Semiconductor Package Market

Semiconductor Package Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706507 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

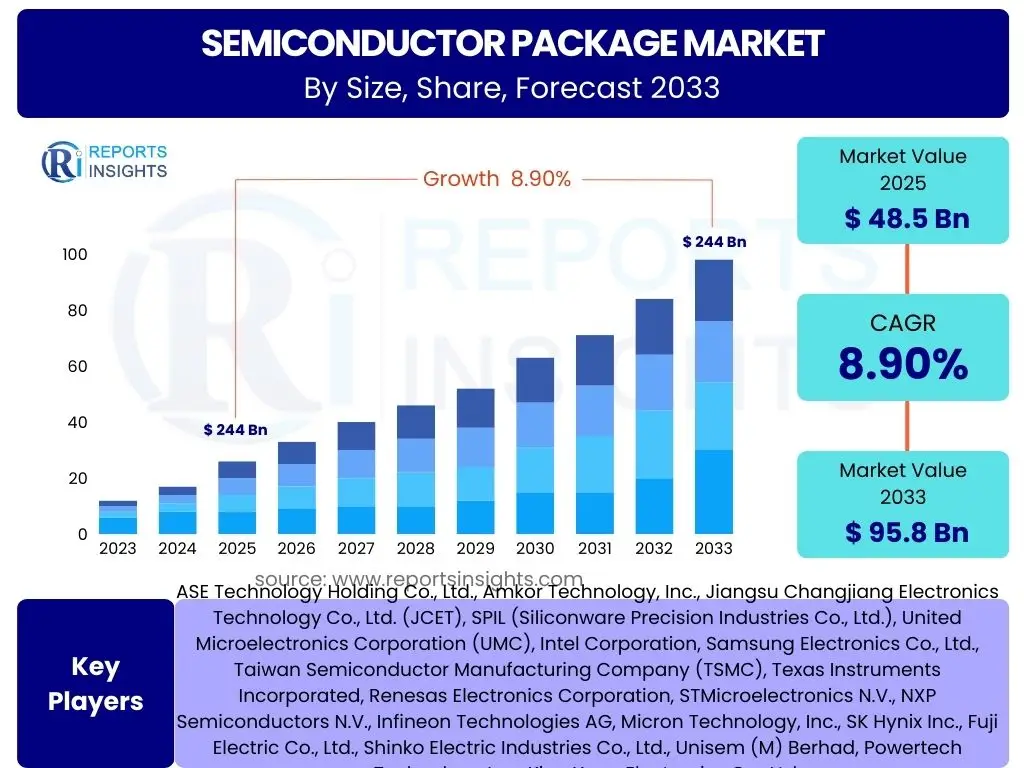

Semiconductor Package Market Size

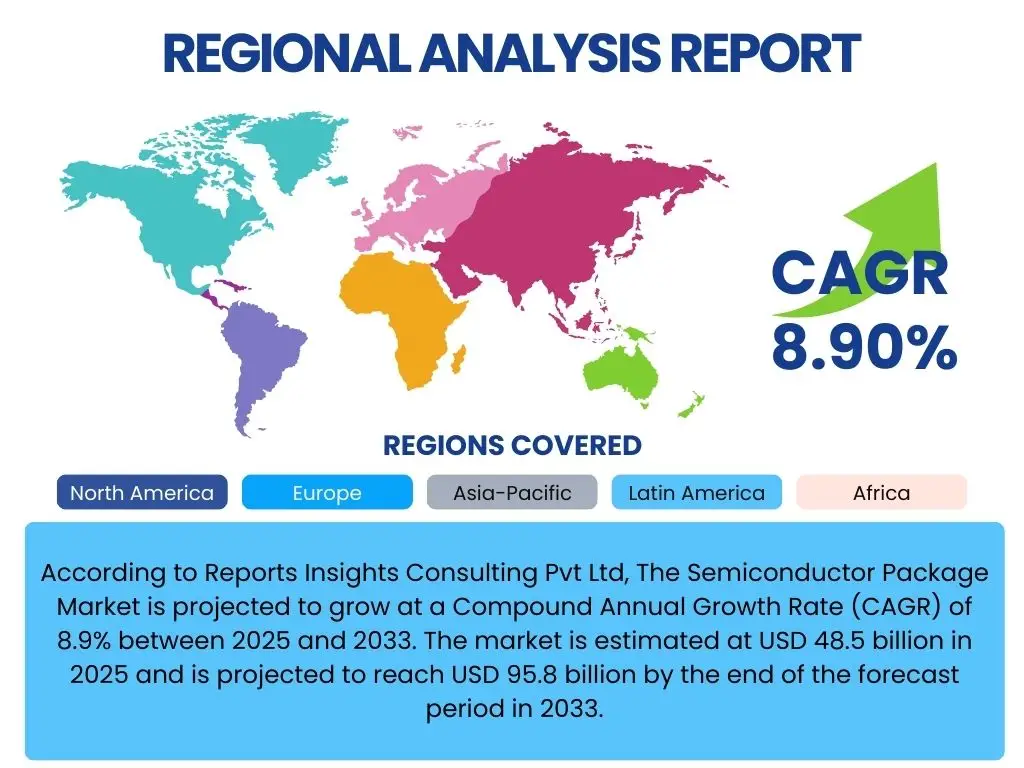

According to Reports Insights Consulting Pvt Ltd, The Semiconductor Package Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2025 and 2033. The market is estimated at USD 48.5 billion in 2025 and is projected to reach USD 95.8 billion by the end of the forecast period in 2033.

Key Semiconductor Package Market Trends & Insights

User queries regarding the semiconductor package market trends frequently revolve around the evolution of packaging technologies, the impact of miniaturization, and the increasing demand for high-performance computing. Common questions include the shift towards advanced packaging solutions, the integration of heterogeneous components, and the imperative for improved thermal management in compact designs. The market is witnessing a profound transformation driven by the need for higher bandwidth, lower power consumption, and enhanced device functionality across diverse applications.

Another prevalent area of user interest concerns the industry's response to supply chain complexities and the push for greater resilience and localization in manufacturing. There is significant curiosity about the adoption of novel materials and innovative manufacturing processes that can reduce costs, improve reliability, and accelerate time-to-market. Furthermore, the convergence of packaging with system-level integration is a key theme, reflecting the industry's move towards more holistic design approaches to meet future technological demands.

- Advanced Packaging Adoption: Increasing demand for 3D packaging, fan-out wafer-level packaging (FOWLP), and chiplets.

- Heterogeneous Integration: Growing trend to combine different chip types (e.g., logic, memory, sensors) in a single package.

- Miniaturization and High-Density Packaging: Continued push for smaller form factors and higher transistor density.

- Thermal Management Innovations: Development of advanced cooling solutions for high-performance applications.

- Material Advancements: Research into novel substrates, interposers, and encapsulation materials.

- Supply Chain Localization: Efforts to diversify manufacturing locations and enhance regional supply chain resilience.

- Automotive Electronics Growth: Rising demand for robust packaging solutions in electric vehicles and autonomous driving.

- Edge Computing Expansion: Need for optimized packaging for low-latency, energy-efficient edge devices.

AI Impact Analysis on Semiconductor Package

User questions about AI's impact on semiconductor packaging primarily focus on how artificial intelligence is enhancing design, manufacturing, and quality control processes. There is significant interest in AI-driven automation for package design optimization, enabling faster iteration cycles and more efficient layout configurations. Users are keen to understand how AI algorithms can predict optimal material usage, identify potential thermal hotspots, and simulate performance under various operational conditions, thereby reducing prototyping costs and accelerating development timelines.

Furthermore, concerns and expectations often center on AI's role in improving manufacturing yield and predictive maintenance. In fabrication, AI is being leveraged for real-time defect detection, anomaly identification, and process optimization, leading to higher quality products and reduced waste. The application of machine learning in supply chain management for demand forecasting and inventory optimization also garners considerable attention, highlighting AI's transformative potential across the entire value chain, from design to post-production support.

- Design Optimization: AI algorithms enhance package layout, material selection, and thermal simulations.

- Automated Inspection: AI-powered vision systems for high-speed, accurate defect detection during manufacturing.

- Predictive Maintenance: Machine learning models forecast equipment failures, minimizing downtime.

- Yield Improvement: AI optimizes manufacturing parameters, leading to higher output and reduced waste.

- Supply Chain Efficiency: AI improves demand forecasting and inventory management for packaging materials.

- Accelerated R&D: AI enables faster exploration of new packaging architectures and material combinations.

- Complex System Integration: AI assists in managing the complexity of heterogeneous integration and 3D stacking.

Key Takeaways Semiconductor Package Market Size & Forecast

Analysis of common user questions regarding the semiconductor package market size and forecast reveals a strong interest in understanding the underlying growth drivers and the factors that might influence market expansion. Users frequently inquire about the specific technologies expected to fuel future growth, such as advanced packaging solutions, and how these innovations contribute to overall market valuation. There is also a keen focus on the regional dynamics and which geographical areas are projected to experience the most significant growth, reflecting concerns about market concentration and diversification.

Moreover, users often seek clarity on the long-term sustainability of the market's growth trajectory, considering potential economic downturns, technological shifts, and geopolitical influences. Questions about the impact of emerging applications like AI, 5G, and automotive electronics on packaging demand are common, as is curiosity regarding investment opportunities and strategic partnerships within the sector. The insights gathered point to a market characterized by continuous innovation and robust demand, driven by pervasive digitalization across industries.

- Strong Growth Trajectory: Market projected for substantial growth, driven by digital transformation.

- Advanced Packaging Dominance: Solutions like 3D ICs and FOWLP will be key growth enablers.

- APAC Leads Growth: Asia Pacific expected to remain the largest and fastest-growing region.

- Diverse Application Demand: Growth fueled by AI, 5G, IoT, automotive, and high-performance computing.

- Investment Opportunities: Significant potential for R&D and manufacturing capacity expansion.

- Technology Convergence: Market benefits from the integration of diverse functionalities into single packages.

Semiconductor Package Market Drivers Analysis

The semiconductor package market is propelled by a confluence of technological advancements and increasing demand across various end-use industries. The relentless pursuit of miniaturization and enhanced performance in electronic devices necessitates more sophisticated packaging solutions that can accommodate higher transistor densities and faster data transfer rates. This intrinsic demand for advanced functionalities, coupled with the proliferation of smart devices and complex systems, directly drives innovation and adoption in packaging technologies.

Furthermore, the rapid expansion of emerging technologies such as Artificial Intelligence (AI), 5G communication, Internet of Things (IoT), and high-performance computing (HPC) significantly contributes to market growth. These applications require specialized packaging that offers superior electrical performance, improved thermal dissipation, and greater reliability. The automotive sector, particularly with the advent of electric vehicles (EVs) and autonomous driving, presents another strong growth catalyst, demanding robust and durable packaging capable of operating under harsh environmental conditions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Advanced Packaging Technologies | +2.5% | Global, particularly APAC (Taiwan, South Korea) | 2025-2033 |

| Proliferation of AI, 5G, and IoT Devices | +2.0% | Global, especially North America, China, Europe | 2025-2033 |

| Increasing Adoption in Automotive Electronics | +1.5% | Europe, North America, Japan, China | 2025-2033 |

| Miniaturization and Performance Enhancement Needs | +1.0% | Global | 2025-2033 |

| Heterogeneous Integration and Chiplet Architectures | +1.2% | Global, focusing on R&D hubs | 2027-2033 |

Semiconductor Package Market Restraints Analysis

Despite robust growth prospects, the semiconductor package market faces several significant restraints. One primary challenge is the escalating cost associated with advanced packaging technologies. Developing and implementing solutions like 3D stacking, fan-out wafer-level packaging, and advanced flip-chip technologies require substantial capital investment in R&D, specialized equipment, and skilled labor. These high upfront costs can deter smaller players and potentially slow the adoption rate, especially in price-sensitive segments.

Another crucial restraint is the inherent complexity and technical challenges involved in designing and manufacturing advanced packages. Issues such as thermal management, signal integrity, and power delivery become increasingly difficult to manage as packages become denser and integrate more diverse functionalities. Furthermore, the global semiconductor supply chain remains vulnerable to geopolitical tensions, trade disputes, and natural disasters, which can lead to disruptions in material supply, production delays, and increased raw material costs, thereby impacting market stability and growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Investment and R&D Costs for Advanced Packaging | -1.8% | Global | 2025-2033 |

| Increasing Design Complexity and Thermal Management Challenges | -1.5% | Global | 2025-2033 |

| Geopolitical Tensions and Supply Chain Vulnerabilities | -1.2% | Global, particularly impacted by US-China relations | 2025-2029 |

| Scarcity of Skilled Workforce | -0.8% | North America, Europe, Asia | 2025-2033 |

Semiconductor Package Market Opportunities Analysis

The semiconductor package market is poised for significant opportunities driven by evolving technological landscapes and expanding application domains. The accelerating adoption of Artificial Intelligence (AI) and Machine Learning (ML) across various industries presents a substantial opportunity for advanced packaging solutions that can support the high computational demands and specialized hardware requirements of AI accelerators. This includes demand for high-bandwidth memory (HBM) integration and sophisticated multi-chip modules that enable powerful AI processing at the edge and in data centers.

Furthermore, the global rollout of 5G networks and the pervasive growth of the Internet of Things (IoT) create vast opportunities for compact, energy-efficient, and highly integrated packaging solutions. These applications necessitate smaller form factors, enhanced radio frequency (RF) performance, and low-power consumption, pushing the boundaries of current packaging technologies. The increasing focus on sustainability and eco-friendly manufacturing also opens avenues for innovation in greener packaging materials and processes, aligning with global environmental objectives and potentially attracting new investments.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of AI and Machine Learning Hardware | +2.3% | Global, particularly North America, China | 2025-2033 |

| Expansion of 5G and IoT Ecosystems | +2.0% | Global | 2025-2033 |

| Growth in Medical and Wearable Electronics | +1.5% | North America, Europe, East Asia | 2026-2033 |

| Development of Sustainable Packaging Materials and Processes | +1.0% | Europe, North America | 2027-2033 |

Semiconductor Package Market Challenges Impact Analysis

The semiconductor package market faces significant challenges that could impede its growth trajectory. The rapid pace of technological change necessitates continuous investment in research and development, making it challenging for companies to keep up with evolving standards and adopt new processes quickly. This fast innovation cycle also shortens product lifecycles, requiring manufacturers to constantly retool and update their facilities, which places considerable financial strain on operational budgets.

Another major challenge is the increasing complexity of advanced packaging designs, which demands highly specialized expertise and sophisticated manufacturing techniques. Achieving high yields and reliability for multi-die integration and 3D stacking often involves intricate processes and stringent quality control, leading to higher production costs and potential delays. Furthermore, intellectual property rights and patent disputes surrounding innovative packaging technologies pose risks, as they can lead to costly legal battles and restrict market access for certain innovations, impacting overall market competitiveness.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence and Need for Constant Innovation | -1.7% | Global | 2025-2033 |

| Ensuring High Yield and Reliability in Advanced Packaging | -1.4% | Global | 2025-2033 |

| Regulatory Compliance and Environmental Concerns | -1.0% | Europe, North America, East Asia | 2025-2033 |

| Intellectual Property and Patent Litigation Risks | -0.7% | Global | 2025-2033 |

Semiconductor Package Market - Updated Report Scope

This market research report provides an in-depth analysis of the global Semiconductor Package market, covering historical data from 2019 to 2023, base year 2024, and forecasts through 2033. The scope encompasses market size estimations, growth drivers, restraints, opportunities, and challenges across various segments and regions. It includes comprehensive competitive landscape analysis, highlighting key players and their strategic developments.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 48.5 Billion |

| Market Forecast in 2033 | USD 95.8 Billion |

| Growth Rate | 8.9% CAGR |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ASE Technology Holding Co., Ltd., Amkor Technology, Inc., Jiangsu Changjiang Electronics Technology Co., Ltd. (JCET), SPIL (Siliconware Precision Industries Co., Ltd.), United Microelectronics Corporation (UMC), Intel Corporation, Samsung Electronics Co., Ltd., Taiwan Semiconductor Manufacturing Company (TSMC), Texas Instruments Incorporated, Renesas Electronics Corporation, STMicroelectronics N.V., NXP Semiconductors N.V., Infineon Technologies AG, Micron Technology, Inc., SK Hynix Inc., Fuji Electric Co., Ltd., Shinko Electric Industries Co., Ltd., Unisem (M) Berhad, Powertech Technology Inc., King Yuan Electronics Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The semiconductor package market is extensively segmented by type, material, and application, reflecting the diverse technological approaches and end-use demands within the industry. Each segment represents distinct market dynamics, driven by specific technological needs for performance, cost-efficiency, and reliability. This granular segmentation allows for a detailed understanding of market trends and growth opportunities within specialized niches, from traditional wire bonding to cutting-edge 3D IC technologies.

- By Type:

- Wire Bond: Traditional, cost-effective packaging for various applications.

- Flip Chip: Enhanced performance and smaller footprint via direct chip-to-substrate connection.

- Fan-Out Wafer-Level Packaging (FOWLP): High I/O density and small form factor without a traditional substrate.

- Fan-In Wafer-Level Packaging (FIWLP): Compact and cost-effective for devices with lower I/O counts.

- 3D IC (Through-Silicon Via - TSV): Vertical stacking of multiple dies for high bandwidth and integration.

- Embedded Die: Dies directly integrated into a substrate for ultra-thin profiles.

- System-in-Package (SiP): Integration of multiple ICs and passive components into a single package.

- Other Advanced Packages: Including wafer-level chip-scale packages (WLCSP) and module-level solutions.

- By Material:

- Leadframes: Metal frames for mechanical support and electrical connections.

- Substrates: Organic (e.g., BT resin, Ajinomoto Build-up Film - ABF) and Ceramic (e.g., Alumina, AlN).

- Bonding Wires: Gold, Copper, Silver, Aluminum wires for electrical interconnections.

- Encapsulation Resins: Mold compounds for protecting the chip and internal connections.

- Die Attach Materials: Adhesives (e.g., epoxy, solder) for mounting the chip to the substrate.

- Solder Balls: Used in flip-chip and BGA packages for electrical and mechanical connections.

- By Application:

- Consumer Electronics: Smartphones, tablets, wearables, laptops, gaming consoles, digital cameras.

- Automotive: Advanced Driver-Assistance Systems (ADAS), infotainment systems, powertrain control, body electronics.

- Telecommunications: 5G base stations, network routers, switches, fiber optic transceivers.

- Industrial: Automation systems, robotics, power management, industrial IoT devices.

- Healthcare: Medical imaging equipment, diagnostic tools, wearable health monitors, implantable devices.

- Aerospace & Defense: Avionics, radar systems, satellite communication, military electronics.

- Data Centers & Cloud Computing: Servers, storage devices, networking equipment, AI accelerators.

- Other Applications: Includes energy, smart home devices, and security systems.

Regional Highlights

- Asia Pacific (APAC) dominates the semiconductor package market due to the presence of major foundries, OSAT (Outsourced Semiconductor Assembly and Test) companies, and a robust electronics manufacturing ecosystem, particularly in Taiwan, South Korea, China, and Japan. The region benefits from significant investments in advanced packaging technologies and a large consumer electronics manufacturing base.

- North America exhibits strong growth driven by demand for high-performance computing, AI, and advanced automotive electronics. The region is home to leading semiconductor design companies and a growing number of advanced packaging R&D initiatives, coupled with strategic investments aimed at re-shoring manufacturing capabilities.

- Europe demonstrates consistent growth, largely fueled by the automotive and industrial electronics sectors, alongside an increasing focus on IoT and sustainable technology. Countries like Germany and France are significant contributors due to their strong manufacturing and research infrastructure.

- Latin America and Middle East & Africa (MEA) are emerging markets, showing gradual growth primarily in consumer electronics and telecommunications infrastructure. While smaller in market share, these regions offer potential opportunities due to increasing digitalization and infrastructure development.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Semiconductor Package Market.- ASE Technology Holding Co., Ltd.

- Amkor Technology, Inc.

- Jiangsu Changjiang Electronics Technology Co., Ltd. (JCET)

- SPIL (Siliconware Precision Industries Co., Ltd.)

- United Microelectronics Corporation (UMC)

- Intel Corporation

- Samsung Electronics Co., Ltd.

- Taiwan Semiconductor Manufacturing Company (TSMC)

- Texas Instruments Incorporated

- Renesas Electronics Corporation

- STMicroelectronics N.V.

- NXP Semiconductors N.V.

- Infineon Technologies AG

- Micron Technology, Inc.

- SK Hynix Inc.

- Fuji Electric Co., Ltd.

- Shinko Electric Industries Co., Ltd.

- Unisem (M) Berhad

- Powertech Technology Inc.

- King Yuan Electronics Co., Ltd.

Frequently Asked Questions

Analyze common user questions about the Semiconductor Package market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate for the Semiconductor Package Market?

The Semiconductor Package Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2025 and 2033, driven by increasing demand for advanced electronic devices and emerging technologies.

Which are the most significant trends impacting semiconductor packaging?

Key trends include the rapid adoption of advanced packaging solutions like 3D ICs and FOWLP, the push for heterogeneous integration, continuous miniaturization, and the increasing focus on thermal management innovations for high-performance applications.

How is AI influencing the Semiconductor Package industry?

AI is significantly impacting the industry by optimizing package design and layout, enhancing automated inspection processes for defect detection, improving manufacturing yield, and enabling predictive maintenance for equipment, leading to greater efficiency and reliability.

What are the primary drivers for the growth of the Semiconductor Package Market?

The market's growth is primarily driven by the escalating demand for advanced packaging technologies, the proliferation of AI, 5G, and IoT devices, increasing adoption in automotive electronics, and the ongoing need for miniaturization and enhanced performance in electronic systems.

Which region is expected to lead the Semiconductor Package Market?

The Asia Pacific (APAC) region is expected to continue leading the Semiconductor Package Market, driven by its robust semiconductor manufacturing ecosystem, significant investments in advanced packaging, and a large consumer electronics production base, particularly in countries like Taiwan, South Korea, and China.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted