Semiconductor Backend Equipment Market

Semiconductor Backend Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709898 | Last Updated : December 22, 2025 |

Format : ![]()

![]()

![]()

![]()

Semiconductor Backend Equipment Market Size

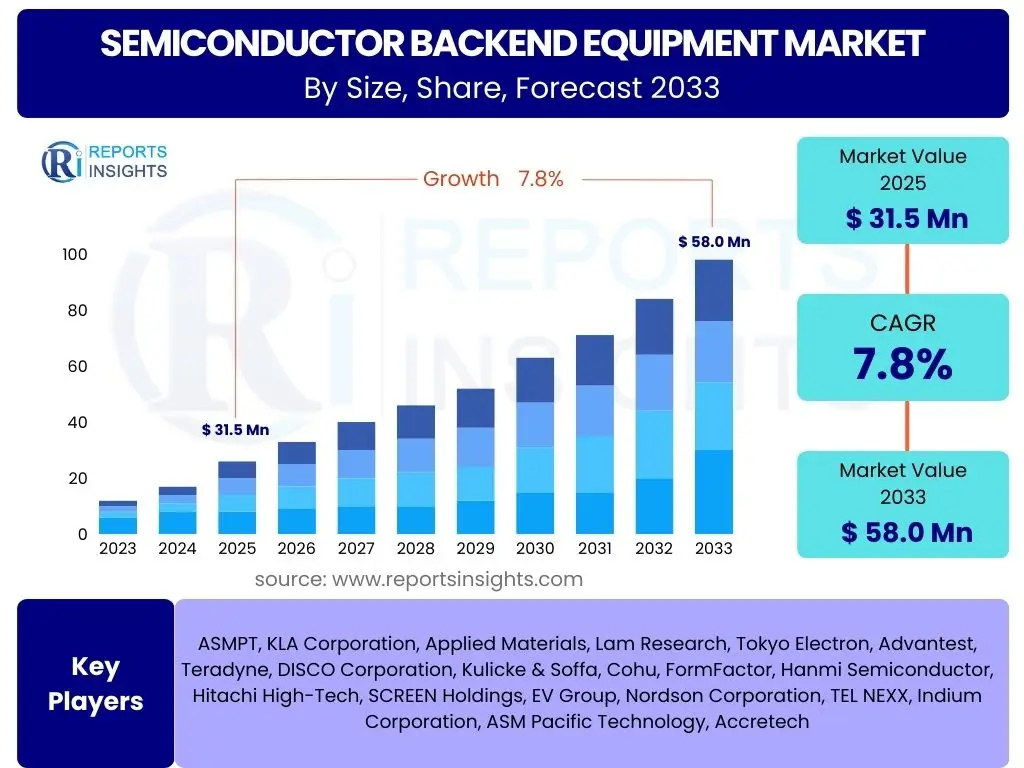

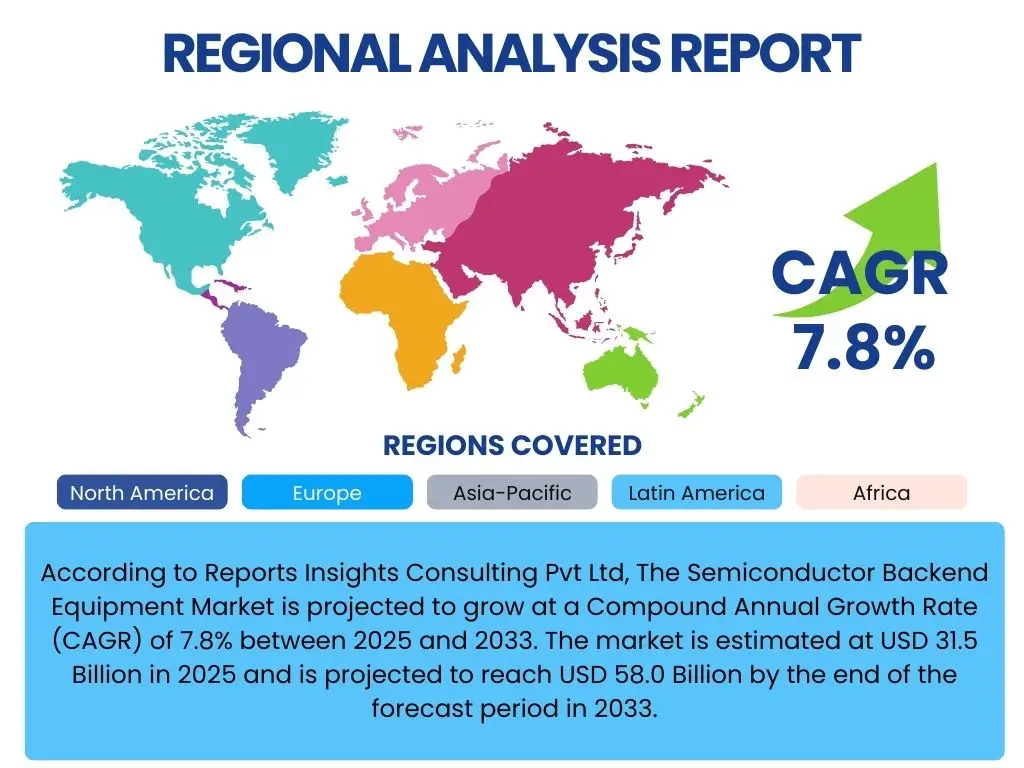

According to Reports Insights Consulting Pvt Ltd, The Semiconductor Backend Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 31.5 Billion in 2025 and is projected to reach USD 58.0 Billion by the end of the forecast period in 2033.

Key Semiconductor Backend Equipment Market Trends & Insights

The semiconductor backend equipment market is undergoing significant transformation driven by the escalating demand for advanced electronic devices and the continuous pursuit of miniaturization and enhanced performance. Industry stakeholders are keenly observing shifts towards heterogeneous integration, sophisticated packaging technologies, and increased automation, all of which are critical for processing the next generation of semiconductors. User inquiries frequently highlight the need for equipment capable of handling complex geometries, diverse material sets, and higher throughput, reflecting a market moving beyond traditional packaging to more integrated and high-density solutions. This evolution is not merely about scaling down; it is about creating multi-functional, high-performance computing platforms within increasingly constrained physical footprints.

Furthermore, the market's trajectory is heavily influenced by geopolitical factors and the imperative for resilient supply chains. Manufacturers are exploring localized production capabilities and robust partnerships to mitigate risks associated with global disruptions, a concern frequently voiced by industry participants. The emphasis on smart manufacturing, predictive maintenance, and data-driven decision-making processes is also gaining prominence, indicating a strategic shift towards operational efficiency and cost optimization. These trends collectively underscore a dynamic environment where technological innovation, operational agility, and strategic foresight are paramount for market leadership and sustained growth.

- Advanced Packaging Adoption: Growing demand for 2.5D, 3D ICs, SiP, and fan-out WLP drives equipment innovation.

- Miniaturization and Heterogeneous Integration: Focus on smaller form factors and combining diverse components on a single package.

- Automation and Industry 4.0: Increased integration of robotics, AI, and IoT for enhanced efficiency and yield.

- Supply Chain Resilience: Regionalization of manufacturing and diversified sourcing strategies to mitigate geopolitical risks.

- Sustainability Initiatives: Development of energy-efficient equipment and processes to reduce environmental impact.

AI Impact Analysis on Semiconductor Backend Equipment

The integration of Artificial Intelligence (AI) is profoundly reshaping the semiconductor backend equipment landscape, addressing critical user concerns regarding process optimization, yield enhancement, and predictive capabilities. Users are increasingly seeking solutions that leverage AI for tasks such as automated visual inspection, real-time process control, and adaptive manufacturing, moving beyond traditional rule-based systems. AI algorithms can analyze vast datasets generated during assembly and test phases, identifying anomalies and predicting potential failures with unprecedented accuracy, thereby reducing defects and improving overall equipment effectiveness (OEE). This capability is crucial for managing the complexity of advanced packaging, where even minute variations can significantly impact device performance and reliability.

Furthermore, AI-driven solutions are enabling a new paradigm in equipment maintenance and operational efficiency. Predictive maintenance, powered by machine learning models, allows for the anticipation of equipment failures before they occur, minimizing downtime and optimizing maintenance schedules. This directly addresses user expectations for higher uptime and lower operational costs. Generative AI, while nascent, holds promise for optimizing equipment design parameters and simulating complex assembly processes, potentially accelerating the development cycle for new backend tools. The shift towards AI-powered intelligent equipment signifies a major leap in operational autonomy and responsiveness, catering to the industry's demand for smarter, more efficient, and more reliable manufacturing processes.

- Enhanced Process Control: AI optimizes parameters for die bonding, wire bonding, and dicing, improving precision and yield.

- Predictive Maintenance: Machine learning algorithms forecast equipment failures, minimizing downtime and extending operational life.

- Automated Visual Inspection: AI-powered vision systems detect microscopic defects faster and more accurately than human inspection.

- Adaptive Manufacturing: Equipment can dynamically adjust to variations in materials and environmental conditions, increasing flexibility.

- Design Optimization: AI assists in simulating and refining equipment designs for improved performance and energy efficiency.

Key Takeaways Semiconductor Backend Equipment Market Size & Forecast

The Semiconductor Backend Equipment market is poised for robust expansion, driven by foundational shifts in technology and consumer demand for sophisticated electronic devices. A critical takeaway is the sustained growth trajectory, with the market projected to nearly double in value by 2033, underscoring the indispensable role of backend processes in modern electronics manufacturing. This growth is intrinsically linked to the proliferation of 5G, IoT, AI, and high-performance computing, all of which necessitate advanced packaging and rigorous testing methodologies. Stakeholders observing this market should recognize the increasing capital expenditure required to keep pace with innovation, as investment in cutting-edge equipment becomes a competitive differentiator.

Another significant insight revolves around the strategic importance of regional manufacturing hubs, particularly in Asia Pacific, which continues to dominate in both production and consumption. The forecast highlights opportunities for equipment manufacturers to innovate in areas like heterogeneous integration and automated testing, which are becoming bottlenecks in the semiconductor value chain. Companies that can offer solutions for reducing total cost of ownership, improving yield, and enhancing automation will be strategically positioned for success. The market's resilience despite macroeconomic fluctuations also signals its foundational criticality, making it an attractive sector for sustained investment and technological development over the forecast period.

- Strong Market Growth: Projected CAGR of 7.8% indicates significant expansion through 2033.

- Technology-Driven Demand: Growth fueled by 5G, AI, IoT, and high-performance computing requiring advanced backend processes.

- Investment in Advanced Packaging: Heterogeneous integration and 3D stacking are key areas for capital expenditure.

- Automation Imperative: Increased adoption of fully automated solutions for efficiency and precision.

- Asia Pacific Dominance: Region remains the primary hub for both manufacturing and demand.

Semiconductor Backend Equipment Market Drivers Analysis

The semiconductor backend equipment market is experiencing substantial growth propelled by several interconnected factors that are fundamentally reshaping the global electronics industry. A primary driver is the accelerating demand for advanced packaging technologies, such as 2.5D, 3D, System-in-Package (SiP), and Fan-Out Wafer Level Packaging (FoWLP). These innovations are essential for achieving higher integration density, improved electrical performance, and reduced form factors in next-generation electronic devices, spanning consumer electronics to high-performance computing. As front-end scaling slows, backend processes become critical for performance enhancement, pushing manufacturers to invest heavily in sophisticated dicing, bonding, and inspection equipment capable of handling these complex architectures. This shift represents a significant capital injection into the backend segment, as existing equipment often cannot meet the stringent requirements of new packaging designs.

Furthermore, the global rollout of 5G technology and the exponential expansion of the Internet of Things (IoT) ecosystem are generating unprecedented demand for semiconductor devices. These applications require a massive number of interconnected chips, many of which are specialized and designed for low power consumption and robust connectivity. Consequently, there is a surge in demand for efficient, high-volume backend equipment that can process a diverse range of chip types for various applications, from smart home devices and wearables to industrial sensors and autonomous vehicles. The automotive sector, in particular, is undergoing a profound transformation with the rise of electric vehicles (EVs) and advanced driver-assistance systems (ADAS), both of which rely on high-reliability, high-performance semiconductors. This necessitates a corresponding upgrade in backend manufacturing capabilities to ensure the quality and durability of chips used in safety-critical applications, further fueling equipment sales.

The relentless pursuit of AI and Machine Learning (ML) capabilities across industries also serves as a potent driver. AI chips, whether designed for training in data centers or inference at the edge, demand bespoke packaging and rigorous testing to ensure optimal performance and energy efficiency. This often involves highly customized backend processes that require specialized equipment for precise assembly, thermal management, and comprehensive functional testing. Additionally, the ongoing digital transformation, accelerated by trends like cloud computing and big data analytics, continues to drive the need for faster, more powerful processors. These macro trends collectively underscore a vibrant market environment where continuous innovation in semiconductor backend equipment is not just an advantage, but an absolute necessity to meet the evolving demands of the digital age.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Advanced Packaging | +2.5% | Global, particularly APAC (Taiwan, South Korea) | Mid-term to Long-term (3-8 years) |

| Proliferation of 5G and IoT Devices | +1.8% | Global, particularly APAC, North America, Europe | Short-term to Mid-term (1-5 years) |

| Growth in Automotive Electronics and EVs | +1.5% | Europe, North America, APAC (China, Japan) | Mid-term to Long-term (3-8 years) |

| Rising Adoption of AI and High-Performance Computing | +1.2% | Global, particularly North America, APAC | Mid-term (3-5 years) |

| Miniaturization and Heterogeneous Integration Trends | +0.8% | Global | Long-term (5-8 years) |

Semiconductor Backend Equipment Market Restraints Analysis

Despite the robust growth drivers, the semiconductor backend equipment market faces several significant restraints that could temper its expansion. One prominent challenge is the extremely high capital expenditure required for advanced backend equipment. The development and procurement of state-of-the-art dicing, bonding, and testing machinery involve substantial financial investments, often running into millions of dollars per unit. This high entry barrier can deter new players and limit the ability of smaller companies to upgrade their facilities, potentially leading to slower adoption rates for the latest technologies. Furthermore, the rapid pace of technological obsolescence means that current generation equipment can quickly become outdated, necessitating frequent and costly upgrades that strain manufacturers' budgets and impact profitability.

Another critical restraint is the ongoing geopolitical tensions and trade disputes, particularly those involving major semiconductor manufacturing regions and technology suppliers. These tensions can lead to supply chain disruptions, restrictions on equipment sales, and increased uncertainty for market participants. The push for localized supply chains, while offering resilience, can also fragment the market and increase manufacturing costs in regions that lack established infrastructure and expertise. Moreover, the industry is heavily reliant on a highly skilled workforce, encompassing engineers, technicians, and researchers proficient in microelectronics, materials science, and automation. A persistent shortage of such specialized talent, particularly in emerging economies with ambitious semiconductor goals, can hinder manufacturing expansion and limit the effective utilization of advanced backend equipment, impacting overall market growth and efficiency.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure and R&D Costs | -1.5% | Global | Short-term to Long-term (1-8 years) |

| Geopolitical Tensions and Supply Chain Disruptions | -1.0% | Global, particularly APAC, North America | Mid-term (3-5 years) |

| Rapid Technological Obsolescence | -0.8% | Global | Short-term to Mid-term (1-5 years) |

| Skilled Labor Shortage | -0.7% | Global | Mid-term to Long-term (3-8 years) |

Semiconductor Backend Equipment Market Opportunities Analysis

The semiconductor backend equipment market presents numerous opportunities for growth and innovation, driven by evolving technological landscapes and unmet industry needs. A significant opportunity lies in the burgeoning demand from emerging markets, particularly in Southeast Asia and India, which are increasingly establishing their own semiconductor manufacturing capabilities. As these regions expand their electronics production and aim for greater self-sufficiency, there will be substantial investment in backend infrastructure and equipment. This creates a fertile ground for equipment manufacturers to expand their sales and service networks, offering tailored solutions that address the specific cost structures and operational requirements of these developing markets, potentially unlocking new revenue streams and market share.

Another key area of opportunity stems from the continuous innovation in materials science and process technologies for advanced packaging. As traditional silicon scaling approaches reach their physical limits, the industry is exploring novel materials and integration techniques to enhance performance and functionality. This includes developments in advanced substrates, bonding materials, and thermal interface materials, all of which necessitate specialized backend equipment capable of handling these new properties with precision. Equipment manufacturers that invest in research and development to align with these material advancements, offering compatible and optimized tools, will gain a significant competitive edge. Furthermore, the growing emphasis on customization and flexible manufacturing for diverse product portfolios presents an opportunity for developing modular, reconfigurable backend equipment that can adapt quickly to changing production requirements, catering to both high-volume standardized production and low-volume highly specialized applications.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion in Emerging Markets | +1.5% | APAC (India, Southeast Asia) | Mid-term to Long-term (3-8 years) |

| Development of Advanced Materials and Processes | +1.2% | Global | Long-term (5-8 years) |

| Customization and Flexible Manufacturing Solutions | +1.0% | Global | Mid-term (3-5 years) |

| Integration of AI/ML for Predictive Manufacturing | +0.9% | Global | Short-term to Mid-term (1-5 years) |

Semiconductor Backend Equipment Market Challenges Impact Analysis

The semiconductor backend equipment market, despite its growth prospects, confronts several formidable challenges that demand strategic responses from industry players. One significant challenge is the intensely competitive landscape, characterized by a few dominant players and a multitude of niche specialists. This high level of competition often leads to price pressures, reduced profit margins, and increased investment in R&D just to maintain market share. Equipment manufacturers must continuously innovate and differentiate their offerings, which can be costly and time-consuming, especially when catering to the rapidly evolving demands of semiconductor foundries and integrated device manufacturers (IDMs). The need to balance innovation with cost-effectiveness remains a perpetual struggle in this environment.

Another critical challenge is the inherent technical complexity and stringent performance requirements for modern backend processes. As semiconductor devices become smaller and more integrated, the precision and reliability demanded from backend equipment reach extreme levels. This includes achieving nanometer-scale accuracy in dicing, micron-level alignment in bonding, and comprehensive defect detection in inspection systems. Developing and maintaining equipment that consistently meets these exacting standards, especially for advanced packaging architectures like 3D ICs and heterogeneous integration, requires significant engineering expertise and robust quality control. Failure to meet these technical benchmarks can lead to substantial yield losses for chip manufacturers, making reliability a paramount concern. Furthermore, the industry faces increasing environmental regulations and sustainability pressures, which necessitate investments in eco-friendly equipment design and processes, adding another layer of complexity and cost.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition and Price Pressure | -1.2% | Global | Short-term to Mid-term (1-5 years) |

| Technical Complexity and Performance Requirements | -1.0% | Global | Mid-term to Long-term (3-8 years) |

| Rapid Technological Cycles and Obsolescence | -0.9% | Global | Short-term (1-3 years) |

| Environmental Regulations and Sustainability Demands | -0.6% | Europe, North America, APAC | Mid-term to Long-term (3-8 years) |

Semiconductor Backend Equipment Market - Updated Report Scope

This report offers a comprehensive analysis of the global Semiconductor Backend Equipment Market, detailing its size, growth trajectory, key trends, and future projections. It provides an in-depth examination of market drivers, restraints, opportunities, and challenges, along with a thorough segmentation analysis across various equipment types, packaging technologies, applications, and regional landscapes. The scope includes a detailed impact assessment of AI on manufacturing processes and an identification of leading market players, offering strategic insights for stakeholders to navigate the evolving industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 31.5 Billion |

| Market Forecast in 2033 | USD 58.0 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ASMPT, KLA Corporation, Applied Materials, Lam Research, Tokyo Electron, Advantest, Teradyne, DISCO Corporation, Kulicke & Soffa, Cohu, FormFactor, Hanmi Semiconductor, Hitachi High-Tech, SCREEN Holdings, EV Group, Nordson Corporation, TEL NEXX, Indium Corporation, ASM Pacific Technology, Accretech |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Semiconductor Backend Equipment Market is meticulously segmented to provide a granular view of its diverse components and growth opportunities. This detailed analysis helps in understanding the specific drivers and challenges impacting each segment, allowing for targeted strategic planning and investment. The segmentation encompasses various equipment types crucial for backend processes, a wide array of packaging technologies that define modern chip architectures, key application areas dictating end-user demand, and the level of automation employed in manufacturing.

- By Equipment Type: Die Bonder, Wire Bonder, Dicing Equipment, Inspection Systems, Test Handlers, Metrology Equipment, Advanced Packaging Equipment.

- By Packaging Type: Flip Chip, Wafer Level Packaging (WLP), 3D Stacking, System-in-Package (SiP), Fan-out Wafer Level Packaging (FoWLP), Through-Silicon Via (TSV).

- By Application: Consumer Electronics, Automotive, Industrial, Healthcare, Telecommunications, Data Centers, Military & Defense.

- By Operation Type: Fully Automatic, Semi-Automatic.

Regional Highlights

- Asia Pacific (APAC): Dominates the market due to the presence of major semiconductor foundries and OSAT (Outsourced Semiconductor Assembly and Test) providers in Taiwan, South Korea, China, and Japan. Significant investments in new fabs and advanced packaging technologies are further bolstering its leadership.

- North America: A key region for research and development, especially in high-performance computing, AI, and defense applications. The region demonstrates strong demand for advanced testing and inspection equipment.

- Europe: Focuses on specialized applications such as automotive electronics, industrial automation, and power semiconductors. Germany and the Netherlands are notable for their contributions to equipment innovation and manufacturing.

- Latin America: An emerging market with growing electronics manufacturing, presenting opportunities for incremental growth in backend equipment, particularly for consumer electronics and automotive assembly.

- Middle East and Africa (MEA): Currently a smaller market, but with strategic governmental initiatives in digital transformation and technological infrastructure development, it shows potential for long-term growth in localized assembly and testing.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Semiconductor Backend Equipment Market.- ASMPT

- KLA Corporation

- Applied Materials

- Lam Research

- Tokyo Electron

- Advantest

- Teradyne

- DISCO Corporation

- Kulicke & Soffa

- Cohu

- FormFactor

- Hanmi Semiconductor

- Hitachi High-Tech

- SCREEN Holdings

- EV Group

- Nordson Corporation

- TEL NEXX

- Indium Corporation

- ASM Pacific Technology

- Accretech

Frequently Asked Questions

Analyze common user questions about the Semiconductor Backend Equipment market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Semiconductor Backend Equipment market?

The Semiconductor Backend Equipment market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033, reaching an estimated USD 58.0 Billion by 2033.

What are the primary drivers propelling the Semiconductor Backend Equipment market?

Key drivers include the increasing demand for advanced packaging technologies, the widespread adoption of 5G and IoT devices, significant growth in automotive electronics and electric vehicles, and the rising global adoption of AI and high-performance computing.

How is AI impacting the Semiconductor Backend Equipment industry?

AI is significantly impacting the industry by enabling enhanced process control, predictive maintenance for machinery, advanced automated visual inspection systems, and adaptive manufacturing capabilities, ultimately leading to improved efficiency, yield, and reliability.

Which regions are expected to exhibit significant growth in the Semiconductor Backend Equipment market?

The Asia Pacific region is expected to maintain its dominance and exhibit significant growth, driven by substantial investments in semiconductor manufacturing and advanced packaging in countries like Taiwan, South Korea, and China.

Who are the leading companies in the Semiconductor Backend Equipment market?

Leading companies include ASMPT, KLA Corporation, Applied Materials, Lam Research, Tokyo Electron, Advantest, Teradyne, DISCO Corporation, Kulicke & Soffa, and Cohu, among others, driving innovation and market competition.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted