Physical Vapor Deposition Coating Service Market

Physical Vapor Deposition Coating Service Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705560 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

Physical Vapor Deposition Coating Service Market Size

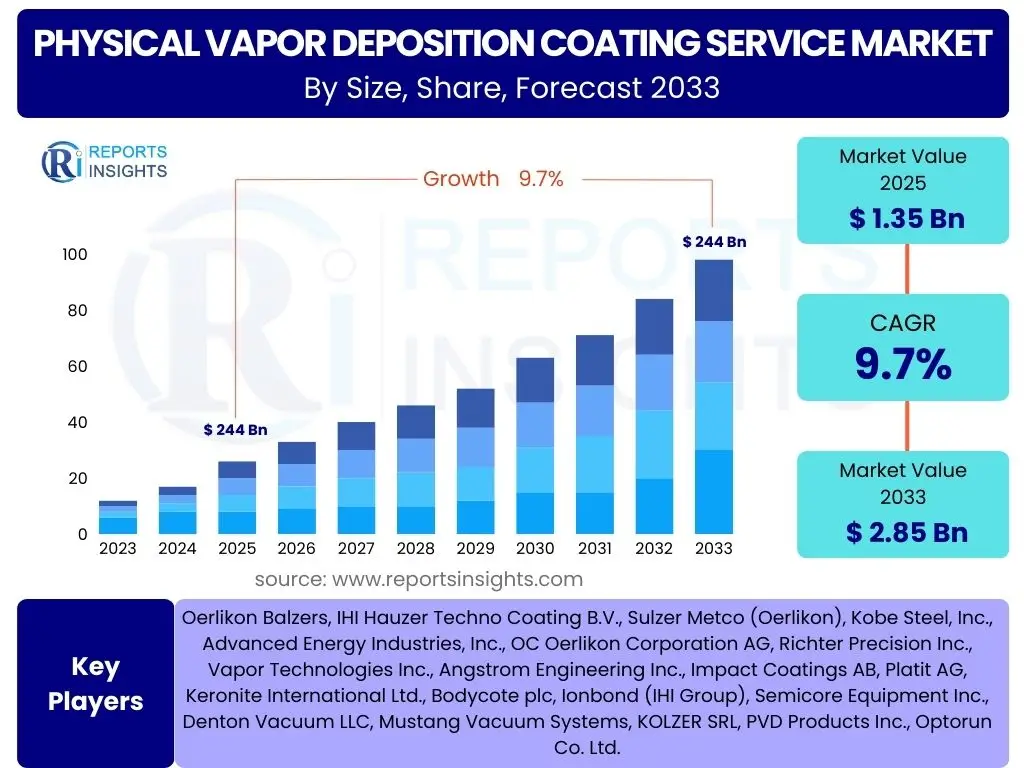

According to Reports Insights Consulting Pvt Ltd, The Physical Vapor Deposition Coating Service Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.7% between 2025 and 2033. The market is estimated at USD 1.35 Billion in 2025 and is projected to reach USD 2.85 Billion by the end of the forecast period in 2033.

Key Physical Vapor Deposition Coating Service Market Trends & Insights

The Physical Vapor Deposition (PVD) Coating Service market is currently experiencing dynamic shifts driven by advancements in material science and increasing demand for high-performance surface solutions. A prominent trend involves the growing adoption of PVD coatings in emerging applications such as electric vehicle components and wearable technology, where enhanced durability, lightweight properties, and aesthetic appeal are critical. Furthermore, there is a clear move towards multi-layered and multi-functional coatings that can offer a combination of properties, such as wear resistance, corrosion protection, and biocompatibility, catering to more complex industrial requirements.

Another significant insight into the market indicates a strong focus on customization and application-specific solutions. Service providers are increasingly investing in research and development to tailor coating properties, thickness, and composition to meet the precise demands of diverse industries, from medical devices requiring inert surfaces to aerospace components needing extreme heat and wear resistance. This bespoke approach, coupled with advancements in deposition technologies like High Power Impulse Magnetron Sputtering (HiPIMS) and cathodic arc evaporation, is enabling the development of superior coatings that were previously unachievable, thereby expanding the market's addressable opportunities and driving innovation.

- Increased demand for thin-film coatings in miniaturized electronic components.

- Rising adoption in electric vehicle (EV) battery components and powertrains for enhanced durability and thermal management.

- Development of advanced multi-layered and hybrid PVD coatings for superior performance.

- Growing integration of PVD with other surface modification technologies for synergistic effects.

- Emphasis on environmentally friendly and sustainable PVD processes to reduce chemical waste.

- Expansion into new applications like smart coatings, flexible electronics, and augmented reality devices.

AI Impact Analysis on Physical Vapor Deposition Coating Service

Artificial Intelligence (AI) is poised to significantly transform the Physical Vapor Deposition (PVD) Coating Service market by enhancing process efficiency, quality control, and predictive maintenance. Users frequently inquire about how AI can optimize the complex parameters involved in PVD processes, such as vacuum levels, temperature, and material feed rates, to achieve desired coating properties with greater consistency. The expectation is that AI-driven algorithms will enable real-time adjustments, minimize defects, and reduce material waste, leading to substantial cost savings and improved operational throughput for coating service providers. This includes leveraging machine learning for anomaly detection during the coating process to preemptively address potential issues.

Furthermore, concerns and expectations revolve around AI's capacity for predictive analytics to forecast equipment maintenance needs and optimize production schedules, thereby maximizing equipment uptime and service capacity. Users also anticipate AI contributing to the development of novel coating materials and designs through computational material science and rapid prototyping. While there is enthusiasm for the potential for increased automation and precision, some common concerns include the initial investment required for AI integration, the need for skilled personnel to manage and interpret AI outputs, and data security issues related to proprietary process information. Despite these challenges, the prevailing sentiment is that AI will be a critical enabler for innovation and competitive advantage in the PVD coating service sector, driving a new era of intelligent manufacturing.

- AI-driven optimization of PVD process parameters for enhanced coating uniformity and adhesion.

- Predictive maintenance of PVD equipment reducing downtime and extending machine lifespan.

- Automated quality control systems identifying defects in real-time using machine vision and AI algorithms.

- Accelerated R&D for new coating materials and compositions through AI-powered simulation and data analysis.

- Improved energy efficiency in PVD processes by optimizing power consumption based on AI insights.

- Enhanced supply chain management and demand forecasting for coating materials using AI.

Key Takeaways Physical Vapor Deposition Coating Service Market Size & Forecast

The Physical Vapor Deposition (PVD) Coating Service market is on a robust growth trajectory, driven by an escalating demand for high-performance surface solutions across diverse industries. A key takeaway is the consistent expansion fueled by technological advancements that enable more precise, durable, and functional coatings, making PVD an indispensable process for modern manufacturing. The market's significant Compound Annual Growth Rate (CAGR) from 2025 to 2033 underscores its critical role in enhancing product lifespan, performance, and aesthetic appeal in applications ranging from consumer electronics to highly specialized medical devices.

Another crucial insight from the market forecast is the increasing specialization within PVD services, moving beyond general-purpose coatings to application-specific, multi-functional layers. This shift is particularly evident in sectors like electric vehicles, aerospace, and advanced medical implants, where stringent performance requirements necessitate tailored coating solutions. The projected market value by 2033 highlights a sustained investment in research and development, capacity expansion, and the adoption of advanced PVD technologies, signaling a mature yet evolving market poised for continued innovation and widespread industrial integration.

- Market demonstrates strong and sustained growth, projected to more than double by 2033.

- Technological advancements in PVD techniques are a primary growth catalyst.

- Demand is highly diversified across critical industries including automotive, medical, and electronics.

- Increasing emphasis on customized and multi-functional coating solutions drives market value.

- Environmental sustainability and cost-efficiency are becoming significant competitive factors.

Physical Vapor Deposition Coating Service Market Drivers Analysis

The Physical Vapor Deposition (PVD) Coating Service market is propelled by a confluence of factors, primarily the escalating demand for enhanced material performance across numerous industrial sectors. Industries such as automotive, aerospace, and medical devices are increasingly reliant on PVD coatings to impart superior wear resistance, corrosion protection, and hardness to components, thereby extending their lifespan and improving operational efficiency. This critical need for durable and high-performing surfaces in demanding environments acts as a foundational driver for market expansion, pushing manufacturers to seek specialized coating services.

Furthermore, the miniaturization trend in consumer electronics and the rapid growth of the electric vehicle (EV) market are significant accelerators. PVD coatings enable the production of smaller, more efficient electronic components and are vital for protecting battery electrodes, motor parts, and various other EV components from wear and corrosion. The aesthetic appeal and functional benefits, such as anti-reflection properties in optics or biocompatibility in medical implants, further broaden the application scope of PVD technology, positioning it as an indispensable solution for modern product development.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for High-Performance Coatings | +2.1% | Global, particularly North America, Europe, Asia Pacific | Short-term to Long-term (2025-2033) |

| Growth in Automotive (EV) and Aerospace Industries | +1.8% | North America, Europe, China, Japan | Mid-term to Long-term (2027-2033) |

| Miniaturization in Consumer Electronics | +1.5% | Asia Pacific (China, South Korea), North America | Short-term to Mid-term (2025-2030) |

| Advancements in Medical Device Manufacturing | +1.3% | North America, Europe | Mid-term (2026-2031) |

| Strict Regulatory Standards for Product Durability and Safety | +1.0% | Global, particularly developed economies | Short-term to Long-term (2025-2033) |

Physical Vapor Deposition Coating Service Market Restraints Analysis

Despite its significant advantages, the Physical Vapor Deposition (PVD) Coating Service market faces several inherent restraints that can temper its growth. A primary challenge is the high capital investment required for PVD equipment and the associated operational costs, including energy consumption and specialized maintenance. This substantial initial outlay can be a barrier for smaller enterprises or those in developing regions seeking to adopt PVD technology, limiting market penetration and fostering reliance on established, larger service providers. Furthermore, the complexity of PVD processes demands highly skilled labor for operation and quality control, leading to potential workforce shortages and increased labor costs.

Another significant restraint involves the material compatibility limitations and the specific substrate requirements for effective PVD application. Not all materials are suitable for PVD processing, and certain geometries or substrate properties can preclude the use of this technology, thereby limiting its applicability in some niche areas. Additionally, the batch processing nature of many PVD systems can impact throughput and efficiency for high-volume production, potentially making it less competitive compared to alternative coating methods like electroplating or chemical vapor deposition (CVD) in certain industrial scenarios. The environmental regulations surrounding the handling of certain target materials and waste disposal also add layers of complexity and cost, particularly in highly regulated regions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Investment and Operational Costs | -1.5% | Global, particularly emerging economies | Short-term to Long-term (2025-2033) |

| Complexity of PVD Processes and Need for Skilled Labor | -1.2% | Global | Short-term to Mid-term (2025-2030) |

| Material Compatibility and Substrate Limitations | -1.0% | Specific niche markets globally | Short-term to Long-term (2025-2033) |

| Competition from Alternative Coating Technologies | -0.8% | Global | Short-term to Mid-term (2025-2030) |

| Environmental Regulations and Waste Management | -0.7% | Europe, North America, parts of Asia Pacific | Mid-term to Long-term (2027-2033) |

Physical Vapor Deposition Coating Service Market Opportunities Analysis

Significant opportunities abound in the Physical Vapor Deposition (PVD) Coating Service market, primarily driven by the continuous innovation in material science and the emergence of new application areas. The increasing focus on sustainability and eco-friendly manufacturing processes presents a substantial opportunity for PVD, as it is inherently cleaner than many traditional coating methods due to its dry process and minimal chemical waste. This aligns well with global environmental mandates and corporate sustainability initiatives, positioning PVD as a preferred choice for future-proof surface engineering solutions. Furthermore, the integration of PVD with additive manufacturing (3D printing) holds immense potential, enabling the creation of complex geometries with high-performance coated surfaces for specialized applications.

The expansion into emerging markets, particularly in Asia Pacific and Latin America, offers fertile ground for growth, as industrialization and technological adoption accelerate in these regions. Demand for durable tools, automotive components, and consumer electronics is surging, creating a robust market for PVD services. Moreover, the development of smart coatings, which can adapt to environmental changes or provide sensing capabilities, opens up entirely new frontiers for PVD technology. These advanced coatings, capable of self-healing or real-time performance monitoring, represent a premium segment that PVD service providers are uniquely positioned to address, driving higher value-added services and market differentiation.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Sustainable and Eco-Friendly Coatings | +1.9% | Global, particularly Europe, North America | Mid-term to Long-term (2027-2033) |

| Emergence of Advanced Functional Coatings (e.g., Smart Coatings) | +1.7% | North America, Europe, Japan, South Korea | Mid-term to Long-term (2026-2033) |

| Integration with Additive Manufacturing (3D Printing) | +1.5% | Global, R&D focused regions | Long-term (2028-2033) |

| Expansion into New Geographic Markets | +1.2% | Asia Pacific (Southeast Asia, India), Latin America, MEA | Short-term to Long-term (2025-2033) |

| Increasing R&D Investments in Material Science | +1.0% | Global, leading research hubs | Long-term (2028-2033) |

Physical Vapor Deposition Coating Service Market Challenges Impact Analysis

The Physical Vapor Deposition (PVD) Coating Service market faces several formidable challenges that can influence its growth trajectory. One significant challenge is the ongoing need for precise process control and consistency, especially for high-volume or intricate components. Achieving uniform coating thickness and desired properties across diverse substrates and complex geometries remains a technical hurdle, often requiring extensive calibration and skilled oversight. Inconsistent quality can lead to rework, increased costs, and reputational damage for service providers, hindering broader adoption in highly sensitive applications.

Another key challenge is managing the intellectual property surrounding proprietary coating recipes and advanced PVD technologies. As companies invest heavily in developing unique coating solutions, protecting these innovations from imitation is crucial. Furthermore, the rapid pace of technological change necessitates continuous investment in upgrading equipment and training personnel, posing a financial burden and risk of obsolescence for service providers. The competitive landscape, characterized by both large, established players and agile specialized firms, also creates pressure on pricing and the need for constant differentiation through innovation and service excellence, which can be particularly challenging for new entrants or smaller businesses.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining Coating Consistency and Quality Across Batches | -1.3% | Global | Short-term to Mid-term (2025-2030) |

| High Cost of Research & Development and Technological Upgrades | -1.1% | Global, particularly developed regions | Mid-term to Long-term (2027-2033) |

| Intense Competition and Pricing Pressure | -0.9% | Global | Short-term to Long-term (2025-2033) |

| Complexity of Customizing Solutions for Niche Applications | -0.8% | Global, specialized markets | Short-term to Mid-term (2025-2030) |

| Ensuring Data Security and Intellectual Property Protection | -0.6% | Global | Long-term (2028-2033) |

Physical Vapor Deposition Coating Service Market - Updated Report Scope

This report provides an in-depth analysis of the Physical Vapor Deposition Coating Service Market, offering a comprehensive overview of market size, trends, drivers, restraints, opportunities, and challenges across various segments and key regions. It aims to deliver actionable insights to stakeholders, enabling informed strategic decision-making within the evolving landscape of advanced surface engineering. The scope encapsulates current market dynamics, historical data, and a forward-looking forecast up to 2033, examining the impact of technological advancements and industrial demands on market growth.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.35 Billion |

| Market Forecast in 2033 | USD 2.85 Billion |

| Growth Rate | 9.7% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Oerlikon Balzers, IHI Hauzer Techno Coating B.V., Sulzer Metco (Oerlikon), Kobe Steel, Inc., Advanced Energy Industries, Inc., OC Oerlikon Corporation AG, Richter Precision Inc., Vapor Technologies Inc., Angstrom Engineering Inc., Impact Coatings AB, Platit AG, Keronite International Ltd., Bodycote plc, Ionbond (IHI Group), Semicore Equipment Inc., Denton Vacuum LLC, Mustang Vacuum Systems, KOLZER SRL, PVD Products Inc., Optorun Co. Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Physical Vapor Deposition (PVD) Coating Service market is extensively segmented to reflect the diverse range of technologies, applications, materials, and end-use industries it serves. This granular segmentation provides a detailed understanding of the market's structure and the specific growth drivers within each category. The classification by type, including sputtering, evaporation, arc PVD, and ion plating, highlights the technological variations that cater to different performance requirements and substrate materials, influencing process efficiency and coating properties. Each type possesses unique characteristics, such as deposition rate, adhesion strength, and coating uniformity, which dictate their suitability for specific industrial applications.

Further segmentation by application areas such as automotive, medical, aerospace, and consumer electronics underscores the pervasive utility of PVD coatings in enhancing product durability, functionality, and aesthetic appeal. The market is also analyzed based on the types of materials deposited, including nitrides, carbides, oxides, and pure metals, reflecting the chemical versatility of PVD technology. This multi-dimensional segmentation allows for a precise evaluation of market dynamics, identifying high-growth segments and emerging opportunities for service providers looking to specialize or expand their offerings to meet evolving industrial demands and technological advancements.

- By Type: Sputtering, Evaporation, Arc PVD, Ion Plating

- By Application: Automotive Components, Medical Devices & Implants, Aerospace & Defense, Consumer Electronics, Industrial Tools & Components, Decorative Coatings, Optics & Glass, Energy

- By Material: Nitrides, Carbides, Oxides, Pure Metals, Carbon-based

- By End-Use Industry: Manufacturing, Healthcare, Automotive, Aerospace, Electronics, Energy, Defense

- By Service Type: Custom Coating, Batch Coating, Consulting & Development, Equipment Maintenance & Support

Regional Highlights

- North America: This region is a significant market for PVD coating services, driven by robust aerospace and defense sectors, advanced medical device manufacturing, and the burgeoning electric vehicle industry. The presence of key market players, high research and development investments, and stringent quality standards foster demand for high-performance and specialized coatings. Innovation in materials science and strong adoption of advanced manufacturing techniques further solidify North America's position as a leading market.

- Europe: Europe represents a mature yet continuously growing market for PVD coating services, largely due to its strong automotive industry, precision engineering, and industrial tool manufacturing sectors. Strict environmental regulations encourage the adoption of cleaner PVD technologies over traditional methods. Countries like Germany, France, and the UK are at the forefront of PVD technology adoption, emphasizing high-quality, durable, and functional coatings for a diverse range of applications.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region in the PVD coating service market, propelled by rapid industrialization, expanding manufacturing bases, and significant investments in consumer electronics, automotive, and general manufacturing. Countries such as China, Japan, South Korea, and India are key contributors, benefiting from lower labor costs and increasing domestic demand for coated products. The region's focus on technological advancements and mass production capabilities makes it a crucial hub for PVD services.

- Latin America: The PVD coating service market in Latin America is in its nascent stage but shows promising growth, particularly in automotive manufacturing (Mexico, Brazil) and industrial applications. Increasing foreign investments in manufacturing and growing awareness of advanced coating benefits are contributing to market expansion. While smaller in scale compared to other regions, the potential for growth in diverse industrial sectors remains significant.

- Middle East and Africa (MEA): The MEA region is experiencing gradual growth in the PVD coating service market, primarily driven by investments in infrastructure development, oil and gas industries, and emerging manufacturing sectors. The demand for corrosion-resistant and durable coatings for harsh environments is a key driver. As economies diversify and industrial capabilities expand, the adoption of advanced surface technologies like PVD is expected to increase steadily.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Physical Vapor Deposition Coating Service Market.- Oerlikon Balzers

- IHI Hauzer Techno Coating B.V.

- Sulzer Metco (Oerlikon)

- Kobe Steel, Inc.

- Advanced Energy Industries, Inc.

- OC Oerlikon Corporation AG

- Richter Precision Inc.

- Vapor Technologies Inc.

- Angstrom Engineering Inc.

- Impact Coatings AB

- Platit AG

- Keronite International Ltd.

- Bodycote plc

- Ionbond (IHI Group)

- Semicore Equipment Inc.

- Denton Vacuum LLC

- Mustang Vacuum Systems

- KOLZER SRL

- PVD Products Inc.

- Optorun Co. Ltd.

Frequently Asked Questions

What is Physical Vapor Deposition (PVD) coating?

Physical Vapor Deposition (PVD) is a vacuum deposition method used to produce thin films and coatings. It involves physical processes like sputtering or evaporation to deposit atoms or molecules from a solid source onto a substrate, forming a thin, durable, and adherent coating. This process is highly versatile, allowing for the creation of various metallic, ceramic, and composite coatings with excellent hardness, wear resistance, and corrosion protection.

What are the primary benefits of PVD coatings?

PVD coatings offer numerous benefits, including superior hardness and wear resistance, enhanced corrosion protection, improved aesthetics, and reduced friction. They significantly extend the lifespan of tools and components, reduce maintenance needs, and allow for the use of less expensive base materials. PVD is also an environmentally friendly process, as it does not typically involve harmful chemicals or generate toxic waste, unlike some traditional coating methods.

Which industries widely use PVD coating services?

PVD coating services are extensively utilized across a broad spectrum of industries. Key sectors include automotive (for engine parts, gears, decorative trim), medical (for surgical instruments, implants, biocompatible surfaces), aerospace and defense (for turbine blades, landing gear components), consumer electronics (for smartphone casings, display panels), and industrial tools (for cutting tools, molds, dies). Its versatility allows it to address diverse functional and aesthetic requirements.

How does PVD differ from Chemical Vapor Deposition (CVD)?

PVD differs from Chemical Vapor Deposition (CVD) primarily in their deposition mechanisms. PVD involves physical processes where material is vaporized from a solid source and deposited onto a substrate in a vacuum, without chemical reactions at the surface. In contrast, CVD uses chemical reactions between gaseous precursors at the substrate surface, often requiring higher temperatures. PVD generally operates at lower temperatures, making it suitable for a wider range of heat-sensitive substrates, and typically offers better adhesion for metallic coatings.

What are the future trends shaping the PVD coating market?

Future trends in the PVD coating market include a growing emphasis on multi-functional and smart coatings that can offer adaptive properties or sensing capabilities. The integration of PVD with additive manufacturing (3D printing) for creating advanced coated geometries is another key development. Furthermore, increasing demand from the electric vehicle sector, continued miniaturization in electronics, and a strong focus on sustainable and eco-friendly coating processes are expected to drive significant innovation and market expansion.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted