Industrial Valve Market

Industrial Valve Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704688 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

Industrial Valve Market Size

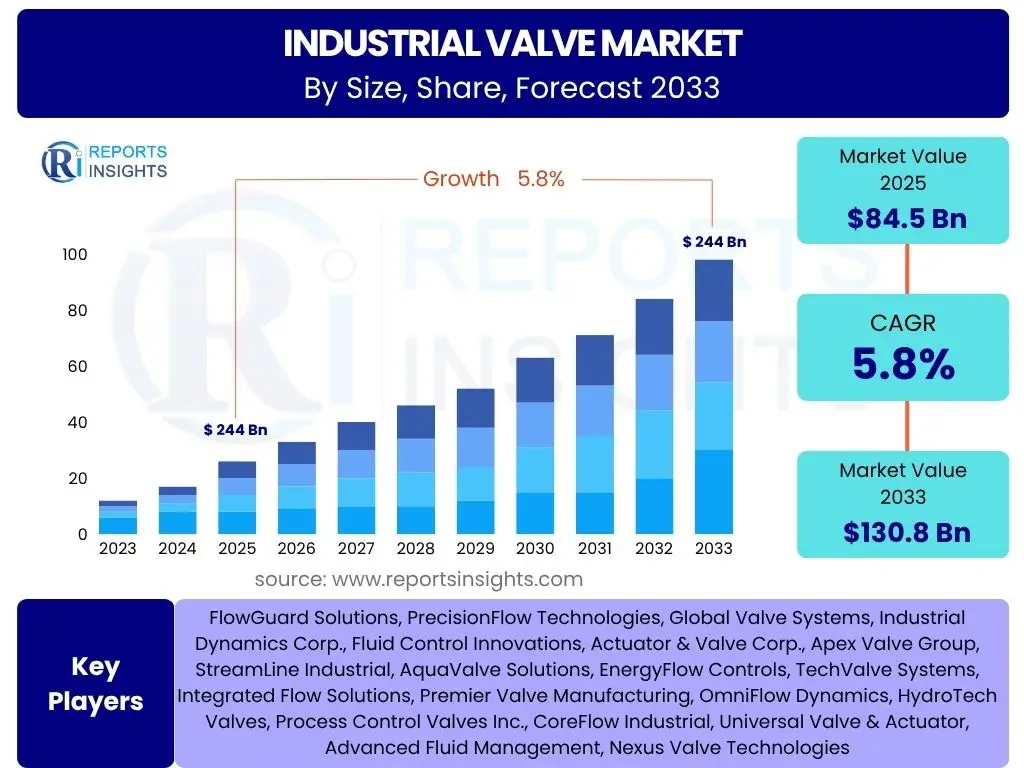

According to Reports Insights Consulting Pvt Ltd, The Industrial Valve Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 84.5 Billion in 2025 and is projected to reach USD 130.8 Billion by the end of the forecast period in 2033.

Key Industrial Valve Market Trends & Insights

The industrial valve market is undergoing significant transformation, driven by a confluence of technological advancements, evolving industrial demands, and increasing focus on efficiency and sustainability. Key trends indicate a strong shift towards intelligent and automated valve systems, which offer enhanced control, predictive maintenance capabilities, and real-time operational insights. This digital transformation is paramount in optimizing industrial processes, reducing operational costs, and ensuring compliance with stringent safety and environmental regulations across various sectors.

Furthermore, the global emphasis on renewable energy infrastructure and water management projects is creating new avenues for specialized valve solutions. Industries are also prioritizing materials that offer superior resistance to corrosion, extreme temperatures, and high pressures, leading to innovations in valve metallurgy and design. The integration of advanced analytics and IoT (Internet of Things) platforms with valve systems is also becoming a standard, enabling smarter decision-making and minimizing downtime, thereby enhancing the overall reliability and performance of industrial operations.

- Adoption of Smart Valves and IoT Integration for enhanced monitoring and control.

- Increased demand for customized and application-specific valve solutions.

- Focus on lightweight and high-performance materials for improved durability.

- Rising investment in renewable energy and water infrastructure projects.

- Growing emphasis on predictive maintenance and asset performance management.

- Stringent environmental regulations driving demand for emission-reducing valves.

AI Impact Analysis on Industrial Valve

Artificial Intelligence (AI) is set to profoundly impact the industrial valve sector by revolutionizing operational efficiency, maintenance strategies, and design processes. Users are keenly interested in how AI can facilitate predictive maintenance, shifting from reactive repairs to proactive interventions that minimize downtime and extend valve lifespan. AI algorithms can analyze vast datasets from sensors on valves, identifying anomalies and predicting potential failures long before they occur, thus optimizing maintenance schedules and reducing unexpected operational disruptions. This capability is crucial for industries where continuous operation is critical, such as oil and gas, power generation, and chemical processing.

Beyond maintenance, AI is also influencing valve design and manufacturing. Generative design, powered by AI, allows engineers to explore a multitude of design iterations rapidly, optimizing for performance, material usage, and manufacturing feasibility. This can lead to lighter, more efficient, and more robust valve components. Additionally, AI-driven process optimization in manufacturing can enhance quality control, reduce waste, and streamline production workflows. However, users also express concerns regarding the complexity and cost of AI implementation, the need for skilled personnel to manage these systems, and data security challenges associated with connected industrial infrastructure. Addressing these concerns through standardized protocols and workforce training will be vital for widespread AI adoption in the valve market.

- Enhanced Predictive Maintenance: AI algorithms analyze sensor data to forecast valve failures, enabling proactive repairs and reducing unplanned downtime.

- Optimized Operational Efficiency: AI-driven control systems adjust valve performance in real-time, leading to improved process flow and energy consumption.

- Smart Design and Manufacturing: AI assists in generative design for optimized valve structures and enhances quality control in production.

- Remote Monitoring and Diagnostics: AI empowers remote oversight of valve health, facilitating quicker response times and reduced on-site inspection needs.

- Supply Chain Optimization: AI can predict demand fluctuations and optimize inventory management for valve components and finished products.

- Cybersecurity Concerns: Increased connectivity of smart valves raises challenges related to data privacy and protection against cyber threats.

- Workforce Reskilling: Adoption of AI necessitates training for personnel in data analytics, AI system management, and advanced maintenance techniques.

Key Takeaways Industrial Valve Market Size & Forecast

The industrial valve market is poised for robust growth, driven primarily by ongoing industrialization in developing economies, significant investments in infrastructure projects, and the modernization of existing industrial facilities. The forecast period highlights a steady expansion, fueled by increasing demand from critical sectors such as oil and gas, power generation, water and wastewater treatment, and chemical industries, all of which rely heavily on efficient fluid control mechanisms. The escalating need for automation and enhanced process efficiency across these industries further propels the adoption of advanced valve technologies, ensuring sustained market momentum.

Furthermore, the market's trajectory is influenced by stringent regulatory frameworks concerning environmental protection and safety, which mandate the use of high-performance and reliable valve systems. This regulatory push, combined with a growing focus on energy efficiency and emission reduction, encourages innovation in valve design and materials. The integration of smart technologies, including IoT and AI, into valve systems is a pivotal factor contributing to the positive market outlook, enhancing operational intelligence and paving the way for predictive maintenance strategies. Overall, the market's future remains promising, underpinned by continuous technological advancements and indispensable demand from vital industrial applications globally.

- Consistent growth projected through 2033, driven by industrial expansion and infrastructure development.

- Significant contributions from the oil and gas, power, and water treatment sectors.

- Technological advancements, including smart valves and automation, are key enablers.

- Regulatory compliance and sustainability initiatives are shaping market demand.

- Asia Pacific is expected to be a major growth engine due to rapid industrialization.

Industrial Valve Market Drivers Analysis

The industrial valve market is predominantly driven by the expansion of infrastructure and the rapid industrialization occurring globally, particularly in emerging economies. This includes large-scale projects in power generation, water distribution, and various manufacturing sectors, all of which require sophisticated fluid control systems. The increasing complexity of industrial processes and the need for precision control also contribute significantly to the demand for advanced valve solutions, pushing manufacturers to innovate and provide more reliable and efficient products. Furthermore, the global drive towards cleaner energy sources and sustainable practices necessitates the upgrade of existing facilities and the construction of new ones, creating continuous demand for specialized valves.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Industrialization & Urbanization | +1.5% | Asia Pacific, Latin America, MEA | 2025-2033 |

| Increasing Investments in Infrastructure Projects | +1.2% | Global, notably China, India, USA, Europe | 2025-2033 |

| Rising Demand from Oil & Gas, Power, and Water Treatment | +1.0% | North America, Middle East, Asia Pacific | 2025-2033 |

| Technological Advancements in Automation & Smart Valves | +0.8% | Developed Regions (North America, Europe), East Asia | 2025-2033 |

| Stringent Regulatory Landscape for Safety & Environment | +0.5% | Europe, North America, APAC | 2025-2033 |

Industrial Valve Market Restraints Analysis

Despite robust growth drivers, the industrial valve market faces several notable restraints that could impede its expansion. Fluctuations in raw material prices, particularly for metals like steel, iron, and various alloys, directly impact manufacturing costs and, consequently, the final product pricing. This volatility can lead to unpredictable market conditions and reduced profit margins for manufacturers. Economic downturns and geopolitical instabilities also play a significant role, as they can lead to delays or cancellations of large-scale industrial projects, thereby reducing overall demand for industrial valves. The capital-intensive nature of valve manufacturing and the high initial investment required for adopting advanced valve technologies can also pose a barrier to entry for new players and slow down technology adoption in price-sensitive markets.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices | -0.7% | Global | Short to Mid-term (2025-2028) |

| Economic Slowdown & Geopolitical Instability | -0.5% | Global, particularly vulnerable regions | Short-term (2025-2027) |

| High Initial Investment & Installation Costs | -0.4% | Emerging Markets | 2025-2033 |

| Intense Competition from Local Manufacturers | -0.3% | Asia Pacific, Latin America | 2025-2033 |

Industrial Valve Market Opportunities Analysis

The industrial valve market is ripe with opportunities stemming from the global shift towards renewable energy sources and the ongoing digital transformation of industries. The expansion of sectors such as hydrogen production, carbon capture, and concentrated solar power creates new demands for specialized valves capable of handling unique media and extreme operating conditions. Furthermore, the increasing adoption of IoT and AI in industrial settings presents significant opportunities for smart and connected valve systems, enabling real-time monitoring, predictive maintenance, and optimized operational control. These technological integrations can drive higher efficiency and lower operational costs for end-users, fostering greater market penetration.

Moreover, the aftermarket services segment, including maintenance, repair, and replacement of existing valve installations, represents a substantial and stable revenue stream. As industrial infrastructure ages globally, the need for servicing and upgrading becomes paramount, offering continuous demand irrespective of new project cycles. The growing focus on environmental compliance and energy efficiency also opens doors for energy-saving valve designs and solutions that help industries reduce their carbon footprint, aligning with global sustainability goals. Penetrating emerging markets with tailored solutions, coupled with strategic partnerships and mergers, further enhances the market opportunity landscape.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Smart Valves and IoT Integration | +1.3% | Global, high adoption in developed regions | 2025-2033 |

| Growth in Renewable Energy and Hydrogen Infrastructure | +1.1% | Europe, North America, East Asia | 2025-2033 |

| Expansion in Water and Wastewater Management | +0.9% | Asia Pacific, Middle East, Africa | 2025-2033 |

| Significant Aftermarket Services Potential | +0.7% | Global | 2025-2033 |

| Increasing Focus on Energy Efficiency and Sustainability | +0.6% | Europe, North America | 2025-2033 |

Industrial Valve Market Challenges Impact Analysis

The industrial valve market faces several complex challenges that can hinder its growth and operational stability. One significant hurdle is the increasing stringency of regulatory standards, particularly concerning environmental emissions and safety. While driving innovation, compliance with diverse and evolving global regulations can lead to higher manufacturing costs and necessitate continuous research and development, posing a burden for smaller manufacturers. Furthermore, the market is susceptible to supply chain disruptions, which can arise from geopolitical tensions, natural disasters, or pandemics, leading to material shortages, increased lead times, and inflated costs, thereby impacting production schedules and profitability.

Another critical challenge is the shortage of skilled labor, especially technicians proficient in installing, maintaining, and troubleshooting advanced valve systems and associated digital technologies. The complexity of modern industrial valves, coupled with the integration of IoT and AI, demands a highly specialized workforce that is currently in short supply. Moreover, intense price competition, particularly from manufacturers in emerging economies offering lower-cost alternatives, can exert downward pressure on profit margins for established players. Ensuring robust cybersecurity measures for smart, connected valves also presents a growing challenge, as vulnerabilities could lead to operational disruptions or data breaches, requiring substantial investment in protective technologies.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent & Evolving Regulatory Compliance | -0.8% | Global, particularly Europe, North America | 2025-2033 |

| Supply Chain Disruptions and Geopolitical Risks | -0.6% | Global | Short to Mid-term (2025-2028) |

| Shortage of Skilled Workforce | -0.5% | Global | 2025-2033 |

| Intense Price Competition | -0.4% | Global, especially competitive regions | 2025-2033 |

| Cybersecurity Risks for Smart Valve Systems | -0.3% | Developed Regions | 2025-2033 |

Industrial Valve Market - Updated Report Scope

This comprehensive market research report delves into the intricate dynamics of the global industrial valve market, offering an in-depth analysis of its size, growth trajectories, and future projections. The scope encompasses a detailed examination of key market segments, including valve types, materials, applications, and end-user industries, providing a granular understanding of the market landscape. It further explores the prevailing market trends, influential growth drivers, significant restraints, emerging opportunities, and critical challenges that are shaping the competitive environment. The report also highlights the regional market performances and outlines the profiles of prominent industry players, offering strategic insights for stakeholders. This extensive analysis is designed to provide businesses with the actionable intelligence necessary for informed decision-making, strategic planning, and identifying lucrative investment avenues within the industrial valve sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 84.5 Billion |

| Market Forecast in 2033 | USD 130.8 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | FlowGuard Solutions, PrecisionFlow Technologies, Global Valve Systems, Industrial Dynamics Corp., Fluid Control Innovations, Actuator & Valve Corp., Apex Valve Group, StreamLine Industrial, AquaValve Solutions, EnergyFlow Controls, TechValve Systems, Integrated Flow Solutions, Premier Valve Manufacturing, OmniFlow Dynamics, HydroTech Valves, Process Control Valves Inc., CoreFlow Industrial, Universal Valve & Actuator, Advanced Fluid Management, Nexus Valve Technologies |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The industrial valve market is extensively segmented to provide a granular understanding of its diverse components and their respective dynamics. These segmentations are critical for identifying specific growth pockets, understanding demand patterns, and tailoring product development and market strategies. The primary segmentation categories include valve type, the materials used in their construction, their specific applications across various industries, and the end-user sectors that utilize them. Each segment exhibits unique characteristics driven by distinct operational requirements, regulatory landscapes, and technological advancements.

Understanding these segments allows market participants to recognize specialized needs, such as the demand for high-pressure control valves in the oil and gas sector or corrosion-resistant valves for chemical processing. The material segmentation reflects the evolving preferences for durability, cost-efficiency, and performance under extreme conditions. Application-specific analysis highlights the indispensable role of valves in critical infrastructure and industrial processes, while end-user segmentation provides insights into the diverse industries driving market demand, from heavy manufacturing to essential utilities. This multi-faceted segmentation ensures a comprehensive view of the market's structure and potential for growth within each niche.

- By Type: Gate Valves, Globe Valves, Ball Valves, Butterfly Valves, Check Valves, Plug Valves, Diaphragm Valves, Pressure Relief Valves, Control Valves, Others (e.g., Pinch Valves, Knife Gate Valves).

- By Material: Cast Iron, Steel (Carbon Steel, Stainless Steel, Alloy Steel), Cryogenic Materials, Plastic, Bronze, Brass, Others (e.g., Exotic Alloys, Composite Materials).

- By Application: Oil and Gas (Upstream, Midstream, Downstream), Water and Wastewater Treatment, Power Generation (Thermal, Nuclear, Renewables), Chemical and Petrochemical, Building and Construction, Mining, Food and Beverage, Pharmaceuticals, Pulp and Paper, Marine, Others (e.g., HVAC, Semiconductors).

- By End-User: Manufacturing, Infrastructure, Commercial, Utilities, Residential.

Regional Highlights

- North America: This region maintains a significant market share due to the presence of well-established industries, continuous investment in infrastructure upgrades, and the adoption of advanced automation technologies. The shale gas boom has fueled demand for specialized valves in the oil and gas sector, while stringent environmental regulations drive the need for high-performance, compliant valve solutions. Demand is also robust from power generation and chemical processing industries.

- Europe: Characterized by mature industrial economies and a strong focus on environmental sustainability and energy efficiency, Europe is a key market for innovative valve solutions. The region's emphasis on renewable energy projects, smart city initiatives, and advanced manufacturing technologies drives the demand for smart valves and those designed for high-purity and high-performance applications. Stringent ATEX and CE certifications also shape product development.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, propelled by rapid industrialization, urbanization, and large-scale infrastructure development projects in countries like China, India, and Southeast Asia. Significant investments in power generation (including renewables), water treatment, oil and gas, and chemical industries contribute substantially to market expansion. The region also benefits from a burgeoning manufacturing sector and increasing foreign direct investment.

- Latin America: This region is experiencing steady growth, driven by investments in the oil and gas sector, particularly in Brazil and Mexico, and ongoing infrastructure development. The expanding mining industry and increasing demand for improved water and wastewater infrastructure also contribute to market growth. Economic stability and governmental initiatives aimed at industrial development are key factors.

- Middle East and Africa (MEA): The MEA region is a substantial market primarily due to its vast oil and gas reserves and ongoing investments in exploration, production, and refining capacities. Large-scale desalination projects, power generation plants, and ambitious urban development initiatives across the Gulf Cooperation Council (GCC) countries are also major contributors to the demand for industrial valves. Economic diversification efforts are opening up new industrial opportunities.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Industrial Valve Market.- FlowGuard Solutions

- PrecisionFlow Technologies

- Global Valve Systems

- Industrial Dynamics Corp.

- Fluid Control Innovations

- Actuator & Valve Corp.

- Apex Valve Group

- StreamLine Industrial

- AquaValve Solutions

- EnergyFlow Controls

- TechValve Systems

- Integrated Flow Solutions

- Premier Valve Manufacturing

- OmniFlow Dynamics

- HydroTech Valves

- Process Control Valves Inc.

- CoreFlow Industrial

- Universal Valve & Actuator

- Advanced Fluid Management

- Nexus Valve Technologies

Frequently Asked Questions

What is the projected growth rate for the Industrial Valve Market?

The Industrial Valve Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033, reaching an estimated USD 130.8 Billion by 2033.

Which key industries are driving the demand for industrial valves?

Key industries driving demand include oil and gas, power generation, water and wastewater treatment, chemical and petrochemical, and manufacturing, all requiring precise fluid control for their operations.

How is AI impacting the industrial valve sector?

AI is transforming the sector through predictive maintenance, optimizing operational efficiency, aiding in smart design and manufacturing, and enabling advanced remote monitoring and diagnostics for industrial valves.

Which region is expected to lead market growth for industrial valves?

The Asia Pacific (APAC) region is anticipated to lead market growth due to rapid industrialization, extensive infrastructure development, and significant investments in various industrial sectors across countries like China and India.

What are the primary challenges faced by the Industrial Valve Market?

Key challenges include volatile raw material prices, stringent regulatory compliance, supply chain disruptions, a shortage of skilled labor, and intense price competition, alongside growing cybersecurity risks for smart valve systems.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted