takeaways for stakeholders often revolve around understanding the drivers behind this growth, the disruptive forces at play, and the evolving competitive landscape. The market's significant Compound Annual Growth Rate (CAGR) is primarily fueled by the burgeoning demand for small satellite constellations, which require frequent, dedicated, and cost-effective launch capabilities. This growth signifies a lucrative opportunity for innovative aerospace companies and investors seeking to capitalize on the increasing commercialization of space.

Furthermore, the forecast underscores a trend towards greater accessibility to space, driven by technological advancements that reduce manufacturing costs and increase launch cadence. The market is becoming increasingly diversified, with a mix of established players adapting to new demands and a surge of new entrants employing novel approaches like reusability and advanced manufacturing. Understanding these dynamics is crucial for strategic planning, including investment decisions, partnership formations, and product development roadmaps within the rapidly evolving small lift launch sector. The emphasis on agile, responsive launch services indicates a future where space access is no longer limited to large, infrequent missions.

- Significant market growth driven by escalating demand for small satellite constellations and Earth observation services.

- Cost reduction initiatives, including reusability and advanced manufacturing, are making space access more affordable.

- Increased competition among a growing number of private sector companies, fostering innovation and service diversification.

- Emergence of dedicated launch services offering greater flexibility and tailored orbital solutions for small payloads.

- North America and Asia Pacific are projected as dominant regions due to strong government support and private investments.

- Technological advancements in propulsion and materials are enabling more efficient and reliable small lift vehicles.

- Focus on rapid launch capabilities to meet the urgent deployment needs of commercial and defense applications.

Small lift Launch Vehicle Market Drivers Analysis

The Small lift Launch Vehicle market is experiencing accelerated growth primarily due to the burgeoning demand for small satellites across various applications. This demand is fueled by the miniaturization of technology, which allows for smaller, more capable satellites to perform tasks previously requiring larger spacecraft. The increasing deployment of satellite mega-constellations for global internet connectivity, Earth observation, and remote sensing further intensifies the need for frequent and cost-effective launch solutions. These constellations require a continuous cadence of launches to replenish, expand, and maintain their operational capabilities, directly driving the market for small lift vehicles.

Additionally, the "New Space" era has witnessed a significant influx of private investment and entrepreneurial ventures into the space industry, leading to increased competition and innovation. These new companies often focus on developing agile and specialized small launch capabilities to cater to the specific needs of small satellite operators, thereby reducing reliance on rideshares on larger, less flexible rockets. Government and defense sectors also contribute significantly, as they increasingly utilize small satellites for intelligence, surveillance, reconnaissance (ISR), and secure communications, demanding dedicated and rapid launch access to maintain strategic advantages.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Small Satellite Constellations | +5.5% | Global, particularly North America, Asia Pacific, Europe | Short to Mid-Term (2025-2030) |

| Technological Advancements and Miniaturization of Payloads | +4.8% | Global, with R&D hubs in US, EU, Japan | Mid to Long-Term (2027-2033) |

| Increasing Private Sector Investment in Space Startups | +4.2% | North America, Europe, emerging in Asia Pacific | Short to Mid-Term (2025-2029) |

| Demand for Responsive and Dedicated Launch Services | +3.9% | Global, critical for Defense and Commercial | Short to Mid-Term (2025-2031) |

| Government and Defense Applications of Small Satellites | +3.5% | US, China, India, Russia, Europe | Long-Term (2028-2033) |

Small lift Launch Vehicle Market Restraints Analysis

Despite the optimistic growth projections, the Small lift Launch Vehicle market faces several significant restraints that could temper its expansion. One of the primary challenges is the high capital investment required for research, development, testing, and manufacturing of launch vehicles. Building and operating launch infrastructure, coupled with the inherent complexities of aerospace engineering, demands substantial financial resources, which can be a barrier to entry for new companies and can strain the balance sheets of existing players. This capital intensity often translates into higher launch costs for end-users, potentially limiting market growth if cost efficiencies are not adequately achieved.

Another major restraint involves the stringent regulatory landscape and the complex permit processes for launch operations. Obtaining licenses for manufacturing, testing, and launching rockets involves navigating a labyrinth of national and international space laws, environmental regulations, and frequency allocation protocols. These regulatory hurdles can introduce significant delays, increase operational costs, and create uncertainty for market participants. Furthermore, the inherent technical risks associated with rocket launches, including the potential for failures, loss of payload, and the significant financial repercussions of such events, pose a constant challenge, demanding meticulous engineering and robust quality control, which adds to the overall cost and complexity.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Investment and Development Costs | -3.0% | Global, impacts startups and smaller players | Short to Mid-Term (2025-2030) |

| Stringent Regulatory Frameworks and Licensing | -2.5% | US, Europe, Asia (complex national laws) | Mid-Term (2026-2031) |

| Technical Complexities and Risk of Launch Failures | -2.0% | Global, impacts market confidence | Short to Mid-Term (2025-2029) |

| Intense Competition from Rideshare Services by Larger Vehicles | -1.8% | Global, particularly by SpaceX (Falcon 9) | Short-Term (2025-2027) |

| Supply Chain Vulnerabilities and Geopolitical Instability | -1.5% | Global, impacts component availability | Short to Mid-Term (2025-2028) |

Small lift Launch Vehicle Market Opportunities Analysis

The Small lift Launch Vehicle market is ripe with opportunities, particularly driven by emerging applications that demand agile and flexible access to space. The most significant opportunity lies in the continued growth of satellite mega-constellations, which require not just initial deployment but also continuous replenishment and expansion. This creates a sustained, long-term demand for dedicated small-lift launches capable of deploying multiple satellites into precise orbital planes efficiently. Furthermore, the development of in-orbit servicing, manufacturing, and assembly capabilities presents a nascent yet highly promising market segment. These future space operations will rely heavily on smaller, more frequent launches to transport components, tools, and potentially even raw materials to orbital facilities.

Another key opportunity lies in expanding into new geographical markets and fostering international collaborations. Many emerging space nations are looking to establish independent or semi-independent space capabilities, which often begin with smaller satellite programs and thus create demand for small lift launch services. Partnerships between private launch providers and national space agencies can unlock new funding, share technical expertise, and provide access to new launch sites. Additionally, the increasing focus on lunar and deep space exploration missions, which may involve deploying smaller scientific probes or logistical support modules, could open specialized niches for small lift vehicles capable of reaching beyond Earth orbit, diversifying their service offerings and revenue streams.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Satellite Mega-Constellations | +6.0% | Global, particularly North America, Europe, Asia Pacific | Short to Long-Term (2025-2033) |

| Emerging In-Orbit Servicing, Manufacturing, and Assembly | +5.2% | Global, key players in US, Europe, Japan | Mid to Long-Term (2028-2033) |

| Lunar and Deep Space Small Payload Missions | +4.5% | Global, driven by national space agencies | Long-Term (2030-2033) |

| Development of Sustainable and Reusable Launch Technologies | +4.0% | Global, R&D focused in US, Europe | Mid-Term (2026-2031) |

| Increased Demand from Remote Sensing and IoT Applications | +3.8% | Global, particularly developing regions | Short to Mid-Term (2025-2029) |

Small lift Launch Vehicle Market Challenges Impact Analysis

The Small lift Launch Vehicle market, while dynamic, faces several significant challenges that could impede its trajectory. One prominent challenge is the fierce competition and potential market saturation, as numerous new entrants vie for a share of the burgeoning small satellite launch market. This intense competition can lead to price wars, eroding profit margins for providers and potentially leading to consolidation or market exits for less resilient companies. Differentiating services and building a sustainable business model in a crowded market remains a critical hurdle for many participants. Ensuring consistent launch success and maintaining high reliability standards is another persistent challenge, as even a single failure can severely impact investor confidence and future contract opportunities, given the high stakes involved in space operations.

Furthermore, managing the high research, development, and production costs, even for smaller vehicles, poses a substantial financial burden. While reusability and advanced manufacturing aim to reduce costs, the initial investment for these technologies is considerable, and profitability can be elusive in the early stages. Environmental concerns, specifically related to space debris generation and the carbon footprint of rocket launches, are also emerging as significant long-term challenges. As launch cadence increases, the imperative to develop more sustainable propulsion systems and mitigate orbital debris becomes critical, potentially necessitating new regulations and costly technological adaptations for launch providers.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition and Potential Market Saturation | -2.8% | Global, particularly North America, Europe | Short to Mid-Term (2025-2029) |

| Maintaining High Reliability and Minimizing Launch Failures | -2.2% | Global, impacts customer confidence | Short to Mid-Term (2025-2030) |

| High Operational Costs and Achieving Profitability | -1.9% | Global, impacts long-term viability | Mid-Term (2027-2032) |

| Ensuring Access to Critical Components and Materials | -1.6% | Global, impacts supply chain resilience | Short-Term (2025-2027) |

| Growing Concerns over Space Debris and Environmental Impact | -1.4% | Global, regulatory pressure in future | Mid to Long-Term (2028-2033) |

Small lift Launch Vehicle Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Small lift Launch Vehicle market, encompassing its current landscape, future growth trajectories, and critical factors influencing market dynamics. It offers detailed insights into market size estimations, historical trends, and forecasts spanning from 2025 to 2033. The scope includes a meticulous examination of market drivers, restraints, opportunities, and challenges, along with an assessment of the impact of AI on the sector. Furthermore, the report delves into market segmentation by various parameters, highlights key regional developments, and profiles leading market participants to provide a holistic view for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.5 Billion |

| Market Forecast in 2033 | USD 5.8 Billion |

| Growth Rate | 18.7% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Rocket Lab, Firefly Aerospace, Astra Space, Virgin Orbit, Relativity Space, ABL Space Systems, Stoke Space, Isar Aerospace, Orbex, HyImpulse Technologies, Skyrora, PLD Space, LinkSpace, LandSpace, i-Space, Exos Aerospace, Vector Launch, Mitsubishi Heavy Industries, Indian Space Research Organisation (ISRO), Japan Aerospace Exploration Agency (JAXA) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Small lift Launch Vehicle market is intricately segmented to reflect the diverse requirements of the global space industry and the varied capabilities of launch service providers. Understanding these segments is crucial for identifying specific market niches, tailoring service offerings, and developing targeted growth strategies. Segmentation typically encompasses factors such as payload capacity, which dictates the size and type of satellites a vehicle can carry; the intended orbit type, ranging from low Earth orbits for communication constellations to sun-synchronous orbits for Earth observation; and the primary end-users, differentiating between commercial enterprises, governmental agencies, and academic institutions.

Further segmentation considers the propulsion technology employed, including established liquid and solid propellants, as well as emerging hybrid and electric propulsion systems that promise greater efficiency or environmental benefits. The method of launch, whether from traditional ground sites, air-launched from carrier aircraft, or sea-launched from maritime platforms, also creates distinct segments with unique operational advantages and geographical flexibilities. This granular segmentation allows for a precise analysis of market demand and supply dynamics across the rapidly evolving small satellite ecosystem, enabling stakeholders to navigate the complexities of this competitive landscape effectively.

- By Payload Capacity: This segment categorizes small lift vehicles based on the maximum weight they can transport to orbit.

- Micro-payload (1-10 kg): Catering to very small cubesats and nanosatellites.

- Nano-payload (10-100 kg): Designed for a range of small scientific or commercial satellites.

- Mini-payload (100-500 kg): Capable of launching larger smallsats for various missions.

- By Orbit Type: Defines the target orbital destination for the payloads.

- Low Earth Orbit (LEO): Dominant for communication and Earth observation constellations.

- Sun-Synchronous Orbit (SSO): Ideal for imaging and weather satellites requiring consistent lighting conditions.

- Medium Earth Orbit (MEO): Used for navigation and some communication satellites.

- Geostationary Transfer Orbit (GTO): Less common for small lift, but an emerging niche for micro-GEOs.

- By End-User: Identifies the primary customers for launch services.

- Commercial: Includes telecommunications, Earth observation, and remote sensing companies.

- Government & Defense: Encompasses military, intelligence, and national space agency missions.

- Academic & Research: Universities and research institutions for scientific experiments and technology demonstrations.

- By Propulsion Type: Categorizes vehicles based on their primary engine technology.

- Liquid Propulsion: Offers high thrust and throttleability, widely used.

- Solid Propulsion: Simpler design, often used for boosters or smaller stages.

- Hybrid Propulsion: Combines solid and liquid elements, offering some benefits of both.

- Electric Propulsion: Emerging for in-space maneuvering or very small, highly efficient concepts.

- By Launch Type: Specifies the method and location of vehicle launch.

- Ground Launch: Traditional method from fixed launch sites.

- Air Launch: Rockets launched from high-altitude aircraft, offering flexibility.

- Sea Launch: Launches from mobile ocean platforms, enabling equatorial launches.

Regional Highlights

The Small lift Launch Vehicle market exhibits distinct regional dynamics, influenced by varying levels of government support, private sector investment, technological capabilities, and demand for space-based services. Each major region contributes uniquely to the market's growth and competitive landscape, reflecting localized strategic priorities and commercial interests.

- North America: This region is a dominant force in the global Small lift Launch Vehicle market, primarily driven by the United States. It benefits from a robust ecosystem of private space companies, significant venture capital investment, and strong government backing for both commercial and defense space initiatives. Key players like Rocket Lab, Firefly Aerospace, and Relativity Space originate from this region, pioneering innovations in reusability, rapid production, and diverse launch capabilities. The demand for satellite constellations, responsive launch for defense, and advanced space technology development further solidifies North America's leading position.

- Europe: Europe represents a strong and growing market for small lift launch vehicles, propelled by national space agencies and a burgeoning private sector. Countries such as the UK, France, Germany, and Spain are actively fostering their domestic launch capabilities to secure independent access to space. Initiatives from the European Space Agency (ESA) and national programs support the development of companies like Isar Aerospace, Orbex, and PLD Space. The region's focus on scientific missions, Earth observation, and European-led constellations contributes significantly to market demand.

- Asia Pacific (APAC): The APAC region is experiencing rapid growth in the small lift launch vehicle market, with countries like China, India, and Japan at the forefront. China's state-backed and increasingly private space industry is developing numerous small launch vehicles, alongside its ambitious constellation plans. India's ISRO is a key player with its PSLV and SSLV programs, offering cost-effective launch solutions. Japan's JAXA and private firms are also investing in this segment. South Korea and Australia are emerging players, indicating a region-wide push for space independence and commercial exploitation of space. The immense demand for connectivity, disaster monitoring, and defense applications fuels this regional expansion.

- Latin America: While nascent, the Latin American market for small lift launch vehicles is showing increasing interest, driven by national space programs and the need for localized satellite services. Countries such as Brazil and Argentina are investing in their aerospace capabilities, seeking to leverage small satellites for remote sensing, agriculture, and communications. The market here is primarily characterized by partnerships with international launch providers and the development of foundational space infrastructure.

- Middle East and Africa (MEA): The MEA region is an emerging market for small lift launch vehicles, driven by countries like the UAE, Saudi Arabia, and South Africa seeking to diversify their economies and build indigenous space capabilities. Investment in space technology for defense, resource management, and telecommunications is growing. While not yet hosting major indigenous launch providers, the region is a potential future customer for international small lift services and may see the development of launch infrastructure through collaborations.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Small lift Launch Vehicle Market.- Rocket Lab

- Firefly Aerospace

- Astra Space

- Virgin Orbit

- Relativity Space

- ABL Space Systems

- Stoke Space

- Isar Aerospace

- Orbex

- HyImpulse Technologies

- Skyrora

- PLD Space

- LinkSpace

- LandSpace

- i-Space

- Exos Aerospace

- Vector Launch

- Mitsubishi Heavy Industries

- Indian Space Research Organisation (ISRO)

- Japan Aerospace Exploration Agency (JAXA)

Frequently Asked Questions

What is a small lift launch vehicle?

A small lift launch vehicle is a type of rocket designed to carry small payloads, typically weighing between 10 kg and 500 kg, into various Earth orbits. These vehicles offer dedicated and flexible launch options, contrasting with rideshare services on larger rockets, catering specifically to the growing small satellite market.

Why is demand for small lift launch vehicles increasing?

The demand is surging due to the rapid proliferation of small satellite constellations for global internet, Earth observation, and remote sensing. These constellations require frequent, dedicated, and cost-effective launches, which small lift vehicles are uniquely positioned to provide, offering greater orbital flexibility and timely deployment compared to larger launchers.

What are the key technologies driving small lift launch vehicles?

Key technologies include advanced manufacturing (e.g., 3D printing for rapid production), reusability concepts (e.g., vertical landing, air-launch systems for quicker turnaround), and new propulsion systems (e.g., methane engines for efficiency). These innovations aim to reduce costs, enhance reliability, and increase the responsiveness of launch services.

Who are the major players in the small lift launch vehicle market?

The market is characterized by a mix of established and new entrants. Key players include private companies like Rocket Lab, Firefly Aerospace, and Relativity Space, alongside national space agencies such as ISRO and JAXA, and numerous emerging startups globally. These entities are developing diverse solutions to meet the burgeoning demand for small satellite launches.

What are the future prospects for the small lift launch vehicle market?

The future prospects are highly positive, driven by sustained demand from mega-constellations, emerging in-orbit services, and specialized lunar/deep space missions for small payloads. Continued innovation in reusability and cost reduction, alongside expanding regional access to space, is expected to fuel significant market growth and diversification through 2033 and beyond.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted