Semiconductor Package Substrates in Mobile Devices Market

Semiconductor Package Substrates in Mobile Devices Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_678213 | Last Updated : July 18, 2025 |

Format : ![]()

![]()

![]()

![]()

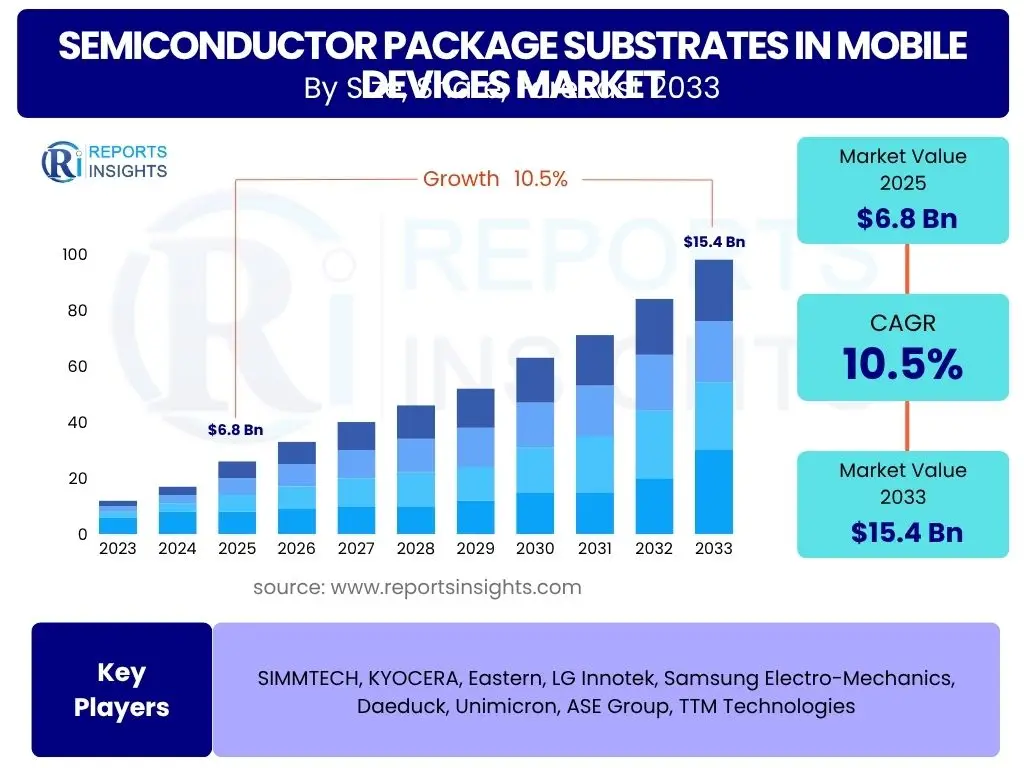

Semiconductor Package Substrates in Mobile Devices Market is projected to grow at a Compound annual growth rate (CAGR) of 10.5% between 2025 and 2033, valued at USD 6.8 Billion in 2025 and is projected to grow by USD 15.4 Billion by 2033 the end of the forecast period.

Key Semiconductor Package Substrates in Mobile Devices Market Trends & Insights

The market for semiconductor package substrates in mobile devices is undergoing a significant transformation, driven by relentless innovation in smartphone technology, the pervasive rollout of 5G networks, and the increasing integration of artificial intelligence capabilities at the edge. These trends collectively demand more sophisticated, compact, and high-performance packaging solutions, directly impacting the design and material science of substrates. Miniaturization remains a core objective, pushing the boundaries for smaller form factors without compromising on power, speed, or heat dissipation. Advanced packaging techniques, such as System-in-Package (SiP) and Fan-Out Wafer Level Packaging (FOWLP), are becoming standard to meet the intricate requirements of multi-component integration within limited spaces.

Furthermore, the evolution towards higher data transfer rates and lower latency, epitomized by 5G, necessitates substrates capable of managing increased signal integrity and power delivery efficiently. This also extends to thermal management, where advanced materials and designs are crucial to dissipate heat from increasingly powerful mobile processors. The industry is also observing a shift towards more sustainable manufacturing practices and materials, aligning with global environmental concerns. This holistic evolution across performance, size, and sustainability is shaping the future landscape of semiconductor package substrates for mobile applications.

- Miniaturization and higher integration for compact mobile devices.

- Increasing adoption of 5G technology demanding superior signal integrity.

- Growth in AI and machine learning processing requiring advanced chip packaging.

- Development of advanced packaging technologies like SiP and FC-CSP.

- Emphasis on enhanced thermal management solutions for high-performance processors.

- Demand for power-efficient substrates to extend mobile device battery life.

- Supply chain diversification and regional manufacturing shifts.

AI Impact Analysis on Semiconductor Package Substrates in Mobile Devices

Artificial intelligence is profoundly reshaping the requirements for semiconductor package substrates in mobile devices by demanding significantly higher computational power, improved data throughput, and optimized energy efficiency for on-device AI processing. As AI functionalities, such as advanced image processing, natural language understanding, and predictive analytics, become integral to smartphones and other mobile gadgets, the underlying silicon chips must handle immense data volumes with minimal latency. This necessitates an evolution in packaging technologies to support denser integration of logic, memory, and specialized AI accelerators, leading to a greater reliance on advanced substrate types like FC-CSP and SiP which offer superior interconnect density and thermal performance.

The imperative for AI-driven mobile devices to perform complex computations locally, reducing reliance on cloud processing, places unprecedented demands on the package substrate. It must facilitate faster communication between components, manage increased power delivery, and dissipate heat effectively from powerful AI processors operating continuously. Consequently, manufacturers are investing in research and development to innovate substrate materials, design architectures, and manufacturing processes that can support these rigorous AI workloads, ensuring mobile devices can deliver seamless and responsive AI experiences while maintaining compact form factors and extended battery life.

- Increased demand for high-performance package substrates to support on-device AI processing.

- Acceleration of advanced packaging solutions for integrating AI accelerators and memory.

- Enhanced requirements for thermal management in substrates due to higher power densities from AI chips.

- Focus on optimizing power delivery networks within substrates for AI-specific workloads.

- Stimulation of research into novel substrate materials with superior electrical and thermal properties.

- Driving miniaturization further to accommodate powerful AI components in sleek mobile designs.

Key Takeaways Semiconductor Package Substrates in Mobile Devices Market Size & Forecast

- The global Semiconductor Package Substrates in Mobile Devices Market is projected to reach USD 15.4 Billion by 2033.

- The market is anticipated to exhibit a robust Compound Annual Growth Rate (CAGR) of 10.5% from 2025 to 2033.

- In 2025, the market size is estimated at USD 6.8 Billion, highlighting a strong base for future expansion.

- Growth is primarily driven by advancements in mobile technology, including 5G adoption and AI integration.

- Miniaturization and higher performance demands in smartphones, tablets, and notebooks are key growth catalysts.

Semiconductor Package Substrates in Mobile Devices Market Drivers Impact Analysis

The market for semiconductor package substrates in mobile devices is propelled by several potent drivers, reflecting the dynamic evolution of consumer electronics and communication technologies. These drivers collectively amplify the demand for more sophisticated and high-performance substrate solutions, essential for the compact yet powerful mobile devices of today and tomorrow. The global rollout of 5G connectivity is a primary catalyst, as it mandates higher frequency support, improved signal integrity, and increased power handling capabilities within mobile chipsets, directly translating to a need for advanced substrates. Similarly, the continuous drive for miniaturization in mobile device design pushes manufacturers to adopt more complex and denser packaging technologies, which rely heavily on advanced substrate designs.

Moreover, the increasing integration of artificial intelligence and machine learning functionalities directly on mobile devices necessitates powerful processors that generate more heat and require efficient power delivery, making high-performance substrates critical. The consistent growth in smartphone penetration, particularly in emerging markets, coupled with the rising demand for premium and foldable smartphones, further fuels the market expansion. These drivers create a compelling environment for innovation in materials science, manufacturing processes, and design architectures for semiconductor package substrates, ensuring they can meet the rigorous demands of next-generation mobile applications.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Global 5G Rollout and Adoption | +1.8% | Asia Pacific (China, South Korea), North America, Europe | Short to Medium Term (2025-2029) |

| Increasing Integration of AI and Edge Computing in Mobile Devices | +1.5% | Global, particularly North America, Europe, East Asia | Medium to Long Term (2026-2033) |

| Continuous Miniaturization and Performance Enhancement in Smartphones | +1.2% | Global, led by developed markets and premium segments | Ongoing (2025-2033) |

| Growing Demand for Advanced Packaging Technologies (SiP, FC-CSP) | +1.0% | Primarily East Asia (Taiwan, South Korea, Japan), North America | Medium Term (2025-2030) |

| Expansion of Smartphone Market in Emerging Economies | +0.8% | Southeast Asia, India, Africa, Latin America | Long Term (2027-2033) |

Semiconductor Package Substrates in Mobile Devices Market Restraints Impact Analysis

Despite the robust growth trajectory, the semiconductor package substrates in mobile devices market faces certain restraints that could temper its expansion. One significant challenge is the inherent complexity and high cost associated with manufacturing advanced package substrates, particularly those utilizing innovative materials or intricate designs. The capital expenditure required for state-of-the-art fabrication facilities and the rigorous quality control processes add substantial overheads, which can influence pricing and market accessibility for smaller players or in cost-sensitive segments. Moreover, the increasing geopolitical tensions and trade disputes have introduced an element of uncertainty into the global supply chain, affecting the stable procurement of raw materials and the distribution of finished products.

Another critical restraint is the potential for market saturation in mature smartphone markets, which could lead to slower upgrade cycles and thus, a reduced demand for new devices and their components. While emerging markets offer growth opportunities, they often present their own set of challenges, including lower purchasing power and a preference for more budget-friendly devices, which might limit the adoption of high-end substrate technologies. Furthermore, the rapid pace of technological change means that existing manufacturing infrastructure and product designs can quickly become obsolete, requiring continuous, costly investments in research and development to remain competitive. These factors combined necessitate careful strategic planning by market participants to mitigate risks and sustain growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs and Complex Production Processes | -0.9% | Global, impacting smaller players and new entrants | Ongoing (2025-2033) |

| Supply Chain Vulnerabilities and Geopolitical Risks | -0.7% | Global, particularly regions reliant on specific material sources | Short to Medium Term (2025-2028) |

| Potential Market Saturation in Developed Smartphone Markets | -0.5% | North America, Europe, East Asia | Medium to Long Term (2027-2033) |

| Rapid Technological Obsolescence Requiring Continuous R&D | -0.4% | Global, affecting all market participants | Ongoing (2025-2033) |

Semiconductor Package Substrates in Mobile Devices Market Opportunities Impact Analysis

The semiconductor package substrates market for mobile devices is rich with opportunities, driven by innovation, evolving consumer preferences, and the expansion into new product categories. The emergence of novel mobile device form factors, such as foldable smartphones, rollable displays, and advanced augmented/virtual reality (AR/VR) headsets, creates new avenues for substrate manufacturers. These cutting-edge devices often require highly flexible, ultra-thin, and robust substrates capable of accommodating complex designs and dynamic movements, presenting a unique niche for specialized substrate development. Furthermore, advancements in material science are continuously opening doors for improved performance, including enhanced thermal conductivity, better electrical properties, and reduced power consumption, which are critical for future mobile applications.

The ongoing global emphasis on sustainability and circular economy principles also provides an opportunity for developing eco-friendly manufacturing processes and recyclable or biodegradable substrate materials. Companies investing in such initiatives can gain a competitive edge and appeal to environmentally conscious consumers and regulations. Additionally, the broader integration of mobile technology with the Internet of Things (IoT) and automotive sectors suggests potential for cross-market applications of advanced substrates, expanding the overall addressable market. Strategic partnerships between substrate manufacturers, chip designers, and mobile device OEMs can accelerate product development and market penetration, capitalizing on these emerging opportunities to sustain market growth and innovation.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of New Mobile Device Form Factors (Foldables, XR Devices) | +1.5% | Global, with early adoption in North America, Europe, East Asia | Medium to Long Term (2026-2033) |

| Advancements in Material Science for Substrates (e.g., lower Dk/Df, higher thermal conductivity) | +1.3% | Global, driven by R&D hubs in North America, Europe, East Asia | Ongoing (2025-2033) |

| Growing Adoption of High-End and Premium Mobile Devices | +1.0% | Developed markets, rising disposable income in emerging economies | Short to Medium Term (2025-2029) |

| Demand for Sustainable and Eco-Friendly Manufacturing Practices | +0.7% | Europe, North America, increasingly Asia Pacific | Long Term (2028-2033) |

Semiconductor Package Substrates in Mobile Devices Market Challenges Impact Analysis

The semiconductor package substrates market for mobile devices contends with several significant challenges that can impede its growth and introduce complexities for manufacturers. One pervasive challenge is the intense price competition within the mobile device ecosystem, which cascades down to component suppliers, including substrate manufacturers. This pressure often forces companies to optimize costs while maintaining high quality and performance, leading to thinner profit margins and constant innovation demands. Additionally, the stringent quality and reliability requirements for mobile device components, given their pervasive use and exposure to varied environmental conditions, necessitate rigorous testing and high production standards, adding to manufacturing complexities and costs.

Another substantial challenge is the rapid evolution of technology and product lifecycles in the mobile sector. New mobile device models are released frequently, each demanding updated, often more advanced, package substrate specifications. This rapid iteration requires manufacturers to continuously invest in research and development, adapt their production lines, and manage inventory effectively to avoid obsolescence, placing considerable strain on resources. Furthermore, intellectual property (IP) disputes and complex patent landscapes surrounding advanced packaging technologies can create legal hurdles and limit market access for some players. Overcoming these challenges requires strategic investments in R&D, efficient supply chain management, and a keen understanding of global market dynamics and regulatory environments.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Price Competition and Margin Pressure | -0.8% | Global, particularly in high-volume, competitive markets | Ongoing (2025-2033) |

| Stringent Quality, Reliability, and Miniaturization Demands | -0.6% | Global, impacting R&D and manufacturing processes | Ongoing (2025-2033) |

| Short Product Lifecycles and Rapid Technological Changes | -0.5% | Global, especially in leading technology markets | Ongoing (2025-2033) |

| Complex Intellectual Property Landscape and Patent Litigation | -0.3% | North America, East Asia, Europe | Medium to Long Term (2026-2033) |

Semiconductor Package Substrates in Mobile Devices Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Semiconductor Package Substrates in Mobile Devices Market, offering crucial insights into market dynamics, trends, and future projections. The report scope encompasses a detailed examination of market size, growth drivers, restraints, opportunities, and challenges, providing a holistic view for stakeholders. It also includes extensive segmentation analysis by product type, application, end-use industry, and geography, enabling targeted strategic planning. Furthermore, the report profiles key industry players, offering competitive intelligence and a deeper understanding of the market landscape. This updated scope ensures decision-makers receive the most current and relevant information to navigate the evolving mobile device ecosystem.

| Report Attributes | Report Details |

|---|---|

| Report Name | Semiconductor Package Substrates in Mobile Devices Market |

| Market Size in 2025 | USD 6.8 Billion |

| Market Forecast in 2033 | USD 15.4 Billion |

| Growth Rate | CAGR of 2025 to 2033 10.5% |

| Number of Pages | 210 |

| Key Companies Covered | SIMMTECH, KYOCERA, Eastern, LG Innotek, Samsung Electro-Mechanics, Daeduck, Unimicron, ASE Group, TTM Technologies |

| Segments Covered | By Type, By Application, By End-Use Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Customization Scope | Avail customised purchase options to meet your exact research needs. Request For Customization |

Segmentation Analysis

Market Product Type Segmentation:-- MCP/UTCSP (Multi-Chip Package / Ultra Thin Chip Scale Package)

- FC-CSP (Flip Chip Chip Scale Package)

- SiP (System-in-Package)

- PBGA/CSP (Plastic Ball Grid Array / Chip Scale Package)

- BOC (Board On Chip)

- FMC (Flexible Microporous Ceramic)

- Smartphones

- Tablets

- Notebook PCs

- Others

Regional Highlights

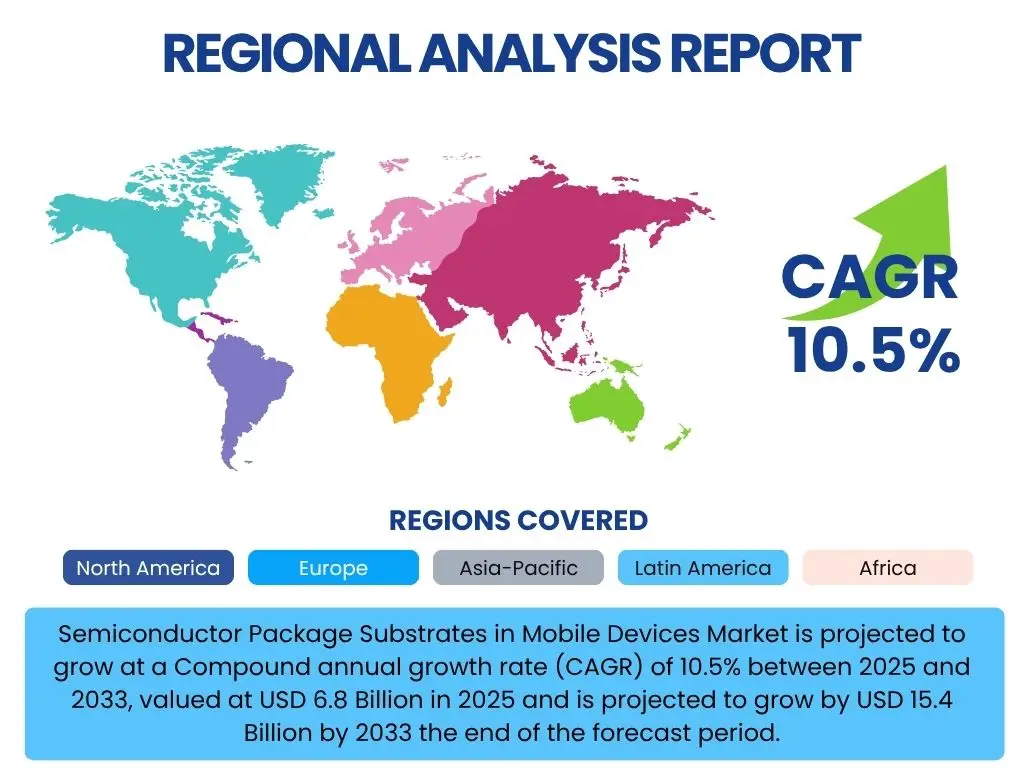

The regional analysis highlights the diverse dynamics influencing the Semiconductor Package Substrates in Mobile Devices Market across key geographical areas. Each region contributes uniquely to the market's growth, driven by factors such as technological adoption, manufacturing capabilities, consumer base, and economic development.- Asia Pacific (APAC): APAC stands as the undisputed leader in the semiconductor package substrates market for mobile devices, primarily due to the presence of major electronics manufacturing hubs in countries like China, South Korea, Taiwan, and Japan. These nations host leading foundries, packaging houses, and mobile device manufacturers, creating a robust demand for substrates. Furthermore, the region boasts the largest consumer base for smartphones and other mobile devices, particularly in rapidly growing economies like India and Southeast Asian countries. The aggressive rollout of 5G infrastructure and increasing disposable incomes in these regions further solidify APAC's dominance.

- North America: North America represents a significant market driven by early adoption of advanced mobile technologies, extensive research and development activities, and the presence of prominent technology companies. The region's focus on high-performance mobile devices, including premium smartphones and next-generation wearables, fuels demand for sophisticated and high-density package substrates. Innovation in AI and edge computing also contributes to the market's growth in this region, pushing the boundaries of substrate technology.

- Europe: Europe is characterized by a strong emphasis on innovation and high-value niche markets within the mobile device sector. While not a primary manufacturing hub for mass-produced mobile devices, countries in Europe contribute significantly through specialized R&D, advanced material science, and the development of high-end mobile technologies. The growing demand for secure and energy-efficient mobile solutions, coupled with initiatives for smart cities and connected devices, influences the demand for advanced package substrates.

- Latin America, Middle East, and Africa (MEA): These regions are emerging markets for mobile devices, characterized by increasing smartphone penetration and improving digital infrastructure. While currently smaller in market share compared to APAC, they offer substantial growth potential. The rising affordability of mobile devices and the expansion of mobile internet access are driving the demand for all mobile components, including package substrates, though often for more cost-effective solutions. Investments in 5G infrastructure are also beginning to stimulate demand for more advanced substrates in select countries.

Top Key Players:

The market research report covers the analysis of key stakeholders of the Semiconductor Package Substrates in Mobile Devices Market. Some of the leading players profiled in the report include -:- SIMMTECH

- KYOCERA

- Eastern

- LG Innotek

- Samsung Electro-Mechanics

- Daeduck

- Unimicron

- ASE Group

- TTM Technologies

Frequently Asked Questions:

What are semiconductor package substrates in mobile devices?

Semiconductor package substrates are critical components that provide the mechanical support, electrical interconnections, and thermal pathways for integrated circuits (ICs) within mobile devices. They act as the foundational layer connecting the tiny silicon chip to the larger circuit board, facilitating communication, power delivery, and heat dissipation essential for the chip's functionality. Without these substrates, the compact, high-performance nature of modern mobile devices would not be possible.

Why are semiconductor package substrates important for mobile devices?

Semiconductor package substrates are vital for mobile devices because they enable miniaturization, enhance performance, and ensure reliability. They allow multiple components to be integrated into a small space, manage the complex electrical signals at high speeds, and efficiently dissipate heat generated by powerful processors. This directly impacts device size, battery life, processing speed, and overall durability, making them indispensable for advanced smartphones, tablets, and other portable electronics.

What are the key types of semiconductor package substrates used in mobile devices?

The key types of semiconductor package substrates extensively used in mobile devices include Multi-Chip Package/Ultra Thin Chip Scale Package (MCP/UTCSP), Flip Chip Chip Scale Package (FC-CSP), System-in-Package (SiP), Plastic Ball Grid Array/Chip Scale Package (PBGA/CSP), Board On Chip (BOC), and Flexible Microporous Ceramic (FMC). Each type offers specific advantages in terms of integration density, thermal performance, electrical characteristics, and cost, catering to diverse mobile device requirements.

How is 5G technology impacting the semiconductor package substrates market for mobile devices?

5G technology is significantly impacting the semiconductor package substrates market by demanding higher frequencies, increased data throughput, and improved power efficiency. This necessitates substrates with superior signal integrity, lower dielectric loss, and enhanced thermal management capabilities. As 5G adoption grows globally, it drives the demand for more advanced and complex substrates like FC-CSP and SiP, capable of supporting the high-speed and low-latency requirements of next-generation mobile networks.

What is the market outlook for semiconductor package substrates in mobile devices?

The market outlook for semiconductor package substrates in mobile devices is highly positive, driven by continuous innovation in mobile technology, the global expansion of 5G networks, and the increasing integration of artificial intelligence. Projections indicate robust growth, with a Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2033, reaching an estimated USD 15.4 Billion by 2033. The ongoing demand for smaller, more powerful, and feature-rich mobile devices will continue to fuel this market's expansion.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted