Armoured Vehicle Market

Armoured Vehicle Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705968 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

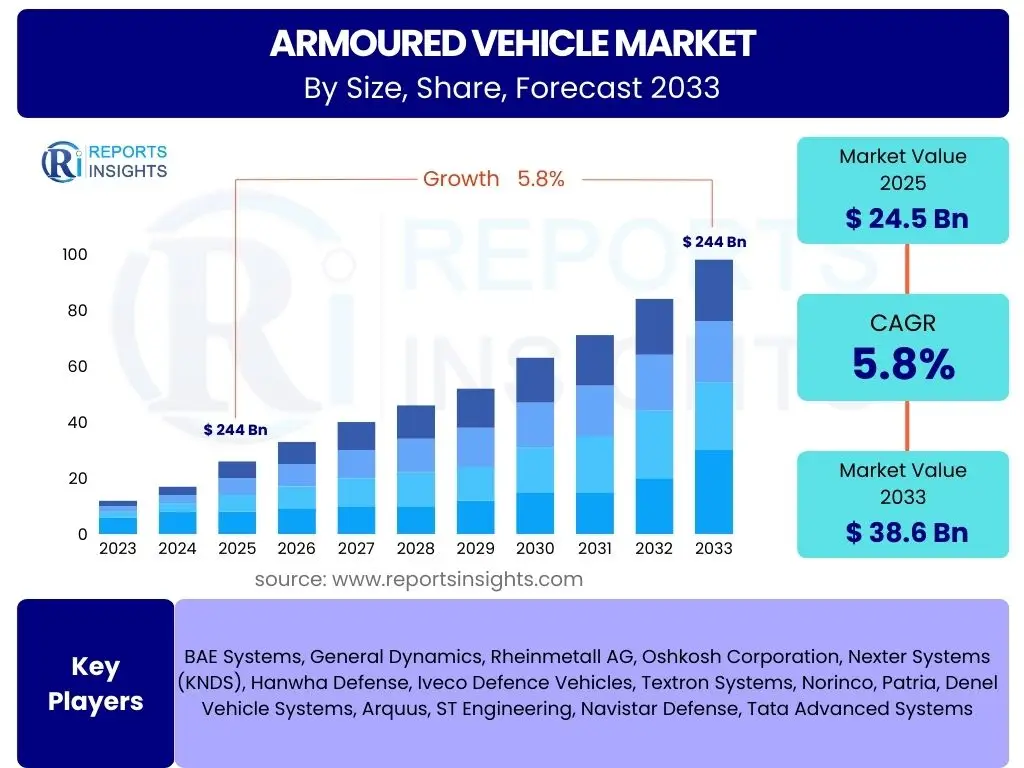

Armoured Vehicle Market Size

According to Reports Insights Consulting Pvt Ltd, The Armoured Vehicle Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 24.5 Billion in 2025 and is projected to reach USD 38.6 Billion by the end of the forecast period in 2033.

Key Armoured Vehicle Market Trends & Insights

The Armoured Vehicle market is undergoing significant transformation, driven by evolving geopolitical landscapes, advancements in defense technologies, and the changing nature of modern warfare. Users frequently inquire about the shift towards modular, lightweight, and highly adaptable vehicle platforms capable of operating in diverse environments, from urban combat to expeditionary operations. There is a strong emphasis on enhanced survivability through advanced armor solutions, active protection systems, and signature management technologies.

Another prominent area of interest concerns the integration of advanced C4ISR (Command, Control, Communications, Computers, Intelligence, Surveillance, and Reconnaissance) systems, enabling greater situational awareness, networked operations, and interoperability across forces. The demand for unmanned and optionally manned ground vehicles (UGVs/OMAVs) is also emerging as a key trend, promising to reduce soldier exposure to risk and expand operational capabilities. Furthermore, sustainable propulsion systems, including hybrid and electric powertrains, are gaining traction due to environmental considerations and operational advantages.

- Emphasis on modularity and adaptability for multi-mission capabilities.

- Integration of advanced C4ISR systems for superior situational awareness.

- Development and adoption of active protection systems (APS) for enhanced survivability.

- Increasing demand for unmanned and optionally manned ground vehicles (UGVs/OMAVs).

- Focus on lightweight materials and advanced armor solutions to improve mobility and protection.

- Shift towards hybrid and electric propulsion systems for operational efficiency and environmental compliance.

- Growth in demand for specialized vehicles for asymmetric warfare and urban combat scenarios.

AI Impact Analysis on Armoured Vehicle

User inquiries regarding AI's impact on armoured vehicles primarily revolve around enhancing operational effectiveness, reducing human cognitive load, and enabling new tactical possibilities. Artificial intelligence is expected to revolutionize various aspects, from autonomous navigation and advanced targeting systems to predictive maintenance and integrated decision support. The ability of AI to process vast amounts of sensor data in real-time will significantly improve threat detection, classification, and response capabilities, making vehicles more lethal and survivable.

Moreover, AI will play a critical role in developing true autonomous capabilities for future armoured vehicles, allowing for unmanned reconnaissance, logistics, and even combat missions, thereby minimizing risks to human personnel. Concerns also arise regarding the ethical implications of AI in lethal autonomous weapons systems and the cybersecurity vulnerabilities associated with highly networked, AI-driven platforms. Despite these concerns, the long-term trend points towards deep integration of AI for superior battlefield performance, including swarming capabilities and enhanced human-machine teaming.

- Enhanced autonomous navigation and pathfinding for unmanned and optionally manned vehicles.

- Improved target acquisition, identification, and tracking through AI-powered sensors and algorithms.

- Predictive maintenance and diagnostics for increased vehicle readiness and reduced downtime.

- Advanced decision support systems for commanders, integrating battlefield data and proposing optimal courses of action.

- Development of intelligent threat detection and countermeasure systems, including AI-driven Active Protection Systems (APS).

- Facilitation of human-machine teaming, allowing crews to offload routine or high-risk tasks to AI systems.

- Potential for robotic swarming and coordinated unmanned operations in complex environments.

Key Takeaways Armoured Vehicle Market Size & Forecast

The Armoured Vehicle market is poised for consistent growth, primarily driven by escalating geopolitical tensions, ongoing military modernization programs across various nations, and the imperative to replace aging fleets. Key takeaways highlight a sustained increase in defense spending, particularly in regions experiencing heightened security concerns, which directly translates into demand for advanced armoured platforms. The forecast underscores a strategic shift towards acquiring vehicles equipped with cutting-edge technologies that offer superior protection, mobility, and offensive capabilities.

Furthermore, the market's trajectory is heavily influenced by the adoption of digital battlefield integration, networked capabilities, and the growing emphasis on multi-role vehicles that can adapt to different mission profiles. The long-term outlook suggests a strong focus on research and development into next-generation systems, including unmanned capabilities and AI integration, which will be critical for maintaining a competitive edge and addressing future threats. The market's resilience is tied to governmental defense policies and the continuous evolution of combat doctrines.

- Market growth fueled by global security instability and defense budget increases.

- Significant investment in modernization and replacement of legacy armoured vehicle fleets.

- Strong emphasis on technological advancements for enhanced protection, firepower, and mobility.

- Increasing adoption of digital and networked capabilities for integrated battlefield operations.

- Emerging demand for unmanned and optionally manned armoured solutions to reduce combat risks.

Armoured Vehicle Market Drivers Analysis

The Armoured Vehicle market is significantly driven by a confluence of factors, primarily global geopolitical instability and the resulting surge in defense expenditures. Nations worldwide are increasingly investing in modernizing their military capabilities to counter evolving threats, ranging from state-sponsored aggression to asymmetric warfare and terrorism. This modernization often involves the procurement of new-generation armoured vehicles that offer superior protection, mobility, and firepower compared to older models.

Another crucial driver is the ongoing technological advancements in materials science, active protection systems, and digital integration. These innovations are enabling the development of more resilient, lighter, and more capable vehicles, making them indispensable for contemporary combat scenarios. Additionally, the need for enhanced border security and internal stability in many countries further propels the demand for specialized armoured vehicles suited for homeland security operations and disaster relief efforts, broadening the market's application scope beyond traditional warfare.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Geopolitical Instability and Conflicts | +1.5% | Eastern Europe, Middle East, Asia Pacific | Short-term to Mid-term (2025-2029) |

| Rising Global Defense Budgets | +1.2% | North America, Europe, Asia Pacific (China, India) | Mid-term (2025-2030) |

| Military Modernization Programs | +1.0% | Globally, particularly NATO members, developing economies | Long-term (2025-2033) |

| Technological Advancements in Protection Systems | +0.8% | North America, Europe, Israel | Continuous (2025-2033) |

| Demand for Multi-Role and Modular Vehicles | +0.7% | Globally, particularly for expeditionary forces | Mid-term (2026-2031) |

| Threat of Asymmetric Warfare and Terrorism | +0.6% | Middle East, Africa, South Asia, parts of Europe | Short-term to Mid-term (2025-2028) |

| Need for Border Security and Internal Stability | +0.4% | Developing Nations, EU Border Countries | Mid-term (2027-2032) |

Armoured Vehicle Market Restraints Analysis

Despite robust drivers, the Armoured Vehicle market faces several significant restraints that can impede its growth. One primary restraint is the inherently high cost associated with the research, development, and procurement of advanced armoured platforms. These vehicles require substantial capital investment, making it challenging for nations with limited defense budgets to acquire or upgrade their fleets, often leading to prolonged procurement cycles and delayed modernization efforts.

Another considerable challenge stems from stringent export control regulations and geopolitical sensitivities. The sale and transfer of advanced military technology, including armoured vehicles, are subject to complex international treaties, domestic laws, and political considerations, which can restrict market access and limit global sales opportunities. Furthermore, increasing public scrutiny and ethical debates surrounding military spending, especially in peacetime, can lead to budget cuts or reprioritization of funds away from defense procurement, impacting market demand. Long procurement processes and the high maintenance costs associated with complex systems also act as deterrents for potential buyers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Research & Development and Procurement Costs | -1.3% | Globally, particularly developing nations | Long-term (2025-2033) |

| Stringent Export Control Regulations and Sanctions | -1.0% | Major exporting nations (US, EU), Geopolitically sensitive regions | Continuous (2025-2033) |

| Lengthy Procurement and Development Cycles | -0.8% | Globally, impacts all major programs | Long-term (2025-2033) |

| Budgetary Constraints and Economic Volatility | -0.7% | Europe (post-COVID recovery), Latin America, Africa | Mid-term (2025-2029) |

| Public Opposition to Military Spending | -0.5% | Western Europe, parts of North America | Short-term (2025-2027) |

| High Maintenance and Sustainment Costs | -0.4% | Globally, particularly for legacy fleets | Continuous (2025-2033) |

Armoured Vehicle Market Opportunities Analysis

Significant opportunities exist in the Armoured Vehicle market, primarily driven by the increasing integration of advanced technologies such as artificial intelligence, robotics, and cybersecurity. The development of unmanned ground vehicles (UGVs) and optionally manned platforms presents a burgeoning segment, allowing for operations in high-risk environments without exposing human personnel. This shift also opens avenues for specialized software and sensor integration, creating new revenue streams for technology providers.

Furthermore, the growing demand for upgrade programs and modernization of existing fleets offers substantial opportunities for manufacturers. Many countries possess aging armoured vehicle inventories that require extensive overhauls to meet modern combat requirements, including enhanced protection, improved mobility, and digital network integration. The expansion into emerging markets, particularly in Asia Pacific and the Middle East, where defense spending is on the rise and indigenous manufacturing capabilities are still developing, also represents a lucrative prospect for international suppliers seeking new export destinations. The exploration of alternative propulsion systems, such as hybrid-electric drivetrains, aligns with global sustainability goals and offers operational advantages, creating additional market niches.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Unmanned Ground Vehicles (UGVs) | +1.1% | North America, Europe, Asia Pacific (China) | Long-term (2027-2033) |

| Modernization and Upgrade Programs for Existing Fleets | +0.9% | Europe, North America, parts of Asia | Mid-term to Long-term (2026-2033) |

| Integration of AI, Robotics, and Advanced Sensors | +0.8% | Global, R&D focused countries | Continuous (2025-2033) |

| Expansion into Emerging Defense Markets | +0.7% | Asia Pacific (Southeast Asia), Middle East, Africa | Mid-term (2025-2030) |

| Demand for Specialized Vehicles for Internal Security | +0.5% | Developing Nations, Countries with high internal security threats | Short-term (2025-2028) |

| Adoption of Hybrid-Electric Propulsion Systems | +0.4% | Europe, North America | Long-term (2028-2033) |

| Growth in Maintenance, Repair, and Overhaul (MRO) Services | +0.3% | Global, linked to fleet size and age | Continuous (2025-2033) |

Armoured Vehicle Market Challenges Impact Analysis

The Armoured Vehicle market is confronted by several complex challenges that necessitate strategic responses from manufacturers and defense ministries. One significant hurdle is the escalating complexity of integrating disparate advanced technologies, such as active protection systems, advanced C4ISR suites, and unmanned capabilities, into a cohesive and reliable platform. This integration often leads to interoperability issues, cost overruns, and delays in project timelines, requiring sophisticated project management and deep technical expertise.

Another major challenge involves navigating the intricacies of global supply chains, which have become increasingly vulnerable to geopolitical events, natural disasters, and pandemics. Disruptions in the supply of critical components, raw materials, or specialized technologies can severely impact production schedules and increase costs. Furthermore, the ethical and legal frameworks surrounding the development and deployment of autonomous and AI-driven lethal systems pose significant challenges, demanding careful consideration and international consensus. Cybersecurity threats to highly networked vehicles, the imperative for continuous technological upgrades, and the persistent pressure to reduce overall vehicle weight while maintaining high protection levels further complicate the market landscape.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex System Integration and Interoperability | -0.9% | Global, particularly for multi-national programs | Continuous (2025-2033) |

| Supply Chain Disruptions and Material Shortages | -0.7% | Global, impacts all manufacturing regions | Short-term to Mid-term (2025-2028) |

| Cybersecurity Threats to Networked Vehicles | -0.6% | Global, especially for advanced systems | Continuous (2025-2033) |

| Ethical and Legal Concerns of Autonomous Systems | -0.5% | North America, Europe, International bodies | Long-term (2027-2033) |

| Maintaining Balance of Protection, Mobility, and Firepower | -0.4% | Global, fundamental design challenge | Continuous (2025-2033) |

| Recruitment and Retention of Skilled Workforce | -0.3% | North America, Europe | Mid-term (2026-2031) |

Armoured Vehicle Market - Updated Report Scope

This comprehensive report delves into the global Armoured Vehicle market, offering an in-depth analysis of its current state, historical performance, and future growth projections. It provides detailed insights into market dynamics, including key drivers, restraints, opportunities, and challenges influencing the industry. The report covers extensive market segmentation by vehicle type, mobility, application, and technology, offering a granular view of market trends and demand patterns across various categories. Furthermore, it highlights regional market performances, identifying key growth regions and countries, alongside profiling major industry players to provide a holistic understanding of the competitive landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 24.5 Billion |

| Market Forecast in 2033 | USD 38.6 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | BAE Systems, General Dynamics, Rheinmetall AG, Oshkosh Corporation, Nexter Systems (KNDS), Hanwha Defense, Iveco Defence Vehicles, Textron Systems, Norinco, Patria, Denel Vehicle Systems, Arquus, ST Engineering, Navistar Defense, Tata Advanced Systems |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Armoured Vehicle market is extensively segmented to provide a detailed understanding of its diverse components and the specific demands driving each category. This segmentation allows for a comprehensive analysis of market dynamics, identifying key growth areas, and understanding regional preferences. The primary segmentation categories include vehicle type, mobility, application, and technology, each revealing unique market characteristics and investment priorities.

By dissecting the market through these segments, stakeholders can pinpoint specific product needs, technological requirements, and strategic opportunities. For instance, the growing focus on asymmetric warfare drives demand for Mine-Resistant Ambush Protected (MRAP) vehicles, while conventional force modernization emphasizes Main Battle Tanks (MBTs) and Infantry Fighting Vehicles (IFVs). Understanding these nuanced segments is crucial for manufacturers to tailor their offerings and for defense planners to make informed procurement decisions that align with their operational doctrines and budget constraints.

- By Vehicle Type:

- Armored Personnel Carriers (APCs)

- Infantry Fighting Vehicles (IFVs)

- Main Battle Tanks (MBTs)

- Mine-Resistant Ambush Protected (MRAPs) Vehicles

- Light Armored Vehicles (LAVs)

- Armored Support Vehicles (ASVs)

- By Mobility:

- Wheeled Armored Vehicles

- Tracked Armored Vehicles

- By Application:

- Combat

- Logistics & Support

- Reconnaissance

- Command & Control

- Homeland Security

- By Technology:

- Manned Armored Vehicles

- Unmanned Armored Vehicles (UGVs)

- Optionally Manned Armored Vehicles (OMAVs)

Regional Highlights

- North America: This region dominates the Armoured Vehicle market, primarily driven by the substantial defense budget of the United States and its continuous investment in military modernization and technological superiority. The U.S. remains at the forefront of developing next-generation armoured systems, including advanced manned and unmanned platforms, active protection systems, and network-centric capabilities. Canada also contributes to regional demand through its own defense procurement programs.

- Europe: Europe represents a significant market, influenced by ongoing security challenges, NATO commitments, and efforts to replace aging Soviet-era equipment in Eastern European countries. Western European nations are focusing on developing indigenous capabilities, promoting interoperability among allied forces, and investing in advanced protection and digital integration for their armoured fleets. Countries like Germany, France, and the UK are key players in both production and procurement.

- Asia Pacific (APAC): The APAC region is projected to be the fastest-growing market, propelled by escalating geopolitical tensions, border disputes, and the rapid increase in defense spending by major economies like China and India. These countries are not only expanding their military might but also investing heavily in indigenous armoured vehicle production and sophisticated defense technologies. Other nations in Southeast Asia are also upgrading their capabilities.

- Middle East and Africa (MEA): This region experiences consistent demand for armoured vehicles due to ongoing conflicts, internal security threats, and the need for robust border protection. Countries with significant oil revenues continue to invest in modernizing their armed forces, often relying on imports from leading global manufacturers. The focus here is on vehicles offering high survivability against IEDs and asymmetric threats, as well as logistical support.

- Latin America: The Armoured Vehicle market in Latin America is relatively smaller compared to other regions, primarily driven by internal security concerns, counter-narcotics operations, and limited border disputes. While some countries are pursuing modernization programs, budget constraints often lead to a preference for cost-effective solutions, upgrades of existing fleets, or acquisition of light armored vehicles suitable for internal security roles rather than heavy combat platforms.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Armoured Vehicle Market.- BAE Systems

- General Dynamics Corporation

- Rheinmetall AG

- Oshkosh Corporation

- Nexter Systems (KNDS)

- Hanwha Defense

- Iveco Defence Vehicles

- Textron Systems

- China North Industries Corporation (Norinco)

- Patria

- Denel Vehicle Systems

- Arquus

- ST Engineering

- Navistar Defense

- Tata Advanced Systems

- Turkish Aerospace Industries (TAI)

- Krauss-Maffei Wegmann (KMW)

- Force Protection, Inc.

- Supacat (SC Group)

- GAZ Group

Frequently Asked Questions

What is the projected growth rate for the Armoured Vehicle Market?

The Armoured Vehicle Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033, reaching USD 38.6 Billion by 2033.

What are the primary drivers of the Armoured Vehicle Market?

Key drivers include increasing geopolitical instability, rising global defense budgets, ongoing military modernization programs, and technological advancements in protection systems and digital integration.

How is AI impacting the Armoured Vehicle Market?

AI is transforming the market by enabling autonomous navigation, enhancing target acquisition, improving predictive maintenance, and facilitating advanced decision support systems for future vehicle operations.

Which region holds the largest share in the Armoured Vehicle Market?

North America currently holds the largest market share, driven by significant defense spending and continuous technological advancements, particularly in the United States.

What are the key types of armoured vehicles covered in the market?

The market includes various types such as Armored Personnel Carriers (APCs), Infantry Fighting Vehicles (IFVs), Main Battle Tanks (MBTs), Mine-Resistant Ambush Protected (MRAPs) vehicles, and Light Armored Vehicles (LAVs).

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted