Shallow Water Decommissioning Service Market

Shallow Water Decommissioning Service Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707898 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Shallow Water Decommissioning Service Market Size

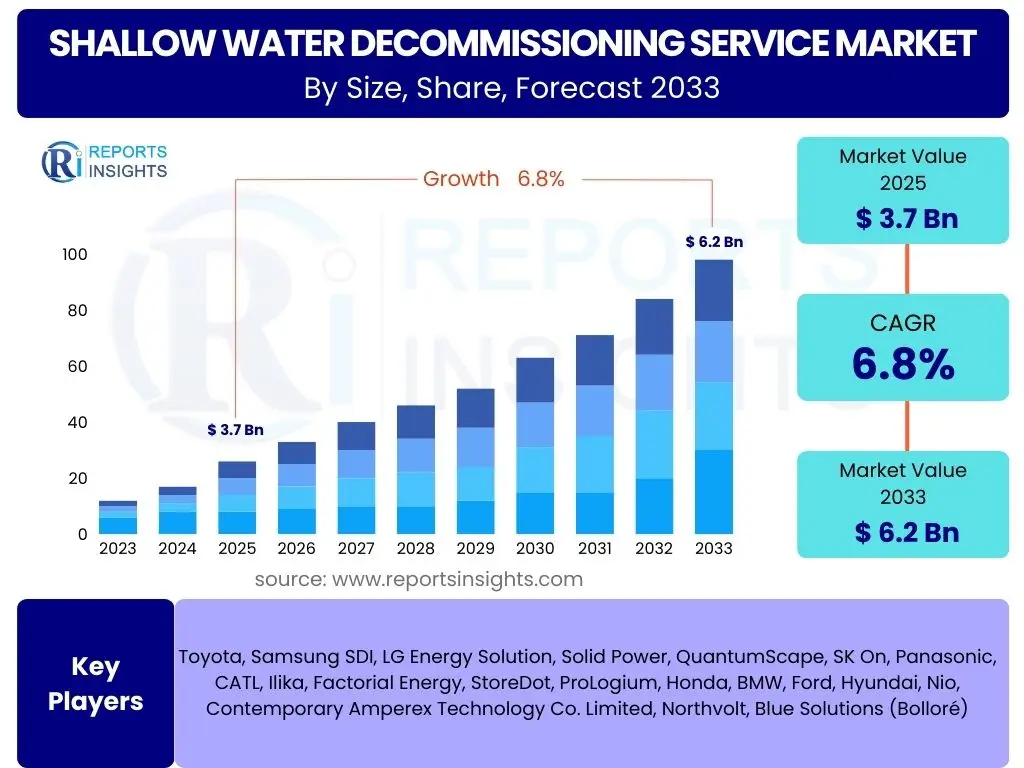

According to Reports Insights Consulting Pvt Ltd, The Shallow Water Decommissioning Service Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 3.7 Billion in 2025 and is projected to reach USD 6.2 Billion by the end of the forecast period in 2033. This growth is primarily driven by an increasing number of aging offshore assets reaching the end of their operational life, coupled with evolving regulatory frameworks that mandate responsible and timely decommissioning activities. The shallow water segment, characterized by its relatively lower operational complexities and costs compared to deepwater, continues to represent a significant portion of the total decommissioning expenditure globally.

The market's expansion is further supported by technological advancements aimed at improving efficiency and reducing the environmental footprint of decommissioning processes. Innovations in robotics, heavy lifting equipment, and waste management techniques are enabling more cost-effective and environmentally sound project execution. The geographical distribution of shallow water assets, predominantly concentrated in mature oil and gas basins such as the North Sea, Gulf of Mexico, and Southeast Asia, ensures a sustained demand for these specialized services throughout the forecast period. Companies are increasingly focusing on integrated service offerings to streamline projects and provide comprehensive solutions to operators, reflecting a trend towards full lifecycle asset management.

Key Shallow Water Decommissioning Service Market Trends & Insights

Analysis of common user questions reveals a strong interest in the evolving operational landscape, regulatory shifts, and technological innovations shaping the shallow water decommissioning service market. Users frequently inquire about the strategies service providers are adopting to manage costs, enhance safety, and comply with stringent environmental regulations. There is also a notable curiosity regarding the adoption of advanced techniques and the overall sustainability of decommissioning practices. The following insights address these key areas, highlighting the predominant trends influencing market dynamics and future growth trajectories.

- Integrated Service Models: A prominent trend is the shift towards integrated service models, where a single contractor or consortium manages the entire decommissioning project from planning and engineering to execution and site remediation. This approach aims to reduce project complexity, optimize costs, and enhance overall efficiency for asset owners.

- Technological Advancements: Continuous innovation in heavy lifting vessels, remote-operated vehicles (ROVs), autonomous underwater vehicles (AUVs), and advanced cutting tools is transforming decommissioning operations. These technologies improve safety, reduce human intervention in hazardous environments, and accelerate project timelines.

- Focus on Circular Economy and Re-use: Growing environmental awareness and sustainability mandates are driving efforts to maximize the reuse, repurpose, or recycle of decommissioned assets and materials. This trend seeks to minimize waste, reduce environmental impact, and potentially create new economic value from salvaged components.

- Stringent Regulatory Enforcement: Regulatory bodies worldwide are implementing and enforcing stricter guidelines for offshore decommissioning, particularly concerning environmental protection, waste disposal, and site clearance. This drives demand for specialized services that can ensure compliance and mitigate risks.

- Cost Optimization Strategies: With the fluctuating oil and gas prices, asset owners are increasingly seeking cost-effective decommissioning solutions. This pushes service providers to develop innovative contracting models, utilize advanced planning tools, and implement lean operational practices to drive down project expenditures without compromising safety or environmental standards.

- Digitalization and Data Analytics: The adoption of digital tools for project management, data analysis, and predictive maintenance is increasing. These tools help optimize planning, monitor operations in real-time, and make data-driven decisions, leading to more efficient and safer decommissioning projects.

AI Impact Analysis on Shallow Water Decommissioning Service

User inquiries regarding the impact of Artificial Intelligence (AI) on the Shallow Water Decommissioning Service market reveal a blend of optimism about efficiency gains and concerns about implementation challenges. Key themes include the potential for AI to optimize project planning, enhance safety protocols, and streamline complex operational workflows. There is significant interest in how AI can contribute to predictive maintenance for equipment, improve risk assessment, and process vast amounts of data generated during decommissioning projects. However, users also express concerns about the initial investment costs, the need for specialized AI expertise, and data privacy implications, suggesting a cautious yet forward-looking approach to AI adoption within the industry.

The integration of AI technologies is anticipated to revolutionize several aspects of shallow water decommissioning. By leveraging machine learning algorithms, project managers can develop more accurate schedules, forecast potential delays, and optimize resource allocation. Computer vision systems, often powered by AI, can enhance the inspection of subsea structures, identifying potential hazards or structural integrity issues with greater precision than traditional methods. Furthermore, AI-driven robotics can perform repetitive or dangerous tasks, significantly improving worker safety and reducing operational risks, thereby accelerating project execution while maintaining high safety standards.

- Enhanced Project Planning and Optimization: AI algorithms can analyze historical project data, weather patterns, and asset specifications to create highly optimized decommissioning plans, predict timelines, and allocate resources more efficiently, leading to cost savings and reduced project duration.

- Predictive Maintenance for Equipment: AI-powered sensors and analytics can monitor the health of heavy lifting equipment, vessels, and ROVs, predicting potential failures before they occur. This minimizes downtime, extends equipment lifespan, and enhances operational safety.

- Improved Risk Assessment and Safety: AI can process vast amounts of environmental and operational data to identify potential risks, forecast hazardous conditions, and develop proactive safety measures. This includes real-time monitoring of work sites and autonomous detection of anomalies.

- Automated Inspection and Data Analysis: AI-driven computer vision systems, integrated with ROVs and drones, can perform highly accurate visual inspections of structures, pipelines, and seabed conditions. They can quickly analyze imagery to detect corrosion, damage, or debris, vastly improving the efficiency and thoroughness of surveys.

- Robotics and Autonomous Systems: AI enables more sophisticated robotic systems to perform complex or dangerous tasks, such as cutting, cleaning, and material handling, with greater precision and autonomy, reducing human exposure to risks.

- Environmental Impact Monitoring: AI can be used to process data from environmental sensors, helping to monitor and predict the environmental impact of decommissioning activities, such as sediment dispersion or contaminant release, allowing for timely mitigation strategies.

Key Takeaways Shallow Water Decommissioning Service Market Size & Forecast

Common user questions regarding key takeaways from the Shallow Water Decommissioning Service market size and forecast consistently point towards the substantial growth trajectory and the underlying drivers. Users are primarily interested in understanding the core reasons for market expansion, the financial implications for stakeholders, and the sustained demand for specialized services. The following points summarize the essential insights, highlighting the market's robust growth potential, the critical role of regulatory pressures, and the increasing importance of efficient and sustainable operational practices. These takeaways underscore a market poised for significant development over the next decade.

The market is experiencing a period of sustained growth, driven by a confluence of factors including an aging global asset base, increasingly stringent regulatory environments, and a concerted industry effort towards environmental stewardship. The forecast indicates a steady increase in decommissioning activity, creating ample opportunities for service providers offering innovative and cost-effective solutions. Stakeholders should recognize that while operational complexities remain, the imperative for timely and responsible decommissioning is paramount, ensuring a continuous demand curve throughout the forecast period. Furthermore, the emphasis on re-use and recycling of materials aligns with broader sustainability goals, adding another layer of value to decommissioning projects.

- Consistent Growth Trajectory: The market is projected for robust growth, indicating a steady increase in demand for shallow water decommissioning services from 2025 to 2033, driven by a global inventory of aging assets.

- Regulatory Compliance as a Primary Driver: Stricter environmental regulations and government mandates for asset retirement are the most significant catalysts for market expansion, compelling operators to decommission structures reaching end-of-life.

- Significant Market Value Expansion: The market size is set to grow from USD 3.7 Billion in 2025 to USD 6.2 Billion by 2033, showcasing substantial financial opportunities for service providers and investors.

- Technological Innovation is Key: Advancements in heavy lift capabilities, remote operations, and waste management are critical for driving efficiency, reducing costs, and ensuring safety in decommissioning projects.

- Sustainability Focus: Increasing emphasis on environmental protection and the circular economy dictates that decommissioning activities prioritize material reuse, recycling, and minimal ecological impact.

- Geographic Concentrations: Major mature oil and gas basins globally, such as the North Sea, Gulf of Mexico, and Southeast Asia, will remain primary hubs for decommissioning activities, offering concentrated market opportunities.

Shallow Water Decommissioning Service Market Drivers Analysis

The Shallow Water Decommissioning Service Market is significantly propelled by several crucial drivers that reflect the evolving landscape of the global energy industry and environmental governance. Primarily, the aging infrastructure of offshore oil and gas assets, many of which were installed decades ago, has reached or is nearing the end of its operational life, necessitating their removal. This natural lifecycle progression creates a foundational demand for decommissioning services, as operators are legally and ethically obligated to address these structures. Moreover, the inherent safety risks associated with dilapidated offshore platforms and pipelines compel operators to initiate decommissioning processes promptly, further stimulating market activity and ensuring that these structures do not pose environmental or navigational hazards.

Another powerful driver is the increasingly stringent regulatory framework imposed by governments and international bodies across various regions. These regulations often mandate specific timelines, environmental standards, and reporting requirements for decommissioning activities, holding operators accountable for the full lifecycle of their assets. Non-compliance can result in substantial penalties, thereby incentivizing proactive decommissioning planning and execution. Coupled with this, the growing global emphasis on environmental protection and sustainability exerts pressure on companies to adopt responsible practices, including the complete removal and site remediation of offshore facilities. This societal and regulatory push reinforces the market's growth, making decommissioning an unavoidable and critical aspect of offshore operations rather than an optional endeavor.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Aging Offshore Infrastructure | +1.5% | Global, particularly North Sea, Gulf of Mexico, Southeast Asia | Mid-to-Long term (2025-2033) |

| Stricter Regulatory Frameworks & Compliance | +1.2% | Europe (UK, Norway), North America (USA), APAC (Australia, Malaysia) | Short-to-Mid term (2025-2029) |

| Increased Focus on Environmental Stewardship | +0.8% | Global, with strong emphasis in Europe and North America | Long term (2028-2033) |

| Decline in Economic Viability of Marginal Fields | +0.7% | Global, affecting smaller operators and older fields | Short-to-Mid term (2025-2029) |

| Technological Advancements in Decommissioning | +0.6% | Global, with key innovation hubs in Europe and North America | Mid-to-Long term (2027-2033) |

Shallow Water Decommissioning Service Market Restraints Analysis

Despite the strong drivers, the Shallow Water Decommissioning Service Market faces significant restraints that can temper its growth and introduce complexities for stakeholders. The most prominent restraint is the exceptionally high cost associated with decommissioning projects. These costs encompass a wide range of activities, from detailed planning and engineering to heavy lift operations, well abandonment, material disposal, and site remediation. The sheer capital expenditure required for even a single platform removal can be substantial, often running into hundreds of millions of dollars, which can strain the financial resources of operators, particularly smaller entities or those managing numerous aging assets.

Another critical restraint is the technical complexity and inherent risks involved in offshore decommissioning. Operations often take place in challenging marine environments, requiring specialized equipment, highly skilled personnel, and meticulous safety protocols. Unexpected weather conditions, structural integrity issues, or unforeseen environmental hazards can lead to project delays and cost overruns. Furthermore, the availability of specialized heavy-lift vessels and skilled workforce can sometimes be limited, particularly during periods of peak demand, leading to bottlenecks and increased service costs. Regulatory uncertainties and varying interpretation of guidelines across different jurisdictions can also pose challenges, creating inconsistencies in project requirements and potentially delaying approvals.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital & Operational Costs | -1.8% | Global, impacting all regions | Short-to-Long term (2025-2033) |

| Technical Complexity & Operational Risks | -1.3% | Global, particularly challenging environments | Short-to-Mid term (2025-2029) |

| Limited Availability of Specialized Assets & Skilled Personnel | -0.9% | Global, especially during high demand periods | Mid-term (2027-2031) |

| Regulatory Ambiguities & Evolving Standards | -0.7% | Region-specific, e.g., nascent regulatory frameworks in new O&G regions | Mid-term (2026-2030) |

| Uncertainty in Oil & Gas Price Fluctuations | -0.5% | Global, impacting investment decisions | Short-term (2025-2027) |

Shallow Water Decommissioning Service Market Opportunities Analysis

The Shallow Water Decommissioning Service Market presents numerous opportunities for growth and innovation, driven by the expanding scope of decommissioning needs and technological advancements. One significant opportunity lies in the development and adoption of innovative technologies that can enhance efficiency, reduce costs, and improve safety. This includes advanced robotics, automation, and digital twins for predictive modeling and project management. Service providers who invest in these cutting-edge solutions can gain a competitive advantage by offering more streamlined and cost-effective decommissioning projects, appealing to operators facing budget constraints and strict deadlines. The continuous development of specialized vessels and equipment for heavy lifts and subsea operations also opens new avenues for optimized project execution.

Another key opportunity emerges from the growing emphasis on environmental sustainability and the circular economy. This trend creates demand for services focused on maximizing the reuse, recycling, and repurposing of decommissioned materials. Companies that can provide comprehensive waste management solutions, including material segregation, processing, and off-take agreements for salvaged steel, concrete, and other valuable components, stand to capture significant market share. Furthermore, the expansion into new geographical regions with maturing shallow water assets, particularly in emerging oil and gas producing nations, offers untapped market potential. Collaborations and strategic partnerships between technology providers, engineering firms, and environmental consultants can also lead to integrated, holistic service offerings that address the complex multifaceted requirements of modern decommissioning projects.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technological Innovation & Automation Adoption | +1.3% | Global, strong in technologically advanced markets (Europe, North America) | Mid-to-Long term (2027-2033) |

| Expansion into Emerging Markets | +1.0% | APAC (Vietnam, Indonesia), Latin America (Brazil, Mexico), West Africa | Mid-to-Long term (2028-2033) |

| Focus on Circular Economy & Material Repurposing | +0.9% | Global, particularly Europe with strong sustainability mandates | Mid-term (2026-2031) |

| Integrated Service Offerings & Strategic Alliances | +0.7% | Global, all major decommissioning markets | Short-to-Mid term (2025-2029) |

| Growth in Pipeline & Subsea Infrastructure Decommissioning | +0.6% | Global, particularly North Sea, Gulf of Mexico | Long term (2028-2033) |

Shallow Water Decommissioning Service Market Challenges Impact Analysis

The Shallow Water Decommissioning Service Market, despite its growth prospects, faces a distinct set of challenges that can significantly impact project execution and market stability. One primary challenge is managing the immense project costs, which often escalate due to unforeseen circumstances, complex engineering requirements, and the fluctuating prices of materials and labor. Operators frequently struggle with accurately estimating and budgeting for decommissioning projects, leading to financial pressures and the potential for delayed or protracted operations. The economic sensitivity of the oil and gas industry means that downturns in crude prices can lead to reduced investment in decommissioning, as companies prioritize core production activities, thereby impacting the market's consistent demand.

Another significant hurdle involves the complex and often conflicting regulatory landscape across different jurisdictions. Varied requirements for waste disposal, environmental impact assessments, and site clearance can create compliance difficulties for international service providers and operators working across multiple regions. This regulatory inconsistency can lead to increased administrative burdens, legal risks, and the need for highly specialized local expertise. Furthermore, the industry grapples with the environmental and safety risks inherent in offshore operations. Protecting marine ecosystems during removal, managing hazardous waste, and ensuring the safety of personnel are paramount concerns that require rigorous planning, advanced techniques, and continuous vigilance, adding layers of complexity and cost to every project.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Escalating Project Costs & Budget Overruns | -1.5% | Global, impacting all major markets | Short-to-Long term (2025-2033) |

| Complex & Inconsistent Regulatory Frameworks | -1.0% | Region-specific, particularly in newer decommissioning markets | Mid-term (2026-2030) |

| Environmental & Safety Risks of Operations | -0.8% | Global, affecting all projects in sensitive marine environments | Short-to-Long term (2025-2033) |

| Availability & Mobilization of Specialized Assets | -0.6% | Global, during periods of high demand or remote locations | Mid-term (2027-2031) |

| Public Perception & Stakeholder Engagement | -0.4% | Globally, especially in environmentally conscious regions | Long term (2028-2033) |

Shallow Water Decommissioning Service Market - Updated Report Scope

This market insights report provides a comprehensive analysis of the Shallow Water Decommissioning Service market, detailing its current size, historical performance, and future growth projections. It encapsulates critical market trends, drivers, restraints, opportunities, and challenges that shape the industry landscape. The scope includes an in-depth assessment of AI's transformative impact, key takeaways for stakeholders, and a detailed segmentation analysis, alongside regional highlights. The report aims to furnish decision-makers with actionable intelligence to navigate market complexities and capitalize on emerging prospects within the shallow water decommissioning sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.7 Billion |

| Market Forecast in 2033 | USD 6.2 Billion |

| Growth Rate | 6.8% CAGR |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Decom Services International, Ocean Decommissioning Solutions, Northsea Offshore Removal, Global Marine Decom, Aqua Decom Partners, Continental Decommissioning, Apex Offshore Solutions, Subsea Decommissioning Group, Horizon Energy Services, Marine Asset Retirement, Blue Ocean Decom, Zenith Decommissioning, Deepwater Decom Solutions, Polaris Offshore Services, Trident Decommissioning, Pacific Basin Decom, Stellar Offshore Retirement, Coastal Decommissioning Group, Terra Marine Decom, Vanguard Decommissioning Systems |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Shallow Water Decommissioning Service market is comprehensively segmented to provide a detailed understanding of its various facets and operational components. This segmentation allows for targeted analysis of specific market dynamics, technological requirements, and regulatory implications across different service types, asset types, water depths, and end-users. Each segment plays a crucial role in shaping the overall market, reflecting the diverse needs and complexities inherent in offshore decommissioning projects. By examining these distinct categories, stakeholders can identify niche opportunities, understand competitive landscapes, and tailor their strategies to specific market demands. The inherent characteristics of shallow water environments often lead to different approaches and technologies compared to deepwater, making these segmentations particularly relevant for strategic planning.

Further granularity within these segments helps in identifying evolving trends, such as the increasing demand for integrated waste management solutions or the specialized needs for pipeline and subsea infrastructure removal. The differentiation by asset type highlights the varying technical challenges and equipment requirements for dismantling fixed platforms versus subsea wells. Meanwhile, segmenting by end-user clarifies who the primary clients are and their specific compliance and operational priorities. This structured breakdown is essential for market participants to accurately assess potential growth areas, develop tailored service offerings, and navigate the complex regulatory and operational environment of shallow Water Decommissioning.

- By Service Type

- Project Management & Engineering: Encompasses planning, design, regulatory liaison, and overall project oversight.

- Well Decommissioning: Focuses on plug and abandonment (P&A) operations for offshore wells.

- Platform Removal: Involves the dismantling and removal of topsides and jackets.

- Subsea Decommissioning: Covers the removal of subsea trees, manifolds, pipelines, and other submerged infrastructure.

- Waste Management: Includes handling, treatment, and disposal of all hazardous and non-hazardous materials.

- Site Remediation: Involves seabed clearance, environmental monitoring, and restoration of the marine environment.

- By Asset Type

- Fixed Platforms: Traditional steel jacket platforms and concrete gravity-based structures.

- Jack-up Rigs: Mobile drilling units, sometimes used for well interventions during decommissioning.

- Floating Production Systems (FPS): Including FPSOs, TLPs, and Semi-submersibles.

- Subsea Infrastructure: Pipelines & Flowlines, Umbilicals, Manifolds & Risers.

- By Depth Range

- Very Shallow Water (0-50 meters)

- Shallow Water (50-125 meters)

- By End-User

- Oil & Gas Operators: Primary clients responsible for asset retirement obligations.

- Government & Regulatory Bodies: Influencing policies and sometimes directly involved in orphaned asset decommissioning.

- Contractors & Service Providers: Companies specializing in offering various decommissioning services.

Regional Highlights

The Shallow Water Decommissioning Service Market exhibits distinct regional characteristics driven by varying levels of oil and gas maturity, regulatory stringency, and economic factors. North America, particularly the Gulf of Mexico, represents a significant market due to its extensive history of offshore exploration and production, leading to a large inventory of aging shallow water assets. The region faces substantial decommissioning backlogs, propelled by federal and state regulations, which mandate timely removal and site clearance. This creates a sustained demand for a wide range of decommissioning services, from well P&A to platform removal and subsea infrastructure. Operators here often seek cost-efficient solutions due to the competitive market and fluctuating energy prices, fostering innovation in project execution and waste management.

Europe, spearheaded by the North Sea, is another crucial region, known for its stringent environmental regulations and well-established decommissioning frameworks. Countries like the UK and Norway have pioneered integrated decommissioning strategies, emphasizing environmental protection and material reuse. The region's mature basins are witnessing a continuous wave of decommissioning projects, often involving complex heavy-lift operations and advanced waste processing. Asia Pacific is emerging as a rapidly growing market, driven by aging infrastructure in countries like Malaysia, Indonesia, and Australia, coupled with increasing regulatory focus on environmental accountability. Latin America and the Middle East & Africa (MEA) are also expected to see increased activity, as their older fields approach end-of-life and regulatory landscapes mature, presenting new opportunities for international service providers capable of adapting to diverse operational and cultural contexts.

- North America (United States, Canada, Mexico): Dominant market due to the vast number of mature shallow water assets in the Gulf of Mexico. Strong regulatory push and a focus on cost-efficient solutions drive market activity.

- Europe (UK, Norway, Netherlands, Denmark): A mature market with highly stringent environmental regulations and a significant pipeline of decommissioning projects, particularly in the North Sea. Emphasis on innovation, sustainability, and integrated project management.

- Asia Pacific (Malaysia, Indonesia, Australia, Vietnam, Thailand): An emerging growth market with a growing number of aging assets and developing regulatory frameworks. Increased focus on local content and capacity building.

- Latin America (Brazil, Mexico, Venezuela): Gradual increase in decommissioning activities as older fields mature. Market growth is influenced by national oil company strategies and evolving local regulations.

- Middle East & Africa (Saudi Arabia, UAE, Nigeria, Angola): Anticipated growth in decommissioning due to aging assets in key producing nations and slowly strengthening regulatory environments. Opportunities for specialized services in complex operational zones.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Shallow Water Decommissioning Service Market.- Decom Services International

- Ocean Decommissioning Solutions

- Northsea Offshore Removal

- Global Marine Decom

- Aqua Decom Partners

- Continental Decommissioning

- Apex Offshore Solutions

- Subsea Decommissioning Group

- Horizon Energy Services

- Marine Asset Retirement

- Blue Ocean Decom

- Zenith Decommissioning

- Deepwater Decom Solutions

- Polaris Offshore Services

- Trident Decommissioning

- Pacific Basin Decom

- Stellar Offshore Retirement

- Coastal Decommissioning Group

- Terra Marine Decom

- Vanguard Decommissioning Systems

Frequently Asked Questions

What is the projected growth rate for the Shallow Water Decommissioning Service Market?

The Shallow Water Decommissioning Service Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, reaching USD 6.2 Billion by 2033.

What are the primary drivers of growth in this market?

Key drivers include aging offshore oil and gas infrastructure, increasingly stringent global regulatory frameworks, and a growing industry focus on environmental stewardship and sustainable asset retirement practices.

How is AI impacting shallow water decommissioning operations?

AI is significantly impacting operations through enhanced project planning, predictive maintenance for equipment, improved risk assessment and safety protocols, automated inspection via ROVs, and more sophisticated robotics for complex tasks.

Which geographical regions are most significant for shallow water decommissioning?

North America (Gulf of Mexico) and Europe (North Sea) are currently the most significant regions, driven by extensive mature assets and stringent regulations. Asia Pacific is an emerging growth market.

What are the main challenges faced by the Shallow Water Decommissioning Service Market?

Major challenges include high capital and operational costs, the technical complexity and inherent risks of offshore operations, potential regulatory inconsistencies across different jurisdictions, and the limited availability of specialized assets and skilled personnel during peak demand.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted