SLI Battery Market

SLI Battery Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705786 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

SLI Battery Market Size

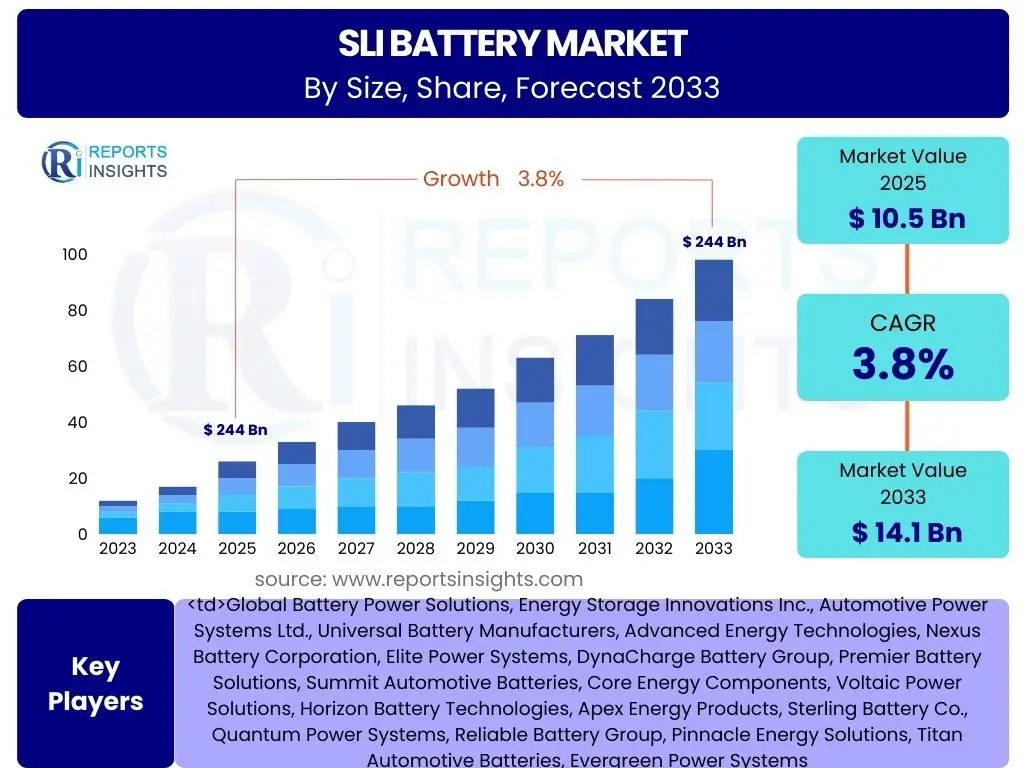

According to Reports Insights Consulting Pvt Ltd, The SLI Battery Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 3.8% between 2025 and 2033. The market is estimated at USD 10.5 Billion in 2025 and is projected to reach USD 14.1 Billion by the end of the forecast period in 2033.

The consistent expansion of the global vehicle parc, particularly in emerging economies, serves as a fundamental driver for this growth. As the number of internal combustion engine (ICE) and mild-hybrid vehicles on the road increases, so does the demand for reliable SLI batteries for both original equipment manufacturing (OEM) and, more significantly, the aftermarket replacement segment. The relatively shorter lifespan of SLI batteries compared to vehicles themselves ensures a continuous cycle of replacement demand, underpinning the market's stability and predictable growth trajectory.

Despite the increasing focus on electric vehicles (EVs), SLI batteries remain indispensable for all vehicle types, including battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs), where they serve critical auxiliary functions such as powering vehicle electronics, lights, and emergency systems. This pervasive need, combined with ongoing technological advancements in lead-acid battery design, such as Enhanced Flooded Batteries (EFB) and Absorbent Glass Mat (AGM) technologies, is contributing to the overall market valuation. These advanced SLI battery types offer improved performance, longer life cycles, and enhanced capabilities, making them suitable for vehicles equipped with fuel-saving features like start-stop systems, thereby further boosting market penetration and value.

Key SLI Battery Market Trends & Insights

Current market discourse and user inquiries frequently highlight several transformative trends shaping the SLI Battery sector. There is significant interest in understanding how the automotive industry's shift towards electrification impacts traditional SLI demand, alongside curiosity about innovations in lead-acid battery technology that enhance efficiency and longevity. Users are also keen to grasp the influence of stringent environmental regulations on manufacturing processes and the implications of evolving consumer preferences, particularly concerning vehicle features like start-stop systems, which necessitate more robust battery solutions. The dynamics of regional market growth and the increasing prominence of the aftermarket segment for replacements are also key areas of focus for stakeholders seeking comprehensive insights into the industry's future trajectory.

- Growing Adoption of Start-Stop Vehicle Systems: This trend significantly boosts demand for advanced SLI batteries like AGM and EFB, which are designed to handle frequent engine restarts and heavier electrical loads, contributing to fuel efficiency and reduced emissions.

- Technological Advancements in Lead-Acid Batteries: Ongoing research and development are improving the energy density, lifespan, and charging capabilities of SLI batteries, making them more competitive against alternative technologies and enhancing their performance in demanding automotive applications.

- Expanding Vehicle Parc and Aftermarket Demand: The continuous increase in the global number of registered vehicles, particularly in developing economies, drives a robust replacement market for SLI batteries, ensuring a stable revenue stream for manufacturers.

- Focus on Eco-Friendly Manufacturing and Recycling: Industry players are increasingly investing in sustainable production processes and advanced recycling technologies to address environmental concerns and comply with stricter regulatory frameworks, enhancing the industry's social responsibility profile.

- Integration into Mild Hybrid Electric Vehicles (MHEVs): SLI batteries, especially advanced types, are playing a crucial role in MHEVs by supporting regenerative braking and engine assist functions, bridging the gap between conventional ICE vehicles and full electric vehicles.

AI Impact Analysis on SLI Battery

User queries regarding the intersection of artificial intelligence (AI) and the SLI Battery market often revolve around its potential to optimize manufacturing processes, enhance battery performance, and improve supply chain efficiencies. Stakeholders are particularly interested in how AI can facilitate predictive maintenance for vehicle batteries, enabling more accurate diagnostics and extending operational lifespans. Furthermore, there is curiosity about AI's role in accelerating research and development for new battery materials and designs, as well as its application in quality control to minimize defects. The overarching expectation is that AI will introduce unprecedented levels of precision, efficiency, and intelligence across the entire SLI battery value chain, from raw material sourcing to end-of-life recycling, ultimately leading to more reliable and sustainable products.

- Optimized Manufacturing Processes: AI-driven analytics can monitor and adjust production lines in real-time, reducing waste, improving consistency, and enhancing the overall efficiency of SLI battery manufacturing.

- Predictive Maintenance and Diagnostics: AI algorithms can analyze battery performance data to predict potential failures, allowing for proactive maintenance and extending the operational life of SLI batteries in vehicles.

- Enhanced Quality Control: Machine learning models can identify defects during production with greater accuracy and speed than human inspection, ensuring higher quality products reach the market.

- Supply Chain Optimization: AI can forecast demand more accurately, optimize logistics, and manage inventory levels for raw materials and finished products, leading to more resilient and cost-effective supply chains for SLI battery components.

- Accelerated R&D for Battery Materials: AI-powered simulations and data analysis can fast-track the discovery and testing of new materials and designs for SLI batteries, leading to innovations in energy density, charge cycles, and durability.

Key Takeaways SLI Battery Market Size & Forecast

The primary insights gleaned from analyzing user questions about the SLI Battery market size and forecast consistently point to a market characterized by stable and essential growth, largely insulated from the immediate, dramatic shifts of the full electric vehicle transition. Users frequently seek confirmation that traditional internal combustion engine (ICE) and mild-hybrid vehicles will continue to drive demand, particularly within the robust aftermarket segment. There is a strong emphasis on understanding the resilience of the lead-acid chemistry in the face of alternative technologies and its indispensable role across diverse vehicle platforms. The overall sentiment suggests a pragmatic view of the market, recognizing its foundational importance within the automotive ecosystem and its continued relevance for the foreseeable future, supported by technological evolution within the lead-acid domain itself.

- Stable Market Growth: The SLI battery market is projected for consistent growth, primarily driven by the expanding global vehicle parc and the essential nature of SLI batteries for all vehicle types, including mild hybrids and BEVs for auxiliary functions.

- Resilient Aftermarket Demand: The replacement market forms the backbone of SLI battery sales, ensuring sustained demand irrespective of new vehicle sales fluctuations due to the finite lifespan of batteries.

- Technological Adaptation: Continued innovation in lead-acid technologies, such as AGM and EFB, is crucial for market relevance, enabling SLI batteries to meet the demands of modern vehicles with advanced electrical systems and start-stop functionality.

- Geographic Variations: While mature markets contribute significantly to replacement demand, emerging economies, particularly in Asia Pacific, are key growth engines due to increasing vehicle ownership and production.

- Complementary to Electrification: SLI batteries remain vital for electric and hybrid vehicles for low-voltage systems and safety functions, ensuring their indispensability even as the automotive industry transitions towards full electrification.

SLI Battery Market Drivers Analysis

The SLI Battery market is fundamentally driven by the continuous expansion of the global automotive industry, particularly the production and sale of internal combustion engine (ICE) and mild-hybrid vehicles. As the vehicle parc grows across both developed and developing regions, the foundational need for reliable starting, lighting, and ignition (SLI) power remains paramount. This enduring demand extends beyond new vehicle installations to a robust and ever-present aftermarket, which represents a significant and stable revenue stream for battery manufacturers. The inherent lifespan limitations of SLI batteries necessitate periodic replacements, creating a consistent sales cycle that is largely unaffected by short-term economic fluctuations.

Moreover, the increasing adoption of fuel-saving technologies, such as start-stop systems in modern vehicles, significantly contributes to market expansion. These systems, designed to improve fuel efficiency and reduce emissions by shutting off the engine when the vehicle is stationary, place higher demands on SLI batteries, necessitating more advanced and durable types like Absorbent Glass Mat (AGM) and Enhanced Flooded Battery (EFB) technologies. The growing prevalence of these features in both passenger and commercial vehicles ensures a rising demand for higher-value, specialized SLI batteries. This technological evolution within the automotive sector directly translates into a more advanced and resilient SLI battery market.

Finally, the inherent cost-effectiveness, reliability, and established manufacturing infrastructure of lead-acid batteries continue to make them the preferred choice for SLI applications compared to alternative chemistries. Their proven performance in diverse climatic conditions, coupled with a well-developed global supply chain and widespread recycling capabilities, reinforces their dominant position. This combination of factors ensures that despite the narrative around electrification, SLI batteries maintain their critical role in the automotive ecosystem, driven by an expanding vehicle base, technological integration, and economic viability.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Vehicle Production and Sales | +0.7% | Global, particularly Asia Pacific | Long-term (2025-2033) |

| Robust Aftermarket Demand for Replacements | +0.5% | Mature Markets (North America, Europe) | Mid-term to Long-term |

| Growing Adoption of Start-Stop Vehicle Systems | +0.4% | Developed and Emerging Economies | Mid-term (2025-2029) |

| Cost-Effectiveness and Reliability of Lead-Acid Batteries | +0.3% | Global | Long-term (2025-2033) |

| Essential Role in Mild Hybrid Electric Vehicles (MHEVs) | +0.2% | Europe, North America | Mid-term to Long-term |

SLI Battery Market Restraints Analysis

The SLI Battery market faces notable restraints, primarily stemming from the increasing proliferation of alternative battery technologies, most prominently lithium-ion batteries. While lithium-ion solutions are not direct replacements for all SLI functions due to cost and technical considerations, their rising adoption in electric vehicles (EVs) and certain high-performance applications creates a perception of obsolescence for traditional lead-acid systems. This shift in the automotive industry's long-term strategic focus towards full electrification could divert investment away from lead-acid research and development, potentially limiting the pace of innovation and market competitiveness in the long run. Moreover, the higher energy density and longer cycle life of lithium-ion batteries, even if currently more expensive, pose a persistent threat to lead-acid's market share in segments where performance is prioritized over cost.

Environmental concerns and increasingly stringent regulations worldwide also act as significant restraints. Lead, the primary component of SLI batteries, is a toxic substance, and its production, use, and disposal are subject to strict environmental controls. This necessitates considerable investment in compliant manufacturing processes and comprehensive recycling programs, which can add to operational costs and complexity for manufacturers. Public awareness regarding environmental impact and the drive towards greener automotive solutions pressure the industry to innovate in sustainable practices, which, while beneficial, can slow growth or increase prices if not managed effectively.

Furthermore, the SLI battery market is susceptible to the volatility of raw material prices, particularly lead. Global supply chain disruptions, geopolitical events, and fluctuations in mining output can lead to unpredictable price swings for lead and other critical materials. These price instabilities directly impact manufacturing costs, eroding profit margins for battery producers and potentially leading to higher end-product prices, which can dampen consumer demand. Managing these external price pressures requires sophisticated hedging strategies and flexible supply chain management, adding another layer of complexity to market operations and potentially restraining overall growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Prominence of Lithium-ion Batteries in Automotive | -0.6% | Developed Markets (Europe, North America) | Long-term (2027-2033) |

| Stringent Environmental Regulations and Lead Recycling Challenges | -0.4% | Global, particularly EU and North America | Long-term (2025-2033) |

| Volatile Raw Material Prices (Lead) | -0.3% | Global | Short-term to Mid-term |

| Reduced Production of Traditional ICE Vehicles in Certain Regions | -0.2% | Europe, parts of North America | Long-term (2028-2033) |

| Technological Obsolescence Risk for Conventional SLI Types | -0.1% | Global | Mid-term to Long-term |

SLI Battery Market Opportunities Analysis

The SLI Battery market presents significant opportunities driven by continuous advancements in lead-acid battery technologies. The development and increasing adoption of Enhanced Flooded Batteries (EFB) and Absorbent Glass Mat (AGM) batteries represent a prime growth avenue. These advanced types offer superior performance, including higher cycle life, improved charge acceptance, and better deep discharge recovery compared to conventional flooded batteries. They are essential for modern vehicles equipped with start-stop systems, regenerative braking, and extensive electronic features, allowing SLI batteries to remain relevant and even expand their utility in the evolving automotive landscape. Investing in these advanced chemistries allows manufacturers to capture higher-value segments of the market and extend the competitive lifespan of lead-acid technology.

Emerging markets, particularly in Asia Pacific, Latin America, and Africa, offer substantial untapped potential for SLI battery manufacturers. Rapid urbanization, increasing disposable incomes, and the consequent growth in vehicle ownership in these regions are fueling demand for both new vehicles and aftermarket replacements. Unlike developed markets where growth is often driven by replacement cycles, these emerging economies are experiencing a surge in new vehicle sales, leading to a concurrent rise in demand for OEM-fitted SLI batteries. Localizing manufacturing and distribution in these regions, while adapting products to specific regional requirements and cost sensitivities, can unlock significant growth opportunities and diversify revenue streams.

Furthermore, the growing trend towards mild hybrid electric vehicles (MHEVs) creates a unique niche for advanced SLI batteries. MHEVs utilize a 12V or 48V electrical system that often incorporates a robust SLI battery alongside a small electric motor to assist the internal combustion engine, enable regenerative braking, and power auxiliary systems. This integration positions SLI batteries as a cost-effective and critical component in the transitionary phase between conventional ICE vehicles and full battery electric vehicles. Companies that can innovate to meet the specific demands of MHEV systems, focusing on higher voltage tolerance, improved charge/discharge rates, and longer durability, stand to gain a competitive edge in this evolving segment of the automotive market.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Advancements in Lead-Acid Technology (AGM/EFB) | +0.8% | Global | Mid-term to Long-term |

| Expansion in Emerging Markets (Vehicle Parc Growth) | +0.7% | Asia Pacific, Latin America, Africa | Long-term (2025-2033) |

| Integration with Mild Hybrid Vehicle (MHEV) Systems | +0.6% | Europe, North America, Asia Pacific | Long-term (2026-2033) |

| Development of Enhanced Battery Recycling Technologies | +0.5% | Developed Markets | Long-term (2025-2033) |

| Demand for Specialized SLI Batteries in Niche Applications (e.g., Marine, Powersports) | +0.3% | Specific regional markets | Mid-term |

SLI Battery Market Challenges Impact Analysis

The SLI Battery market faces significant challenges primarily driven by the broader automotive industry's accelerating shift towards electric vehicles (EVs). While SLI batteries retain auxiliary functions in EVs, their primary role in providing starting power for internal combustion engines (ICE) is gradually diminishing as battery electric vehicle (BEV) adoption grows. This fundamental transition poses a long-term threat to core market demand, particularly for traditional flooded SLI batteries. Manufacturers must strategically navigate this paradigm shift, potentially diversifying their product portfolios or focusing on the robust aftermarket for existing ICE and hybrid vehicles to mitigate the impact of reduced OEM demand for new ICE vehicles in the future.

Another pressing challenge for the SLI battery market is the intense competitive landscape and the continuous pressure on pricing. The market is mature, with numerous established players and increasing competition from regional manufacturers, especially in Asia. This leads to fierce price wars, making it difficult for companies to maintain healthy profit margins, particularly for standard flooded battery types. Innovation in product features, cost-efficient manufacturing processes, and strong brand recognition become crucial for companies to differentiate themselves and sustain profitability. Furthermore, the ability to manage supply chain complexities and raw material costs effectively is vital in this highly competitive environment.

Finally, regulatory pressures and environmental compliance continue to present a substantial challenge. Governments worldwide are imposing stricter regulations on lead usage, emissions, and waste management, pushing battery manufacturers to adopt more environmentally friendly production methods and invest heavily in recycling infrastructure. While promoting sustainability, these regulations can increase operational costs, requiring significant capital expenditure for facility upgrades and adherence to complex compliance protocols. Failure to meet these standards can result in penalties, reputational damage, and even market exclusion, necessitating a proactive approach to environmental stewardship and continuous innovation in sustainable battery technologies and recycling solutions.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Accelerated Shift Towards Electric Vehicles (BEV, PHEV) | -0.9% | Developed Markets (Europe, North America, China) | Long-term (2028-2033) |

| Intense Market Competition and Price Pressures | -0.5% | Global | Long-term (2025-2033) |

| Increasing Cost of Regulatory Compliance and Recycling | -0.4% | Global, particularly Europe | Long-term (2025-2033) |

| Supply Chain Disruptions and Geopolitical Instabilities | -0.3% | Global | Short-term (2025-2026) |

| Technological Advancements in Battery Monitoring and Diagnostics | -0.2% | Global | Mid-term (2025-2029) |

SLI Battery Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the SLI Battery market, covering historical data from 2019 to 2023 and offering detailed forecasts for the period 2025-2033. The scope includes a thorough examination of market size estimations, growth rates, key trends, and a detailed segmentation analysis across various types, applications, and sales channels. It further highlights regional dynamics and profiles leading market players, offering a holistic view for strategic decision-making within the global SLI Battery industry. The report also addresses the impact of emerging technologies and market challenges, providing actionable insights for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 10.5 Billion |

| Market Forecast in 2033 | USD 14.1 Billion |

| Growth Rate | 3.8% |

| Number of Pages | 245 |

| Key Trends | |

| Segments Covered | |

| Key Companies Covered | Global Battery Power Solutions, Energy Storage Innovations Inc., Automotive Power Systems Ltd., Universal Battery Manufacturers, Advanced Energy Technologies, Nexus Battery Corporation, Elite Power Systems, DynaCharge Battery Group, Premier Battery Solutions, Summit Automotive Batteries, Core Energy Components, Voltaic Power Solutions, Horizon Battery Technologies, Apex Energy Products, Sterling Battery Co., Quantum Power Systems, Reliable Battery Group, Pinnacle Energy Solutions, Titan Automotive Batteries, Evergreen Power Systems |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The SLI Battery market is comprehensively segmented to provide granular insights into its diverse components, enabling stakeholders to understand specific demand drivers, competitive landscapes, and growth opportunities within each category. This segmentation analysis considers battery types, the various vehicle applications they serve, and the primary sales channels through which they reach consumers and automotive manufacturers. Each segment is influenced by distinct technological trends, regulatory environments, and consumer preferences, contributing uniquely to the overall market dynamics. Understanding these segment-specific nuances is crucial for strategic planning, product development, and market entry decisions, allowing companies to tailor their offerings and maximize their market penetration.

- By Type

- Flooded Batteries: Representing traditional SLI technology, widely used due to their cost-effectiveness and reliability.

- Absorbent Glass Mat (AGM) Batteries: Premium batteries offering enhanced performance, vibration resistance, and suited for start-stop vehicles and demanding applications.

- Enhanced Flooded Battery (EFB): A cost-effective alternative to AGM, providing improved cycling performance over standard flooded batteries, commonly used in entry-level start-stop vehicles.

- By Application

- Passenger Vehicles: The largest segment, covering sedans, SUVs, hatchbacks, and other personal transportation.

- Commercial Vehicles: Including trucks, buses, and vans, requiring robust batteries for heavy-duty cycles.

- Two-Wheelers: Motorcycles, scooters, and other two-wheeled vehicles, particularly prevalent in Asian markets.

- Marine: Batteries for boats and marine vessels, designed for deep cycling and harsh conditions.

- Industrial Equipment: For forklifts, cleaning machines, and other industrial applications where starting power is required.

- By Sales Channel

- Original Equipment Manufacturer (OEM): Batteries supplied directly to vehicle manufacturers for installation in new vehicles.

- Aftermarket: Replacement batteries sold through distributors, retailers, and service centers to end-users.

Regional Highlights

- Asia Pacific (APAC): Dominates the SLI battery market due to high automotive production volumes, rapid urbanization, increasing disposable incomes, and a vast vehicle parc, particularly in countries like China, India, and Japan. The region experiences substantial demand from both OEM and aftermarket segments, driven by a growing middle class and expanding vehicle ownership.

- North America: A mature market characterized by a significant aftermarket segment due to a large existing vehicle fleet. The region sees strong demand for replacement batteries and advanced SLI types (AGM/EFB) driven by the prevalence of vehicles with start-stop technology and consumer preference for high-performance batteries.

- Europe: A key region for technological adoption, with a high penetration of start-stop systems and a growing focus on mild hybrid vehicles, driving demand for advanced SLI batteries. Strict environmental regulations also push for innovations in battery technology and recycling practices.

- Latin America: Presents considerable growth opportunities driven by increasing vehicle sales and production, albeit with economic fluctuations. The market is characterized by a mix of conventional flooded batteries and a growing adoption of advanced types as automotive technology progresses.

- Middle East and Africa (MEA): Emerging markets with nascent but growing automotive industries. Demand is primarily driven by expanding vehicle fleets and infrastructure development, with a notable focus on cost-effective solutions and increasing aftermarket needs.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the SLI Battery Market.- Global Battery Power Solutions

- Energy Storage Innovations Inc.

- Automotive Power Systems Ltd.

- Universal Battery Manufacturers

- Advanced Energy Technologies

- Nexus Battery Corporation

- Elite Power Systems

- DynaCharge Battery Group

- Premier Battery Solutions

- Summit Automotive Batteries

- Core Energy Components

- Voltaic Power Solutions

- Horizon Battery Technologies

- Apex Energy Products

- Sterling Battery Co.

- Quantum Power Systems

- Reliable Battery Group

- Pinnacle Energy Solutions

- Titan Automotive Batteries

- Evergreen Power Systems

Frequently Asked Questions

What is the forecast for the SLI Battery market?

The SLI Battery Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 3.8% between 2025 and 2033, reaching an estimated USD 14.1 Billion by 2033 from USD 10.5 Billion in 2025.

What are the primary drivers of SLI Battery market growth?

Key drivers include the increasing global vehicle production and sales, robust aftermarket demand for replacement batteries, the growing adoption of start-stop vehicle systems, and the inherent cost-effectiveness and reliability of lead-acid battery technology.

How do regional markets contribute to the SLI Battery industry?

Asia Pacific is the largest and fastest-growing market due to high vehicle production. North America and Europe are significant for replacement demand and the adoption of advanced SLI technologies like AGM and EFB, while Latin America and MEA offer emerging growth opportunities.

What are the key technological advancements in SLI batteries?

Significant advancements include the development and widespread adoption of Absorbent Glass Mat (AGM) and Enhanced Flooded Battery (EFB) technologies, which offer improved cycle life, charge acceptance, and suitability for modern vehicles with advanced electrical systems and start-stop functions.

What challenges does the SLI Battery market face?

Major challenges include the accelerated shift towards electric vehicles (BEVs), intense market competition and price pressures, increasing costs associated with regulatory compliance and lead recycling, and potential supply chain disruptions for raw materials.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted