Ship Exhaust Gas Scrubber Market

Ship Exhaust Gas Scrubber Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700188 | Last Updated : July 23, 2025 |

Format : ![]()

![]()

![]()

![]()

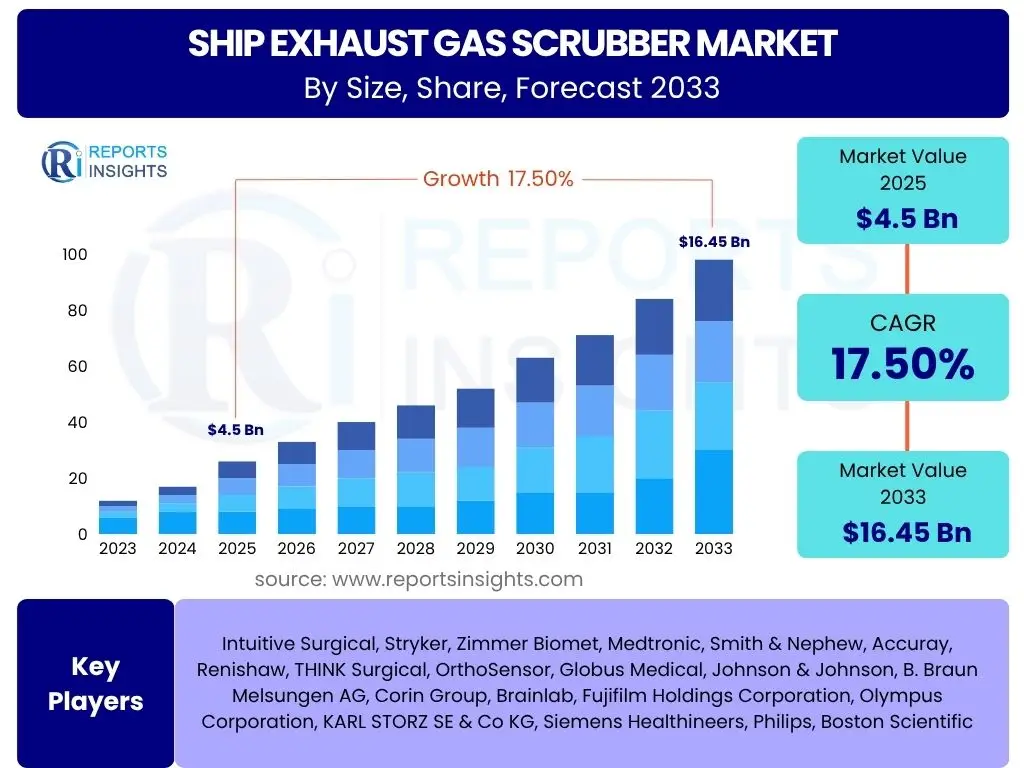

Ship Exhaust Gas Scrubber Market is projected to grow at a Compound annual growth rate (CAGR) of 17.5% between 2025 and 2033, current valued at USD 4.5 billion in 2025 and is projected to grow by USD 16.45 billion by 2033 the end of the forecast period.

Key Ship Exhaust Gas Scrubber Market Trends & Insights

The global Ship Exhaust Gas Scrubber Market is currently experiencing a dynamic phase, driven by an unwavering commitment to environmental sustainability and stringent regulatory frameworks. Key trends indicate a significant shift towards more advanced and efficient scrubber technologies, alongside a rising demand for retrofitting existing vessels to comply with current and anticipated emission standards. This evolution is also marked by an increased focus on lifecycle costs, operational efficiency, and the integration of digital solutions for enhanced performance monitoring and compliance reporting.

- Strict global and regional emission regulations drive scrubber adoption.

- Growing preference for hybrid and closed-loop scrubber systems for flexibility.

- Increasing investment in retrofitting existing maritime fleets.

- Technological advancements enhancing scrubber efficiency and reducing footprint.

- Integration of smart monitoring and data analytics for performance optimization.

- Focus on cost-effective compliance solutions amidst fluctuating fuel prices.

AI Impact Analysis on Ship Exhaust Gas Scrubber

Artificial intelligence is increasingly influencing the Ship Exhaust Gas Scrubber Market, primarily by enhancing operational intelligence, predictive maintenance, and overall system optimization. AI-driven platforms can process vast amounts of data from scrubber operations, including exhaust gas composition, fuel consumption, and environmental conditions, to provide real-time insights. This capability allows for proactive adjustments, improved compliance, and reduction in operational complexities, thereby significantly boosting the efficiency and reliability of scrubber systems across the maritime industry.

- AI-driven predictive maintenance reduces downtime and operational costs of scrubbers.

- Real-time optimization of scrubber performance based on environmental conditions and vessel operations.

- Enhanced data analysis for precise emissions monitoring and regulatory compliance reporting.

- Autonomous decision-making for optimal waste management and discharge strategies.

- Improved training and operational efficiency for crew through AI-powered simulations.

Key Takeaways Ship Exhaust Gas Scrubber Market Size & Forecast

- The market is poised for robust growth, driven primarily by ongoing regulatory pressures to curb sulfur oxide emissions.

- Significant investment in retrofitting existing fleets represents a major share of market expansion.

- Asia Pacific is anticipated to remain a dominant region, fueled by its extensive shipbuilding industry and high shipping traffic.

- Technological advancements in scrubber design and material science are contributing to market dynamism and product innovation.

- The economic viability of scrubbers compared to alternative low-sulfur fuels continues to influence adoption rates.

- The hybrid scrubber segment is expected to witness the fastest growth due to its operational flexibility.

- Market players are focusing on developing more compact and energy-efficient systems to meet diverse vessel requirements.

Ship Exhaust Gas Scrubber Market Drivers Analysis

The Ship Exhaust Gas Scrubber Market is predominantly driven by the imperative to comply with stringent environmental regulations imposed by international bodies and national governments. The International Maritime Organization's (IMO) 2020 sulfur cap has been a pivotal force, mandating a reduction in sulfur content in marine fuels, thus making exhaust gas scrubbers a viable and economically attractive compliance option for many shipowners. Beyond compliance, the growing global maritime trade increases the sheer volume of emissions, compelling greater adoption of abatement technologies. Furthermore, the economic advantage of continuing to use cheaper heavy fuel oil while meeting emission standards, as opposed to switching to more expensive low-sulfur fuels, provides a significant financial incentive for scrubber installation. Advancements in scrubber technology, leading to more compact, efficient, and reliable systems, also enhance their appeal, making them a more practical choice for a wider range of vessel types.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent IMO 2020 Sulfur Cap and Regional Regulations | +7.2% | Global, particularly ECA zones (North America, Europe, Asia) | Ongoing, Long-term (2025-2033) |

| Cost-effectiveness of Scrubbers vs. Low-Sulfur Fuel | +5.8% | Global, particularly for large vessel operators | Medium-term (2025-2029) |

| Increasing Global Seaborne Trade and Vessel Traffic | +3.5% | Asia Pacific, Europe, North America | Long-term (2025-2033) |

| Technological Advancements in Scrubber Systems | +2.8% | Global, focus on key maritime technology hubs | Ongoing, Long-term (2025-2033) |

| Growing Emphasis on Corporate Sustainability and ESG Compliance | +1.5% | Global, especially among publicly listed companies | Long-term (2025-2033) |

Ship Exhaust Gas Scrubber Market Restraints Analysis

Despite the strong drivers, the Ship Exhaust Gas Scrubber Market faces several significant restraints that could temper its growth trajectory. The initial high capital expenditure required for the purchase and installation of scrubber systems remains a substantial barrier for many shipowners, particularly smaller operators or those with older vessels nearing the end of their operational lives. Furthermore, the limited availability of drydock space and skilled labor for retrofitting operations can lead to extended vessel downtime, incurring additional costs and disrupting shipping schedules. Concerns regarding the disposal of wash water from open-loop scrubbers, particularly in sensitive environmental areas and ports with local bans, introduce uncertainty and operational complexities. The ongoing debate about the long-term environmental impact of wash water discharge and the potential for future regulatory changes beyond sulfur emissions, such as carbon pricing or stricter wastewater discharge limits, also creates a degree of hesitancy among potential investors. Lastly, the fluctuating price differential between compliant fuels and heavy fuel oil can diminish the economic attractiveness of scrubbers, particularly during periods of narrow spread.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Upfront Capital Expenditure and Installation Costs | -4.0% | Global, disproportionately affects smaller operators | Ongoing, Medium-term (2025-2029) |

| Limited Shipyard Capacity and Drydock Availability for Retrofits | -2.5% | Global, particularly major shipbuilding hubs | Short-to-Medium term (2025-2027) |

| Regulatory Uncertainty and Evolving Environmental Standards (beyond sulfur) | -1.8% | Global, especially Europe and North America | Long-term (2025-2033) |

| Concerns over Wash Water Disposal and Local Port Bans | -1.2% | Specific port jurisdictions (e.g., Baltic Sea, Singapore) | Ongoing, Medium-term (2025-2029) |

Ship Exhaust Gas Scrubber Market Opportunities Analysis

Opportunities within the Ship Exhaust Gas Scrubber Market are emerging from several strategic avenues, offering pathways for significant growth and innovation. The increasing global fleet size, driven by rising demand for goods and commodities, naturally expands the potential customer base for scrubber installations, both for new builds and retrofits. A significant opportunity lies in the development and adoption of advanced hybrid and closed-loop scrubber systems, which mitigate concerns associated with open-loop discharge and offer greater operational flexibility, particularly in regions with stricter environmental controls. Furthermore, the growing emphasis on sustainable shipping practices and the availability of green financing initiatives provide a favorable environment for investment in emission abatement technologies. Market players also have the opportunity to integrate scrubbers with broader vessel energy efficiency solutions, offering a more holistic approach to environmental compliance and operational cost reduction. The expansion into untapped emerging markets, where regulatory enforcement is strengthening, also represents a notable growth avenue for scrubber manufacturers and service providers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development and Adoption of Advanced Hybrid and Closed-Loop Systems | +6.5% | Global, particularly in environmentally sensitive regions | Medium-to-Long term (2026-2033) |

| Expansion into Emerging Markets with Strengthening Regulations | +4.0% | Asia Pacific (Southeast Asia), Latin America, MEA | Long-term (2027-2033) |

| Integration with Digitalization and Smart Shipping Solutions | +3.0% | Global, tech-savvy maritime clusters | Ongoing, Long-term (2025-2033) |

| Green Financing and Investment Incentives for Sustainable Shipping | +2.5% | Europe, North America, key financial centers | Medium-term (2025-2030) |

Ship Exhaust Gas Scrubber Market Challenges Impact Analysis

The Ship Exhaust Gas Scrubber Market navigates various challenges that demand strategic responses from industry participants. One primary challenge is the uncertainty surrounding long-term regulatory evolution, particularly concerning greenhouse gas emissions and stricter discharge limits, which could potentially diminish the long-term viability or perceived value of sulfur-focused scrubber investments. The fluctuating price spread between heavy fuel oil and compliant very low sulfur fuel oil (VLSFO) directly impacts the economic payback period for scrubbers; a narrow spread reduces the financial incentive for installation. Furthermore, the operational complexities associated with scrubber maintenance, waste sludge disposal, and ensuring consistent compliance across diverse operating conditions present ongoing technical and logistical hurdles. The competition from alternative decarbonization pathways and propulsion technologies, such as LNG, methanol, ammonia, or even future electric and hydrogen-powered vessels, poses a significant long-term challenge to the dominance of scrubber technology. Lastly, public perception and media scrutiny regarding the environmental impact of open-loop scrubber discharge, despite regulatory compliance, can create reputational risks for shipping companies and influence port state controls.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Uncertainty Regarding Future Environmental Regulations (beyond sulfur) | -3.0% | Global, especially regulatory bodies and policymakers | Long-term (2028-2033) |

| Fluctuating Fuel Price Spreads and Economic Payback Period | -2.0% | Global, impacting shipowners and investors | Short-to-Medium term (2025-2028) |

| Operational Complexities and Maintenance Requirements | -1.5% | Global, affecting vessel operators and crew training | Ongoing, Medium-term (2025-2030) |

| Competition from Alternative Compliance Options and Decarbonization Pathways | -1.0% | Global, impacting investment decisions | Long-term (2028-2033) |

Ship Exhaust Gas Scrubber Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Ship Exhaust Gas Scrubber Market, covering historical data, current market dynamics, and future growth projections. It meticulously examines market size, growth drivers, restraints, opportunities, and challenges across various segments and key regions. The report offers a detailed competitive landscape, profiling leading companies and their strategic initiatives, alongside a robust AI impact analysis. Tailored for business professionals and decision-makers, it delivers actionable insights to navigate the evolving maritime regulatory environment and capitalize on emerging market trends. The study’s scope encompasses both existing installations and anticipated new adoptions, providing a holistic view of the market's trajectory.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.5 billion |

| Market Forecast in 2033 | USD 16.45 billion |

| Growth Rate | 17.5% CAGR from 2025 to 2033 |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Alfa Laval, Wartsila, Yara Marine Technologies, Fuji Electric, Valmet, CR Ocean Engineering, Evoqua Water Technologies, Pacific Green Technologies, Clean Marine, Pureteq, ME Production, Andritz, Langh Tech, Saacke, Weihai Puyi Marine Environmental Technology, Shanghai Bluesoul Environmental Technology, Headway Technology, AEC Maritime, SunRui Marine Environment Engineering, EcoSpray Technologies |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

:The Ship Exhaust Gas Scrubber Market is comprehensively segmented to provide granular insights into its diverse components, facilitating a detailed understanding of market dynamics across various categories. This segmentation allows for precise analysis of adoption trends, technological preferences, and operational requirements across different vessel types and compliance strategies. Each segment is critically examined to highlight its contribution to the overall market growth and to identify specific opportunities and challenges.

- By Type:

- Open-Loop Scrubber: The most common and cost-effective type, using seawater for scrubbing and discharging treated water overboard. Predominantly adopted where discharge is permitted and convenient.

- Closed-Loop Scrubber: Utilizes an alkaline solution for scrubbing, storing the wash water onboard for later disposal ashore. Favored in areas with strict discharge regulations or in sensitive waters.

- Hybrid Scrubber: Offers the flexibility to switch between open-loop and closed-loop modes, providing operational adaptability to varying regulatory environments. This segment is gaining significant traction due to its versatile nature.

- By Application:

- New Builds: Scrubbers installed during the construction phase of new vessels, often integrated seamlessly into the ship's design. This segment benefits from long-term planning and optimized installation.

- Retrofit: Installation of scrubber systems on existing vessels to comply with current emission regulations. This segment accounts for a substantial portion of the market, driven by the existing global fleet.

- By Fuel Type:

- Heavy Fuel Oil (HFO): Scrubber systems specifically designed to remove sulfur from the exhaust gases when burning high-sulfur HFO. This remains a primary application due to HFO's lower cost.

- Marine Diesel Oil/Marine Gas Oil (MDO/MGO): While these fuels have lower sulfur content, scrubbers can still be applied for additional emission control or for vessels operating in ultra-low emission zones.

- Other Fuel Types: Includes emerging alternative fuels where exhaust gas treatment might still be necessary for specific pollutants or future regulations.

- By End-Use:

- Cargo Ships:

- Bulk Carriers: Large vessels transporting unpackaged bulk cargo like grain, coal, iron ore.

- Container Ships: Vessels designed to carry intermodal cargo containers.

- General Cargo Ships: Ships carrying packaged goods or break-bulk cargo.

- Tankers:

- Crude Oil Tankers: For transporting crude oil.

- Product Tankers: For refined petroleum products.

- Chemical Tankers: For various chemicals in bulk.

- Cruise Ships & Ferries: Passenger vessels with stringent environmental requirements due to their proximity to populated areas and sensitive marine environments.

- Offshore Vessels: Support vessels for offshore oil and gas operations.

- Other Vessels:

- RO-RO Ships: Roll-on/roll-off vessels for wheeled cargo.

- Naval Vessels: Military ships requiring specialized emission control.

- Cargo Ships:

Regional Highlights

-

Asia Pacific (APAC): This region stands as the undisputed leader in the Ship Exhaust Gas Scrubber Market, primarily due to its extensive shipbuilding industry, high volume of maritime trade, and the presence of major shipping lanes. Countries like China, South Korea, and Japan are at the forefront of both new vessel construction and retrofitting projects. The region's rapid economic growth and increasing port traffic contribute significantly to the demand for emission control technologies. Additionally, growing awareness and strengthening environmental regulations across several APAC nations further propel market expansion, particularly with the establishment of local emission control areas.

-

Europe: Europe represents a mature market driven by some of the world's most stringent environmental regulations, particularly in Emission Control Areas (ECAs) like the Baltic Sea and North Sea. European shipowners and operators have been early adopters of scrubber technology, prioritizing environmental compliance and sustainability. The region also benefits from a strong presence of advanced maritime technology providers and research institutions, fostering innovation in scrubber design and efficiency. The ongoing focus on green shipping initiatives and decarbonization goals continues to stimulate demand for advanced and hybrid scrubber systems.

-

North America: The North American market is characterized by strict domestic environmental regulations, especially in its coastal ECAs, such as those along the U.S. and Canadian coasts. The demand for scrubbers is driven by the need for compliance in these designated zones and across the Great Lakes. The region's significant port activity and high volume of vessel traffic, particularly for container and cruise ships, necessitate effective emission control solutions. While less focused on new builds than Asia, the retrofit segment is robust, as existing fleets operating in North American waters seek to ensure compliance and avoid penalties.

-

Middle East and Africa (MEA): This region is experiencing nascent but growing demand for ship exhaust gas scrubbers, primarily influenced by increasing oil and gas trade, expanding port infrastructure, and emerging environmental regulations in key maritime hubs. As countries within MEA strengthen their environmental policies and as major shipping routes pass through the region, the adoption of scrubbers is expected to accelerate. Investment in new builds and retrofits is gradually increasing, driven by international shipping lines operating in or through these waters.

-

Latin America: The Latin American market for ship exhaust gas scrubbers is in its developing stages, with growth primarily influenced by an increase in seaborne trade and the gradual adoption of international environmental standards. Key countries like Brazil and Mexico, with significant coastlines and port activities, are showing increasing interest in emission reduction technologies. While regulatory enforcement may vary, the desire for sustainable shipping practices and the movement of international vessels in their waters are expected to drive future market expansion, particularly for vessels involved in commodities export.

Top Key Players:

The market research report covers the analysis of key stake holders of the Ship Exhaust Gas Scrubber Market. Some of the leading players profiled in the report include -:- Alfa Laval

- Wartsila

- Yara Marine Technologies

- Fuji Electric

- Valmet

- CR Ocean Engineering

- Evoqua Water Technologies

- Pacific Green Technologies

- Clean Marine

- Pureteq

- ME Production

- Andritz

- Langh Tech

- Saacke

- Weihai Puyi Marine Environmental Technology

- Shanghai Bluesoul Environmental Technology

- Headway Technology

- AEC Maritime

- SunRui Marine Environment Engineering

- EcoSpray Technologies

Frequently Asked Questions:

What is a ship exhaust gas scrubber?

A ship exhaust gas scrubber, also known as an exhaust gas cleaning system (EGCS), is a technology installed on marine vessels to remove harmful pollutants, primarily sulfur oxides (SOx), from the ship's engine exhaust gases. These systems enable ships to continue using higher sulfur content fuel while complying with international and regional emission regulations, such as the IMO 2020 sulfur cap, by "scrubbing" the SOx before the gases are released into the atmosphere.

Why are ship exhaust gas scrubbers used in the maritime industry?

Ship exhaust gas scrubbers are primarily used to ensure compliance with stringent environmental regulations that limit sulfur emissions from marine vessels. The International Maritime Organization (IMO) has mandated a global 0.50% sulfur cap on fuel oil used by ships, effective January 1, 2020. By installing scrubbers, shipowners can continue to use cheaper heavy fuel oil (HFO) while chemically removing the sulfur oxides from the exhaust, thereby avoiding the higher costs associated with compliant low-sulfur fuels. This offers a cost-effective solution for environmental compliance.

What are the different types of ship exhaust gas scrubbers?

There are three main types of ship exhaust gas scrubbers: open-loop, closed-loop, and hybrid systems. Open-loop scrubbers use seawater to spray and absorb sulfur from the exhaust, then discharge the treated water back into the sea after monitoring. Closed-loop scrubbers use an alkaline solution, recirculating the wash water and storing the residual sludge onboard for disposal ashore, making them suitable for sensitive areas. Hybrid scrubbers offer the flexibility to operate in either open-loop or closed-loop mode, allowing ship operators to adapt to varying regulations and environmental conditions across different sailing areas.

What is the impact of IMO 2020 on the Ship Exhaust Gas Scrubber Market?

The IMO 2020 regulation, which significantly reduced the global sulfur cap for marine fuel from 3.5% to 0.50%, has been a monumental driver for the Ship Exhaust Gas Scrubber Market. This regulation compelled shipowners to either switch to more expensive compliant fuels or invest in scrubbers. For many, installing scrubbers presented a viable economic alternative, leading to a surge in demand for both new build installations and retrofitting projects globally. The regulation fundamentally reshaped the competitive landscape and accelerated the adoption of emission abatement technologies across the maritime industry, making scrubbers a critical component of compliance strategies.

What are the operational benefits of installing exhaust gas scrubbers?

Beyond regulatory compliance, installing exhaust gas scrubbers offers several operational benefits for shipowners. Firstly, it provides fuel flexibility, allowing vessels to continue burning readily available and often cheaper heavy fuel oil, which can lead to significant cost savings over time compared to high-priced low-sulfur fuels. Secondly, it reduces the need for frequent bunkering of different fuel types, simplifying logistics. Thirdly, by addressing sulfur emissions, scrubbers help companies enhance their environmental performance and corporate social responsibility image. Finally, modern scrubbers are designed for high efficiency and reliability, contributing to overall operational stability and reducing the risk of non-compliance penalties.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted