Silicon Carbide Semiconductor Device Market

Silicon Carbide Semiconductor Device Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706418 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Silicon Carbide Semiconductor Device Market Size

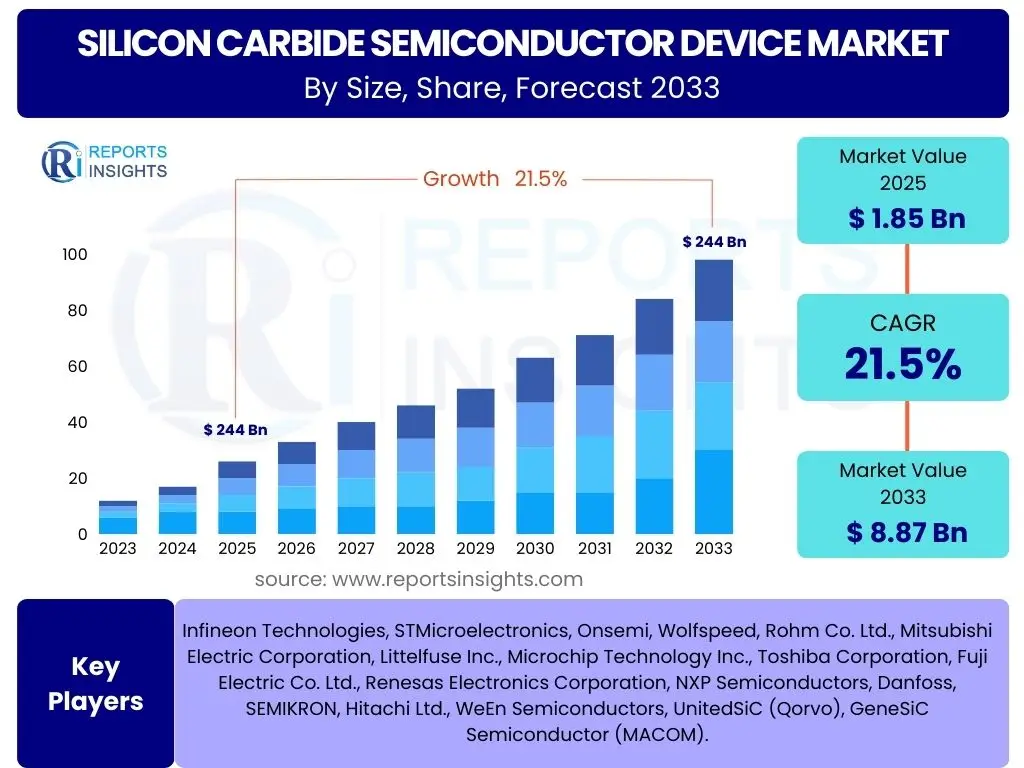

According to Reports Insights Consulting Pvt Ltd, The Silicon Carbide Semiconductor Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 21.5% between 2025 and 2033. The market is estimated at USD 1.85 Billion in 2025 and is projected to reach USD 8.87 Billion by the end of the forecast period in 2033. This significant growth is primarily driven by the increasing demand for high-efficiency power electronics across various industries, alongside advancements in manufacturing technologies that make SiC devices more accessible and cost-effective. The inherent properties of SiC, such as higher breakdown voltage, faster switching speeds, and superior thermal conductivity, position it as a critical enabler for next-generation power management solutions.

Key Silicon Carbide Semiconductor Device Market Trends & Insights

Common inquiries from users regarding Silicon Carbide Semiconductor Device market trends often revolve around the adoption rates in key industries, technological advancements, and the competitive landscape. There is a keen interest in understanding how SiC is displacing traditional silicon-based solutions, particularly in high-power and high-frequency applications. Users frequently seek information on the long-term viability and sustainability of SiC as a foundational material for future electronic systems, along with insights into emerging application areas beyond automotive and renewable energy. The focus is also on supply chain dynamics and the impact of geopolitical factors on the market's trajectory.

The market is witnessing a strong push towards larger wafer sizes, moving from 4-inch to 6-inch, with significant research and development efforts aimed at commercializing 8-inch SiC wafers. This transition is crucial for reducing production costs and increasing manufacturing throughput, making SiC devices more competitive on a per-chip basis. Furthermore, the integration of SiC technology into compact and robust modules is a key trend, addressing the increasing power density requirements in applications like electric vehicles and industrial power supplies. This modular approach simplifies design and enhances reliability, driving broader adoption across various sectors. The focus on improved packaging technologies that can withstand higher operating temperatures and power cycling is also paramount, ensuring the long-term performance and durability of SiC devices in demanding environments.

- Accelerated adoption in Electric Vehicles (EVs) for powertrains and charging infrastructure.

- Increased demand from renewable energy sectors, particularly solar inverters and wind turbine converters.

- Transition to larger SiC wafer sizes (6-inch and 8-inch) for cost reduction and higher volume production.

- Development of integrated SiC modules for enhanced power density and simplified design.

- Growing investment in R&D for next-generation SiC materials and device architectures.

- Expansion into new application areas such as aerospace, defense, and smart grid solutions.

- Focus on supply chain localization and resilience due to geopolitical considerations.

AI Impact Analysis on Silicon Carbide Semiconductor Device

User queries concerning the impact of Artificial Intelligence (AI) on the Silicon Carbide Semiconductor Device market often explore how AI is used in design, manufacturing, and application optimization. There is significant interest in understanding AI's role in accelerating material discovery and characterization, optimizing device performance, and streamlining the complex fabrication processes unique to SiC. Users also want to know if AI can help address some of the current challenges in SiC manufacturing, such as defect density reduction and yield improvement, and how AI-driven analytics might enhance the reliability and predictive maintenance of SiC-based systems in their operational environments.

AI's influence on the SiC semiconductor device market is multifaceted, enhancing capabilities across the entire value chain. In the design phase, AI-driven simulations and optimization algorithms are significantly reducing the time and cost associated with developing new SiC device architectures, allowing for more efficient exploration of design parameters and performance characteristics. During manufacturing, AI-powered process control and predictive analytics are vital for improving wafer quality, minimizing defects, and optimizing production yields, which are traditionally challenging for SiC. Furthermore, AI contributes to the reliability and longevity of SiC devices by enabling more precise thermal management and fault prediction in deployed systems, thereby extending their operational lifespan and reducing maintenance costs. This integration of AI not only streamlines current operations but also paves the way for innovative applications and further expands the market potential of SiC technology.

- AI-driven optimization of SiC device design parameters for enhanced performance.

- Improved manufacturing yield and defect reduction through AI-powered process control and predictive analytics.

- Accelerated material discovery and characterization of new SiC substrates and epitaxial layers.

- Predictive maintenance and enhanced reliability of SiC-based systems using AI algorithms.

- Automated inspection and quality control in SiC wafer and device fabrication.

- AI integration into power management units for smarter energy conversion and distribution.

- Reduced development cycles for new SiC products through advanced simulation and modeling.

Key Takeaways Silicon Carbide Semiconductor Device Market Size & Forecast

Common user questions regarding key takeaways from the Silicon Carbide Semiconductor Device market size and forecast often center on understanding the most significant growth drivers, the primary hurdles to widespread adoption, and the sectors poised for the most substantial impact. Users are keen to grasp the underlying reasons for the projected high growth rates, such as the increasing global push for energy efficiency and the rapid expansion of electric vehicle infrastructure. They also inquire about the competitive landscape, the emergence of new players, and the potential for consolidation within the industry, all of which shape the long-term market outlook.

The Silicon Carbide Semiconductor Device market is poised for robust expansion, driven primarily by the global imperative for energy efficiency and the accelerating electrification across various industries. The high breakdown voltage, superior thermal conductivity, and faster switching speeds of SiC devices are crucial for enabling next-generation power electronics that outperform traditional silicon. While challenges such as high manufacturing costs and supply chain complexities persist, ongoing advancements in production technologies and economies of scale are gradually mitigating these barriers. The market's future will be defined by continued innovation in material science, device design, and manufacturing processes, coupled with supportive government policies promoting sustainable energy and electric mobility. This convergence positions SiC as an indispensable component in the transition to a more energy-efficient and electrified world.

- The market is experiencing a significant CAGR, indicating strong demand and rapid expansion.

- Electric Vehicles and renewable energy sectors are the primary growth catalysts.

- Technological advancements in wafer size and manufacturing processes are crucial for cost reduction.

- Supply chain robustness and material availability remain key considerations for sustained growth.

- Increased investment in research and development is fostering continuous innovation in device performance.

- The long-term outlook remains highly positive, driven by global electrification trends and energy efficiency mandates.

- Market competition is intensifying, leading to improved product offerings and competitive pricing.

Silicon Carbide Semiconductor Device Market Drivers Analysis

The Silicon Carbide Semiconductor Device market is propelled by a confluence of powerful drivers rooted in global energy transition, technological advancements, and industrial demands. The escalating adoption of electric vehicles globally is a primary catalyst, as SiC devices enable more efficient powertrains, faster charging, and extended range, which are critical for consumer acceptance. Simultaneously, the growing integration of renewable energy sources such as solar and wind power necessitates highly efficient power converters and inverters that can withstand harsh operating conditions, where SiC offers distinct advantages over silicon. These macro trends, coupled with continuous innovation in device manufacturing and design, are creating a robust demand environment for SiC technology, pushing it into a broader array of applications.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Growth in Electric Vehicle (EV) Adoption | +1.8% | Global, particularly China, Europe, North America | Short to Long-term (2025-2033) |

| Increasing Demand for Renewable Energy Systems | +1.5% | Europe, Asia Pacific, North America | Short to Mid-term (2025-2029) |

| Rising Need for High Power Density & Efficiency | +1.2% | Global | Short to Long-term (2025-2033) |

| Advancements in 5G Telecommunications Infrastructure | +0.9% | Asia Pacific, North America, Europe | Mid-term (2027-2031) |

| Government Initiatives & Subsidies for Green Energy | +0.7% | Europe, China, United States | Short to Mid-term (2025-2030) |

| Expansion of Industrial Automation & Robotics | +0.6% | Global, particularly industrialized nations | Mid to Long-term (2028-2033) |

| Growing Data Center Infrastructure Demands | +0.5% | North America, Asia Pacific, Europe | Short to Long-term (2025-2033) |

Silicon Carbide Semiconductor Device Market Restraints Analysis

Despite its significant advantages, the Silicon Carbide Semiconductor Device market faces several notable restraints that can impede its growth rate. The primary challenge remains the relatively high manufacturing cost of SiC wafers and devices compared to traditional silicon counterparts, driven by complex crystal growth processes and specialized fabrication facilities. This higher upfront cost can be a barrier for industries operating on tighter margins or those hesitant to undertake the significant capital expenditure required for transitioning their designs to SiC. Furthermore, the limited availability of large-diameter SiC wafers and the technical challenges in reducing material defects pose supply chain bottlenecks, hindering mass production and scalability. These factors collectively contribute to a slower adoption rate in certain price-sensitive or high-volume applications, despite the long-term efficiency benefits offered by SiC.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs of SiC Wafers and Devices | -1.3% | Global | Short to Mid-term (2025-2030) |

| Complexities in SiC Material Growth & Fabrication | -0.9% | Global | Short to Mid-term (2025-2029) |

| Limited Availability of Large-Diameter SiC Wafers | -0.8% | Global | Short to Mid-term (2025-2028) |

| Competition from Advanced Silicon-Based Technologies | -0.6% | Global | Short to Long-term (2025-2033) |

| Lack of Standardized Testing and Qualification Procedures | -0.4% | Global | Short-term (2025-2027) |

| Potential Thermal Management Challenges in High-Power Applications | -0.3% | Global | Mid to Long-term (2028-2033) |

Silicon Carbide Semiconductor Device Market Opportunities Analysis

The Silicon Carbide Semiconductor Device market is rich with opportunities stemming from emerging technological frontiers and expanding application domains. The burgeoning aerospace and defense sector presents a significant opportunity, as SiC devices can enable lighter, more power-efficient systems for avionics, radar, and satellite applications, where extreme conditions demand robust performance. The global push towards smart grids and advanced energy storage solutions also opens new avenues for SiC, facilitating more efficient power conversion and distribution in grid-tied and off-grid scenarios. Furthermore, the continuous drive for miniaturization and enhanced performance in consumer electronics and specialized medical devices offers niche but high-value opportunities for SiC components. These diverse applications underscore the versatility and untapped potential of SiC technology beyond its mainstream adoption, promising sustained market expansion.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Aerospace and Defense Applications | +1.1% | North America, Europe, Asia Pacific | Mid to Long-term (2028-2033) |

| Growth in Smart Grid and Energy Storage Systems | +0.9% | Global | Short to Long-term (2025-2033) |

| Development of Off-Grid and Remote Power Solutions | +0.7% | Africa, Latin America, parts of Asia Pacific | Mid to Long-term (2027-2033) |

| Emergence of Quantum Computing and Advanced Electronics | +0.6% | North America, Europe, Asia Pacific (Research Hubs) | Long-term (2030-2033) |

| Miniaturization in Consumer Electronics and Medical Devices | +0.5% | Global | Mid to Long-term (2028-2033) |

| Increased Adoption in Traction Systems for Rail & Industrial Vehicles | +0.4% | Europe, Asia Pacific | Short to Mid-term (2025-2029) |

Silicon Carbide Semiconductor Device Market Challenges Impact Analysis

The Silicon Carbide Semiconductor Device market faces distinct challenges that require strategic responses to ensure sustained growth. A significant hurdle is the scalability of manufacturing processes, particularly the production of high-quality, large-diameter SiC wafers at a commercially viable cost and volume. This impacts the overall supply chain and limits the ability to meet rapidly escalating demand from key sectors like automotive. Furthermore, the intellectual property landscape around SiC technology is complex and highly competitive, leading to potential disputes and fragmented innovation. Another critical challenge is the shortage of skilled professionals with expertise in SiC material science, device design, and power electronics, which can hinder research, development, and mass production efforts. Addressing these challenges through collaborative industry initiatives, advanced technological breakthroughs, and dedicated talent development programs is essential for the market to realize its full potential.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Scalability of SiC Wafer Production and Supply | -1.1% | Global | Short to Mid-term (2025-2029) |

| Intellectual Property (IP) Disputes and Licensing Complexities | -0.8% | North America, Europe, Asia Pacific | Short to Long-term (2025-2033) |

| Shortage of Skilled Workforce and Expertise | -0.7% | Global | Short to Long-term (2025-2033) |

| Ensuring Device Reliability in Harsh Operating Environments | -0.6% | Global | Mid to Long-term (2027-2033) |

| High Capital Investment Required for Manufacturing Facilities | -0.5% | Global | Short to Mid-term (2025-2030) |

| Disposal and Recycling Challenges of SiC Devices | -0.2% | Global | Long-term (2030-2033) |

Silicon Carbide Semiconductor Device Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the Silicon Carbide Semiconductor Device market, offering an in-depth analysis of its current landscape and future trajectory. It provides detailed insights into market sizing, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. The scope encompasses detailed market projections from 2025 to 2033, building upon historical data from 2019 to 2023, to offer a robust forecast. Furthermore, the report outlines the competitive environment, profiling key players and their strategic initiatives, and highlights critical technological trends shaping the industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 8.87 Billion |

| Growth Rate | 21.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Infineon Technologies, STMicroelectronics, Onsemi, Wolfspeed, Rohm Co. Ltd., Mitsubishi Electric Corporation, Littelfuse Inc., Microchip Technology Inc., Toshiba Corporation, Fuji Electric Co. Ltd., Renesas Electronics Corporation, NXP Semiconductors, Danfoss, SEMIKRON, Hitachi Ltd., WeEn Semiconductors, UnitedSiC (Qorvo), GeneSiC Semiconductor (MACOM). |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Silicon Carbide Semiconductor Device market is comprehensively segmented to provide granular insights into its diverse components and applications. This segmentation allows for a detailed analysis of market performance across different device types, wafer sizes, and end-use applications, offering a nuanced understanding of specific growth trajectories and opportunities. Each segment represents distinct technological requirements and market demands, influencing investment decisions and strategic planning within the industry. Understanding these segments is crucial for stakeholders to identify high-growth areas and tailor their product development and market entry strategies effectively.

- By Device Type:

- MOSFETs (Metal-Oxide-Semiconductor Field-Effect Transistors)

- Diodes (including Schottky Barrier Diodes)

- BJT (Bipolar Junction Transistors)

- IGBT (Insulated Gate Bipolar Transistors)

- Others (e.g., Thyristors, JFETs)

- By Wafer Size:

- 4-inch

- 6-inch

- 8-inch

- Others (e.g., smaller R&D wafers)

- By Application:

- Electric Vehicles (EVs)

- EV Chargers (on-board and off-board)

- EV Powertrains (inverters, DC-DC converters)

- Power Electronics (General Purpose)

- Inverters

- Converters

- Power Supplies (AC-DC, DC-DC)

- Uninterruptible Power Supplies (UPS)

- Renewable Energy

- Solar Inverters (Photovoltaic systems)

- Wind Turbine Converters

- Industrial

- Motor Drives

- Robotics

- Automation Systems

- Welding Equipment

- Aerospace & Defense

- Consumer Electronics (e.g., high-power adapters, home appliances)

- Others (e.g., Medical Devices, Telecommunications, Smart Grid infrastructure)

- Electric Vehicles (EVs)

Regional Highlights

- North America: This region is a significant hub for research and development in SiC technology, particularly driven by advancements in electric vehicles, defense applications, and data center infrastructure. Government initiatives and robust venture capital funding further stimulate market growth. The presence of key automotive OEMs and power electronics manufacturers contributes substantially to demand.

- Europe: Europe stands out for its strong emphasis on renewable energy integration and stringent environmental regulations, which are accelerating the adoption of SiC devices in solar inverters, wind power systems, and smart grid applications. The region's leading position in automotive innovation, especially in premium EV segments, also fuels the demand for high-performance SiC power modules.

- Asia Pacific (APAC): As the largest and fastest-growing market, APAC is dominated by its extensive manufacturing capabilities and massive consumer base, especially in China, Japan, and South Korea. Rapid expansion of the EV market, significant investments in 5G telecommunications infrastructure, and booming industrial automation contribute to the region's prominent share. Government support for electric mobility and domestic semiconductor production further boosts the market.

- Latin America: While currently a smaller market, Latin America is poised for significant growth, primarily driven by emerging electric vehicle adoption and increasing investments in renewable energy projects. Countries like Brazil and Mexico are seeing an uptick in EV manufacturing and solar energy installations, creating a nascent but promising market for SiC devices.

- Middle East and Africa (MEA): The MEA region is experiencing growth spurred by infrastructure development projects, including smart city initiatives and diversification away from fossil fuels towards renewable energy. The increasing need for reliable power solutions in remote areas and data centers also presents opportunities for SiC technology, particularly for efficient power conversion and distribution systems.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Silicon Carbide Semiconductor Device Market.- Infineon Technologies

- STMicroelectronics

- Onsemi

- Wolfspeed

- Rohm Co. Ltd.

- Mitsubishi Electric Corporation

- Littelfuse Inc.

- Microchip Technology Inc.

- Toshiba Corporation

- Fuji Electric Co. Ltd.

- Renesas Electronics Corporation

- NXP Semiconductors

- Danfoss

- SEMIKRON

- Hitachi Ltd.

- WeEn Semiconductors

- UnitedSiC (Qorvo)

- GeneSiC Semiconductor (MACOM)

- Basler AG

- Braskem

Frequently Asked Questions

Analyze common user questions about the Silicon Carbide Semiconductor Device market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Silicon Carbide (SiC) and why is it important for semiconductors?

Silicon Carbide (SiC) is a compound semiconductor material known for its superior electrical and thermal properties compared to traditional silicon. It is crucial for semiconductors due to its high breakdown voltage, excellent thermal conductivity, and fast switching speeds, making it ideal for high-power, high-frequency, and high-temperature applications. These properties enable more efficient power conversion, reduced energy losses, and smaller, lighter electronic systems.

Which industries are primarily driving the demand for SiC semiconductor devices?

The primary industries driving the demand for SiC semiconductor devices are electric vehicles (EVs) for their powertrains and charging infrastructure, and the renewable energy sector, specifically for solar inverters and wind turbine converters. Other significant growth areas include industrial power supplies, data centers, and advanced telecommunications (5G) infrastructure, all benefiting from SiC's efficiency and reliability.

What are the main advantages of SiC devices over traditional silicon-based devices?

SiC devices offer several key advantages over silicon: they can operate at much higher temperatures, withstand significantly higher voltages, exhibit faster switching speeds, and have lower on-resistance. These characteristics lead to greater power efficiency, reduced cooling requirements, smaller form factors, and enhanced reliability in demanding applications, ultimately lowering overall system costs and improving performance.

What challenges does the Silicon Carbide semiconductor market face?

The Silicon Carbide semiconductor market faces several challenges, including the relatively high manufacturing cost of SiC wafers and devices, complexities in crystal growth and fabrication processes, and limitations in the supply of large-diameter wafers. Additionally, the industry is navigating issues related to supply chain scalability, intellectual property disputes, and the need for a skilled workforce with specialized expertise.

What is the future outlook for the Silicon Carbide semiconductor device market?

The future outlook for the Silicon Carbide semiconductor device market is highly positive, with projections indicating robust growth. This growth is underpinned by the accelerating global transition towards electrification and renewable energy, continuous technological advancements, and increasing adoption across a wider range of high-power applications. Ongoing efforts to reduce production costs and enhance manufacturing capabilities are expected to further solidify SiC's position as a foundational technology for future power electronics.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted