Single Photon Avalanche Photodiode Market

Single Photon Avalanche Photodiode Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702879 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

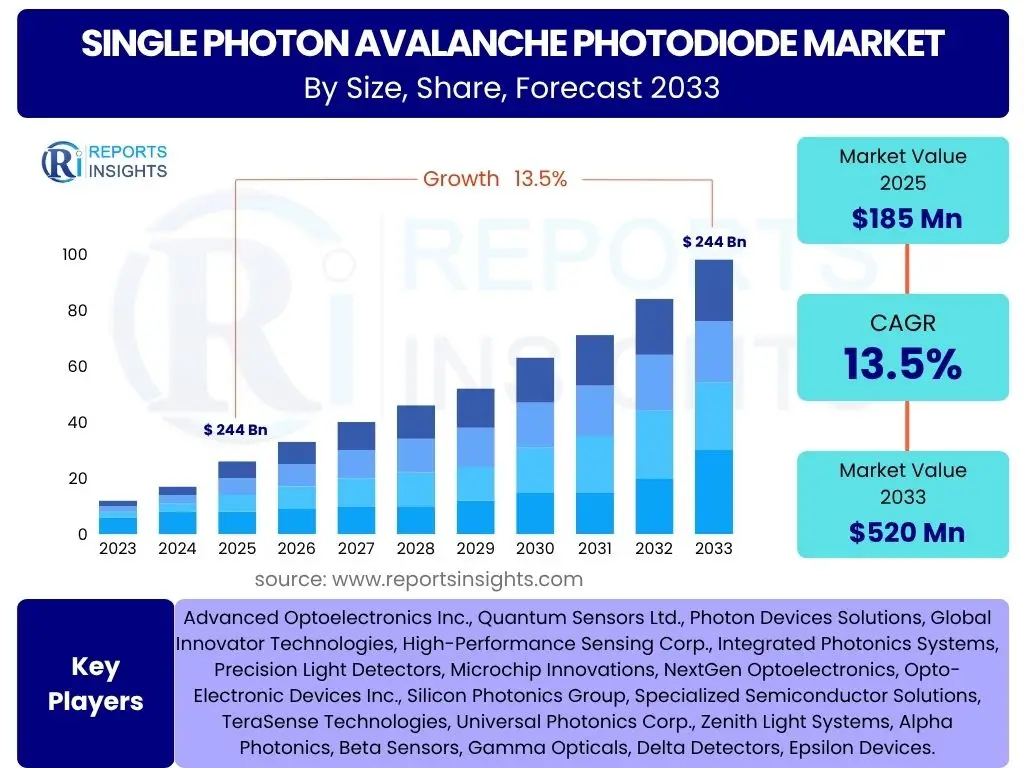

Single Photon Avalanche Photodiode Market Size

According to Reports Insights Consulting Pvt Ltd, The Single Photon Avalanche Photodiode Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 13.5% between 2025 and 2033. The market is estimated at USD 185 Million in 2025 and is projected to reach USD 520 Million by the end of the forecast period in 2033.

Key Single Photon Avalanche Photodiode Market Trends & Insights

The Single Photon Avalanche Photodiode (SPAD) market is experiencing transformative trends driven by technological advancements and expanding application landscapes. A prominent trend involves the miniaturization and integration of SPADs into array formats, enabling high-resolution 3D imaging and sensing applications. This push towards compact, high-performance SPAD arrays is critical for their adoption in consumer electronics, automotive LiDAR, and advanced medical diagnostics. Furthermore, there is a significant focus on improving photon detection efficiency (PDE) across a broader spectrum, particularly in the near-infrared (NIR) range, which is crucial for applications requiring deep penetration and long-range sensing.

Another key insight revolves around the increasing demand for SPADs in emerging fields such as quantum computing and communication. These applications leverage the single-photon detection capability of SPADs for secure data transmission and complex computational tasks, highlighting a shift towards more sophisticated uses beyond traditional light detection. Moreover, advancements in material science are paving the way for new SPAD structures, including those based on III-V semiconductors, offering enhanced performance characteristics like lower dark count rates and higher operational temperatures, thereby expanding their versatility and reliability across diverse environments. The synergy between these technological improvements and the growing need for precise, real-time sensing solutions is shaping the market's trajectory.

- Miniaturization and integration of SPAD arrays for compact systems.

- Enhanced Photon Detection Efficiency (PDE) across broader spectral ranges, particularly NIR.

- Growing adoption in quantum computing and secure communication systems.

- Development of advanced SPAD structures using novel semiconductor materials.

- Increased focus on reducing dark count rates and improving operational stability.

AI Impact Analysis on Single Photon Avalanche Photodiode

Artificial Intelligence (AI) is profoundly influencing the Single Photon Avalanche Photodiode market by enhancing data processing capabilities and optimizing sensor performance. AI algorithms are increasingly employed to process the large volumes of data generated by SPAD arrays, particularly in applications like LiDAR and medical imaging. This enables faster and more accurate interpretation of complex spatial and temporal information, leading to improved object recognition in autonomous vehicles or more precise diagnostic images in healthcare. The integration of AI facilitates noise reduction, signal amplification, and adaptive thresholding, thereby pushing the practical limits of SPAD sensitivity and reliability in real-world scenarios.

Furthermore, AI plays a crucial role in the design and optimization of SPAD devices themselves. Machine learning techniques can be applied to simulate and predict the performance of new SPAD architectures, accelerating research and development cycles. AI-driven models can identify optimal doping profiles, junction designs, and passivation layers to maximize photon detection efficiency while minimizing dark counts and afterpulsing effects. Beyond device design, AI contributes to the calibration and self-correction mechanisms of SPAD-based systems, ensuring consistent performance over time and across varying environmental conditions. This symbiotic relationship between AI and SPAD technology is unlocking new capabilities and expanding the potential for SPAD adoption in intelligent systems requiring high-fidelity light detection.

- AI-enhanced data processing for improved image reconstruction and object recognition in SPAD-based systems.

- Machine learning algorithms optimizing SPAD design for higher efficiency and lower noise.

- Predictive maintenance and self-calibration of SPAD sensors using AI models.

- Fusion of SPAD data with other sensor inputs via AI for comprehensive environmental perception.

- Enabling advanced features like real-time anomaly detection and predictive analytics in SPAD applications.

Key Takeaways Single Photon Avalanche Photodiode Market Size & Forecast

The Single Photon Avalanche Photodiode market is poised for robust expansion, driven primarily by its indispensable role in next-generation sensing and imaging technologies. The projected substantial CAGR highlights a significant confidence in SPAD capabilities to meet growing demands across diverse high-tech sectors. A key takeaway is the increasing integration of SPAD technology into everyday and specialized applications, moving beyond research laboratories into commercial products, especially within the automotive and healthcare industries. This widespread adoption is underpinned by continuous improvements in SPAD performance, including higher photon detection efficiency and lower dark count rates, making them more attractive for precision light sensing.

Another critical insight reveals that while innovation in core SPAD technology continues, the market's growth is also heavily influenced by the development of sophisticated system-level solutions that leverage SPAD arrays for 3D mapping, quantum communication, and advanced medical diagnostics. The forecast indicates that regional markets such as Asia Pacific and North America will likely remain dominant, fueled by strong R&D investments and a burgeoning presence of key technology developers and end-users. The market's future remains bright, with continuous innovation in both the underlying technology and its diverse applications promising sustained growth and market diversification, despite facing some technical challenges related to manufacturing scalability and cost efficiencies.

- Significant growth anticipated, driven by increasing adoption in advanced sensing and imaging.

- LiDAR for autonomous vehicles and quantum technologies are primary growth catalysts.

- Technological advancements in SPAD performance are enabling new application frontiers.

- Strong market concentration in North America and Asia Pacific due to R&D and manufacturing hubs.

- Continued innovation in array integration and material science will sustain market momentum.

Single Photon Avalanche Photodiode Market Drivers Analysis

The Single Photon Avalanche Photodiode (SPAD) market is primarily driven by the escalating demand for highly sensitive and precise light detection capabilities across various advanced applications. The rapid proliferation of autonomous vehicles, particularly the growing adoption of LiDAR technology for accurate 3D mapping and obstacle detection, stands as a paramount driver. SPADs offer superior single-photon sensitivity and fast response times, making them ideal for long-range and high-resolution LiDAR systems crucial for safe and reliable autonomous navigation. This automotive sector's continuous innovation and investment directly contribute to the expansion of the SPAD market, pushing for higher performance and cost-effectiveness.

Another significant driver is the burgeoning field of quantum technologies, including quantum computing and quantum cryptography. SPADs are fundamental components in these applications due to their ability to detect individual photons, which is essential for quantum information processing and secure communication protocols. The global push for quantum supremacy and enhanced cybersecurity measures ensures a sustained and increasing demand for SPAD devices. Furthermore, the advancements in biomedical imaging, such as Positron Emission Tomography (PET) and Optical Coherence Tomography (OCT), where SPADs provide high temporal resolution and sensitivity for detailed biological insights, also contribute substantially to market growth, underscoring their versatility and critical role in cutting-edge scientific and industrial domains.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for LiDAR in Autonomous Vehicles | +3.0% | North America, Europe, Asia Pacific (China, Japan, South Korea) | 2025-2033 |

| Growing Adoption in Quantum Communication and Computing | +2.5% | North America, Europe, Asia Pacific (China) | 2027-2033 |

| Advancements in Medical Imaging and Diagnostics | +2.0% | North America, Europe, Asia Pacific | 2025-2030 |

| Expansion of Industrial Automation and Machine Vision | +1.5% | Asia Pacific (China, India), Europe | 2026-2032 |

Single Photon Avalanche Photodiode Market Restraints Analysis

Despite the robust growth prospects, the Single Photon Avalanche Photodiode market faces certain restraints that could temper its expansion. One significant challenge is the relatively high manufacturing cost associated with SPADs, particularly for large-scale arrays and specialized materials. The complex fabrication processes required to achieve high photon detection efficiency, low dark count rates, and precise uniformity across arrays contribute to increased production expenses, making SPADs less competitive in cost-sensitive applications where alternative photodetectors suffice. This cost factor can hinder broader adoption, especially in consumer-grade electronics or industrial applications where budget constraints are paramount.

Another crucial restraint is the inherent limitation of SPADs regarding dynamic range and saturation effects. While excelling at single-photon detection, SPADs can become saturated in environments with high ambient light levels, limiting their utility in diverse lighting conditions without complex external gating or filtering mechanisms. This can lead to a trade-off between sensitivity and operational range, posing a challenge for applications requiring both. Furthermore, the dark count rate (DCR) and afterpulsing effects, although continuously being improved, remain performance limitations that affect the signal-to-noise ratio, particularly in applications demanding extreme precision and low noise, such as deep-space communication or certain quantum experiments, thereby imposing technical hurdles for widespread integration.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs and Complexity | -1.8% | Global | 2025-2030 |

| Limited Dynamic Range and Saturation Issues | -1.5% | Global | 2025-2033 |

| Challenges with Dark Count Rate and Afterpulsing | -1.2% | Global | 2025-2028 |

| Competition from Alternative Photodetector Technologies | -1.0% | Global | 2025-2033 |

Single Photon Avalanche Photodiode Market Opportunities Analysis

Significant opportunities abound in the Single Photon Avalanche Photodiode market, primarily driven by the continuous advancement in integration technologies and the exploration of new application areas. The miniaturization of SPADs and their integration into highly dense arrays offer substantial potential, enabling compact and powerful 3D imaging systems for consumer electronics, such as smartphones for facial recognition and augmented reality applications. This trend towards consumer-grade integration promises to open up a massive volume market, significantly expanding the addressable market beyond specialized industrial and scientific uses. Investments in System-on-Chip (SoC) integration for SPAD arrays further reduce system complexity and cost, making them more appealing for mass production.

Another major opportunity lies in the development of SPADs based on novel materials beyond traditional silicon, such as III-V semiconductors (e.g., InGaAs for infrared detection) and wide-bandgap materials (e.g., GaN, SiC for UV detection). These materials enable SPADs to operate across a broader spectrum with enhanced performance characteristics, including higher temperature operation and improved detection efficiency in specific wavelengths critical for specialized applications like free-space optical communication, environmental monitoring, and next-generation medical diagnostics. Furthermore, the strategic partnerships between SPAD manufacturers and automotive OEMs, defense contractors, and quantum technology developers are fostering co-innovation and accelerating market penetration, creating tailored solutions that capitalize on the unique capabilities of single-photon detection technology.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Miniaturization and Integration in Consumer Electronics | +2.8% | Asia Pacific (China, South Korea), North America | 2026-2033 |

| Development of Novel Material-based SPADs | +2.2% | Global (Research & Development Hubs) | 2027-2033 |

| Expansion into Free-Space Optical Communication | +1.9% | North America, Europe | 2028-2033 |

| Strategic Partnerships and Collaborations | +1.6% | Global | 2025-2033 |

Single Photon Avalanche Photodiode Market Challenges Impact Analysis

The Single Photon Avalanche Photodiode market faces several technical and commercial challenges that necessitate continuous innovation and strategic solutions. A significant technical challenge is achieving higher photon detection efficiency (PDE) while simultaneously reducing the dark count rate (DCR) across varying wavelengths, especially at elevated temperatures. Improving PDE is critical for enhancing sensitivity, but maintaining a low DCR is essential to avoid false positive signals, which is particularly challenging in compact, high-density SPAD arrays where thermal management and crosstalk become major concerns. The trade-off between these performance metrics requires advanced fabrication techniques and innovative device architectures, adding complexity to the manufacturing process.

Another notable challenge revolves around the scalability of manufacturing processes for SPAD arrays, especially as demand from high-volume applications like automotive LiDAR grows. Ensuring uniformity in performance across millions of SPAD elements on a single chip, while maintaining cost-effectiveness and high yield rates, presents substantial engineering and logistical hurdles. Furthermore, the intellectual property landscape surrounding SPAD technology is becoming increasingly complex, with numerous patents held by key players. Navigating this landscape and securing access to essential technologies can be challenging for new entrants and can influence market dynamics and competitive strategies. Addressing these challenges effectively will be crucial for the sustained growth and widespread adoption of SPAD technology in emerging markets.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Balancing High PDE with Low DCR at Various Temperatures | -1.7% | Global | 2025-2030 |

| Scalability and Yield Management in Large Array Manufacturing | -1.4% | Global | 2026-2033 |

| Complex Intellectual Property Landscape | -1.0% | Global | 2025-2033 |

| Integration with Existing System Architectures | -0.8% | Global | 2025-2029 |

Single Photon Avalanche Photodiode Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Single Photon Avalanche Photodiode (SPAD) market, offering detailed insights into market size, growth drivers, restraints, opportunities, and key trends. It encompasses a thorough examination of market segments, regional dynamics, and the competitive landscape, delivering a forward-looking perspective on market evolution and strategic recommendations for stakeholders. The report aims to equip businesses with actionable intelligence to navigate the complexities of this rapidly evolving high-technology market.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 185 Million |

| Market Forecast in 2033 | USD 520 Million |

| Growth Rate | 13.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Advanced Optoelectronics Inc., Quantum Sensors Ltd., Photon Devices Solutions, Global Innovator Technologies, High-Performance Sensing Corp., Integrated Photonics Systems, Precision Light Detectors, Microchip Innovations, NextGen Optoelectronics, Opto-Electronic Devices Inc., Silicon Photonics Group, Specialized Semiconductor Solutions, TeraSense Technologies, Universal Photonics Corp., Zenith Light Systems, Alpha Photonics, Beta Sensors, Gamma Opticals, Delta Detectors, Epsilon Devices. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Single Photon Avalanche Photodiode (SPAD) market is meticulously segmented to provide a granular view of its diverse landscape, categorized by type, application, end-use industry, and operation mode. This segmentation allows for a detailed understanding of the market dynamics within specific niches and highlights areas of significant growth or emerging potential. Each segment is influenced by distinct technological requirements, market drivers, and competitive landscapes, contributing uniquely to the overall market trajectory. Analyzing these segments helps stakeholders identify lucrative opportunities and tailor their strategies to specific market demands.

By type, the market is primarily divided into Silicon SPADs, which currently dominate due to mature manufacturing processes and cost-effectiveness, and III-V Semiconductor SPADs, which are gaining traction for their superior performance in specific spectral ranges like infrared. The application segment is broad, ranging from high-growth areas like LiDAR for autonomous vehicles and quantum technologies, to established fields such as medical imaging and industrial automation. The end-use industry classification further refines this by categorizing adoption across sectors like automotive, healthcare, and telecommunications, while the operation mode distinction between Geiger mode and linear mode SPADs defines their specific functionalities in different detection scenarios, collectively painting a comprehensive picture of the market structure and its evolving demands.

- By Type: Silicon SPAD (Si-SPAD), III-V Semiconductor SPAD (e.g., InGaAs SPAD), Other SPAD Materials (e.g., SiC, GaN).

- By Application: LiDAR (Light Detection and Ranging), Quantum Communications and Computing, Medical Imaging (e.g., PET, OCT), Industrial Automation and Machine Vision, Scientific Research, Defense and Security, Consumer Electronics (e.g., Facial Recognition, AR/VR), Optical Communications.

- By End-Use Industry: Automotive, Healthcare, Telecommunications, Industrial, Aerospace & Defense, Research & Development, Consumer Electronics.

- By Operation Mode: Geiger Mode, Linear Mode.

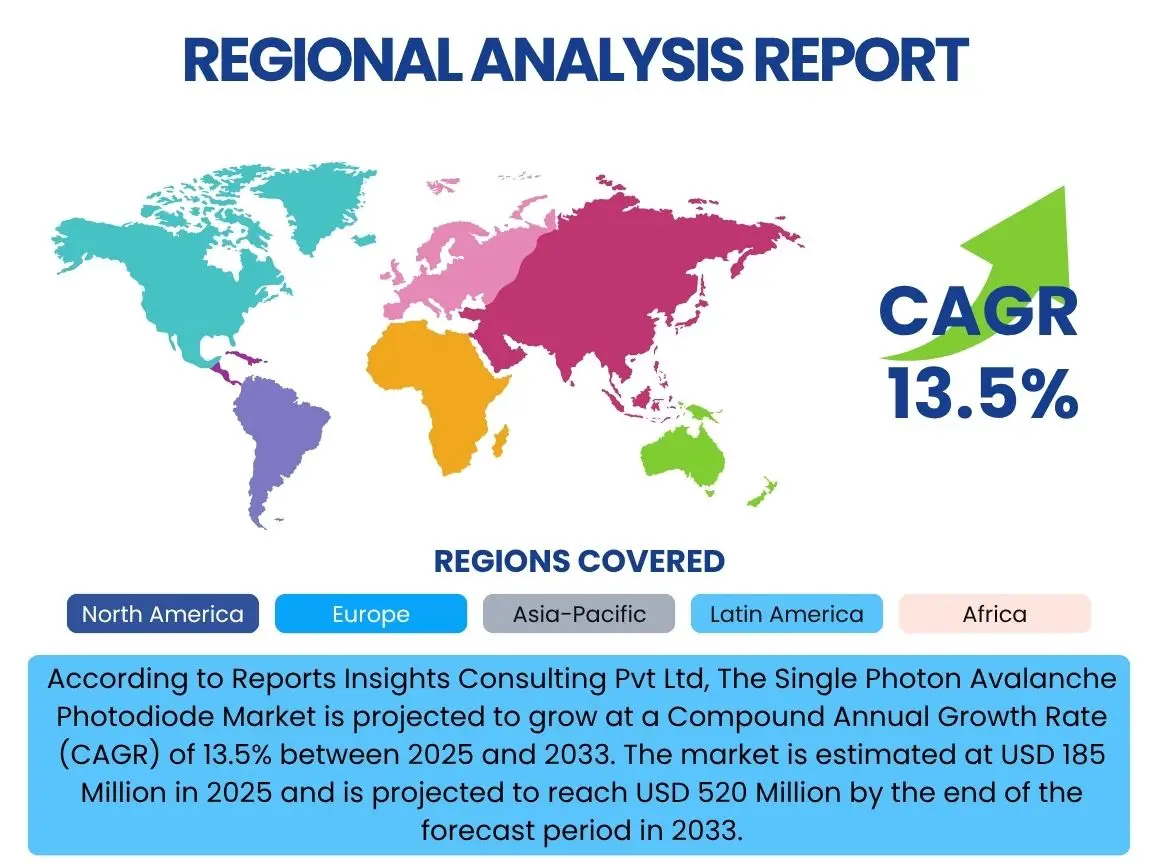

Regional Highlights

Geographically, the Single Photon Avalanche Photodiode market exhibits significant variation in growth and adoption, primarily concentrated in regions with robust technological infrastructure, high research and development investments, and a strong presence of key end-use industries. North America, particularly the United States, holds a dominant position due to its advanced automotive industry, substantial investments in defense and aerospace, and a flourishing quantum technology ecosystem. The presence of leading SPAD manufacturers, research institutions, and early adopters in LiDAR and medical imaging applications further solidifies its market share. This region continues to drive innovation in SPAD design and system integration.

Asia Pacific is projected to witness the highest growth rate during the forecast period, fueled by rapid industrialization, increasing adoption of autonomous vehicles in countries like China and Japan, and a booming consumer electronics manufacturing base. Government initiatives promoting advanced technologies and a large talent pool also contribute to this growth. Europe, with countries like Germany and the UK at the forefront, also represents a significant market due driven by strong automotive and industrial automation sectors, coupled with substantial research in quantum optics. Latin America, the Middle East, and Africa are emerging markets, expected to show gradual growth as infrastructure develops and awareness of SPAD applications increases in various sectors, especially in telecommunications and security.

- North America: Dominant market share driven by robust R&D, autonomous vehicle industry, and defense sector investments.

- Asia Pacific (APAC): Fastest growing region due to rapid industrialization, burgeoning consumer electronics, and automotive markets, particularly in China and Japan.

- Europe: Significant market contribution from strong automotive manufacturing, industrial automation, and quantum technology research.

- Latin America: Emerging market with growing adoption in telecommunications and security applications.

- Middle East & Africa (MEA): Gradual market expansion anticipated with increasing investments in smart infrastructure and defense.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Single Photon Avalanche Photodiode Market.- Advanced Optoelectronics Inc.

- Quantum Sensors Ltd.

- Photon Devices Solutions

- Global Innovator Technologies

- High-Performance Sensing Corp.

- Integrated Photonics Systems

- Precision Light Detectors

- Microchip Innovations

- NextGen Optoelectronics

- Opto-Electronic Devices Inc.

- Silicon Photonics Group

- Specialized Semiconductor Solutions

- TeraSense Technologies

- Universal Photonics Corp.

- Zenith Light Systems

- Alpha Photonics

- Beta Sensors

- Gamma Opticals

- Delta Detectors

- Epsilon Devices

Frequently Asked Questions

What is a Single Photon Avalanche Photodiode (SPAD)?

A Single Photon Avalanche Photodiode (SPAD) is a highly sensitive semiconductor photodetector capable of detecting individual photons. It operates in Geiger mode, where a single photon triggers a strong avalanche current, producing a detectable electrical pulse, making it ideal for applications requiring extreme sensitivity and precise timing.

How do SPADs differ from traditional APDs?

While both SPADs and Avalanche Photodiodes (APDs) utilize avalanche multiplication for signal amplification, SPADs operate above their breakdown voltage in Geiger mode, allowing them to detect single photons by producing a macroscopic current pulse. Traditional APDs typically operate below their breakdown voltage in linear mode, providing analog amplification for varying light intensities, but lack single-photon sensitivity.

What are the primary applications of SPADs?

SPADs are widely used in applications requiring high sensitivity and fast response times, including LiDAR for autonomous vehicles, quantum communication and computing, medical imaging (e.g., PET scanners, OCT), industrial machine vision, scientific research, and increasingly in consumer electronics for 3D sensing and facial recognition.

What are the key technical challenges facing SPAD technology?

Key technical challenges for SPAD technology include reducing the dark count rate (false detections in the absence of light), improving photon detection efficiency across a broader spectrum (especially in the infrared), mitigating afterpulsing effects (secondary avalanches), and achieving high uniformity and yield in large-scale array manufacturing.

What is the future outlook for the Single Photon Avalanche Photodiode market?

The future outlook for the SPAD market is highly positive, driven by continuous technological advancements in miniaturization, integration, and performance. Expanding applications in autonomous systems, quantum technologies, and advanced medical diagnostics, coupled with increasing investments in research and development, are expected to fuel significant market growth and diversification over the next decade.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted