Gypsum Board Market

Gypsum Board Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702456 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

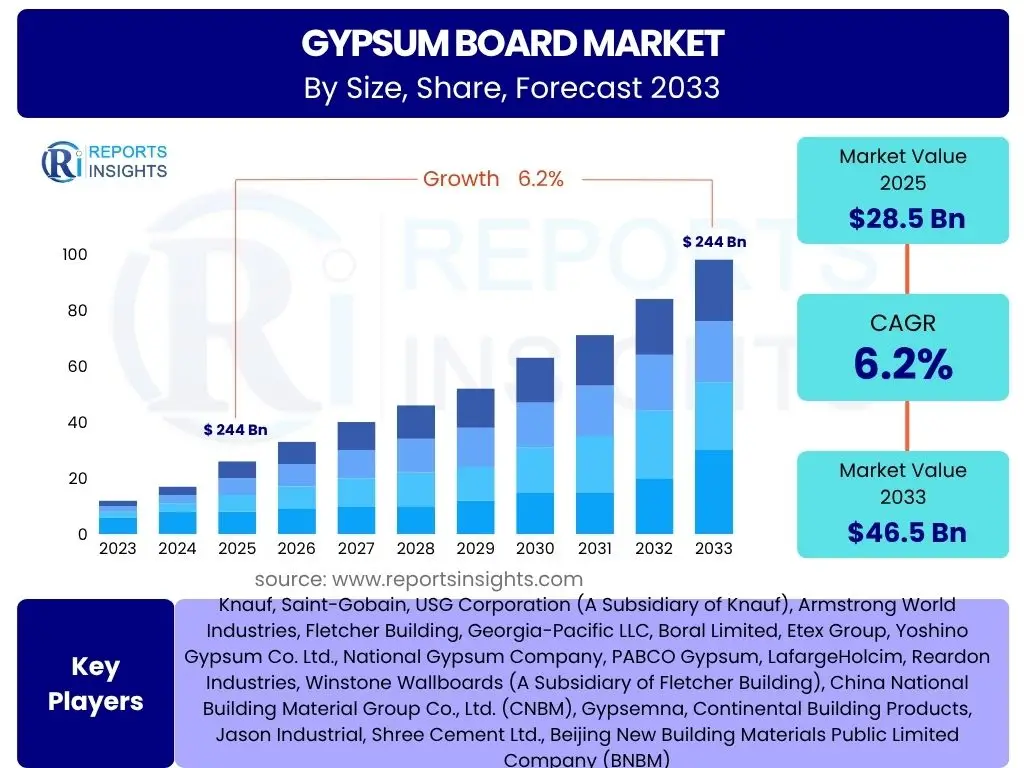

Gypsum Board Market Size

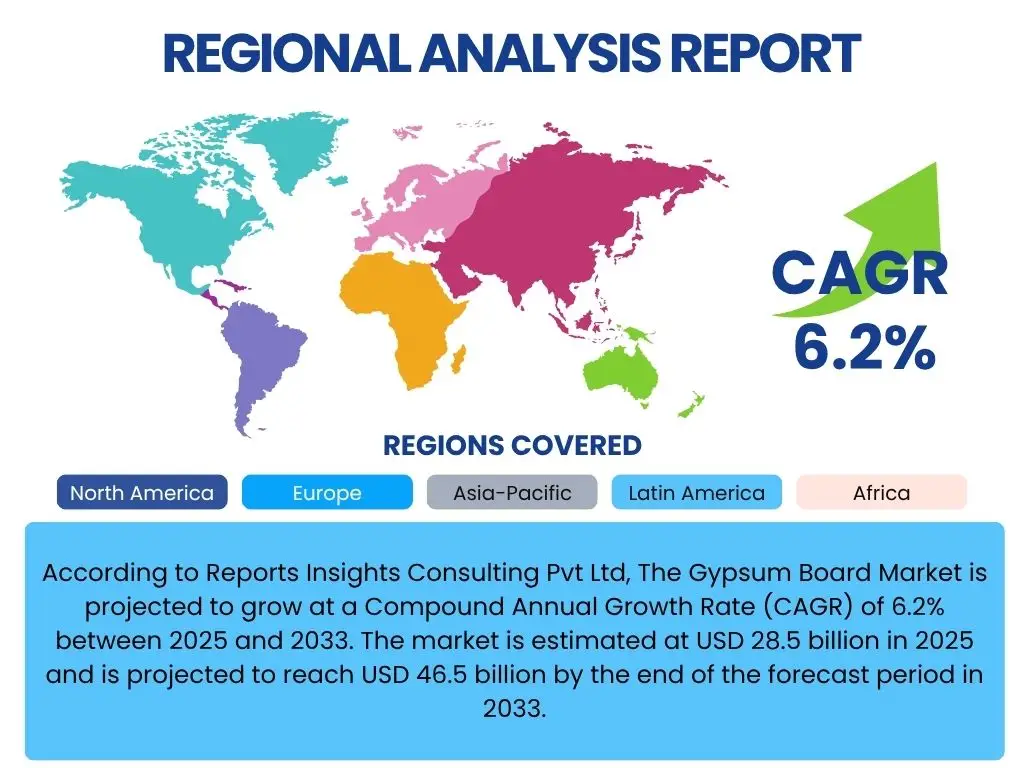

According to Reports Insights Consulting Pvt Ltd, The Gypsum Board Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.2% between 2025 and 2033. The market is estimated at USD 28.5 billion in 2025 and is projected to reach USD 46.5 billion by the end of the forecast period in 2033.

Key Gypsum Board Market Trends & Insights

The Gypsum Board market is experiencing significant shifts driven by evolving construction practices and increasing demand for sustainable and high-performance building materials. Users frequently inquire about the adoption of green building initiatives, the rise of modular and prefabricated construction techniques, and the integration of advanced functionalities such as enhanced fire resistance and sound insulation. Additionally, there is a growing interest in the impact of urbanization and infrastructure development projects, particularly in emerging economies, on the overall market trajectory.

Technological advancements in manufacturing processes, leading to more efficient production and improved product properties, are also prominent themes. The market is witnessing a move towards lighter, stronger, and more versatile gypsum board products. Furthermore, the increasing emphasis on interior aesthetics and innovative design in both residential and commercial spaces is influencing product development and market demand.

- Growing adoption of green building materials and sustainable construction practices.

- Increased demand for fire-resistant and moisture-resistant gypsum board variants.

- Rising urbanization and rapid infrastructure development in developing regions.

- Technological advancements in manufacturing processes leading to cost efficiencies and enhanced product quality.

- Preference for lightweight and easy-to-install building materials in modern construction.

- Expansion of the renovation and remodeling sector, driving demand for interior finishing materials.

AI Impact Analysis on Gypsum Board

Common user inquiries regarding the impact of Artificial Intelligence (AI) on the Gypsum Board market revolve around its potential to optimize manufacturing processes, enhance supply chain efficiency, and improve product quality. Users are particularly interested in how AI can facilitate predictive maintenance for machinery, automate quality control, and personalize product offerings to meet specific architectural or performance requirements. There is also curiosity about AI's role in construction site management, potentially streamlining the installation of gypsum boards and minimizing waste.

The integration of AI could lead to more intelligent design processes, where algorithms suggest optimal board layouts or material specifications for specific projects, considering factors like thermal efficiency and acoustic performance. Furthermore, AI-driven analytics can provide deeper insights into market demand, inventory management, and raw material sourcing, allowing manufacturers to respond more dynamically to market fluctuations. While initial adoption may present investment challenges, the long-term benefits in terms of operational efficiency and product innovation are a significant area of focus for industry stakeholders.

- Optimization of manufacturing processes through AI-driven predictive maintenance and automation, leading to reduced downtime and increased production efficiency.

- Enhanced supply chain management and logistics, with AI algorithms forecasting demand and optimizing inventory levels.

- Improved quality control and defect detection during production, ensuring higher product consistency and performance.

- Facilitation of generative design in architecture and construction, allowing for more efficient and customized gypsum board applications.

- Data-driven insights for market analysis, enabling manufacturers to better understand consumer preferences and tailor product development.

Key Takeaways Gypsum Board Market Size & Forecast

Analysis of user questions regarding key takeaways from the Gypsum Board market size and forecast reveals a strong interest in understanding the primary growth catalysts, the segments poised for the most significant expansion, and the regions that will dominate future market share. Users are keen to identify the underlying macroeconomic factors and specific construction trends contributing to the projected growth trajectory. There is also a focus on the role of regulatory frameworks and environmental considerations in shaping market dynamics.

The forecast indicates sustained growth driven by global construction boom, particularly in residential and commercial sectors. The increasing preference for durable, fire-resistant, and aesthetically versatile interior building materials is a consistent demand driver. Emerging economies are expected to be pivotal in market expansion due to rapid urbanization and infrastructure investments, while developed regions will focus on renovation and sustainable building practices. Innovation in product features, such as enhanced soundproofing and moisture resistance, will also play a crucial role in maintaining market momentum.

- The Gypsum Board market is set for robust growth, driven by an expanding global construction industry and increasing urbanization.

- Residential and commercial construction sectors will remain the primary demand generators, with a growing emphasis on interior finishing.

- Asia Pacific is anticipated to be the fastest-growing region, fueled by infrastructure development and housing demand.

- Product innovation focusing on multi-functionality (e.g., fire, moisture, and sound resistance) will be a key competitive differentiator.

- Sustainability initiatives and green building certifications are increasingly influencing purchasing decisions and product development.

Gypsum Board Market Drivers Analysis

The expansion of the global construction industry is a primary driver for the Gypsum Board market. Rapid urbanization, particularly in developing economies, has led to a significant increase in both residential and commercial building projects. Governments worldwide are investing heavily in infrastructure development, including public buildings, hospitals, and educational institutions, all of which utilize gypsum boards for interior finishes due to their versatility, ease of installation, and aesthetic appeal.

Furthermore, the growing emphasis on fire safety and sound insulation in modern building codes and consumer preferences is propelling the demand for specialized gypsum board products. Gypsum's inherent fire-resistant properties make it a preferred material, and ongoing advancements are leading to products with superior performance in fire ratings and acoustic dampening. The increasing trend of renovation and remodeling activities, especially in developed countries, also contributes significantly to market growth as property owners upgrade existing structures with modern, high-performance interior materials.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Urbanization and Construction Boom | +1.5% | Asia Pacific, Latin America, Middle East | 2025-2033 |

| Growing Demand for Fire-Resistant Materials | +1.2% | North America, Europe, Asia Pacific | 2025-2033 |

| Increasing Renovation and Remodeling Activities | +1.0% | North America, Europe | 2025-2030 |

| Government Initiatives for Affordable Housing | +0.8% | India, China, Southeast Asian Countries | 2025-2033 |

| Advancements in Building Technologies and Product Innovation | +0.7% | Global | 2025-2033 |

Gypsum Board Market Restraints Analysis

Despite robust growth, the Gypsum Board market faces certain restraints that could impact its expansion. Volatility in raw material prices, particularly for gypsum, paper, and various additives, can lead to increased production costs and exert pressure on profit margins for manufacturers. Economic downturns or slowdowns in the construction sector, often influenced by global economic conditions, interest rate fluctuations, or geopolitical instability, can directly reduce demand for building materials, including gypsum boards.

Furthermore, the availability of alternative building materials, such as plywood, fiber cement boards, and plaster, poses a competitive challenge to gypsum boards. While gypsum boards offer distinct advantages, these substitutes may sometimes be preferred for specific applications or due to cost considerations in certain regions. Environmental concerns associated with gypsum mining and the disposal of construction waste also present regulatory and public perception challenges, necessitating sustainable practices and recycling initiatives.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices | -0.7% | Global | 2025-2033 |

| Economic Slowdown and Construction Sector Fluctuations | -0.5% | Global, especially developed markets | 2025-2027 |

| Availability of Alternative Building Materials | -0.4% | Specific regional markets | 2025-2033 |

| Environmental Regulations and Disposal Challenges | -0.3% | Europe, North America | 2025-2033 |

Gypsum Board Market Opportunities Analysis

The Gypsum Board market presents significant opportunities for growth driven by product innovation and expanding applications. The development of advanced gypsum board types with enhanced properties, such as superior moisture resistance for wet areas, improved soundproofing for commercial and residential buildings, and mold-resistant variants for health-conscious constructions, opens up new market niches and increases adoption across diverse environments. These innovations address specific pain points in construction and contribute to overall building performance and longevity.

Moreover, the burgeoning demand for green and sustainable building materials globally offers a substantial opportunity for gypsum board manufacturers. As environmental awareness grows and stricter building codes promote eco-friendly construction, gypsum boards, particularly those made from recycled content or offering energy-efficient insulation properties, are well-positioned to capitalize on this trend. Emerging markets in Asia Pacific, Latin America, and Africa, with their rapid urbanization and infrastructure deficits, represent untapped potential for significant market expansion, driven by large-scale construction projects and increasing disposable incomes.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Product Innovation (e.g., moisture, sound, mold resistance) | +1.3% | Global | 2025-2033 |

| Growth in Green Building and Sustainable Construction | +1.0% | Europe, North America, Japan, Australia | 2025-2033 |

| Expansion into Emerging Markets and Untapped Regions | +0.9% | Africa, Southeast Asia, Latin America | 2025-2033 |

| Increasing Use in Prefabricated and Modular Construction | +0.7% | Global | 2025-2033 |

Gypsum Board Market Challenges Impact Analysis

The Gypsum Board market faces several challenges that require strategic responses from manufacturers. Intense competition among established players and the entry of new regional manufacturers can lead to price wars, compressing profit margins and necessitating continuous differentiation through product quality and innovation. Maintaining a robust and cost-effective supply chain is also a significant challenge, particularly given the global nature of raw material sourcing and the logistics involved in transporting bulky gypsum boards to diverse construction sites.

Furthermore, the market is subject to various regulatory hurdles related to building codes, environmental standards, and safety compliances, which vary by region and can add complexity and cost to manufacturing and distribution. The skilled labor shortage in the construction industry, especially for specialized installation techniques, can impede the efficient deployment of gypsum boards, potentially delaying projects and increasing overall construction costs. Addressing these challenges requires strategic investments in technology, sustainable practices, and workforce development.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Market Competition and Price Pressures | -0.6% | Global | 2025-2033 |

| Supply Chain Disruptions and Logistics Costs | -0.5% | Global | 2025-2028 |

| Stringent Building Codes and Environmental Regulations | -0.4% | Europe, North America | 2025-2033 |

| Skilled Labor Shortage in Construction Industry | -0.3% | North America, Europe, parts of Asia | 2025-2033 |

Gypsum Board Market - Updated Report Scope

This market research report provides a comprehensive analysis of the Gypsum Board market, offering in-depth insights into its size, growth drivers, restraints, opportunities, and challenges across various segments and key regions. The scope encompasses detailed historical data from 2019 to 2023, coupled with robust forecasts extending from 2025 to 2033, enabling a thorough understanding of market dynamics and future trajectories. The report also highlights the competitive landscape, profiles key industry players, and identifies emerging trends that will shape the market's evolution.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 28.5 billion |

| Market Forecast in 2033 | USD 46.5 billion |

| Growth Rate | 6.2% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Knauf, Saint-Gobain, USG Corporation (A Subsidiary of Knauf), Armstrong World Industries, Fletcher Building, Georgia-Pacific LLC, Boral Limited, Etex Group, Yoshino Gypsum Co. Ltd., National Gypsum Company, PABCO Gypsum, LafargeHolcim, Reardon Industries, Winstone Wallboards (A Subsidiary of Fletcher Building), China National Building Material Group Co., Ltd. (CNBM), Gypsemna, Continental Building Products, Jason Industrial, Shree Cement Ltd., Beijing New Building Materials Public Limited Company (BNBM) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Gypsum Board market is meticulously segmented to provide a granular understanding of its diverse components and their respective growth trajectories. This segmentation allows for precise market sizing and forecasting, identifying key areas of demand and opportunities for product differentiation. The classification by type reflects the evolving needs of modern construction, moving beyond standard boards to specialized products offering enhanced performance attributes such as fire, moisture, and sound resistance.

Further segmentation by application highlights the primary structural components where gypsum boards are utilized, including walls, ceilings, and partitions, each with unique requirements and installation methods. The end-use sector categorization delineates demand from residential, commercial, and industrial constructions, further broken down into new builds and renovation projects. This multi-layered segmentation ensures a comprehensive view of market dynamics across various consumer and industry verticals.

- By Type:

- Regular Gypsum Board

- Type X (Fire-Resistant) Gypsum Board

- Type C (Fire & Moisture Resistant) Gypsum Board

- Water-Resistant Gypsum Board

- Soundproof Gypsum Board

- Moisture-Resistant Gypsum Board

- Mold-Resistant Gypsum Board

- By Application:

- Walls

- Ceilings

- Partitions

- By End-Use Sector:

- Residential

- New Construction

- Renovation & Repair

- Commercial

- Office Spaces

- Retail

- Hospitality

- Healthcare

- Educational Institutions

- Industrial

- Residential

Regional Highlights

- Asia Pacific (APAC): Expected to be the fastest-growing region due to rapid urbanization, significant infrastructure development, and a booming residential construction sector, especially in countries like China, India, and Southeast Asian nations. Increased foreign direct investment in commercial projects further boosts demand.

- North America: A mature market characterized by stringent building codes, a strong emphasis on sustainable construction, and a robust renovation and remodeling sector. Demand is driven by the adoption of high-performance gypsum boards for enhanced fire safety and acoustic properties, particularly in the United States and Canada.

- Europe: Exhibits steady growth fueled by renovation activities, adherence to strict energy efficiency standards, and increasing adoption of lightweight and prefabricated building solutions. Germany, France, and the UK are key contributors, with a focus on green building certifications and sound insulation.

- Latin America: Demonstrates emerging growth potential driven by increasing construction activities in developing economies like Brazil, Mexico, and Argentina. Government initiatives for affordable housing and growing foreign investments in commercial infrastructure contribute to market expansion.

- Middle East and Africa (MEA): Projected to witness substantial growth due to mega-projects in the construction sector, including new cities, hospitality, and commercial complexes, particularly in the UAE, Saudi Arabia, and Qatar. Growing population and infrastructure development efforts also drive market demand.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Gypsum Board Market.- Knauf

- Saint-Gobain

- USG Corporation (A Subsidiary of Knauf)

- Armstrong World Industries

- Fletcher Building

- Georgia-Pacific LLC

- Boral Limited

- Etex Group

- Yoshino Gypsum Co. Ltd.

- National Gypsum Company

- PABCO Gypsum

- LafargeHolcim

- Reardon Industries

- Winstone Wallboards (A Subsidiary of Fletcher Building)

- China National Building Material Group Co., Ltd. (CNBM)

- Gypsemna

- Continental Building Products

- Jason Industrial

- Shree Cement Ltd.

- Beijing New Building Materials Public Limited Company (BNBM)

Frequently Asked Questions

What is the current market size of the Gypsum Board industry?

The Gypsum Board market is estimated at USD 28.5 billion in 2025, reflecting its significant role in the global construction sector.

What is the projected growth rate for the Gypsum Board market?

The Gypsum Board market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.2% between 2025 and 2033, reaching USD 46.5 billion by 2033.

Which regions are driving the growth of the Gypsum Board market?

Asia Pacific, particularly countries like China and India, is a primary growth driver due to rapid urbanization and infrastructure development, while North America and Europe show steady demand from renovation and specialized product adoption.

What are the key trends influencing the Gypsum Board market?

Major trends include the increasing demand for fire-resistant and moisture-resistant boards, the growth of green building initiatives, urbanization, and advancements in manufacturing technologies enhancing product performance.

What are the main applications of Gypsum Boards?

Gypsum boards are primarily used for interior applications such as walls, ceilings, and partitions in both residential and commercial buildings, including offices, retail spaces, healthcare facilities, and educational institutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted