Separator Coating Material Market

Separator Coating Material Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702092 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Separator Coating Material Market Size

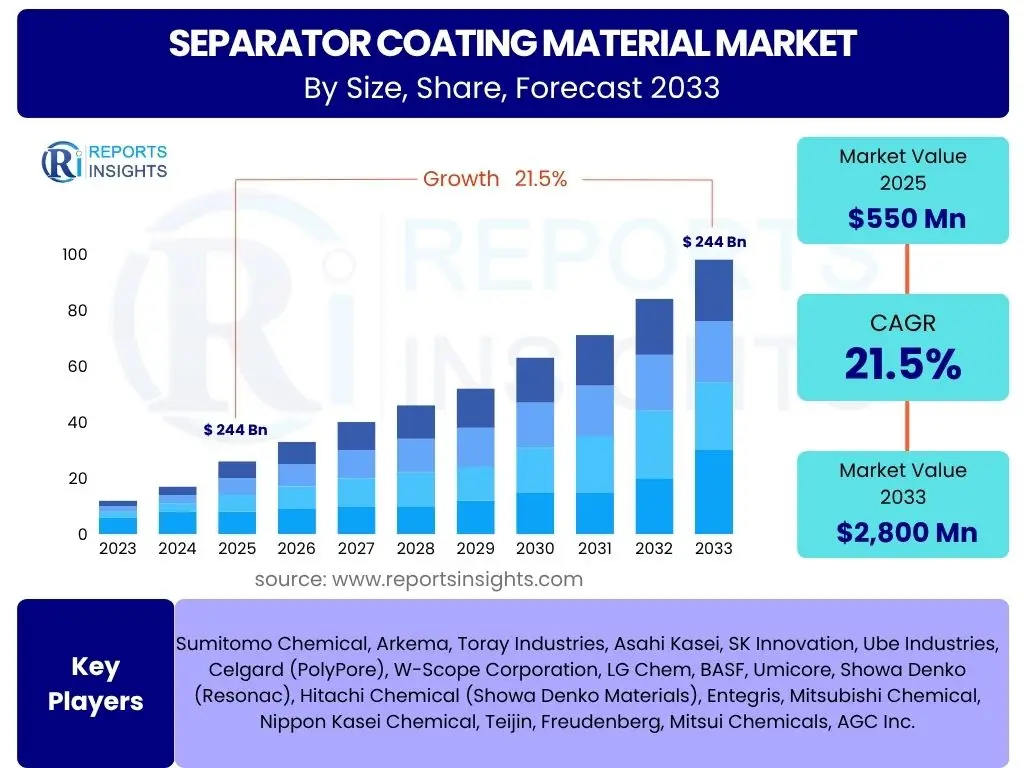

According to Reports Insights Consulting Pvt Ltd, The Separator Coating Material Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 21.5% between 2025 and 2033. The market is estimated at USD 550 million in 2025 and is projected to reach USD 2,800 million by the end of the forecast period in 2033.

Key Separator Coating Material Market Trends & Insights

The separator coating material market is experiencing significant transformation, driven primarily by the escalating demand for high-performance and safer battery solutions. Users are frequently inquiring about the latest innovations in coating materials, their role in enhancing battery energy density and cycle life, and the impact of electric vehicle (EV) proliferation on material demand. There is also considerable interest in how new coating technologies are addressing thermal runaway risks and improving overall battery longevity, particularly for applications requiring robust performance under extreme conditions.

Another area of widespread user interest revolves around the sustainability aspects of separator coating materials, including questions about environmentally friendly production processes, the use of recyclable materials, and the reduction of hazardous substances. The trend towards advanced ceramic and polymer coatings, which offer superior thermal stability and mechanical strength, is a key discussion point, along with the integration of multi-functional coatings designed to provide protection against dendrite formation and improve electrolyte wettability. Furthermore, the market is seeing a push towards thinner, more uniform coatings to maximize energy density without compromising safety.

- Increased adoption of ceramic-coated separators for enhanced thermal stability and safety in lithium-ion batteries.

- Development of multi-layered and hybrid coating materials to optimize performance characteristics such as porosity, mechanical strength, and ionic conductivity.

- Growing preference for polymer-based coatings offering flexibility and improved adhesion to separator substrates.

- Focus on environmentally friendly and sustainable coating processes and materials, including water-based solutions.

- Integration of advanced materials like aramid, polyimide, and alumina for superior heat resistance and anti-short circuit capabilities.

- Tailored coating solutions for specific battery chemistries and applications, including high-nickel cathodes and silicon anodes.

- Emphasis on ultra-thin and uniform coatings to maximize energy density and minimize internal resistance.

AI Impact Analysis on Separator Coating Material

Users frequently inquire about the transformative potential of Artificial Intelligence (AI) in the separator coating material domain. Key questions revolve around how AI can accelerate material discovery, optimize coating formulations, and enhance manufacturing processes for these critical battery components. There is keen interest in AI's capability to predict material performance under various conditions, thereby reducing the extensive and time-consuming experimental cycles traditionally required in R&D. Furthermore, stakeholders are exploring AI's role in establishing precise control over coating thickness and uniformity, which are crucial for battery safety and efficiency.

The application of AI extends beyond initial development to real-time production monitoring and quality control. Users are interested in how machine learning algorithms can detect defects in coating layers instantaneously, identify anomalies in production lines, and predict equipment failures, leading to significant improvements in yield rates and reduction in waste. The integration of AI for supply chain optimization, demand forecasting, and even understanding market trends for specific coating materials is also a growing area of inquiry, suggesting a holistic view of AI's potential to drive efficiency and innovation across the entire value chain of separator coating materials.

- Accelerated material discovery and optimization of coating formulations through AI-driven simulations and data analysis.

- Enhanced quality control and defect detection in manufacturing processes using machine vision and machine learning algorithms.

- Predictive maintenance for coating machinery, reducing downtime and optimizing production efficiency.

- Personalized coating development based on specific battery performance requirements and application scenarios.

- Optimized supply chain management and inventory forecasting for raw coating materials.

- Improved R&D efficiency by predicting material behavior and performance, minimizing physical prototyping.

- Automated process control in coating lines, ensuring precise thickness and uniformity for enhanced battery safety and performance.

Key Takeaways Separator Coating Material Market Size & Forecast

User queries regarding the Separator Coating Material market size and forecast consistently highlight the pivotal role of lithium-ion battery advancements and the accelerating pace of electric vehicle (EV) adoption. A significant takeaway is the market's robust growth trajectory, primarily fueled by the global shift towards electrification in transportation and increasing investments in renewable energy storage solutions. The underlying demand for enhanced battery safety, extended cycle life, and higher energy density is directly driving innovation and market expansion for these specialized coating materials, positioning them as indispensable components in the modern energy landscape.

Another critical insight gathered from user questions pertains to the strategic importance of material innovation and regional manufacturing capabilities. The market is not just expanding in size but also evolving in terms of material composition, with a clear trend towards ceramic-based and advanced polymer coatings that offer superior thermal stability and mechanical integrity. Furthermore, the forecast indicates a concentrated growth in regions with robust battery manufacturing ecosystems, particularly Asia-Pacific, underscoring the interconnectedness of the battery supply chain and the critical role of localized production for future market dynamics. The emphasis on high-performance and sustainable solutions will continue to shape market evolution.

- The Separator Coating Material market is poised for substantial growth, driven largely by the exponential expansion of the electric vehicle (EV) and energy storage sectors.

- Innovations in coating materials are crucial for improving battery safety, extending cycle life, and increasing energy density, which are key consumer demands.

- Asia-Pacific maintains its dominance as a manufacturing hub, influencing global supply and demand dynamics.

- The market is seeing a significant shift towards advanced ceramic and polymer coatings due to their superior thermal stability and mechanical properties.

- Sustainability and environmental considerations are increasingly influencing material selection and production processes within the industry.

- Strategic partnerships and collaborations across the battery value chain are becoming essential for securing material supply and accelerating technological advancements.

- Continuous research and development into next-generation battery chemistries, such as solid-state batteries, will open new avenues for specialized coating applications.

Separator Coating Material Market Drivers Analysis

The Separator Coating Material market is fundamentally propelled by the surging global demand for lithium-ion batteries across diverse applications. The unprecedented growth in the electric vehicle (EV) industry, alongside the rapid deployment of grid-scale energy storage systems, acts as a primary catalyst. These applications necessitate batteries with higher energy density, improved safety features, and extended lifespan, all of which are significantly influenced by the performance of separator coating materials. As regulatory pressures intensify for cleaner energy solutions and reduced carbon emissions, the push for efficient and safe battery technology directly translates into increased demand for advanced coating solutions.

Furthermore, the continuous advancements in battery technology, including the development of high-nickel cathodes and silicon-anode batteries, inherently demand more robust and sophisticated separator coatings to mitigate issues like dendrite formation and thermal runaway. Consumer electronics, while a more mature segment, still contributes to sustained demand, especially for devices requiring thinner, lighter, and more powerful batteries. Innovations in material science, leading to the development of new ceramic and polymer composites, also serve as a crucial driver, offering enhanced thermal stability, mechanical strength, and electrochemical performance, thereby broadening the scope of application for these specialized materials.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Growth of Electric Vehicle (EV) Industry | +5.0% | Global, especially China, Europe, North America | 2025-2033 (Long-term) |

| Increasing Demand for Grid-Scale Energy Storage Systems (ESS) | +3.5% | North America, Europe, Asia Pacific | 2025-2033 (Mid to Long-term) |

| Advancements in Battery Technology and Energy Density Needs | +3.0% | Global, driven by R&D hubs (e.g., Japan, South Korea, US) | 2025-2033 (Continuous) |

| Enhanced Battery Safety Regulations and Performance Standards | +2.5% | Europe, North America, China | 2025-2030 (Mid-term) |

| Consistent Demand from Consumer Electronics Sector | +1.5% | Asia Pacific, Global | 2025-2033 (Stable) |

Separator Coating Material Market Restraints Analysis

Despite the robust growth drivers, the Separator Coating Material market faces several notable restraints that could temper its expansion. One significant challenge is the high production cost associated with advanced coating materials and the complex manufacturing processes required to achieve precise and uniform coatings. The specialized nature of these materials, often involving rare or difficult-to-process chemicals, contributes to elevated raw material expenses. Furthermore, the energy-intensive nature of some coating techniques adds to the overall operational costs, which can impact pricing competitiveness and limit widespread adoption, especially in cost-sensitive applications.

Another substantial restraint is the volatility in raw material prices and the potential for supply chain disruptions. Many of the critical components for ceramic or polymer coatings are subject to global commodity price fluctuations or rely on a limited number of suppliers, making the market vulnerable to external economic or geopolitical events. The increasing complexity of regulatory frameworks pertaining to material safety and environmental impact also presents a barrier, requiring significant investments in compliance and potentially slowing down the introduction of new products. Additionally, the development of alternative battery technologies that might require different or no separator coatings, though nascent, poses a long-term threat to the conventional separator coating market.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Production Costs and Capital Intensive Manufacturing | -2.0% | Global | 2025-2030 (Mid-term) |

| Volatility in Raw Material Prices and Supply Chain Vulnerabilities | -1.5% | Global, particularly regions dependent on specific imports | 2025-2033 (Continuous) |

| Stringent Environmental Regulations and Compliance Costs | -1.0% | Europe, North America, parts of Asia | 2025-2033 (Long-term) |

| Emergence of Alternative Battery Technologies (e.g., solid-state, next-gen without liquid electrolytes) | -0.8% | Global, primarily R&D intensive regions | 2030-2033 (Long-term, nascent) |

| Intellectual Property and Patent Landscape Complexity | -0.5% | Global, highly competitive regions (e.g., US, Japan, South Korea) | 2025-2033 (Continuous) |

Separator Coating Material Market Opportunities Analysis

The Separator Coating Material market is ripe with opportunities stemming from the continuous evolution of battery technology and the expansion into new application areas. A significant opportunity lies in the ongoing research and development of solid-state batteries, which, while promising, still require sophisticated interlayers or coatings to address interfacial stability and dendrite formation issues. Developing specialized coating materials that can seamlessly integrate with solid electrolytes and improve their performance could unlock a substantial new market segment. Furthermore, as battery energy density targets continue to climb, there is an increasing need for ultra-thin, highly porous, and mechanically robust coatings that allow for maximum active material packing while ensuring safety.

Another promising avenue is the customization of coating materials for niche and high-performance applications beyond conventional EVs and consumer electronics, such as aerospace, medical implants, and defense, where specific operational requirements demand tailored battery solutions. The global push for sustainability also presents a compelling opportunity for innovations in green coating technologies, including water-based formulations, solvent-free processes, and the development of bio-degradable or recyclable coating materials. Companies investing in these environmentally conscious solutions can gain a competitive edge and align with evolving consumer and regulatory preferences. Emerging markets in Southeast Asia, Latin America, and Africa also offer untapped potential for battery manufacturing expansion, creating new demand centers for separator coating materials as electrification trends gain momentum globally.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Solid-State Battery Compatible Coatings | +4.0% | Global, R&D focused regions (Asia, Europe, N. America) | 2028-2033 (Long-term) |

| Customization for Niche and High-Performance Applications | +2.5% | North America, Europe, Japan | 2025-2033 (Mid to Long-term) |

| Expansion into Emerging Markets for EVs and ESS | +2.0% | Southeast Asia, Latin America, parts of Africa | 2027-2033 (Mid to Long-term) |

| Investment in Sustainable and Green Coating Technologies | +1.5% | Europe, North America, Japan | 2025-2033 (Continuous) |

| Integration with Advanced Battery Chemistries (e.g., Silicon Anodes) | +1.0% | Global R&D centers | 2025-2030 (Mid-term) |

Separator Coating Material Market Challenges Impact Analysis

The Separator Coating Material market confronts several significant challenges that could impede its growth and innovation. One critical challenge is the intense competitive landscape, characterized by a mix of established chemical giants and specialized material manufacturers. This competition drives down profit margins and necessitates continuous investment in research and development to maintain a competitive edge, often leading to rapid product obsolescence as new, more efficient materials emerge. Furthermore, the market demands high levels of technical expertise and specialized equipment, posing entry barriers for new players and consolidating power among existing ones.

Another substantial challenge is the complexity of achieving uniform coating thickness and porosity at a high production scale, which is paramount for battery performance and safety. Any inconsistencies can lead to reduced battery life, lower energy density, and increased risk of thermal events. The rapid pace of technological advancements in battery design means that coating material manufacturers must constantly innovate to keep pace with evolving requirements, which demands significant R&D expenditure and agility in product development cycles. Additionally, managing the intricate global supply chain for precursor materials and navigating geopolitical tensions or trade disputes can lead to supply disruptions and increased costs, creating instability in the market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition and Pricing Pressure | -1.8% | Global, particularly Asia Pacific | 2025-2033 (Continuous) |

| Achieving Consistent Coating Uniformity at Scale | -1.2% | Global, manufacturing hubs | 2025-2030 (Mid-term) |

| Rapid Technological Obsolescence and R&D Investment Needs | -1.0% | Global, R&D focused regions | 2025-2033 (Continuous) |

| Supply Chain Instability and Geopolitical Risks | -0.7% | Global, especially for raw material sourcing | 2025-2030 (Mid-term) |

| Waste Management and Recycling Challenges for Coated Separators | -0.5% | Europe, North America (due to regulations) | 2028-2033 (Long-term) |

Separator Coating Material Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Separator Coating Material market, covering historical trends, current market dynamics, and future growth projections. The scope encompasses detailed segmentation by material type, application, battery type, and end-use industry, offering a granular view of market performance across various dimensions. It also includes an exhaustive regional analysis, identifying key growth markets and factors influencing regional demand and supply landscapes. The report aims to furnish stakeholders with actionable insights into market size, growth drivers, restraints, opportunities, and competitive landscape, enabling informed strategic decision-making.

Furthermore, the report highlights the impact of emerging technologies, such as Artificial Intelligence, on material development and manufacturing efficiency within the separator coating sector. It identifies key market trends, addresses common user inquiries through a dedicated FAQ section, and profiles leading market players to provide a holistic understanding of the competitive environment. The data presented is meticulously collected and validated from primary and secondary research sources, ensuring accuracy and reliability for market sizing, forecasting, and strategic analysis.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 550 Million |

| Market Forecast in 2033 | USD 2,800 Million |

| Growth Rate | 21.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Sumitomo Chemical, Arkema, Toray Industries, Asahi Kasei, SK Innovation, Ube Industries, Celgard (PolyPore), W-Scope Corporation, LG Chem, BASF, Umicore, Showa Denko (Resonac), Hitachi Chemical (Showa Denko Materials), Entegris, Mitsubishi Chemical, Nippon Kasei Chemical, Teijin, Freudenberg, Mitsui Chemicals, AGC Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Separator Coating Material market is extensively segmented to provide a detailed understanding of its diverse components and drivers. This segmentation allows for a granular analysis of market dynamics, identifying specific growth areas and technological shifts across different material types, applications, battery chemistries, and end-use industries. The intricate interplay between these segments is critical for manufacturers, suppliers, and investors to pinpoint lucrative opportunities and develop targeted strategies that align with market demands and technological advancements.

Understanding these segmentations is paramount for strategic planning, as each category responds to unique market forces and technological imperatives. For instance, the demand for ceramic coatings is largely driven by safety concerns in high-power applications like electric vehicles, whereas polymer coatings might be favored for their flexibility and cost-effectiveness in consumer electronics. Similarly, the rapid evolution of lithium-ion battery technology necessitates continuous innovation within coating materials to keep pace with increasing energy density and safety requirements, influencing material choices and research directions across all segments.

- By Material Type:

- Alumina (Al2O3): Widely used for its excellent thermal stability and chemical inertness, preventing short circuits and improving safety.

- Silica (SiO2): Offers good thermal resistance and mechanical strength, often used in ceramic composites.

- Polyimide (PI): Known for its high heat resistance, mechanical strength, and chemical stability, crucial for high-performance batteries.

- Polyvinylidene Fluoride (PVDF): A versatile polymer often used as a binder in electrode coatings and for its electrochemical stability.

- Aramid: Provides exceptional thermal resistance and mechanical integrity, enhancing separator robustness.

- Other Polymers (e.g., Polyethylene Terephthalate (PET), Polypropylene (PP), Polytetrafluoroethylene (PTFE)): Employed for specific properties like flexibility, chemical resistance, or cost-effectiveness.

- Other Ceramics (e.g., Zirconia (ZrO2), Titania (TiO2)): Explored for enhanced thermal and electrochemical stability in advanced battery designs.

- Nanomaterials (e.g., Carbon Nanotubes, Graphene): Used to improve conductivity, mechanical strength, and porosity of coatings.

- By Application:

- Electric Vehicles (EVs) & Hybrid Electric Vehicles (HEVs): The largest and fastest-growing segment, demanding high safety, power, and cycle life.

- Consumer Electronics (Smartphones, Laptops, Wearables): Requires compact, lightweight, and high-energy density batteries, with a focus on safety.

- Energy Storage Systems (ESS) (Grid-scale, Residential): Demands long-duration, highly stable, and safe batteries for renewable energy integration.

- Industrial Equipment: Includes applications like forklifts, robotics, and power tools, requiring robust and durable battery solutions.

- Medical Devices: Requires highly reliable and safe batteries for critical applications such as pacemakers and portable medical equipment.

- Aerospace & Defense: Demands extreme performance, reliability, and safety under challenging environmental conditions.

- By Battery Type:

- Lithium-ion Batteries (LiB): The predominant segment, driving significant demand for all types of separator coating materials due to their widespread use.

- Solid-State Batteries: An emerging segment with unique coating material requirements for solid electrolyte compatibility and interfacial stability.

- Lithium Polymer Batteries: Utilizes gel or solid polymer electrolytes, influencing coating choices for flexibility and performance.

- Nickel-Metal Hydride (Ni-MH) Batteries: A mature market, but still requires specific coatings for performance and longevity in certain applications.

- By End-Use Industry:

- Automotive: Encompasses the entire range of passenger and commercial EVs, driving the largest volume of demand.

- Consumer Electronics: Includes personal electronic devices, portable power banks, and related accessories.

- Energy (Renewables, Utilities): Focuses on large-scale energy storage for grid stabilization, renewable energy integration, and backup power.

- Industrial: Covers battery applications in manufacturing, logistics, construction, and other industrial sectors.

- Healthcare: Includes batteries for medical devices, diagnostic equipment, and mobile healthcare solutions.

Regional Highlights

The global Separator Coating Material market exhibits distinct regional dynamics, with Asia Pacific standing as the dominant force due to its extensive battery manufacturing ecosystem. Countries like China, South Korea, and Japan are at the forefront of lithium-ion battery production and innovation, driven by massive investments in electric vehicle manufacturing and consumer electronics. This region benefits from established supply chains, robust research and development capabilities, and supportive government policies promoting electrification and advanced material science. The sheer volume of battery production in this region directly translates into unparalleled demand for separator coating materials, solidifying its market leadership.

North America and Europe represent significant growth regions, primarily fueled by increasing electric vehicle adoption, ambitious renewable energy targets, and a concerted effort to localize battery production and supply chains. Governments in these regions are offering substantial incentives for EV purchases and charging infrastructure development, alongside investments in giga-factories for battery cell manufacturing. This strategic push is creating a burgeoning demand for advanced battery components, including separator coating materials. While these regions are currently net importers of many battery components, their rapid expansion in EV and ESS manufacturing capabilities indicates a strong future trajectory for domestic demand and production of separator coating materials.

- Asia Pacific (APAC) dominates the global market, primarily driven by China, South Korea, and Japan, which are major hubs for battery manufacturing and EV production.

- North America is experiencing substantial growth due to increasing EV sales, rising investments in energy storage, and government initiatives promoting domestic battery manufacturing.

- Europe demonstrates strong market expansion, propelled by ambitious climate targets, significant EV adoption, and strategic investments in giga-factories across countries like Germany, France, and Sweden.

- China is a key player, leading in both battery production capacity and EV market penetration, driving massive demand for separator coating materials.

- South Korea and Japan continue to be critical innovation centers, contributing advanced material technologies and high-quality separator products.

- Latin America, Middle East, and Africa (MEA) are emerging markets with nascent but growing EV and renewable energy sectors, indicating future opportunities for market penetration.

- Government policies and subsidies for electric vehicles and renewable energy storage significantly influence regional market growth across all geographies.

- Localized supply chain development in North America and Europe is a strategic focus to reduce reliance on Asian imports, fostering regional market growth for coating materials.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Separator Coating Material Market.- Sumitomo Chemical

- Arkema

- Toray Industries

- Asahi Kasei

- SK Innovation

- Ube Industries

- Celgard (PolyPore)

- W-Scope Corporation

- LG Chem

- BASF

- Umicore

- Showa Denko (Resonac)

- Hitachi Chemical (Showa Denko Materials)

- Entegris

- Mitsubishi Chemical

- Nippon Kasei Chemical

- Teijin

- Freudenberg

- Mitsui Chemicals

- AGC Inc.

Frequently Asked Questions

Analyze common user questions about the Separator Coating Material market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is separator coating material used for in batteries?

Separator coating materials are applied to battery separators to enhance their thermal stability, mechanical strength, and electrochemical performance. They prevent direct contact between electrodes, mitigate internal short circuits, and improve overall battery safety, particularly under high temperatures or overcharge conditions. These coatings are crucial for extending battery lifespan and enabling higher energy densities.

What are the primary types of separator coating materials?

The primary types of separator coating materials include ceramic-based coatings like alumina (Al2O3) and silica (SiO2), known for their excellent thermal stability and chemical inertness. Polymer-based coatings such as polyimide (PI) and polyvinylidene fluoride (PVDF) are also widely used for their flexibility, mechanical strength, and adhesive properties. Hybrid coatings combining ceramic and polymer materials are also gaining prominence for optimized performance.

How does coating material enhance battery safety?

Coating materials significantly enhance battery safety by improving the thermal runaway resistance of separators. Ceramic coatings, for instance, prevent separator shrinkage at high temperatures, which can lead to internal short circuits and thermal events. They also act as a physical barrier against dendrite penetration and improve the overall structural integrity of the battery, reducing the risk of catastrophic failures.

What role do Electric Vehicles (EVs) play in the Separator Coating Material market growth?

Electric Vehicles (EVs) are the leading growth driver for the Separator Coating Material market. The rapidly increasing global production and adoption of EVs necessitate high-performance, safe, and durable lithium-ion batteries. Separator coatings are indispensable for meeting the stringent safety and longevity requirements of EV batteries, directly correlating EV market expansion with the demand for advanced coating materials.

What are the future trends in separator coating technology?

Future trends in separator coating technology include the development of ultra-thin and uniform coatings to maximize energy density, tailored coatings for emerging battery chemistries like solid-state batteries, and increased focus on sustainable and environmentally friendly coating materials and processes. Integration of AI for accelerated material discovery and process optimization is also a significant trend, aiming for higher efficiency and customized solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted