Semiconductor Equipment Market

Semiconductor Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702106 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

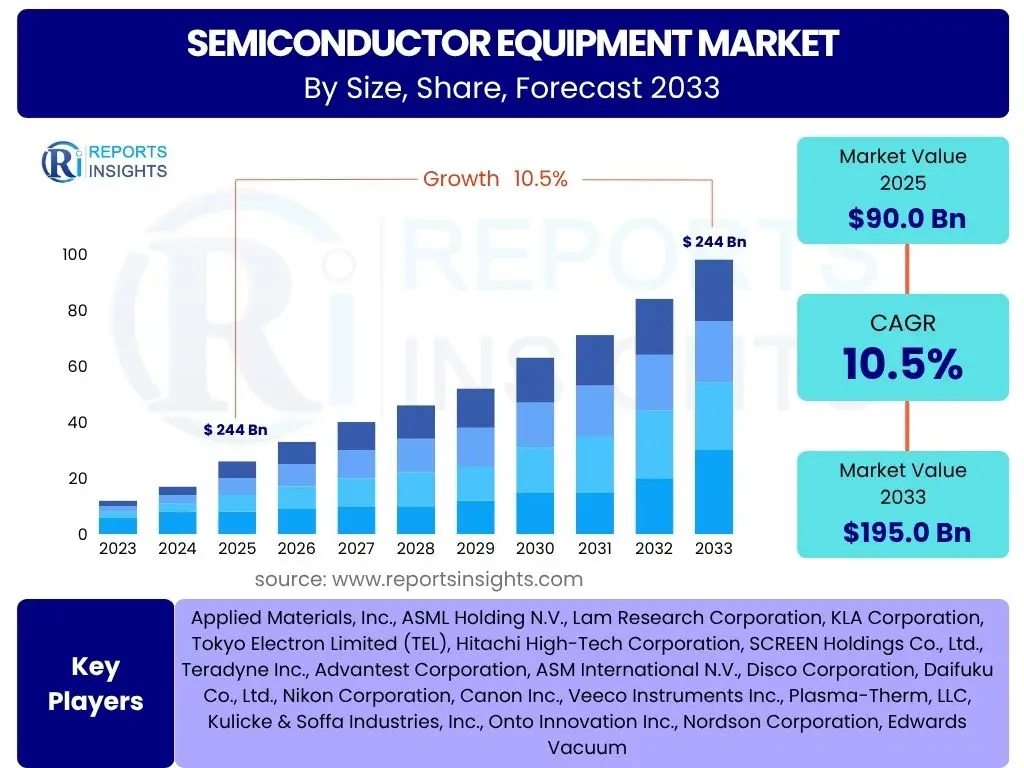

Semiconductor Equipment Market Size

According to Reports Insights Consulting Pvt Ltd, The Semiconductor Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2033. The market is estimated at USD 90.0 Billion in 2025 and is projected to reach USD 195.0 Billion by the end of the forecast period in 2033.

Key Semiconductor Equipment Market Trends & Insights

The semiconductor equipment market is currently undergoing a transformative period, shaped by several significant trends that are redefining manufacturing processes and technological capabilities. A primary trend involves the relentless pursuit of advanced miniaturization and increasing chip complexity, driven by demand for more powerful and efficient electronic devices. This necessitates continuous innovation in lithography, etching, and deposition technologies, pushing the boundaries of what is physically possible at the atomic level. Furthermore, the industry is witnessing a robust shift towards automation, artificial intelligence (AI), and machine learning (ML) integration within manufacturing facilities, optimizing production yields, reducing human error, and enhancing operational efficiency.

Another crucial insight points to the growing emphasis on sustainable manufacturing practices. As environmental concerns escalate, semiconductor equipment manufacturers are focusing on developing energy-efficient machines and processes that reduce waste, conserve resources, and lower the carbon footprint of chip production. Geopolitical shifts and the drive for supply chain resilience have also become prominent, leading to increased investment in localized manufacturing capabilities across various regions, particularly in North America and Europe, diversifying the global semiconductor ecosystem beyond its traditional Asian strongholds. These trends collectively underline a dynamic market characterized by technological advancement, operational optimization, and strategic regionalization.

- Advanced Miniaturization and Heterogeneous Integration: Driving demand for EUV lithography, advanced packaging, and 3D stacking.

- Increased Automation and Smart Manufacturing: Adoption of AI, ML, and IoT for predictive maintenance, process control, and yield optimization.

- Sustainability Initiatives: Focus on energy-efficient equipment, waste reduction, and green manufacturing processes.

- Supply Chain Localization and Diversification: Reshoring and nearshoring of manufacturing capacities to enhance regional resilience.

- Growth in Specialty Materials and Advanced Processes: Development of novel materials and techniques for next-generation devices, including GaN and SiC.

AI Impact Analysis on Semiconductor Equipment

The profound impact of Artificial Intelligence (AI) on the semiconductor equipment market is a dominant theme in user inquiries, reflecting widespread interest in how this technology is reshaping the industry. Users frequently question how AI is being leveraged within manufacturing processes to enhance efficiency, reduce costs, and improve chip quality. The integration of AI and machine learning algorithms into semiconductor fabrication tools is revolutionizing operations, enabling capabilities such as real-time process monitoring, predictive maintenance, and sophisticated defect detection. This allows for proactive adjustments to equipment, minimizing downtime and optimizing yield rates, which are critical in a capital-intensive industry with stringent quality requirements.

Beyond optimizing manufacturing, AI's influence extends to the demand side, driving the need for new generations of high-performance chips designed specifically for AI workloads. This creates a direct pull for advanced manufacturing equipment capable of producing complex AI accelerators, neural processing units (NPUs), and specialized memory solutions. Consequently, equipment manufacturers are investing heavily in research and development to deliver tools that can meet these evolving design and production requirements, including capabilities for advanced packaging and heterogeneous integration. The continuous evolution of AI will thus perpetuate a cycle of innovation in semiconductor equipment, pushing the boundaries of material science, process control, and metrology to support the ever-increasing computational demands of AI applications across various sectors.

- Enhanced Process Optimization: AI algorithms optimize manufacturing parameters for improved yield and efficiency.

- Predictive Maintenance: AI-driven analytics forecast equipment failures, reducing unplanned downtime and maintenance costs.

- Advanced Defect Detection: AI-powered vision systems identify microscopic defects with higher accuracy and speed.

- Accelerated R&D and Design: AI assists in simulating new material properties and optimizing chip designs.

- Increased Demand for High-Performance Chips: Growth of AI applications drives the need for advanced manufacturing equipment for specialized AI processors.

Key Takeaways Semiconductor Equipment Market Size & Forecast

A central theme in common inquiries regarding the semiconductor equipment market's size and forecast revolves around understanding the underlying drivers of its projected robust growth. Stakeholders are keen to ascertain what factors will sustain the significant compound annual growth rate anticipated through 2033. The primary takeaway is that this market's expansion is intrinsically linked to the pervasive digitalization of the global economy, the proliferation of data-intensive technologies, and the strategic importance of semiconductors in geopolitical landscapes. The forecast reflects an expectation of sustained investment in fabrication facilities (fabs) globally, fueled by both established technology leaders and emerging regional players aiming for supply chain self-sufficiency.

Another critical insight gathered from market inquiries emphasizes the role of technological advancements as a continuous growth catalyst. The transition to more complex chip architectures, the imperative for higher performance, and the growing demand for specialized components in burgeoning sectors such as artificial intelligence, 5G, automotive electronics, and the Internet of Things (IoT) are compelling equipment manufacturers to innovate. These forces ensure a steady demand for cutting-edge tools and services required for leading-edge node production and advanced packaging techniques. The market's resilience, despite cyclical industry trends, points towards a foundational and indispensable role for semiconductor equipment in the global technology ecosystem, underpinned by long-term strategic investments and persistent technological evolution.

- Strong Growth Trajectory: Market projected to nearly double from 2025 to 2033, driven by continuous technological advancements and increasing chip demand.

- Foundational Industry: Semiconductor equipment remains critical for global digital transformation, supporting advancements in AI, 5G, IoT, and high-performance computing.

- Strategic Global Investments: Significant capital expenditure in new and upgraded fabs worldwide underpins market expansion.

- Innovation Imperative: Ongoing R&D in lithography, deposition, etching, and metrology tools is essential for next-generation chip production.

- Resilience to Cyclicality: Despite inherent industry cycles, long-term demand for advanced semiconductors ensures sustained investment in equipment.

Semiconductor Equipment Market Drivers Analysis

The semiconductor equipment market is significantly propelled by the relentless global demand for advanced electronic devices and the fundamental digitalization occurring across industries. The rapid expansion of sectors such as artificial intelligence, 5G telecommunications, the Internet of Things (IoT), and high-performance computing necessitates increasingly sophisticated and powerful semiconductors. This creates a direct and continuous demand for state-of-the-art manufacturing equipment capable of producing chips with higher transistor densities, improved energy efficiency, and enhanced functionalities. Furthermore, the automotive industry's pivot towards electric vehicles (EVs) and autonomous driving systems substantially boosts the need for specialized power semiconductors and sensor chips, requiring new types of fabrication and testing equipment.

Another pivotal driver is the ongoing expansion of data centers and cloud infrastructure worldwide. The exponential growth in data generation and consumption fuels the need for massive data storage, processing, and networking capabilities, all reliant on advanced semiconductor components. This necessitates significant investments in memory chips, processors, and specialized accelerators, which in turn drives demand for the equipment used in their fabrication. Additionally, geopolitical considerations and national security concerns have spurred many countries to invest heavily in domestic semiconductor manufacturing capabilities, leading to the construction of new fabs and the upgrading of existing ones across North America, Europe, and Asia. These strategic investments ensure a steady pipeline of orders for semiconductor equipment manufacturers, supporting market growth and diversification.

Finally, the evolution towards advanced packaging technologies, such as 3D stacking, heterogeneous integration, and chiplets, is a crucial driver. These innovations allow for greater integration, improved performance, and reduced form factors, even when traditional Moore's Law scaling becomes more challenging. Equipment capable of precise stacking, bonding, and testing of these complex packages is in high demand, opening new avenues for growth within the back-end segment of the market. The confluence of these technological advancements, escalating demand for compute power, and strategic investments forms a robust foundation for the sustained growth of the semiconductor equipment market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Exponential Growth of AI, 5G, IoT, and HPC | +3.0% | Global, particularly North America, APAC (China, South Korea, Taiwan) | 2025-2033 |

| Increased Investment in New Fabs and Capacity Expansion | +2.5% | North America (USA), Europe (Germany, France), APAC (Japan, China, Taiwan, South Korea) | 2025-2030 |

| Development of Advanced Packaging Technologies | +2.0% | Global, with strong innovation in APAC (Taiwan, South Korea, Japan) and North America | 2025-2033 |

| Automotive Electrification and Autonomous Driving | +1.5% | Europe, North America, APAC (China, Japan) | 2026-2033 |

Semiconductor Equipment Market Restraints Analysis

Despite its robust growth trajectory, the semiconductor equipment market faces several significant restraints that could temper its expansion. One primary concern is the inherent cyclical nature of the semiconductor industry, characterized by boom-and-bust cycles driven by fluctuations in demand, inventory corrections, and economic downturns. These cycles can lead to periods of overcapacity or underutilization of equipment, affecting investment decisions and revenue predictability for equipment manufacturers. Furthermore, the extremely high capital expenditure required to establish and upgrade semiconductor fabrication plants poses a substantial barrier, limiting the number of new entrants and making expansion challenging even for established players, particularly during periods of economic uncertainty or tighter credit conditions.

Geopolitical tensions and trade disputes represent another considerable restraint. The semiconductor industry is deeply intertwined with international relations, and ongoing conflicts or protectionist policies can disrupt global supply chains, restrict technology transfers, and impose tariffs or export controls. Such measures can significantly impact the sourcing of critical components, raw materials, or even the sale of advanced equipment, leading to delays, increased costs, and reduced market access for manufacturers. The complex web of international regulations and political considerations adds a layer of unpredictability, forcing companies to re-evaluate their global strategies and potentially leading to less efficient regionalization efforts.

Lastly, the market is constrained by the escalating costs and complexity of research and development (R&D) for next-generation equipment. As chip designs push the limits of physics, developing tools for extreme ultraviolet (EUV) lithography, advanced etching, and metrology becomes exponentially more expensive and technically challenging. This necessitates significant, long-term investments with uncertain returns, and a highly specialized workforce. The difficulty in attracting and retaining highly skilled engineers and scientists further exacerbates this challenge, potentially slowing down innovation and the commercialization of new technologies, thereby limiting the pace at which the market can introduce new capabilities and sustain its growth momentum.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Cyclical Nature of Semiconductor Industry | -1.5% | Global, pronounced in major manufacturing regions | Short-term (2025-2027), recurrent |

| High Capital Expenditure for Fabs | -1.0% | Global, affects new entrants and expansion plans | 2025-2033 |

| Geopolitical Tensions and Trade Restrictions | -1.2% | Global, especially US-China, Europe-Asia dynamics | Ongoing |

| Shortage of Highly Skilled Workforce | -0.8% | North America, Europe, parts of APAC | 2025-2033 |

Semiconductor Equipment Market Opportunities Analysis

The semiconductor equipment market is ripe with opportunities driven by emerging technological frontiers and evolving industry paradigms. One significant area of opportunity lies in the burgeoning field of advanced packaging technologies. As traditional Moore's Law scaling faces increasing physical and economic hurdles, heterogeneous integration, 3D stacking, and chiplet designs are becoming critical for achieving higher performance and lower power consumption. This shift creates substantial demand for new generations of bonding, dicing, inspection, and test equipment specifically designed for these complex packaging architectures, opening up a specialized and high-value segment within the market.

Another major opportunity stems from the global push towards sustainable and environmentally friendly manufacturing. As regulatory pressures intensify and corporate social responsibility becomes paramount, semiconductor manufacturers are increasingly investing in 'green' equipment that reduces energy consumption, minimizes waste generation, and utilizes less hazardous materials. This provides a lucrative avenue for equipment suppliers to innovate and offer solutions that align with environmental, social, and governance (ESG) goals, potentially unlocking new market segments and gaining a competitive edge through eco-conscious product development. The focus on resource efficiency and closed-loop systems will drive demand for equipment enabling these practices.

Furthermore, the development of new materials and processes beyond silicon offers significant long-term growth prospects. Emerging technologies such as gallium nitride (GaN), silicon carbide (SiC), and eventually quantum computing materials require entirely new sets of deposition, etching, and metrology tools tailored to their unique properties. This diversification away from silicon-centric manufacturing opens up entirely new markets for specialized equipment. Similarly, the increasing adoption of AI and machine learning in smart manufacturing environments creates opportunities for equipment suppliers to integrate AI-driven analytics, automation, and robotics directly into their machines, enhancing operational efficiency and providing advanced data-driven insights for their customers. These convergent technological and strategic shifts promise to redefine market landscapes and unlock substantial growth potential for agile equipment manufacturers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Advanced Packaging Technologies (3D, Heterogeneous Integration) | +2.5% | Global, with emphasis on major OSAT and IDM hubs (APAC, North America) | 2025-2033 |

| Demand for Sustainable and Energy-Efficient Equipment | +1.8% | Europe, North America, Japan, South Korea | 2026-2033 |

| Emergence of New Materials (e.g., GaN, SiC) and Quantum Computing | +1.5% | Global, particularly R&D intensive regions (North America, Europe, Japan) | 2027-2033 |

| Integration of AI/ML for Smart Manufacturing Solutions | +1.2% | Global | 2025-2033 |

Semiconductor Equipment Market Challenges Impact Analysis

The semiconductor equipment market faces several formidable challenges that require strategic navigation. One of the most pressing issues is the escalating cost of developing and acquiring cutting-edge technology. As chip feature sizes shrink and complexity increases, the research and development (R&D) costs for next-generation equipment, particularly for advanced lithography and deposition tools, have become astronomical. This high investment requirement places immense pressure on equipment manufacturers to innovate continuously while ensuring a return on their significant R&D outlays. For chipmakers, the cost of installing and maintaining these advanced systems also represents a substantial capital expenditure, influencing their fab expansion plans and upgrade cycles.

Another critical challenge is the inherent technological obsolescence risk. The rapid pace of innovation in the semiconductor industry means that equipment can become outdated relatively quickly, especially with the transition to newer process nodes or the advent of revolutionary manufacturing techniques. Equipment manufacturers must constantly anticipate future technological requirements and invest proactively to avoid falling behind competitors. This dynamic environment necessitates agile R&D cycles and a keen understanding of evolving customer needs, making long-term strategic planning particularly complex. The pressure to deliver performance enhancements with each new generation while managing product lifecycles is a continuous balancing act.

Furthermore, the semiconductor equipment supply chain is highly complex and geographically concentrated, making it vulnerable to disruptions. Events such as natural disasters, pandemics, or geopolitical conflicts can severely impact the availability of specialized components, raw materials, or skilled labor, leading to production delays and increased costs. The need for precise, high-tolerance components often means relying on a limited number of specialized suppliers, creating single points of failure. Ensuring resilience and diversification within this intricate global supply chain is a persistent operational challenge, requiring extensive risk management strategies and, increasingly, efforts towards regional localization to mitigate potential disruptions.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High R&D and Manufacturing Costs for Advanced Equipment | -1.8% | Global, impacts all major players | 2025-2033 |

| Rapid Technological Obsolescence and Innovation Pace | -1.0% | Global | Ongoing |

| Supply Chain Vulnerabilities and Geopolitical Risks | -1.5% | Global, critical impact on major manufacturing hubs | Ongoing |

| Intense Competition and Intellectual Property Protection | -0.7% | Global | 2025-2033 |

Semiconductor Equipment Market - Updated Report Scope

This market research report provides an in-depth analysis of the Semiconductor Equipment Market, covering market size, forecast, growth drivers, restraints, opportunities, and challenges. It includes a comprehensive segmentation analysis by equipment type, application, and end-use industry, along with a detailed regional outlook. The report also profiles key industry players, offering insights into their competitive landscape and strategic initiatives. This updated scope offers a holistic view of the market dynamics, aiming to provide actionable intelligence for stakeholders navigating the evolving semiconductor landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 90.0 Billion |

| Market Forecast in 2033 | USD 195.0 Billion |

| Growth Rate | 10.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Applied Materials, Inc., ASML Holding N.V., Lam Research Corporation, KLA Corporation, Tokyo Electron Limited (TEL), Hitachi High-Tech Corporation, SCREEN Holdings Co., Ltd., Teradyne Inc., Advantest Corporation, ASM International N.V., Disco Corporation, Daifuku Co., Ltd., Nikon Corporation, Canon Inc., Veeco Instruments Inc., Plasma-Therm, LLC, Kulicke & Soffa Industries, Inc., Onto Innovation Inc., Nordson Corporation, Edwards Vacuum |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The semiconductor equipment market is meticulously segmented to provide a granular understanding of its diverse components and dynamics. This segmentation is crucial for identifying specific growth areas, understanding technological shifts, and tailoring strategic investments. The primary categories include equipment type, which differentiates between the intricate processes involved in front-end wafer fabrication and the subsequent back-end assembly, packaging, and testing stages. Each sub-segment within these types, such as lithography, etching, deposition, or automatic test equipment, represents a specialized market with unique technological requirements and competitive landscapes.

Further segmentation by application highlights the key customer bases for semiconductor equipment, including independent foundries, integrated device manufacturers (IDMs), outsourced semiconductor assembly and test (OSAT) providers, and dedicated memory manufacturers. This categorization helps in understanding the varying demands and investment patterns across different business models within the semiconductor ecosystem. Lastly, the end-use industry segmentation provides insight into the ultimate drivers of chip demand, ranging from broad consumer electronics and automotive to specialized applications in telecommunications, data centers, healthcare, and industrial automation. This multi-dimensional segmentation allows for a comprehensive assessment of market opportunities and challenges across the entire semiconductor value chain.

- By Type:

- Front-End Equipment

- Wafer Fabrication Equipment (Lithography, Etch, Deposition, Ion Implantation, Polishing & Grinding, Thermal Processing, Cleaning, Metrology & Inspection)

- Back-End Equipment

- Assembly & Packaging Equipment (Dicing, Bonding, Encapsulation)

- Test Equipment (Automatic Test Equipment (ATE), Wafer Probers)

- Front-End Equipment

- By Application:

- Foundry

- Integrated Device Manufacturers (IDMs)

- Outsourced Semiconductor Assembly and Test (OSAT)

- Memory Manufacturers

- By End-Use Industry:

- Consumer Electronics

- Automotive

- Telecommunications

- Data Centers & Cloud Computing

- Healthcare

- Industrial

Regional Highlights

The global semiconductor equipment market exhibits significant regional disparities and strategic importance, with distinct characteristics shaping growth and investment. Asia Pacific (APAC) continues to dominate the market, primarily driven by robust investments in new fabrication facilities and capacity expansion in Taiwan, South Korea, and China. These countries are home to the world's largest chip manufacturers and foundry operations, making them the epicenter of demand for advanced manufacturing equipment. Japan also remains a critical player, particularly in specialized equipment and materials, owing to its strong legacy in precision engineering and high-quality manufacturing processes. The APAC region's relentless pursuit of technological leadership in chip production ensures its sustained position as the largest market for semiconductor equipment.

North America, particularly the United States, is undergoing a resurgence in domestic semiconductor manufacturing, fueled by government initiatives and strategic investments aimed at enhancing supply chain resilience and national security. This has led to substantial capital expenditure in new fabs and R&D facilities, creating significant demand for advanced equipment from both domestic and international suppliers. Europe is also strengthening its semiconductor ecosystem, with countries like Germany, France, and the Netherlands investing in advanced manufacturing and R&D capabilities. The region's focus on automotive electronics, industrial applications, and collaborative research initiatives, such as those related to next-generation lithography and materials, drives demand for specialized equipment and fosters innovation. These regional dynamics highlight a global shift towards a more distributed and diversified semiconductor manufacturing landscape.

- Asia Pacific (APAC): The largest and fastest-growing region, led by extensive fab expansions and technological leadership in Taiwan, South Korea, and China. Dominates demand for advanced wafer fab equipment.

- North America: Experiencing significant reshoring initiatives and substantial government investments, driving demand for new fab construction and advanced R&D equipment in the United States.

- Europe: Focused on strengthening domestic capabilities in specialty semiconductors, automotive electronics, and R&D, with notable investments in Germany, France, and the Netherlands.

- Japan: A key supplier of highly specialized equipment, materials, and components, and a significant market for advanced manufacturing tools for domestic fabs.

- Latin America and Middle East & Africa (MEA): Emerging markets with growing electronics manufacturing bases and increasing interest in developing localized semiconductor ecosystems, though currently smaller in market share.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Semiconductor Equipment Market.- Applied Materials, Inc.

- ASML Holding N.V.

- Lam Research Corporation

- KLA Corporation

- Tokyo Electron Limited (TEL)

- Hitachi High-Tech Corporation

- SCREEN Holdings Co., Ltd.

- Teradyne Inc.

- Advantest Corporation

- ASM International N.V.

- Disco Corporation

- Daifuku Co., Ltd.

- Nikon Corporation

- Canon Inc.

- Veeco Instruments Inc.

- Plasma-Therm, LLC

- Kulicke & Soffa Industries, Inc.

- Onto Innovation Inc.

- Nordson Corporation

- Edwards Vacuum

Frequently Asked Questions

What is the projected growth rate for the Semiconductor Equipment Market?

The Semiconductor Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2033, demonstrating a robust expansion driven by increasing demand for advanced chips.

How will AI impact the Semiconductor Equipment Market?

AI is set to significantly impact the market by enhancing manufacturing efficiency through process optimization and predictive maintenance, and by driving demand for specialized equipment to produce high-performance AI chips, fostering continuous innovation in tool design.

What are the primary drivers of the Semiconductor Equipment Market?

Key drivers include the exponential growth in AI, 5G, IoT, and high-performance computing, substantial global investments in new fabrication facilities, and the continuous advancement of complex packaging technologies like 3D integration.

What challenges does the Semiconductor Equipment Market face?

The market faces challenges such as the high costs associated with advanced R&D and manufacturing, the rapid pace of technological obsolescence, and vulnerabilities within the complex global supply chain, exacerbated by geopolitical tensions.

Which regions are key contributors to the Semiconductor Equipment Market?

Asia Pacific, particularly Taiwan, South Korea, and China, is the leading market due to extensive manufacturing investments. North America and Europe are also significant contributors, driven by strategic reshoring initiatives and R&D efforts in advanced technologies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted